Gate Institutional Weekly: BTC ETF Continues Net Inflows, Aave Lending Balance Plunges 26.7%

- 核心观点:上周加密市场呈现“谨慎乐观”格局,BTC 因地缘风险缓和及降息预期升温上涨至7.7万美元上方;链上资金向高流动性与结算型资产集中,但对复杂风险路径(如rsETH事件)的重新定价导致资金出现结构性迁移。

- 关键要素:

- BTC ETF 周净流入5.85亿美元,BlackRock的IBIT占比超八成;总资产净值突破1026.4亿美元,市场信心修复。

- 稳定币资金回流结算型资产,USDT供应量升至近2000亿美元,而收益型稳定币USDe单周净流出近20亿美元。

- rsETH事件后链上风险偏好下降,Aave 借贷余额单周暴跌26.7%,资金加速流向Spark等竞争协议,核心稳定币借款利率大幅上升。

- 衍生品市场呈现“负资金费率+高位震荡”的典型背离结构,BTC空头持续拥挤,但现货与机构买盘提供支撑,隐含波动率回升。

- 机构交易热度回升,现货交易周环比增长20.09%,CrossEx交易量与资金规模创新高(周环比分别增长79%与816%)。

Summary

• Last week, the crypto market showed a pattern of "cautious optimism." Geopolitical risks in the Middle East marginally eased, and expectations for a Fed rate cut within the year increased. BTC rose from $68,000 to over $77,000, with BTC ETFs maintaining a net inflow trend.

• Trading activity in TradFi has cooled from the March risk-off peak, but gold remains the core trading asset, while the share of stocks and commodities has rebounded.

• On-chain capital continues to concentrate in high-liquidity and high-turnover scenarios. PancakeSwap's weekly trading volume approached $36 billion, while the Solana ecosystem exhibited characteristics of "small-ticket, high-frequency trading."

• Stablecoin capital significantly flowed back into settlement-type USD assets. USDT supply rose to nearly $200 billion, while the yield-bearing stablecoin USDe saw a net outflow of nearly $2 billion in a single week.

• Following the rsETH incident, on-chain risk appetite dropped markedly. Aave's total loans plunged 26.7% in a single week, core stablecoin borrowing rates rose sharply, and capital accelerated towards competing protocols like Spark.

• The derivatives market shows a classic divergence structure of "negative funding rates + high-range volatility." BTC perpetual contract shorts remain crowded, but spot and institutional buying provide support; simultaneously, implied volatility and options trading volume have rebounded.

• On the institutional and platform side, spot trading volume increased by +20.09% WoW, with 30+ new opportunities added; CrossEx trading volume and capital scale hit new highs, up +79% and +816% respectively, with institutions accelerating cross-exchange arbitrage and hedging; the trading system 3.0 architecture is advancing, infrastructure continues to improve, and institutional capital access is accelerating.

1. Market Focus Analysis

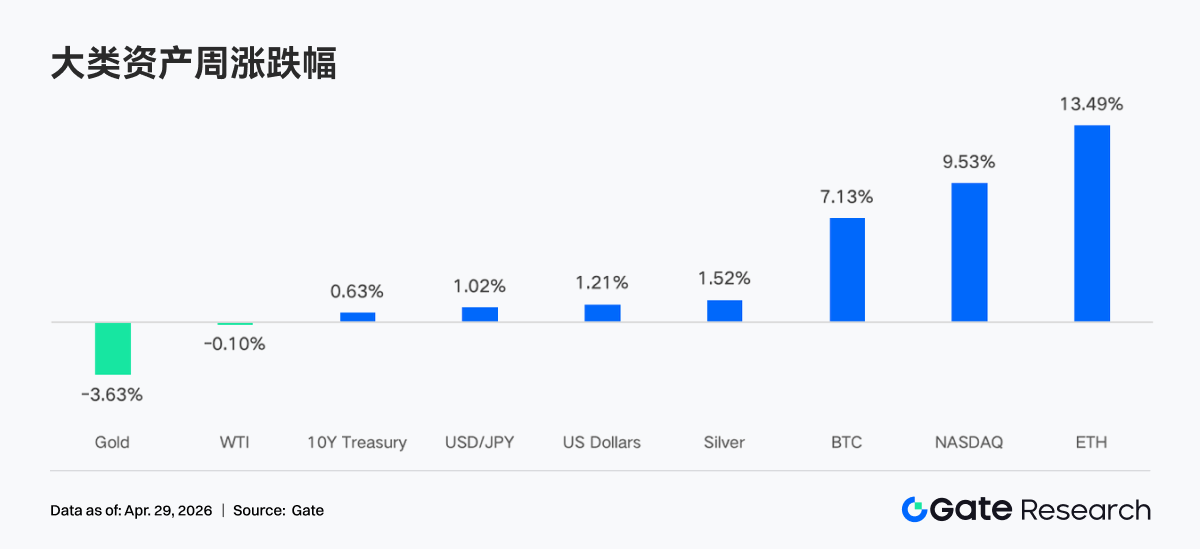

Last week's overall crypto market sentiment was characterized as "cautiously optimistic," primarily driven by easing geopolitical tensions in the Middle East, rising expectations for a Fed rate cut, and continued institutional buying effectively hedging against profit-taking pressure from short-term holders. During this period, BTC rose from around $68,000 to over $77,000, a gain of approximately 12%.

Trump extended the ceasefire agreement with Iran, signaling a desire for a diplomatic resolution to the conflict, but negotiations for a longer-term peace deal are currently at an impasse. The Strait of Hormuz, a passageway for about one-fifth of the world's oil supply, remains closed, pushing oil prices back to $95 per barrel. In recent weeks, the market has largely priced in the tail risks of the Middle East situation. BTC and ETH have continued to rise, with ETH showing greater resilience due to ecosystem expectations. Stock markets have also recovered from the March sell-off. Yields have stabilized ahead of the Federal Open Market Committee (FOMC) meeting, with the 10-year Treasury yield around 4.30%. The US Dollar Index is steady near 98, entering a consolidation phase after falling back from above 100. Affected by the dollar and interest rates, gold is under general pressure. Meanwhile, expectations of a Bank of England rate hike are rising, with the British pound rebounding to around 1.36. If it raises rates by 25 basis points before the end of the year, it could weaken a key structural support for the dollar.

Although this week's FOMC meeting is likely to keep rates unchanged, the market will closely watch for changes in the statement's language regarding inflation, the war's impact, and the balance of risks, as well as any adjustment signals on the long-term neutral rate of 3.1%. Market expectations for the Fed's rate cut path this year have significantly warmed up. The probability of a 25-basis-point cut by December is now seen at 39%, up from 23% previously. This shift is partly attributed to the DOJ dropping its investigation into Powell, further clearing the way for a potential successor, and also reflects market expectations that the Fed will have more easing room in the second half of the year if oil prices return to normal ranges.

2. Liquidity Analysis

2.1 BTC ETF Total Net Assets Surpass $102.64 Billion

Last week, BTC ETFs continued their net inflow trend that began on April 14, recording four positive inflow days for a total weekly net inflow of $585 million. ETH ETFs saw a weekly net inflow of $87.3 million, a slight slowdown compared to the previous week's pace, but overall market sentiment remained optimistic, with institutional investors displaying strong long-term holding convictions.

Top BTC ETF Products by Net Flow:

1. IBIT (BlackRock) Weekly Net Inflow: $476.6M

2. ARKB (ARK 21Shares) Weekly Net Inflow: $59.6M

Top ETH ETF Products by Net Flow:

1. ETHA (BlackRock) Weekly Net Inflow: $61.9M

2. ETHB (Bitwise) Weekly Net Inflow: $47.8M

Fund flows show a clear concentration effect among leaders. BlackRock's IBIT dominated with a $476 million weekly net inflow, contributing over 80% of the total weekly BTC ETF inflow. ETHA also led the ETH ETF market with a $61.9 million net inflow. Meanwhile, Grayscale's GBTC and ETHE continue to face persistent capital outflows, reflecting an ongoing structural migration trend from high-fee legacy products to lower-fee new products.

As of April 24, the total net assets of US spot BTC ETFs had surpassed $102.64 billion, representing approximately 6.5% of Bitcoin's total market cap. The total net assets of ETH ETFs stood at about $13.79 billion, roughly 4% of Ethereum's total market cap. In terms of flow trends, the year-to-date net flow for BTC ETFs has turned positive to around $1.85 billion, indicating a recovery in market confidence. However, whether a new all-time cumulative net inflow high can be reached depends on the outcome of the tug-of-war near the $80,000 resistance level.

2.2 TradFi Liquidity

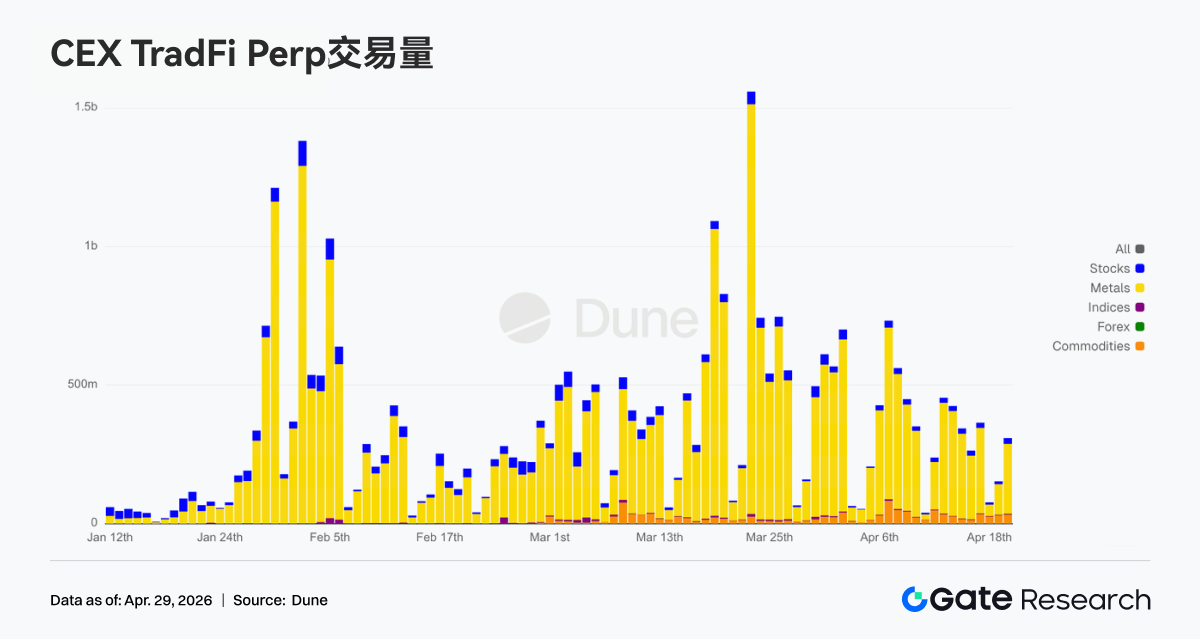

• TradFi Perp DEX: Trading volume in the past week continued to decline slightly compared to previous weeks, with the latest total weekly volume falling to around $10 billion. This shows that the high trading activity driven by risk aversion earlier is gradually cooling as Middle East tensions marginally ease and market risk appetite recovers. In terms of asset structure, commodities still dominate, with gold-related asset trading remaining the market core and accounting for the majority of volume. However, compared to the peak in March, the share of commodities has narrowed, while the share of equity-like assets such as indices, ETFs, and stocks has slightly rebounded. This indicates that capital is gradually shifting from singular safe-haven trading towards a broader range of risk assets.

• TradFi Perp CEX: Since April 20, overall market trading activity has cooled from the March peak but remains in a relatively active range. In terms of volume structure, precious metal assets like gold still dominate. However, compared to the mid-to-late March peak of over $1.5 billion in a single day, recent overall volume has clearly contracted, with most trading days maintaining a range of $300 million to $500 million. This reflects market sentiment transitioning from extreme risk-off to a digestion phase with oscillation. Concurrently, the share of the stock and commodity sectors has ticked up, suggesting capital is spreading from single-asset gold trading to broader TradFi assets, with some users beginning to reposition in equities and cyclical assets.

• CEX TradFi Asset Classes: In the past week, the number of TradFi asset classes on CEXs expanded further. The total count across three major CEXs (only counting TradFi and CFD segments, excluding perpetual contracts) increased from 955 to 956, a sequential increase of 0.1%. The stock sector showed the most significant growth, rising from 590 to 594 instruments. Among mainstream exchanges last week, only Gate added 4 stock TradFi instruments, driving the overall sequential increase of 0.7%.

• TradFi Order Book Depth: We selected XAUT, the TradFi asset with the highest trading volume, to analyze its order book depth (Delta). Between April 20 and 22, market depth Delta showed several large negative values, approaching -$600,000 particularly around April 21. During this time, XAUT's price also fell quickly from around $4,780 to below $4,700, indicating a phase of cooling risk-off sentiment related to gold. However, since April 22, the order book structure has shifted significantly bullish. Green positive Deltas have continuously expanded, with one-sided bid depth frequently maintained in the $300,000 to $800,000 range. Around April 23, bid depth even peaked near $1 million, suggesting significantly increased support capital at lower price levels. Overall, XAUT is currently in a phase of "weak price but improved liquidity absorption." This indicates that while demand for gold-related assets still exists against the backdrop of unresolved Middle East tensions and rising rate cut expectations, short-term momentum chasing is significantly weaker than during the earlier peak risk-off phase.

3. On-Chain Data Insights

3.1 Trading Returns to Spot and High-Turnover Scenarios, Liquidity Further Concentrates Among Leaders

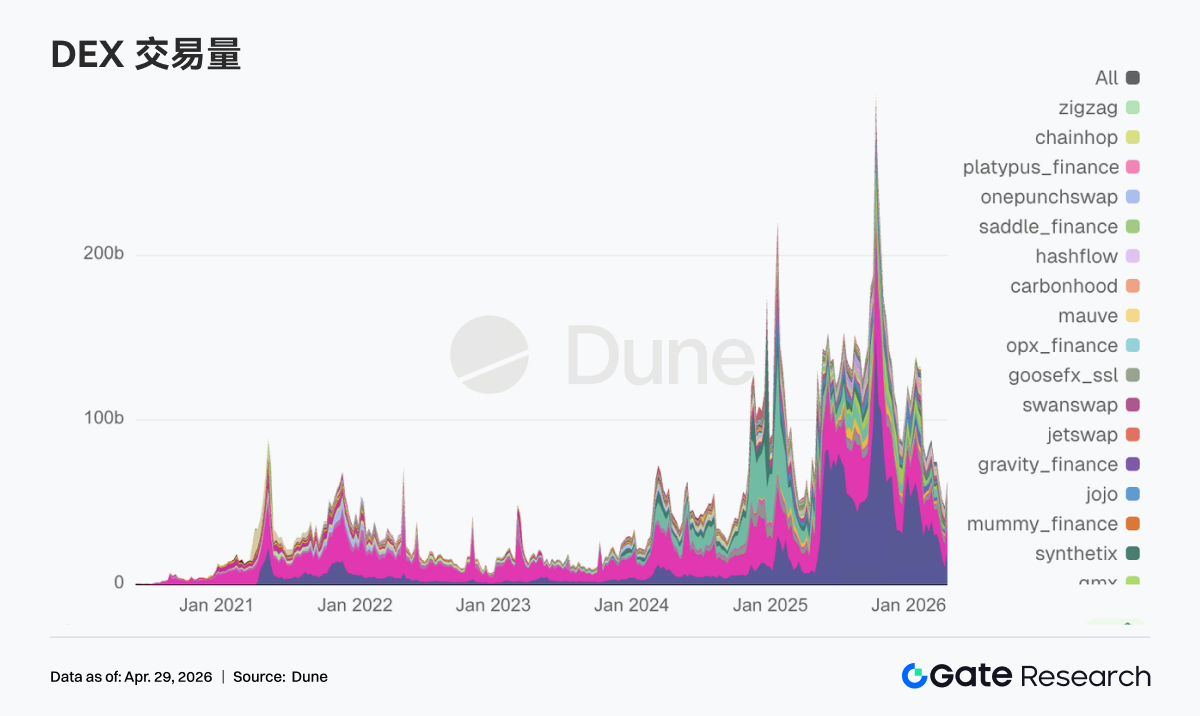

This week, PancakeSwap's trading volume was nearly $36 billion, significantly higher than Uniswap's $18.3 billion. Aerodrome, Curve, and Fluid volumes ranged between $2.5 billion and $3.5 billion. On the Solana side, Raydium and Meteora recorded about $1 billion each, but transaction counts exceeded 100 million, showing a small-ticket, high-frequency pattern. Trading volume remains at elevated levels, suggesting on-chain trading demand hasn't contracted significantly. However, as capital shifts from credit-based DeFi to low-fee, high-turnover spot trading scenarios, liquidity is further concentrating into top-tier pools.

3.2 Stablecoin Capital Concentrates into Settlement USD, USDe Sees ~$2B Weekly Net Outflow

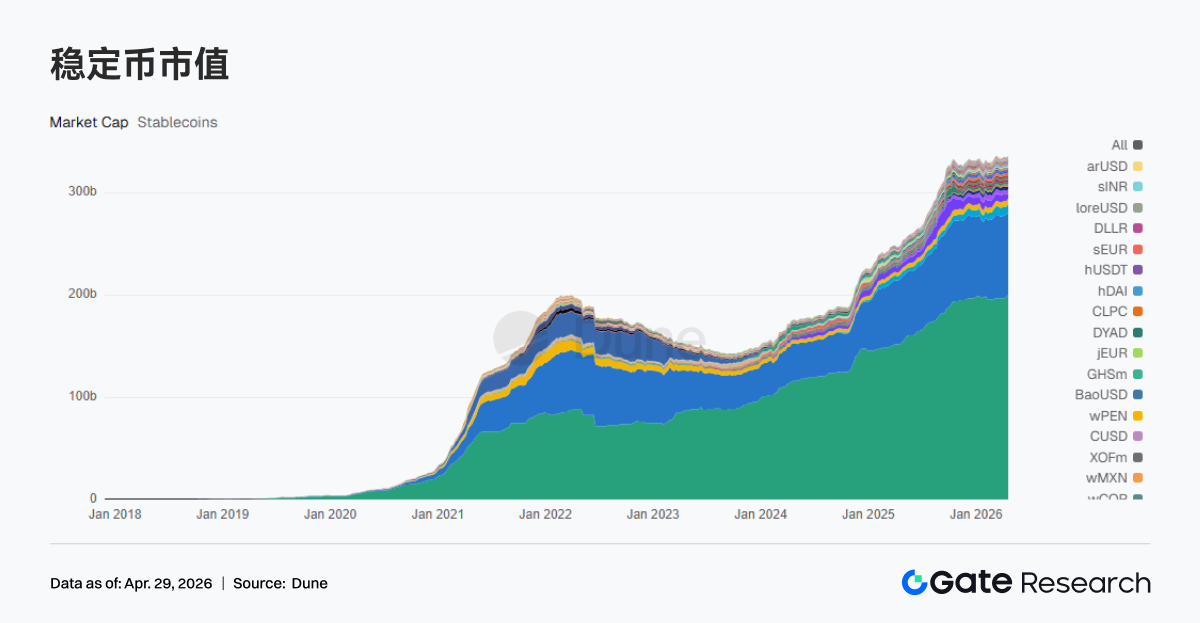

Over the past week, USDT supply rose to $199.959 billion (+$2.418B WoW); USDC was $80.391 billion (-$184M WoW); UShDS was $8.136 billion (+$340M WoW); USDe was $4.410 billion (-$1.997B WoW); PYUSD was $2.750 billion (-$677M WoW). This week, stablecoin capital generally centralized towards directly settled, quickly allocable USD assets, while yield-bearing and synthetic stablecoins saw significant net outflows. USDe led the outflow with nearly $2 billion. Leading stablecoins are all prioritizing their settlement layer and compliant asset capabilities, exemplified by Circle and OSL launching 1:1 USD/USDC conversion with unified margin systems, and Tether cooperating with law enforcement to freeze $344 million in USDT.

3.3 LST Risk Begins Pricing Complex Pathways, Minor Decline in Leading Protocols

Leading LST protocols for ETH and Solana, including Lido, Rocket Pool, Jito, and Jupiter Staked SOL, all experienced minor outflows of 2%-5% over the past week. Following the rsETH incident, the market hasn't rejected staking yields entirely but is repricing the risks associated with cross-chain and restaking pathways. The size of leading LST protocols has slightly decreased, while higher-complexity, yield-enhancing pathways have seen more pronounced pullbacks. Lido, a leading LST protocol, recently proposed using up to 2,500 stETH for bailout efforts, further illustrating the wide reach of systemic risk and the need for collective action from relevant DeFi protocols.

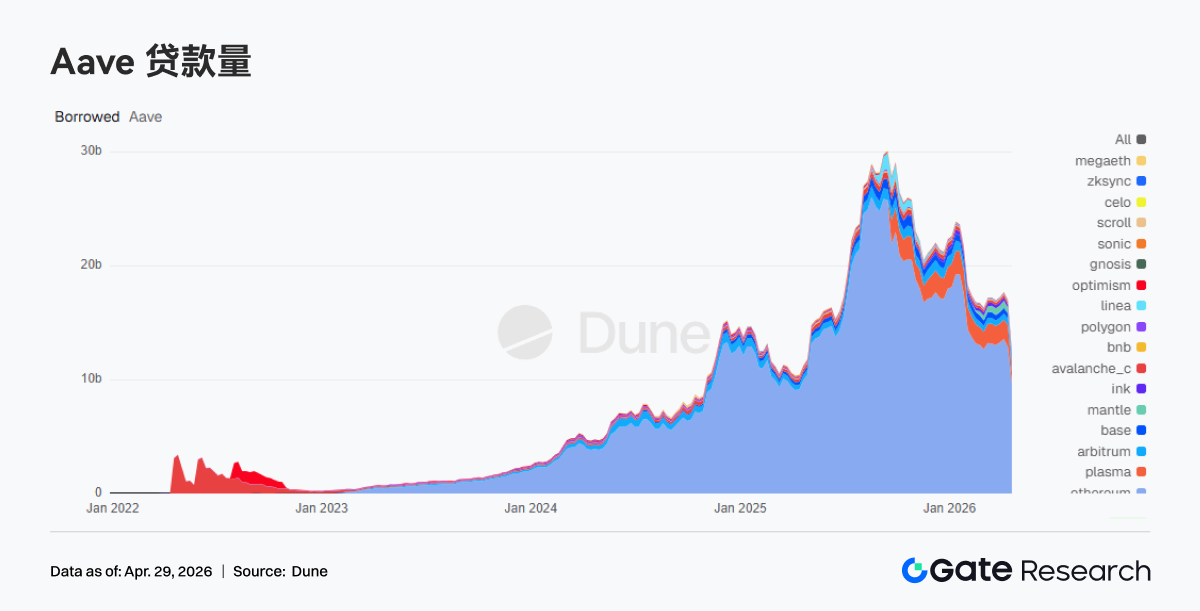

3.4 Aave Lending Balance Crashes, Capital Flees to Competitors

Aave's total lending balance dropped from $17.027 billion the previous week to $12.481 billion, a decrease of $4.546 billion (-26.7%). Ethereum mainnet fell from $12.88 billion to $9.671 billion, while Plasma dropped from $1.93 billion to $942 million. The lending balance showed a step-function decline, characteristic of a risk-event-triggered capital retreat. Following the rsETH incident, Aave froze rsETH/wrsETH across multiple chains and restricted new WETH borrowing, further accelerating position reductions. Most of this capital did not leave the chain but rather moved to Aave's competitor, Spark.

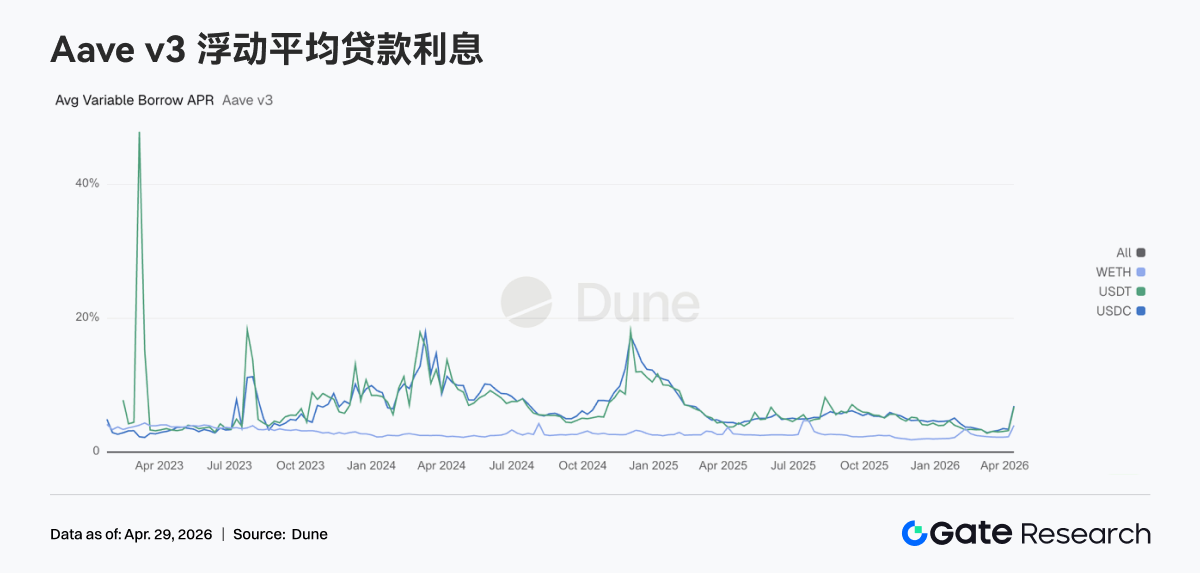

3.5 Phased Liquidity Tightness, Aave Core Asset Rates Rise Significantly

Over the past week, on Aave Ethereum V3, the average USDC borrowing rate rose to 12.50% (from 6.91% previously); USDT rose to 13.30% (from 6.76%); WETH rose to 5.21% (from 4.00%). The rate increases reflect the contraction of stablecoin liquidity. Due to the ongoing contagion from the rsETH security incident, the utilization rate of core assets like USDC in the Ethereum Core market approached 100%, making some liquidity inaccessible and keeping borrowing rates high. Market demand for withdrawable USD liquidity has risen significantly, and the chain has entered a liquidity repair phase. However, as joint rescue efforts progress, asset rates are expected to return to normal ranges in the coming weeks.

3.6 Revenue Flows Back to Settlement and Volatility Linkages, Lending Protocols Benefit

Tether and Circle revenues were roughly flat; Hyperliquid and Pump saw declines of over 10% in a single week; amidst interest rate volatility, Aave's revenue grew over 40% in a single week to nearly $2.9 million. Stablecoin issuance and settlement remain the most stable source of cash flow. Revenue from trading-related protocols is starting to diverge, while lending protocols capture more revenue during periods of volatility and position restructuring. Aave's revenue increasing while its lending scale decreased also reflects shorter position durations and faster capital turnover.

4. Derivatives Tracking

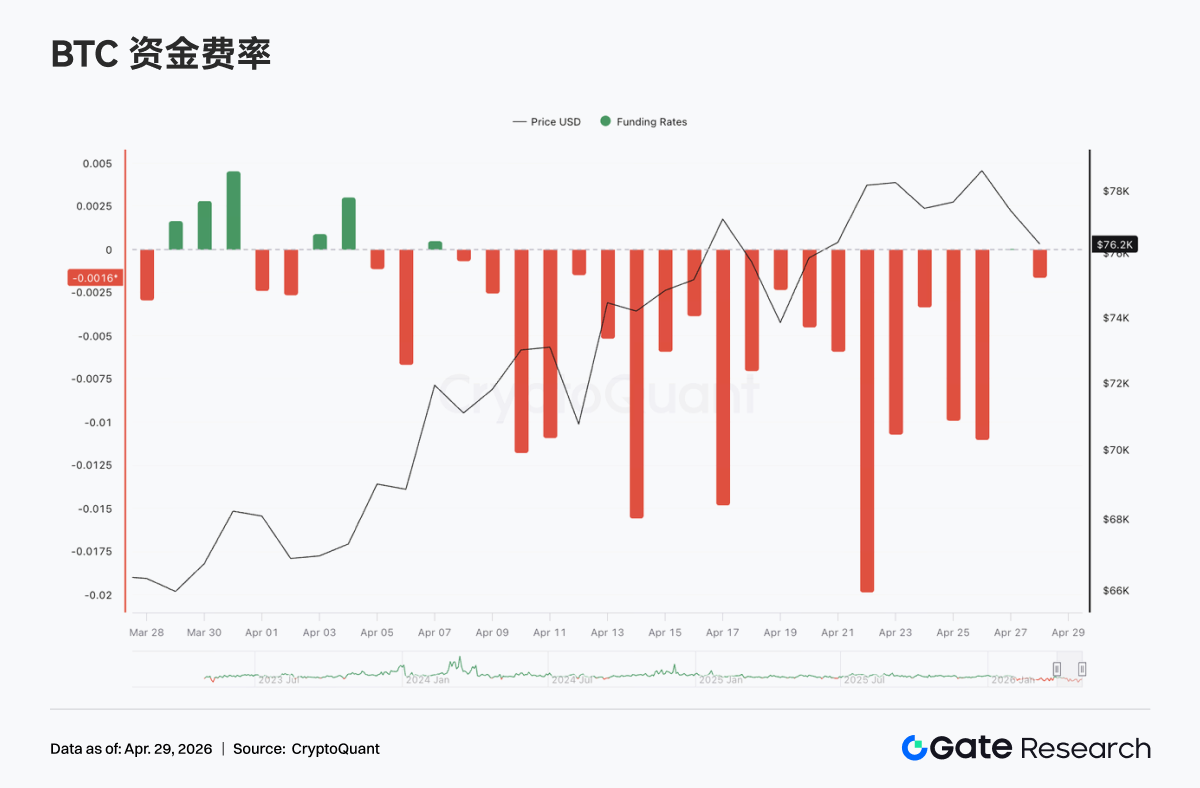

4.1 Deeply Negative BTC Funding Rate Coupled with Rising OI, Squeeze Structure Strengthens

Over the past week, BTC perpetual contract funding rates remained in negative territory overall, repeatedly reaching extreme negative values (as low as nearly -0.02) in mid-to-late April, indicating that bearish sentiment and short crowding stayed at elevated levels. Correspondingly, the BTC price has oscillated upwards since early April, peaking near $78k around April 20. This presents a classic divergence structure of "deeply negative funding rates but sustained high prices," suggesting shorts are under upward price pressure while continuously paying funding fees.

Concurrently, Open Interest (OI) showed an overall upward trend, climbing from approximately $21 billion to over $25 billion. Despite occasional pullbacks, the central tendency has clearly increased. The combination of persistently negative funding rates and rising OI means that during the price's oscillating upward movement, new positions were predominantly shorts, forming a classic divergence pattern of "adding shorts + price not falling."

Around April 17 and April 22, OI spiked rapidly, corresponding to price rallies and high-range consolidation. Meanwhile, funding rates remained deeply negative, indicating that shorts did not effectively stop out during the price increase but instead continued to add positions. This "negative funding rate + OI expansion + price strengthening" combination typically signals accumulating squeeze momentum. If the price breaks out of its range, short covering could accelerate the move. However, it's important to note that high OI coupled with high divergence also implies elevated market leverage. Should the price turn weak, the deleveraging process could similarly amplify volatility.

4.2 Options Volume Shows Phased Expansion, Monthly Contracts Remain Dominant

BTC options market volume showed a characteristic of phased expansion overall, with clear peaks around April 17 and April 23, where single-day volume significantly exceeded the weekly average. Structurally, monthly options still dominate, consistently holding a higher share than weekly or daily options. This indicates that market participants are primarily engaged in medium-term structural positioning, while shorter-dated trades serve more as event-driven or short-term hedging tools.

In terms of rhythm, the volume surges roughly correspond to periods of rapid price movement or around local highs, reflecting a simultaneous increase in hedging demand and active trading during upward price moves. Overall, the options market hasn't shown