铠侠年报里的「存储超级周期」:苹果订单暴增、原料库存激增,整条产业链都在抢先布局

- Quan điểm chính: Báo cáo nghiên cứu của Morgan Stanley chỉ ra rằng ngành công nghiệp lưu trữ đang bước vào một "siêu chu kỳ". Các ông lớn công nghệ tiêu dùng như Apple, do lo ngại giá sẽ tăng, đang mua hàng với tâm lý hoảng loạn, trong khi các nhà sản xuất thượng nguồn cũng tích cực dự trữ nguyên liệu thô. Toàn bộ chuỗi cung ứng đã chuyển sang chế độ tăng giá và dự trữ hàng.

- Các yếu tố chính:

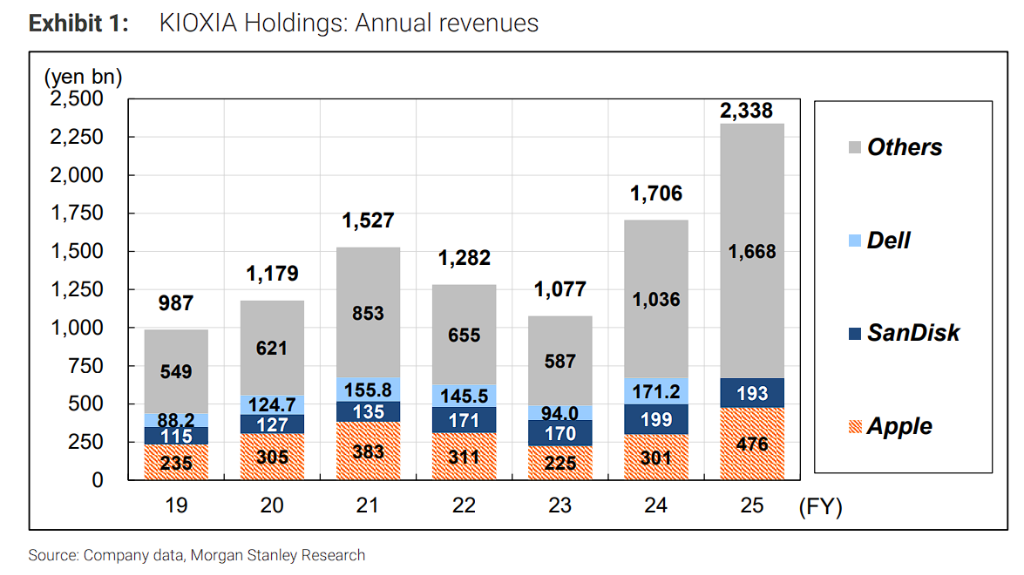

- Doanh thu từ Apple tăng vọt 58% so với cùng kỳ, đạt 476 tỷ Yên, vượt xa tốc độ tăng trưởng chung của Kioxia (+37%), cho thấy giá lưu trữ ở mảng tiêu dùng đã thực sự tăng.

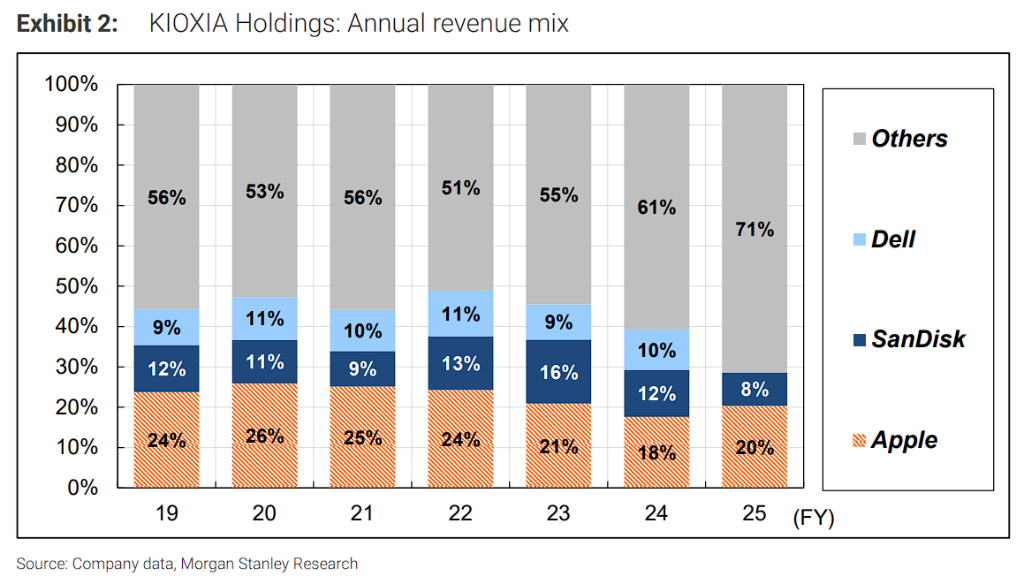

- Tỷ trọng doanh thu từ Apple đã tăng từ khoảng 18% lên đến khoảng 20%, và có hiện tượng mua hàng trước (pull-in procurement) để chốt chi phí và đảm bảo nguồn cung.

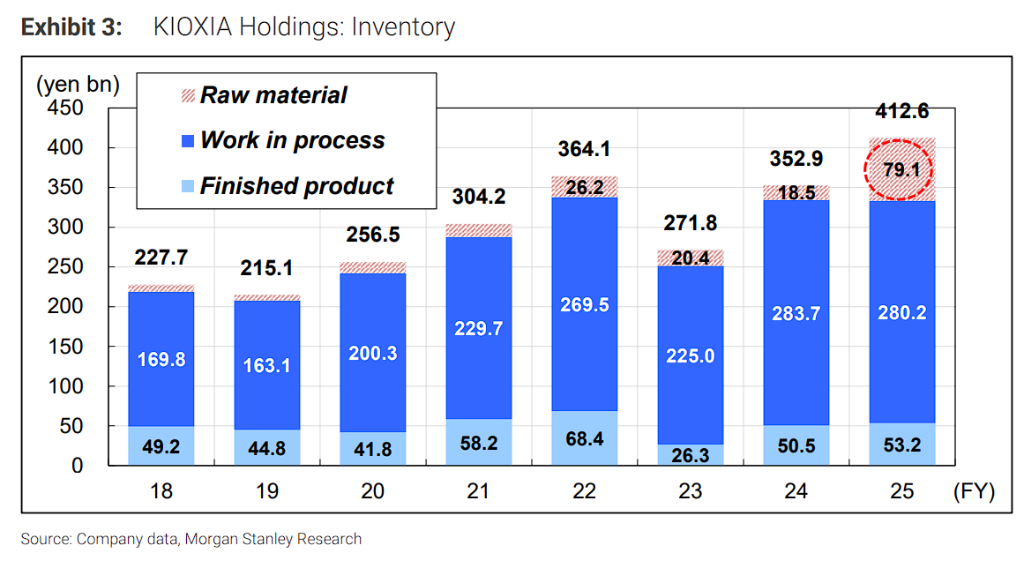

- Tính đến cuối tháng 3 năm 2026, hàng tồn kho nguyên liệu thô của Kioxia đã tăng đáng kể, nguyên nhân chính là do việc mua trước DRAM cho SSD, phản ánh kỳ vọng về sự khan hiếm nguồn cung ở thượng nguồn.

- Cơ cấu chi tiêu vốn của Kioxia đã chuyển hoàn toàn từ xây dựng nhà xưởng (đầu tư xây dựng giảm mạnh xuống còn 6,2 tỷ Yên) sang đầu tư thiết bị tiền đạo cho BiCS-8 và các công nghệ khác (đầu tư máy móc tăng lên 259,8 tỷ Yên).

- Morgan Stanley duy trì xếp hạng "Tăng tỷ trọng" đối với Kioxia, với giá mục tiêu là 110,000 Yên, dựa trên tỷ suất dòng tiền tự do khoảng 10% và hệ số P/E ngụ ý là 11 lần.

Original Author: Dong Jing

Original Source: Wall Street News

Morgan Stanley's latest interpretation of Kioxia's annual report reveals a "super cycle" brewing in the storage industry.

According to Zhui Feng Trading Desk on June 25, the core conclusion of Morgan Stanley's latest research report points directly to a signal: The storage industry's super cycle is accelerating its realization, with consumer electronics giants panic-buying, while upstream manufacturers are frantically stockpiling raw materials. Kioxia's annual report data is the clearest footnote to this cycle.

The report states that Apple contributed revenue surged 58% year-on-year to 476 billion yen, far exceeding Kioxia's overall growth rate. This not only suggests a significant price hike for consumer-grade storage but also indicates that major customers are "stockpiling in advance" before anticipated price increases.

Meanwhile, Kioxia's raw material inventory surged as of the end of March 2026, primarily used for the early procurement of DRAM needed for SSDs, confirming tightness expectations in the upstream supply chain. Additionally, the company's capital expenditure is shifting entirely from factory construction to front-end equipment investments like BiCS-8.

Morgan Stanley maintains an "Overweight" rating on Kioxia with a target price of 110,000 yen, stating that AI-driven demand and strong free cash flow will provide solid support for the stock price.

Apple Orders Surge 58%, Consumer Giant Kicks Off 'Pre-Stocking' Mode

The biggest highlight of the annual report data is the sharp divergence in major customer orders.

In the fiscal year ending March 2026, annual revenue from Apple reached 476 billion yen, a 58% year-on-year increase. This growth rate significantly outpaced the company's overall revenue growth (+37%) and also exceeded the growth rate of the SSD and storage business (+40%).

Morgan Stanley believes this data supports two important judgments:

- First, the storage price hike in the March 2026 quarter has spread to the consumer end. Previously, the market was broadly focused on demand pull from data center clients. However, the rapid growth in Apple orders indicates that the consumer electronics sector also experienced substantial price increases, with Kioxia implementing significant price hikes for consumer-facing clients.

- Second, Apple engaged in early pull-in behavior. Against the backdrop of continuously strengthening expectations of sustained storage price increases, Apple likely conducted pull-in procurement of components to lock in lower costs or ensure supply security. This behavior itself is a direct manifestation of the entire supply chain's "pre-positioning" logic.

Looking at historical data, Apple's share of Kioxia's revenue has jumped from approximately 18% in the fiscal year ending March 2024 to about 20% in the current fiscal year, with the absolute figure rising sharply from roughly 301 billion yen to 476 billion yen.

It is worth noting that two major clients disclosed in the annual report for the fiscal year ending March 2025—SanDisk and Dell—are no longer listed separately in this report as their revenue share fell below the 10% threshold. SanDisk's revenue was previously reported in the quarterly report as 193.4 billion yen (down 3% year-on-year).

Raw Material Inventory Surge: The Entire Supply Chain Pre-Stocks for the Next Price Hike

Morgan Stanley believes Kioxia's annual report inventory data reveals another key signal.

As of the end of March 2026, Kioxia's finished goods and work-in-process inventories were roughly flat year-on-year, but raw material inventory showed a notable increase.

Morgan Stanley judges that this change is likely due to early procurement of DRAM for SSDs. DRAM is an important raw material for SSD production, and locking in raw material supply ahead of time is a rational choice for manufacturers during an uptrend in storage prices.

This shift in inventory structure echoes Apple's pull-in behavior—from the end-brand OEM to the storage manufacturer, the entire supply chain is pre-positioning in its own way, betting on continued storage price increases.

Looking at total inventory, Kioxia's total inventory at the end of the March 2026 fiscal year reached 412.6 billion yen, up from 352.9 billion yen in the March 2025 fiscal year, with the increase in raw material inventory being the most pronounced.

CapEx Structure Shifts: From 'Building Factories' to 'Installing Equipment', BiCS-8 Ramp-Up Accelerates

The report points out that Kioxia's capital expenditure structure underwent a significant shift in the current fiscal year, directly reflecting the company's transition from the capacity construction phase to the equipment investment and production ramp-up phase.

FY3/25 (Previous Fiscal Year): In tangible fixed assets, assets under construction for buildings and structures transferred in amounted to 109.9 billion yen, while machinery and equipment transferred in were 192.7 billion yen, indicating large-scale factory and infrastructure investments in projects like the Kitakami plant.

FY3/26 (Current Fiscal Year): Transfers for buildings and structures plummeted to 6.2 billion yen, while machinery and equipment transfers in rose to 259.8 billion yen. Morgan Stanley believes this clearly shows that the focus of capital expenditure has shifted decisively to BiCS-8 front-end wafer fabrication equipment at the Yokkaichi and Kitakami plants.

Looking ahead to FY3/27 (Next Fiscal Year), Kioxia plans capital expenditure of 450 billion yen, an increase of 166 billion yen year-on-year. Morgan Stanley judges that while there may be some cleanroom construction investment within existing factories, the primary direction will remain front-end equipment investment for BiCS-8 and BiCS-10.

This capital expenditure trajectory clearly indicates: Kioxia is fully committed to building mass production capabilities for next-generation NAND flash technology, preparing supply-side capacity for the upcoming demand peak.

Morgan Stanley maintains its "Overweight" rating on Kioxia, with a target price set at 110,000 yen, representing approximately 19% upside from the current stock price (closing price of approximately 92,290 yen as of June 23, 2026), and lists Kioxia as a Top Pick in the Japanese semiconductor sector.

Morgan Stanley uses an expected free cash flow (FCF) yield of approximately 10% for FY3/28 as a valuation anchor, believing this level provides adequate support for the stock price. The implied price-to-earnings ratio based on the FY3/28 EPS forecast is 11 times.