股价新高,但存储股的估值仍在洼地

- Quan điểm chính: Nhu cầu AI đã biến chip nhớ từ một mặt hàng theo chu kỳ thành “hàng xa xỉ” có khả năng định giá và lợi nhuận bền vững, khiến giá cổ phiếu và lợi nhuận của các ông lớn ngành nhớ như Micron tăng vọt. Tuy nhiên, thị trường vẫn áp dụng khung định giá cũ, khiến tỷ lệ P/E forward của họ thấp hơn nhiều so với các mắt xích khác trong chuỗi AI, khiến định giá có vẻ "rẻ".

- Các yếu tố then chốt:

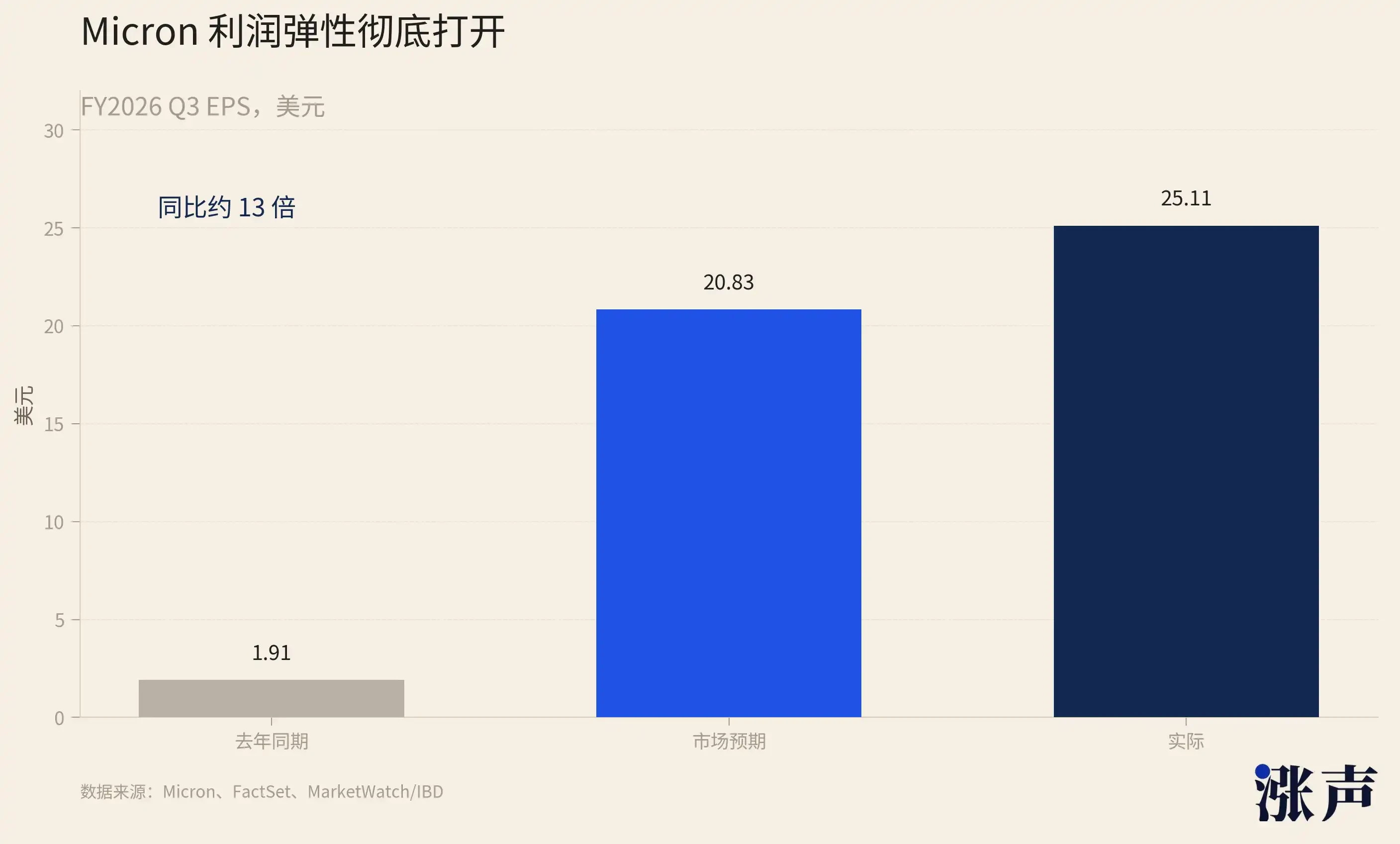

- Báo cáo tài chính Q3 FY2026 của Micron vượt kỳ vọng, với doanh thu 41,46 tỷ USD, hướng dẫn biên lợi nhuận gộp đạt 86%, cổ phiếu tăng 13% sau giờ giao dịch, vốn hóa thị trường vượt 1,16 nghìn tỷ USD, cho thấy xu hướng tăng giá chip nhớ vẫn chưa dừng lại.

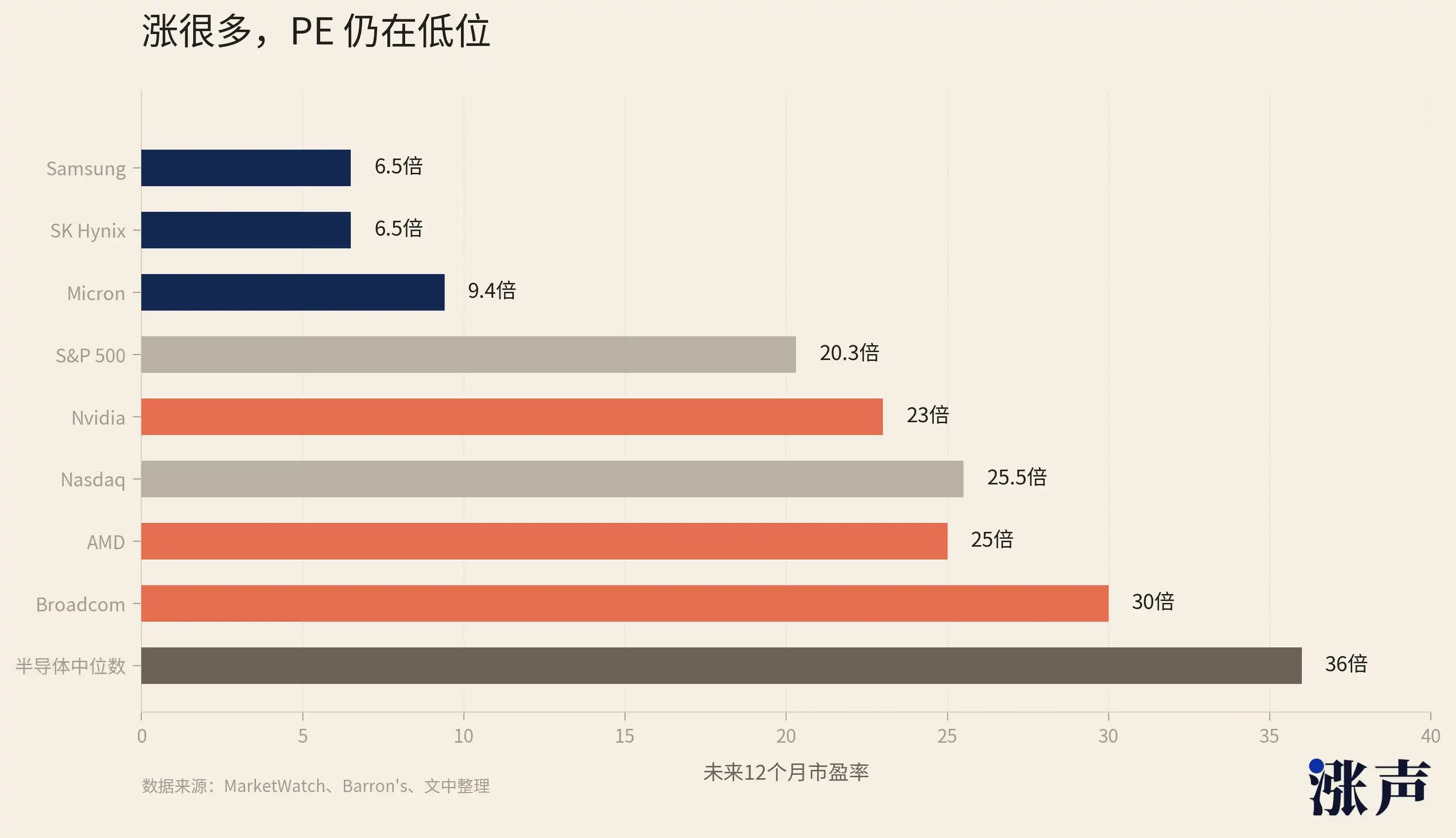

- Mặc dù giá cổ phiếu của Micron và các cổ phiếu ngành nhớ khác đã tăng rất mạnh trong năm qua (ví dụ Micron tăng hơn 850%), tỷ lệ P/E forward của chúng chỉ khoảng 9-10 lần, thấp hơn nhiều so với NVIDIA (23 lần) và mức trung vị của ngành bán dẫn (36 lần), cho thấy tốc độ tăng trưởng lợi nhuận nhanh hơn giá cổ phiếu.

- Nhu cầu HBM đã phá vỡ quy luật lịch sử chi phí DRAM giảm một nửa sau mỗi 5 năm. Các nhà sản xuất chuyển hướng năng lực sản xuất sang HBM có lợi nhuận cao, dẫn đến tình trạng thiếu hụt nguồn cung mang tính cấu trúc liên tục, giá DRAM đã tăng trong 8 quý liên tiếp.

- Khoảng cách cung-cầu chip NAND còn cứng nhắc hơn, do giá giảm mạnh trong giai đoạn 2022-2023 khiến các nhà sản xuất không mở rộng sản xuất trong nhiều năm, và nhu cầu SSD doanh nghiệp bùng nổ nhờ suy luận AI và sự thay thế HDD, công suất năm 2026 đã được bán hết.

- Mùa báo cáo tài chính của toàn bộ ngành lưu trữ sắp diễn ra dày đặc (TSMC, Samsung, SK Hynix, Western Digital...). Hướng dẫn mạnh mẽ của Micron đặt ra tông màu cho xu hướng ngành, đặc biệt HBM4 và NAND sẽ là tâm điểm chú ý.

Original author: Jialiu

Today, Micron delivered a historic earnings report that boosted confidence across the entire semiconductor sector.

FY2026 Q3 revenue reached $41.46 billion, exceeding market expectations by nearly $6 billion. A memory company, labeled a "low-margin commodity" for decades, posted a gross margin guidance comparable to a software company. Its stock surged 13% to 14% in after-hours trading, pushing its market cap to $1.16 trillion.

Micron's gains this year have already been remarkable. Closing at $1,211.38 on June 22, the stock has more than tripled year-to-date and surged over 850% in the past 12 months, making it the third-best performer in the S&P 500 for 2026, behind SanDisk and Western Digital, also memory companies. The entire sector is rising on this scale. SK Hynix has gained over 800% in the past 52 weeks, while Samsung is up over 400%.

With such a rally, many people's first reaction is, of course, "It's too expensive." But in reality, a high stock price doesn't necessarily mean expensive valuation. From many perspectives, memory remains a very "cheap" hot sector.

Stock Price Up 9x, Yet PE Stays Flat

One of the most common indicators to judge whether a company's stock is expensive or cheap is PE, the price-to-earnings ratio.

Simply put, PE measures how much the market is willing to pay for each dollar of profit a company earns. A PE of 10 means investors are willing to pay $10 for every $1 of annual profit. A high PE typically indicates the market expects strong future growth; a low PE might suggest the stock is cheap, or that the market believes the current profit is just a cyclical peak destined to fall soon.

Here lies the most counterintuitive part about memory stocks right now: stock prices have risen significantly, but PE ratios remain low.

According to FactSet data highlighted in a mid-June MarketWatch report, Micron's forward 12-month PE was around 9 times, while SK Hynix and Samsung were around 6.5 times. Barron's estimated Micron's forward PE at about 9.74 times, compared to the Nasdaq Composite's ~25.5 times and the S&P 500's ~20.3 times. GuruFocus data from June 21 showed Micron's forward PE at 9.90 times, SK Hynix's at 5.92 times (late May data), and Samsung's at approximately 5.45 times.

In other words, most data sources suggest the forward PEs of the memory Big Three are all in the single digits to low teens.

Across the entire AI industry chain, these numbers are among the lowest tier.

Nvidia's forward PE is around 23 times, Broadcom's around 30 times, AMD's around 25 times, and TSMC's around 20 times. The median PE for the overall semiconductor industry is around 36 times. In other words, the valuation of the memory Big Three is roughly one-third of Nvidia's and about one-quarter of the semiconductor industry median.

Ironically, however, the money in the AI industry is increasingly flowing into the memory segment.

AI servers aren't just about GPUs. Every high-end AI accelerator needs HBM, every inference server needs large-capacity DRAM, and KV cache, model weights, local cache, and data throughput are all inseparable from SSDs. Without HBM, there are no GPU training clusters; without server DRAM, no inference clusters; without high-capacity NAND, the storage and caching costs for AI applications cannot be reduced.

Memory is no longer just an ordinary component in the AI supply chain; it's a physical bottleneck that all AI capital expenditures must contend with. One number from Micron's recent earnings report illustrates this clearly: single-quarter data center revenue of $25 billion, with enterprise SSD revenue reaching $5 billion, accounting for 20% of data center revenue.

It's evident that this bottleneck is now even starting to impact consumer electronics.

AI data centers have pushed up the capacity and prices of HBM, DRAM, and NAND, ultimately forcing even terminal companies with strong bargaining power like Apple to face cost pressures and pass some of the price increases onto consumers. In the past, when discussing who makes money from AI, the immediate answer was Nvidia. But now it's increasingly clear that a significant portion of the AI bill is flowing to memory manufacturers.

Memory stocks have indeed risen a lot in price, but profits have grown even faster.

Micron just announced Q3 EPS of $25.11, compared to $1.91 in the same quarter last year, a more than tenfold increase in one year. SK Hynix reported Q1 2026 operating profit of 37.61 trillion Korean won, up 405% year-over-year. Samsung's semiconductor division saw Q1 operating profit increase more than eightfold year-over-year. Stock prices have multiplied several times, but profits have multiplied even more, preventing the PE from being pulled up.

AI money is flowing in real, tangible terms into the income statements of memory manufacturers.

Sector Releasing Catalysts in Clusters, Micron Just the First Shot

Micron's earnings report marks the starting gun for this round of the memory earnings season.

Next, the memory sector enters a month with a high density of information: TSMC on July 16, Samsung on July 23, and SK Hynix and Western Digital on July 29.

And the magnitude of Micron's report has already set the tone for the others. Its most critical information isn't the single-quarter beat, but the Q4 guidance of $50 billion in revenue and 86% gross margin.

This guidance essentially tells the market that price increases haven't peaked but are accelerating. The four subsequent companies will, in their different markets and with different product mixes, essentially verify or refute the same trend revealed by Micron's guidance.

First, look at TSMC, which reports on July 16.

TSMC doesn't make memory, but it's the foundation of the entire AI chip supply chain. Nvidia's GPUs, Broadcom's custom accelerators, and AMD's data center chips all come off its production lines. TSMC answers a more fundamental question than memory: whether the capacity bottleneck for AI chips has been broken. Q1 revenue was $35.9 billion, up 40.6% YoY, with a gross margin of 66.2%. Advanced process nodes accounted for 74% of wafer revenue. Q2 guidance is for revenue between $39 billion and $40.2 billion.

TSMC and memory have a multiplier effect. For every advanced process wafer it sells, there's one more AI accelerator downstream, and for every accelerator, several HBM stacks. The HBM capacity paired with a single GPU in Nvidia's Vera Rubin platform is several times that of the previous generation. The more TSMC ships, the tighter memory capacity becomes.

July 23rd is Samsung's earnings report.

Fifteen brokerages expect Samsung's Q2 operating profit to be around 88.3 trillion Korean won, with operating margins flat or even higher than Q1's 66%. For a comprehensive conglomerate making phones, panels, and home appliances, its profit margin has been dragged to this level by its memory segment alone.

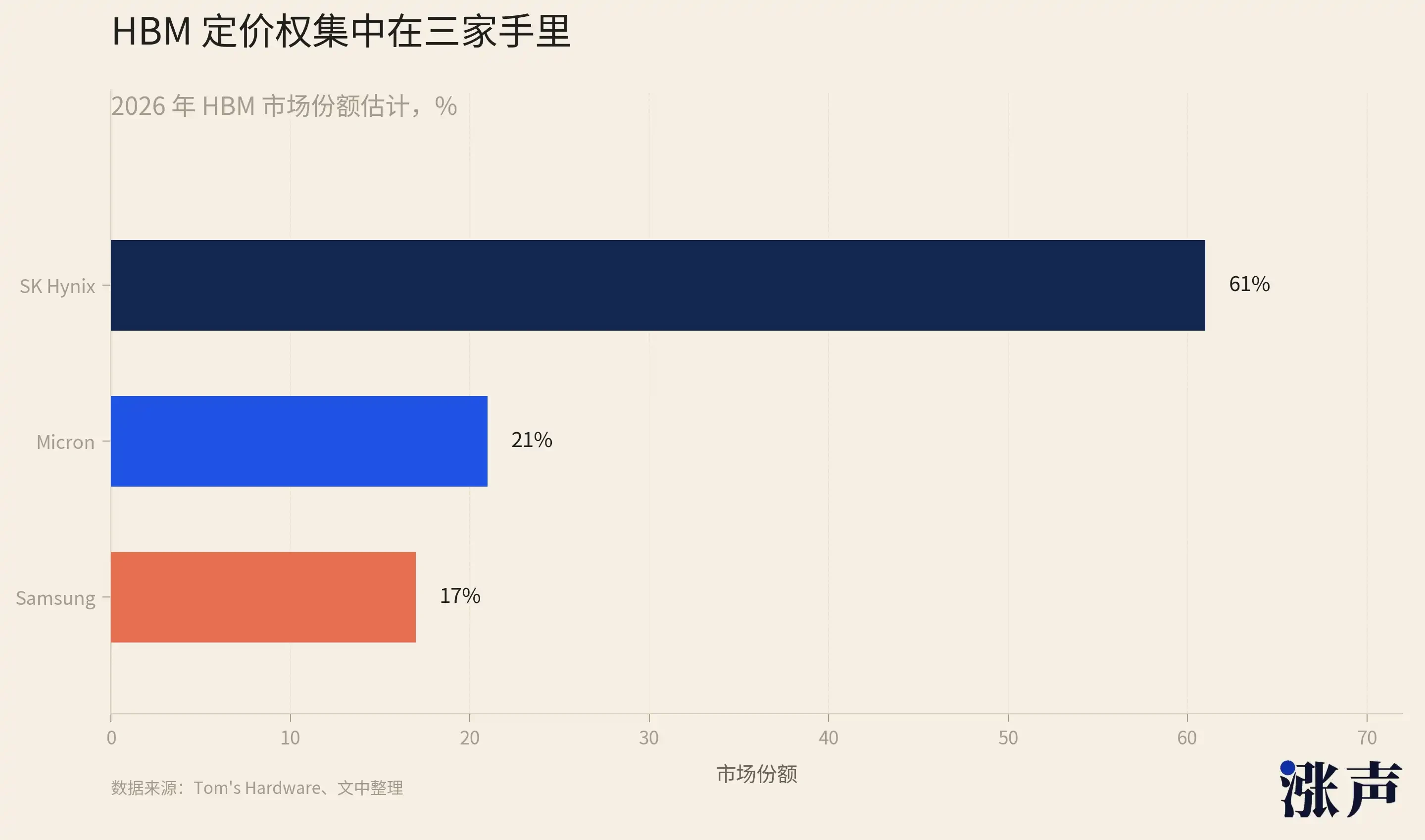

However, the most important aspect of Samsung's earnings report isn't the profit figure, but HBM4. Samsung holds only about 17% market share in HBM, far behind SK Hynix's 62% and Micron's 21%. The generational shift to HBM4 is Samsung's only window to close the gap. During its Q1 conference call, it made a few very specific statements: HBM sales in 2026 will increase more than three times year-over-year, and from Q3 onwards, HBM4 will account for over 50% of HBM sales. Micron just disclosed that its 36GB 12-Hi HBM4 has begun volume production and shipment. The positioning battle among the three on HBM4 is the most crucial fight to watch in the second half of the year.

On July 29, SK Hynix and Western Digital report earnings on the same day.

SK Hynix's Q1 was textbook-worthy: quarterly revenue of 52.6 trillion Korean won, up 198% YoY, an operating margin of 72%, and a net profit margin of 77%. For a hardware manufacturer to achieve a 77% net profit margin is remarkable—Apple's is about 25%, Nvidia's around 58%. Some brokerages predict Q2 operating margin could approach 80%. Micron has already taken the lead with an operating margin of 81.2%, surpassing TSMC. As the market leader in HBM share, SK Hynix is highly likely to deliver a Q2 report comparable to Micron's. The combined Q2 operating profit for Samsung and SK Hynix is expected to exceed 150 trillion Korean won. Together with Micron, the Big Three's single-quarter combined profit will set a new record.

Western Digital reports Q4 on the same day. It has no DRAM or HBM, being purely NAND and SSD. It offers another dimension of AI storage demand: the KV cache for inference requires large-capacity SSDs. Q3 Cloud revenue grew 48% YoY, and gross margin hit a record 50.5%. It's worth noting that Western Digital and its spun-off SanDisk are the two best-performing stocks in the S&P 500 for 2026, ahead of Micron. While NAND segment growth hasn't been as explosive as DRAM, the direction is entirely consistent.

AI Transforms Memory from Commodity to Luxury

Stock prices are at all-time highs, yet PEs are low. Each earnings report is more explosive than the last.

By this point, some might still doubt whether this is sustainable or just another cyclical party destined to crash.

We can look at the analysis from Jukan, a semiconductor analyst at Citrini Research.

Back in Q1 2024, when SK Hynix and Micron were still mired in post-pandemic DRAM inventory gluts and depressed stock prices, Citrini's team called them outperformers. Both stocks subsequently multiplied several times, with some nearing tenfold gains. They have been almost spot-on throughout this memory cycle. A detail from early June shows his position in the market: he reposted a SemiAnalysis report about adjustments to Nvidia's Rubin server memory configuration, which immediately put visible pressure on Micron and SK Hynix's stock prices that day.

Jukan's core bullish thesis for memory isn't a short-term judgment like "prices will go up," but rather a belief that AI is transforming memory from a commodity into a luxury good.

First, HBM has broken a six-decade-long curve. From 1957 to 2020, the cost per Gb of DRAM dropped roughly an order of magnitude every five years; prices were always falling. This is the fundamental law of the memory industry, upon which the competitive model and valuation framework for the entire sector are built. Jukan points out that AI-driven demand for HBM has completely shattered this law. Manufacturers are shifting capacity to HBM, which requires more complex processes and occupies more silicon area, squeezing traditional DRAM supply.

Currently, no manufacturer plans to convert HBM production lines back to traditional DRAM. The reason is simple: HBM profit margins are far higher than those of ordinary DRAM. A rational manufacturer will not swap high-margin lines for low-margin products. This transforms supply tightness from a cyclical phenomenon into a structural one that won't reverse as long as AI demand persists.

Therefore, the sustained price increase for HBM and DRAM will be long-term.

HBM's full-year volume and pricing are essentially negotiated at the beginning of the year, providing manufacturers with strong earnings visibility. Data from TrendForce confirms this: in Q1 2026, contract prices for traditional DRAM rose 90% to 95% quarter-over-quarter, the largest single-quarter increase on record, with further increases expected in Q2. In a normal DRAM cycle, the price increase phase typically peaks after 4 to 6 quarters. This cycle has been rising for nearly 8 quarters without stopping. JPMorgan even predicts DRAM prices could rise for four consecutive years, something unprecedented in the industry's history.

So, it's almost fair to say that memory has transformed from a commodity into a luxury good.

The biggest difference between luxury goods and commodities lies in pricing. Commodity prices are determined by marginal cost; anyone can expand production, competition eventually erodes profits, leading to low valuations. Luxury good prices are determined by scarcity and pricing power; supply is controlled, allowing profits to remain high long-term, commanding a premium. The old rule of "low PE means the cycle is topping" assumes that earnings will revert to that long-term declining trend line. But if the trend line itself has turned, the question of where earnings revert to becomes an open one.

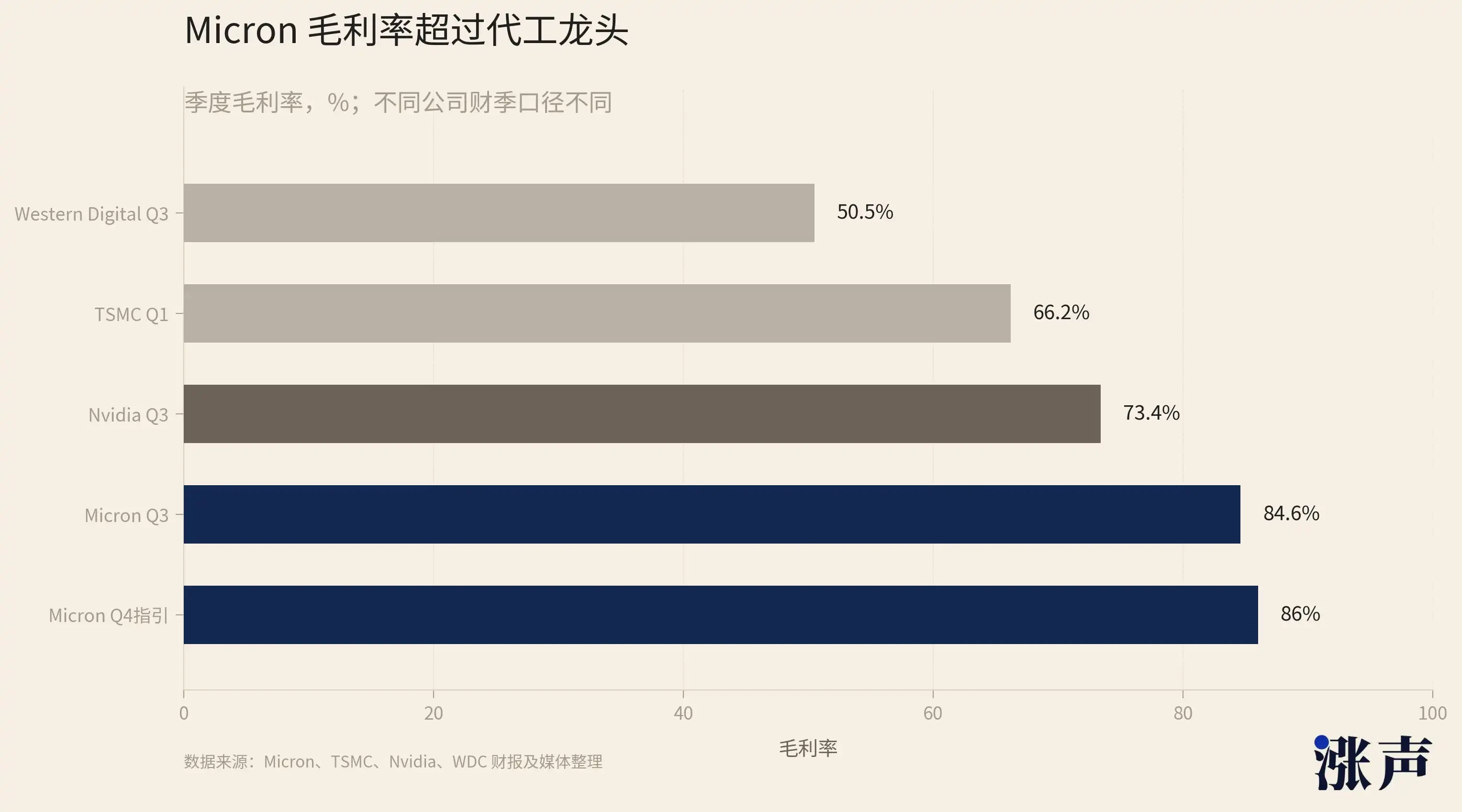

Returning to the contradiction at the start: stock prices are at historical highs, but valuations are at historical lows. This anomaly exists because the market is still pricing an industry that has become a luxury good using the old framework for commodities. Micron has just delivered a heavy blow to this old framework with an earnings report showing 84.9% gross margin and guidance for 86% gross margin. If the trend doesn't reverse, the current 5-10x PEs are wrong.

Therefore, we believe that even with record gains, memory stocks are still not expensive.

After HBM, Could NAND Be the Real Main Course?

In every major market cycle, when the leaders have run their course, the market inevitably asks: who's next in line?

HBM and DRAM have been the absolute protagonists of this memory cycle, with the Big Three's massive gains largely attributed to them. NAND has consistently been treated as a supporting actor.

But if you look closely at the supply-demand structure, you'll find something counterintuitive: NAND, often seen as just a side dish, might actually be the main course itself. Its level of scarcity is, in some ways, even more severe than HBM's.

First, let's consider why HBM is so hot. HBM is standard on AI accelerator cards—high unit price, thick margins, high technical barriers. SK Hynix leverages it to achieve 62% market share and a 77% net profit margin. These are all facts. However, HBM has one characteristic: although supply is tight, the expansion path is clear. The Big Three are all pouring money into expanding HBM capacity. Samsung and Micron are chasing SK Hynix, climbing the ladder from HBM4 to HBM4E generation by generation. Supply is increasing at a visible rate, just temporarily unable to keep up with demand.

In contrast, NAND manufacturers haven't expanded capacity for years.

The NAND price crash of 2022-2023 scared all players. Kioxia, Western Digital, Samsung, and SK Hynix slashed their capital expenditure on NAND to extremely low levels, delaying new production lines repeatedly. The earliest new capacity won't come online until 2027.

The Big Three prioritize wafer capacity and capital expenditure for HBM and high-end DRAM, leaving fewer resources for NAND. Micron even shut down its consumer-grade Crucial business entirely, shifting all capacity to enterprise and GPU-grade storage.

There is a significant lack of NAND supply, but demand is huge.

Large model inference requires massive amounts of KV cache and data throughput, directly fueling explosive demand for enterprise SSDs (eSSD). In Q1 2026, global eSSD revenue grew 86% quarter-over-quarter. Another factor is HDD shortage. The supply of hard disk drives is similarly tight, forcing data centers to use high-capacity SSDs as replacements, shifting some demand originally meant for HDDs onto NAND.

The CEO of Phison Electronics stated, "Every NAND manufacturer tells us they are sold out for the entire year of 2026." Kioxia has also confirmed that its full-year NAND capacity for 2026 is completely sold out. The price of a 1Tb TLC NAND chip has roughly doubled from around $4.8 in July 2025 to around $10.7 by the end of 2025 in just a few months.

HBM is scarce, but supply is increasing predictably; NAND is scarce, but there is almost no increase in supply on the horizon. HBM's tightness has a remedy, just slow-acting; NAND's tightness currently has no solution because no one is preparing the medicine. From this perspective, NAND's supply-demand gap is more rigid, and its price sustainability might be stronger.

This is precisely why the two best-performing stocks in the S&P 500 for 2026 are not HBM leader SK Hynix, nor Micron, but pure-play NAND and SSD companies Western Digital and its spun-off SanDisk. The