Insurance industry faces its biggest rival: Are prediction markets the "barbarians at the gate"?

- Core Thesis: Prediction market platforms (such as Kalshi and Polymarket) are encroaching on the traditional insurance industry by offering lower-cost, more transparent risk hedging tools, covering scenarios like sports insurance, housing price hedging, and small business operational risks, signaling a fundamental shift in the risk transfer model.

- Key Elements:

- Kalshi partnered with sports insurance broker Game Point Capital to provide performance bonus hedging for NBA teams. Its pricing (e.g., 6%) is significantly lower than traditional markets (12-13%), and it is expected to process tens of millions of dollars.

- Polymarket collaborated with real estate platform Parcl, allowing users to make monthly/quarterly predictions on housing price index movements in major US cities. Sellers can hedge against falling prices, while buyers can hedge against rising prices.

- A New York bar, The Jeffrey, invested $5,000 on Kalshi to predict a Knicks victory, thus hedging the cost of a "customer free drinks" promotional event, achieving dual wins in risk transfer and marketing.

- Kalshi explicitly positions itself as a "small business insurance provider," offering hedging against risks related to weather, sports, and policy, replacing expensive and inefficient traditional insurance, applicable to industries like hospitality and retail.

- The insurance value of prediction markets is superior to traditional betting: broader market scope, flexible exit options; neutral platform without direct counterparty risk; transparent transaction information; and rejection of "banruptcy or bust" user access models.

- Facing challenges: insufficient liquidity, ambiguous regulatory boundaries (e.g., the insurance function of Kalshi/Polymarket is yet to be formally recognized), and decentralization risks (e.g., fraud cases using hair dryers to manipulate weather prediction machines).

Original|Odaily Planet Daily (@OdailyChina)

Author|Wenser (@wenser2010 )

For a long time, the insurance industry has held a "ballast stone" position in the economic system due to its monopolistic posture. However, with the emergence of prediction markets, this status quo may be about to change.

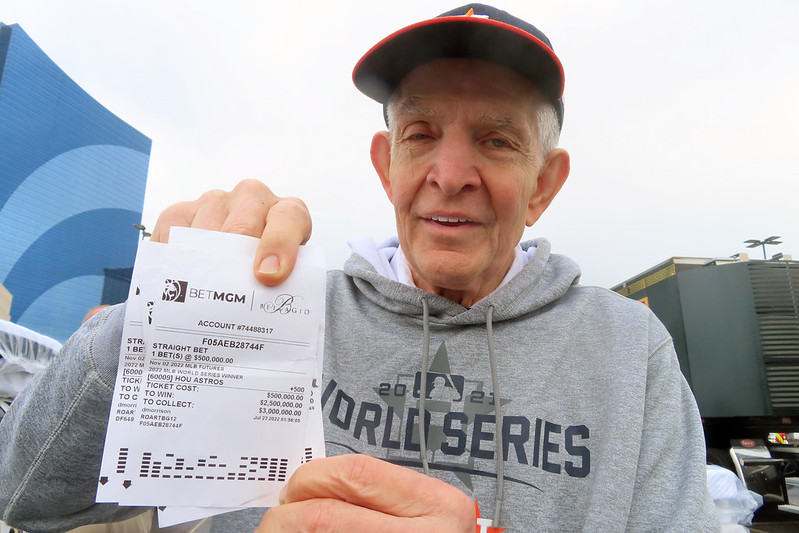

In early June, the NBA Finals concluded, with the Knicks defeating the Spurs 4-1 to win the championship, bringing joy or sorrow to countless people who participated in game predictions. Perhaps one of the happiest people was Andy Freedman, owner of The Jeffrey bar in New York's Upper East Side. Before the game started, he launched a marketing campaign offering "all drinks on the house if the Knicks win Game 1" and simultaneously placed a $5,000 risk hedge on the prediction market platform Kalshi. In the end, the Knicks won the first game, The Jeffrey bar used the prediction winnings to cover drink expenses, and the bar patrons enjoyed free drinks – a "triple-win" conclusion to the story.

This is just one example of prediction market platforms playing a role in risk hedging and property insurance. With the World Cup attracting hundreds of billions of dollars in participation, the real-world insurance industry is now facing a "barbarian at the gate."

Prediction market platforms can also "buy insurance"? Believe it or not?

Yes, you read that right. To some extent, prediction market platforms like Kalshi and Polymarket are now encroaching on the business territory of insurance companies, not just in conventional marketing but also in areas like sports insurance and meteorological disasters.

When Prediction Markets Poach Sports Insurance Clients: Kalshi Partners with Game Point Capital

In February this year, specialized sports insurance broker Game Point Capital announced a partnership with Kalshi, where the latter would provide hedging for NBA team performance bonuses (e.g., playoff advancement bonuses).

As a professional company issuing hundreds of millions of dollars in sports insurance annually, Game Point Capital's shift is clearly not just to cater to the development of the prediction market industry, but a comprehensive consideration based on business, costs, and other factors.

From a market demand perspective, sports insurance has always existed. It is understood that since championship bonuses are usually paid by the teams themselves, professional sports teams typically purchase insurance in advance to cover these expenses. Due to the large sums involved, teams traditionally relied on conventional insurance companies like Lloyd's, Munich Re, and Swiss Re.

From a cost perspective, prediction market platforms offer more advantageous pricing. Kalshi's pricing is reportedly significantly lower than traditional over-the-counter markets (e.g., ~6% hedging fee vs. traditional 12-13%). The platform is expected to handle tens of millions of dollars in hedging funds through this partnership, a direct example of prediction markets entering the traditional insurance and reinsurance space. Kalshi CEO Tarek Mansour described it as "a better way to hedge risk and insure," emphasizing that "the pricing will be more transparent."

When Prediction Markets Become "Home Price Hedging Tools": Polymarket Teams Up with Parcl to Launch "New Home Trading Mode"

In January this year, on-chain real estate platform Parcl announced a partnership with Polymarket to introduce Parcl's daily home price index into Polymarket's new real estate prediction market. The initial markets will focus on major US cities (New York, Los Angeles, Miami, Austin, etc.). Users can predict whether the home price index for a specific city will rise or fall, and by how much, on a monthly, quarterly, or yearly basis.

Upon the announcement, Parcl's native token PRCL surged over 100% that day. For Americans priced out of the housing market, this allows them to participate in "property trading" without actually buying a house. Realtor senior economist Joel Berner believes, "Beyond speculating on home prices, homeowners and potential buyers can use these markets to protect their market interests."

For sellers worried about falling prices, they can buy "Under" contracts on Polymarket. If prices subsequently fall, the related gains can partially offset actual property losses, acting as insurance. For buyers, or those planning to purchase, worried about rising prices, they can predict "Over" gains, which can also be used to cover purchase costs.

When NBA Games Meet Free Drinks: Cross-industry Marketing Between a NYC Bar and Kalshi

In early June, Kalshi officially announced that the New York bar The Jeffrey had placed a $5,000 prediction on "Knicks winning Game 1," with the slogan – "If the New York Knicks win, all customers' bills are on the house." Notably, Kalshi's official statement used the term "place a $5,000 hedge on Kalshi," strongly emphasizing the insurance value of the prediction market.

In this official press release, Kalshi also revealed greater ambition – to become an "insurance provider for small businesses." This includes offering services related to sports event predictions, weather condition forecasts, and import/export policy changes to hotels and inns affected by seasonal sports seasons, clothing stores and other commercial venues impacted by weather-related foot traffic, and small businesses dependent on imported goods – thereby achieving insurance hedging.

Kalshi's Head of Business, Nicolas Hull, stated, "Small businesses face various real-world risks every day – weather, politics, sports, economics. Traditional insurance is expensive and inefficient, unable to effectively address these operational risks. Kalshi changes this: we provide a liquid, transparent market platform that allows any business to take appropriate action against risks affecting their operations. This marks a fundamental shift in how small businesses deal with risk."

These cases demonstrate that the insurance value of prediction markets can be widely applied across multiple fields, not just limited to sports events or brand marketing. In practical applications, traditional sports betting has already had successful precedents.

Old Wine in New Bottles, But the New Bottles Work Better: The Insurance Value of Prediction Markets Lies in Transparency and Liquidity

In 2018, home appliance brand Vatti launched a massive marketing campaign promising "full refund if French team wins World Cup". Although it ultimately ended in a fiasco involving "tight deadlines, cumbersome processes, and cash-equivalent coupons," it left a deep impression on many regarding "freebie marketing."

Coincidentally, someone had done this before.

In 2017, Houston furniture tycoon Jim McIngvale (AKA "Mattress Mack") staged a $12 million "refund marketing" campaign based on the "Houston Astros win the championship" gimmick.

Five years later, in 2022, "Mattress Mack" revisited the strategy with a similar campaign. Between May and July of that year, he invested $10 million across six different sportsbooks in Louisiana, Iowa, and Las Vegas, again predicting the "Astros championship," stating he would refund "every single penny" of the winnings to the 3,000 customers who previously participated in his furniture chain's promotion. (Odaily Note: It is understood the promotion offered customers who purchased furniture over $3,000 either a full refund or double refund depending on their participation time).

Ultimately, the then-71-year-old "Mattress Mack" won big again, pocketing $72.6 million in winnings, setting a record for the largest sports betting payout at the time.

However, compared to sports betting, the "insurance" function of prediction markets has undergone significant upgrades.

First, the monetization of information. This brings two major benefits: (1) Wider market scope. Unlike traditional betting with limited options and narrow fields, prediction markets offer a much broader "range of choices"; (2) More flexible exit mechanisms. Unlike betting activities where you can mostly only get your money back, prediction markets react more directly to the potential impact of information changes, facilitating immediate decision-making for participants.

Second, the neutral role of the platform. Unlike the "platform," "house," or "whales" in sports betting events, prediction market platforms act as neutral entities. They only provide trading channels and do not act as direct counterparties to users.

Third, transaction information transparency. Sports betting odds are usually determined by backend companies using their own algorithms and internal information. Many even adopt a "copy trading" model, directly mirroring odds movements from other major platforms. Odds changes and order transaction information are extremely opaque, and event determination standards are often controversial or subject to insider buying (like sweeping late positions).

Fourth, participant access rules. In the US, most sports betting operators operate on a "ban or bankrupt" model, a business model designed to "restrict high-win-rate customer transactions and induce losers and casual players to trade." In 2024, legendary gambler Billy Walters, "Spanky" Kyrollos, and former casino executive Richard Schuetz co-founded a non-profit advocacy organization called American Bettors Voice (ABV). Its core claim is opposing the "ban or bankrupt" model and demanding reasonable regulation of betting limits to ensure market fairness.

Compared to traditional sports betting, the insurance value of prediction markets is undoubtedly more attractive and secure. Prominent market maker SIG CEO Jeff Yass previously mentioned in a Forbes interview: "Prediction markets allow parties to share risk more efficiently based on specific parameters. For example, a Florida homeowner facing hurricane risk could buy a 'positive outcome' contract based on the latest meteorological data that pays out when wind speeds exceed a specified threshold. This way, they effectively get insurance protection against potential property loss risk, more efficiently than buying annual coverage."

Of course, currently, the insurance value of prediction markets is not yet fully developed or widely promoted, and they still face the following issues:

- Insufficient liquidity. A wide range of options does not necessarily mean sufficient market depth.

- Blurred regulatory boundaries. Whether platforms like Kalshi and Polymarket can sustainably bear insurance functions still awaits regulatory approval.

- Decentralized democracy risks. The incident where someone used a hairdryer to influence observation machines for profit during Polymarket's weather prediction event is a case in point. Sometimes, event determination standards can be affected by unpredictable external forces and various loopholes in platform judgment rules.

But regardless, the first step has been taken. Whether the insurance industry acknowledges it or not, prediction market platforms are a threat not only to sports betting platforms but also to many traditional insurance companies.

Recommended Reading

Not Speculation, but a Necessity: 4 Unique Values of Prediction Markets

The Prediction Markets Are Coming For Risk Markets and Insurance