《Đạo luật CLARITY》ra mắt: Ethereum trở thành người chiến thắng lớn nhất?

- Quan điểm cốt lõi: Đạo luật CLARITY (Đạo luật về sự rõ ràng của thị trường tài sản kỹ thuật số) của Hoa Kỳ, bằng cách thiết lập một bài kiểm tra phi tập trung nghiêm ngặt, sẽ biến Ethereum trở thành hàng hóa kỹ thuật số duy nhất trong hệ thống pháp luật Hoa Kỳ vừa có khả năng lập trình vừa có sự rõ ràng về mặt quản lý. Điều này sẽ chấm dứt hai luận điểm giảm giá chính đã đè nặng lên ETH trong thời gian dài (rủi ro quản lý và mối đe dọa cạnh tranh), đồng thời đẩy nó vào một hệ thống định giá dựa trên phần bù tiền tệ thay vì dòng tiền, mở ra một cuộc định giá lại tiềm năng trị giá hàng nghìn tỷ đô la.

- Các yếu tố chính:

- Trong năm bài kiểm tra về "kiểm soát phối hợp" của dự luật (như phi tập trung, mã nguồn mở, quyền hạn, v.v.), ngưỡng tập trung 49% token hoặc quyền biểu quyết là ranh giới quan trọng. Bitcoin và Ethereum vượt qua một cách dễ dàng, trong khi các nền tảng hợp đồng thông minh chính thống khác như Solana, BNB Chain, Sui vì những lý do cấu trúc không vượt qua được, và bị xếp vào loại "tài sản phụ thuộc".

- Việc phân loại "tài sản phụ thuộc" sẽ kích hoạt nghĩa vụ công bố thông tin nửa năm một lần và một khuôn khổ định giá dựa trên dòng tiền, điều này sẽ khiến token mất đi phần bù tiền tệ. Ngược lại, các tài sản vượt qua bài kiểm tra (như ETH và BTC) có thể được định giá dựa trên các yếu tố phi cơ bản như sự khan hiếm, hiệu ứng mạng lưới, và giới hạn định giá của chúng hoàn toàn được mở rộng.

- ETH vượt qua cả năm bài kiểm tra, trực tiếp loại bỏ rủi ro quản lý khi bị coi là "chứng khoán". Đồng thời, các đối thủ cạnh tranh trực tiếp không vượt qua được bài kiểm tra (như Solana) sẽ buộc phải bước vào hệ thống định giá dựa trên dòng tiền, không thể cạnh tranh với ETH trong khuôn khổ định giá phần bù tiền tệ, chấm dứt câu chuyện "kẻ hủy diệt Ethereum".

- So với Bitcoin, lợi suất staking gốc của Ethereum mang lại chi phí nắm giữ thực tế dương, đồng thời tránh được áp lực bán cấu trúc và rủi ro trợ cấp bảo mật dài hạn do cơ chế bằng chứng công việc gây ra, khiến nó trở thành tài sản tiền tệ Tầng 1 có lợi thế kinh tế hơn.

- Nhóm vốn phần bù tiền tệ toàn cầu (khoảng 50 nghìn tỷ đô la tài sản) đang dịch chuyển từ các vật mang truyền thống như bất động sản, vàng sang tài sản kỹ thuật số để đối phó với sự suy giảm lòng tin của các tổ chức và rủi ro địa chính trị. ETH trở thành tài sản ứng cử viên đầu tiên kết hợp chi phí nắm giữ âm, thanh khoản toàn cầu, bảo mật mật mã và tính độc lập của tổ chức.

- Ngay cả khi Solana hoặc Aptos vượt qua bài kiểm tra trong giai đoạn chuyển tiếp bốn năm tới, chỉ có chứng nhận pháp lý là không đủ để tự động đạt được định giá Tầng 1. Chúng còn cần sự đồng thuận từ chính mạng lưới, hệ sinh thái và thị trường về thuộc tính "phần bù tiền tệ" của chúng, đây là một thách thức to lớn đối với các mạng lưới hiện đang tập trung vào hiệu suất và ứng dụng.

Author: Adriano Feria

Compiled by: Jiahuan, ChainCatcher

On May 12, the Senate Banking Committee released the full 309-page revised text of the Digital Asset Market Clarity Act.

Most reports will focus on which tokens fail the new decentralization test, which issuers face new disclosure burdens, and which projects need to restructure within the four-year transitional certification window. These reports aren't wrong, but they are incomplete.

The more significant story lies in the bill's impact on the only asset that passes every single test criterion, which happens to be the only one with a programmable smart contract platform.

Once this framework becomes law, Ethereum will occupy a unique regulatory category in the U.S. legal system. Over the past five years, the two dominant bearish theses on ETH will simultaneously collapse, and the market has yet to price this in.

Two Bills, One Framework

Before delving into the substance, it is necessary to briefly review the broader regulatory architecture, as public discussion often conflates two distinct pieces of legislation.

The GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act) was signed into law by the President on July 18, 2025.

It establishes the first federal regulatory framework for payment stablecoins: requiring 1:1 reserves in liquid assets, monthly reserve disclosures, federal or state licensing for issuers, a ban on algorithmic stablecoins, and a key restriction that stablecoin issuers cannot directly pay interest or yield to holders.

The GENIUS Act covers USDC, USDT, and bank-issued stablecoins. It covers nothing else.

The CLARITY Act covers everything else. It addresses the SEC and CFTC jurisdictional split, decentralization tests for non-stablecoin tokens, exchange registration, DeFi rules, custody rules, and the ancillary asset framework.

These two acts are complementary parts of a broader regulatory architecture.

Most financial media coverage of the CLARITY Act has centered on stablecoin yield issues, because Title IV on "Preserving Stablecoin Holder Rewards" was the political focus that nearly killed the bill.

Banks pushed to ban indirect yield through exchanges and DeFi protocols, because yield-bearing stablecoins compete with bank deposits. Crypto exchanges argued strongly to preserve the provision. The bipartisan compromise reached on May 1, 2026, cleared the bill's path, but after several delays in consideration, the bill remains in a precarious state.

This debate is important, but it is just one piece in a nine-title bill. For anyone actually holding and trading non-stablecoin tokens, the far-reaching implications lie in Section 104, and almost no one is talking about its second-order effects on asset valuation.

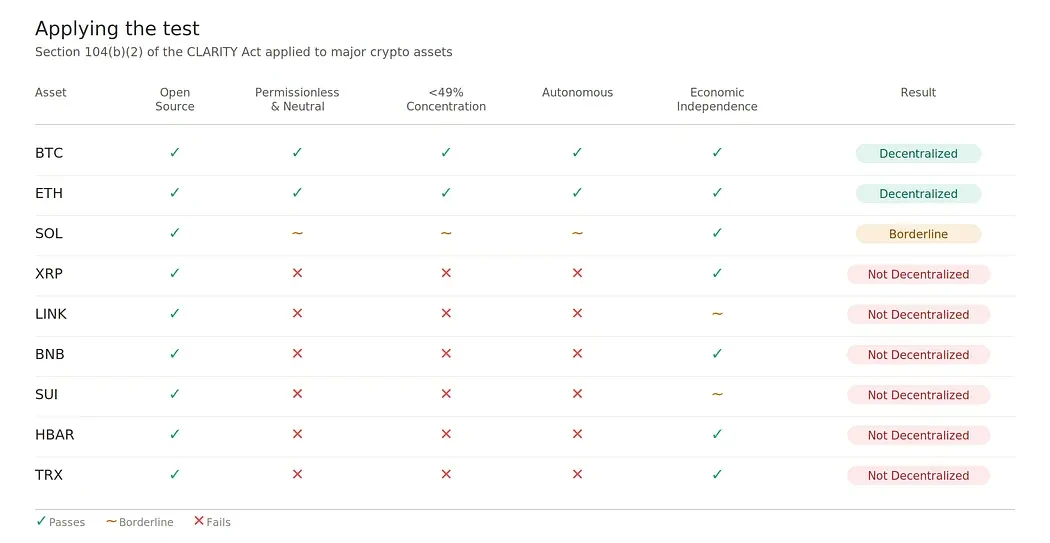

The Five Tests

Section 104(b)(2) of the Act instructs the SEC to weigh five criteria when determining whether a network and its token are under coordinated control:

Open digital system. Is the protocol publicly available open-source code?

Permissionless and credibly neutral. Does any coordinating group have the ability to censor users or grant itself hardcoded priority access?

Distributed digital network. Does any coordinating group beneficially own 49% or more of the circulating tokens or voting power?

Autonomous distributed ledger system. Has the network reached a state of autonomy, or does someone retain unilateral upgrade power?

Economic independence. Is the primary value capture mechanism actually functioning?

Networks failing this test produce a "network token" presumptively classified as an "ancillary asset," meaning its value depends on the entrepreneurial or managerial efforts of a specific promoter.

This classification triggers semi-annual disclosure obligations, insider resale restrictions mimicking Rule 144, and initial issuance registration requirements. Secondary market trading on exchanges can proceed unaffected.

The 49% threshold is the core data point. It is more lenient than the House version of the CLARITY Act's 20% line. Networks failing at the 49% threshold fail for genuine structural reasons, not technicalities.

Bitcoin and Ethereum pass all criteria without dispute. Solana hovers at the edge; the Foundation's influence on upgrades, heavy early insider allocations, and a history of coordinated network pauses argue against autonomy and credible neutrality.

All other major smart contract platforms fail for structural reasons not easily remedied. This list includes XRP, BNB Chain, Sui, Hedera, and Tron, and extends to most L1 competitors.

Among the assets that pass, exactly one has a functioning native smart contract economy.

The Shift in Valuation Frameworks

Tokens trade on two fundamentally different valuation frameworks.

The first is a commodity/monetary premium framework, where value derives from scarcity, network effects, store-of-value properties, and reflexive demand, with no fundamental-valuation ceiling.

The second is a cash-flow/equity framework, where value derives from revenue capitalized through standard multiples, limited by hard caps imposed by realistic revenue projections.

Most non-Bitcoin tokens have existed in strategic ambiguity between these two frameworks, marketing themselves under whichever produces a higher valuation. The CLARITY Act ends this ambiguity through three mechanisms.

First, disclosure requirements impose a cognitive framework. Section 4B(d) requires semi-annual disclosures including audited financial statements (for those above $25 million), a CFO's going-concern statement, related-party transaction summaries, and forward-looking development costs.

Once a token has SEC filings resembling a 10-Q, institutional analysts evaluate it as they evaluate entities filing 10-Qs. The filing format dictates the valuation framework.

Second, the statutory definition is itself a qualifier. An ancillary asset is defined as a token "whose value depends on the entrepreneurial or managerial efforts of the ancillary asset promoter." This definition is conceptually incompatible with a monetary premium, which requires value independent of any issuer's efforts.

A token cannot simultaneously meet the legal definition of an ancillary asset and credibly claim monetary premium pricing.

Third, visible scarcity is fragile scarcity. Monetary premium is reflexive, and reflexivity requires a credible scarcity narrative the market can collectively believe.

When a token discloses its treasury, named insider unlock schedules, and quarterly reports on related-party transactions to the SEC, its scarcity story becomes visible; once visible, reflexivity ends. Investors can see exactly how much supply insiders hold and when those tokens will be sold. This visibility kills buy pressure.

The result is a two-tier market. Tier 1 assets trade on monetary premium, with no fundamental valuation ceiling. Tier 2 assets trade on revenue multiples, with rational valuation caps.

Tokens currently pricing on Tier 1 logic but relegated to Tier 2 will face structural re-rating. For tokens with weak fundamentals and narrative-driven valuations, typified most starkly by LINK and SUI, this re-rating could be severe.

The End of the Two Dominant ETH Bear Theses

For five years, the bear case for ETH rested on two pillars.

The first logic held that ETH would ultimately be classified not as a commodity, but as a security. The pre-mine, the Foundation's ongoing influence, Vitalik's public role, and post-merge validator economics gave the SEC ample grounds to challenge it if desired.

Every bullish case for ETH had to discount the tail risk that institutional capital channels might be restricted.

The second logic held that ETH would be displaced by faster, cheaper smart contract platforms. Each cycle produces new "Ethereum killers"—Solana, Sui, Aptos, Avalanche, Sei, BNB Chain—each marketing better user experience and lower fees.

This argument posited that ETH's technical limitations would force economic activity to migrate, diluting its value capture ability.

The CLARITY Act not only weakens these bear theses but structurally overturns them.

The first thesis collapses because ETH cleanly passes all five criteria of Section 104. No coordinated control, ownership concentration far below 49%, no unilateral upgrade power post-merge, fully open source, value capture mechanism functioning normally.

The regulatory tail risk that long justified a discount on ETH disappears.

The second thesis collapses in a more interesting way. "Ethereum killers" only compete with ETH if they share the same valuation framework.

If SOL is certified as decentralized, competition continues. If it fails (as currently all other major smart contract competitors appear to), they are forced into a Tier 2 valuation framework, while ETH remains in Tier 1.

The competitive landscape thus changes. Tier 2 assets cannot compete with Tier 1 assets on monetary premium, because Tier 1's entire point is that it is not bound by fundamental valuation ceilings.

Those faster, cheaper chains can still win in specific verticals on throughput and developer mindshare. But they cannot win on the asset valuation framework that determines L1 market cap most critically.

The Single Entry Ticket

Among assets passing the Section 104 test, Ethereum is the only one with a functioning native smart contract economy. Bitcoin passes the test but does not support programmable finance at its base layer.

Every smart contract platform with meaningful TVL has one or more material fails on the test. This includes Solana, BNB Chain, Sui, Tron, Avalanche, Near, Aptos, and Cardano.

Thus, the Act creates a new regulatory category: decentralized digital commodities with native smart contract economies, which currently has exactly one member.

Every traditional financial institution exploring tokenization, settlement, custody, or on-chain finance needs two things: programmability and regulatory clarity.

Before CLARITY, these attributes were strictly separated. Bitcoin had clarity but no programmability. Smart contract platforms had programmability but legal ambiguity. After CLARITY, Ethereum becomes the single asset offering both within one statutory category.

Once this framework takes effect, anyone building tokenized treasuries, tokenized funds, on-chain settlement infrastructure, or institutional DeFi onboarding has a clear preferred base layer.

This preference is not aesthetic or technical. It is compliance-driven. Asset managers, custodians, and bank-affiliated funds operate within legal frameworks that favor commodity-class assets over security-like ones.

Institutional capital flows follow asset classifications, and the classification has now narrowed to a single programmable asset.

The Sound Money Question

Once BTC and ETH share Tier 1 classification, a careful examination of their monetary properties is warranted, because conventional wisdom gets the causality backward.

Bitcoin's favor has always rested on its nominally fixed supply schedule of 21 million and predictable halving every four years. As a scarcity narrative, this is incredibly valuable, and the simplicity of that story is part of why BTC acquired monetary premium first.

But BTC's supply model also carries three structural burdens rarely mentioned in scarcity discussions.

First, mining creates continuous structural sell pressure. Network security depends on miners bearing real-world operating costs: electricity, hardware, hosting, financing.

These costs are denominated in fiat, meaning miners must consistently sell a significant portion of their newly issued BTC into the market regardless of price.

This selling is permanent, price-insensitive, and embedded in the consensus mechanism itself. It is the price of maintaining proof-of-work security.

Second, BTC offers no native yield. Holders seeking yield must either lend BTC to counterparties (introducing credit risk) or move it onto non-BTC platforms (introducing custody and bridge risk).

The opportunity cost of holding non-yield-bearing BTC compounds over time relative to assets that generate native yield. For institutional holders measuring performance against yield-inclusive benchmarks, this is a real and persistent drag.

Third, the subsidy cliff is a long-tail risk to the decentralization that qualifies BTC for Tier 1 classification in the first place.

Block rewards halve every four years and approach zero by 2140, but the pressure begins much sooner. By the 2030s, subsidy revenue will be a fraction of today's, and the network must rely on fee revenue to bridge the security gap.

If fee markets do not develop sufficiently, the lowest-cost miners will consolidate, miner concentration will rise, and the credibly neutral decentralization that Section 104 values will begin to erode. This is not an imminent risk but a structural risk that BTC's model has not solved.

Ethereum reverses each of these properties.

ETH has a variable issuance and no fixed cap, which is the core argument sound-money purists use against it. This argument is superficial.

What matters to the holder is the rate of change in their share of total supply, not whether the supply schedule has a fixed terminal value.

Under Ethereum's post-merge design, all issued tokens are distributed as staking rewards to validators. Validators have historically earned a yield higher than the inflation rate, meaning anyone who stakes maintains or increases their share of total supply over time.

For anyone participating in a validator node or holding liquid staking derivatives, the "infinite supply" argument is rhetorically loud but mathematically unsound.

The structural selling that burdens BTC does not exist at the same scale for ETH. Validator operating costs are negligible relative to their returns. Solo staking requires a one-time hardware purchase and minimal ongoing electricity. Liquid staking and pooled staking abstract even those costs away.

Newly issued tokens accrue to validators and are largely retained, rather than sold into the market to cover costs. The same security model that distributes yield to holders also avoids the price-insensitive selling required by proof-of-work.

The subsidy cliff problem similarly does not exist. Ethereum's security budget scales with the value of ETH staked and is funded through ongoing issuance and fee revenue. There is no predetermined date when security funding drops off a cliff.

This model is self-sustaining in a way that BTC's model is increasingly reliant on fee market development that may or may not materialize.

None of this argues that ETH will replace BTC. They serve different roles in institutional portfolios.

BTC is a simpler, cleaner, more politically defensible scarcity asset. ETH is productive monetary collateral that pays its holders for participating in its security.

The key point is that the conventional view, that BTC is "harder money" than ETH because of a fixed supply cap, collapses under examination.

ETH's variable issuance combined with native yield provides better actual economic properties for holders than BTC's fixed supply combined with zero yield, and it does so without structural selling pressure or long-term security funding risk.

For institutional allocators building Tier 1 crypto exposure, this matters significantly. The case for ETH alongside BTC is not just "the programmable one" but "the one that pays you to hold it without forcing structural selling to maintain its security."

Treasury Companies Tell the Same Story

The structural differences between BTC and ETH are not abstract. They