A major rival is approaching, with CRCL plummeting over 17%

- Core Thesis: The new stablecoin project Open USD has secured joint support from 140 enterprises, including Visa, BlackRock, and Coinbase. Its model of zero-cost minting and redemption, along with sharing reserve yields with partners, threatens Circle's USDC market position, causing Circle's stock to plunge 17.55% in a single day.

- Key Elements:

- Open USD announced the launch of a new US dollar stablecoin, backed by a collaboration list of 140 enterprises covering payment, banking, technology, and crypto industries, including Visa, BlackRock, Google, and Coinbase.

- Core Innovation: Enterprise users can mint and redeem stablecoins with unlimited amounts and zero fees, lowering the barrier to capital utilization.

- Key Difference: The yield generated from stablecoin reserve assets will be returned to partners rather than retained solely by the issuer, changing the existing model of USDC and others.

- Governance Model: "Neutral governance" is conducted through a board of directors composed of partners, positioning the stablecoin as an open industry infrastructure.

- Market Reaction: Impacted by this news and being removed from the Russell Index, Circle (CRCL) stock saw a sharp single-day decline of 17.55%.

- Competitive Analysis: Backed by its star-studded partnership list and yield-sharing model, Open USD possesses advantages in compliance and network effects from the outset, directly challenging USDC's moat.

Original by Odaily Planet Daily (@OdailyChina)

Author: Azuma (@azuma_eth)

The stablecoin track has welcomed a truly heavyweight new player.

On the evening of June 30, Beijing time, a new company named Open Standard announced the launch of a new dollar stablecoin, Open USD, which is set to officially go live later this year.

Who is Open Standard? No one might have heard of it before today. The real key information is that accompanying the unveiling of Open USD is a partnership list covering 140 enterprises — including giants from the payments sector like Visa, Mastercard, Stripe, and Adyen; financial institutions such as BlackRock, BNY, DBS, Standard Chartered, and Mizuho; tech representatives like Google, Shopify, and IBM; as well as leading crypto industry entities like Coinbase, OKX, Bybit, Ripple, Fireblocks, and MetaMask. These span multiple fields including payments, banking, the internet, and digital assets.

Open Standard stated that the goal of Open USD is to create a stablecoin "for global capital flow," offering enterprises a lower-cost, more open on-chain dollar infrastructure.

Following the announcement, capital markets reacted swiftly. The stock price (CRCL) of stablecoin issuer Circle plummeted by 17.55% in a single day, marking its largest decline in recent times. The market widely believes that the launch of Open USD signifies that the stablecoin industry has finally welcomed a truly competitive new challenger.

What Makes Open USD Different?

At first glance, Open USD might not seem vastly different from USDC or USDT. It is also a stablecoin pegged to the US dollar and employs an over-collateralization model. However, in terms of issuance and operational mechanisms, Open USD incorporates several distinctly different design elements, which seem somewhat aimed at challenging Circle...

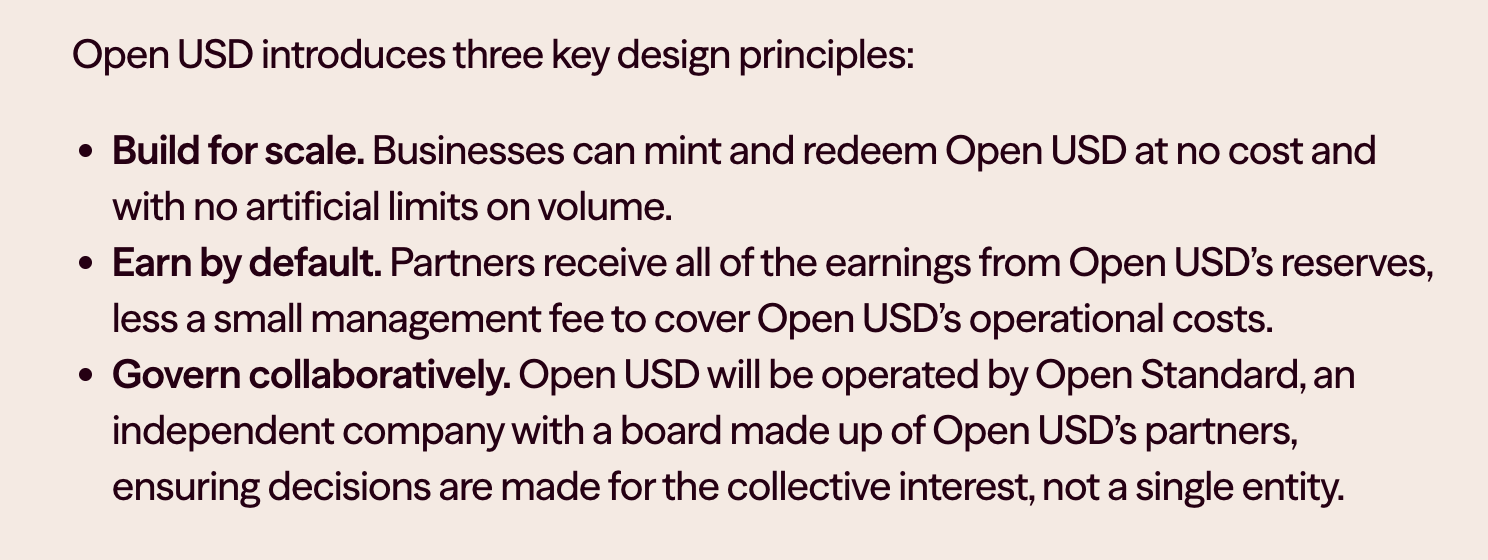

First, zero-cost minting and redemption.

Open Standard stated that enterprise users can issue and redeem stablecoins with unlimited quantities and zero fees, without additional scale limitations. For payment institutions and financial firms that need to handle large capital flows, this implies lower capital usage costs, reducing the barrier to entry for adopting stablecoins as payment infrastructure.

Second, and most critically — the returns generated from reserve assets will belong to the partners.

This is the biggest difference between Open USD and existing mainstream stablecoins. Currently, most stablecoins, including USDC, allocate user-deposited dollars into low-risk assets like US Treasury bonds. The interest income generated primarily goes to the issuer, which is one of Circle's most important profit sources.

Open USD, however, adopts a completely different model. The company stated that the returns from the stablecoin reserves will be returned to partners by default, with Open Standard only charging a small management fee to cover operational costs. In other words, the reserve income, which was traditionally enjoyed exclusively by the issuer, will be redistributed to participants across the entire ecosystem.

Finally, a change in the cooperative governance model.

Open USD is not independently operated by a single company. Instead, it is managed by Open Standard, with a board of directors composed of partner companies that participate in future development directions and major decisions.

Open Standard calls this model "Neutral Governance," aiming to position Open USD as an open industry infrastructure rather than a product belonging to any single company.

Circle Faces a True Adversary

Over the past few years, many stablecoins have attempted to challenge USDC, but most have struggled to truly shake Circle's market position. The reason is simple: the deepest moat for stablecoins has never been technology, but trust, compliance, and adoption rates.

In terms of compliance, Circle has long actively embraced regulation and is one of the most mature stablecoin issuers within the US regulatory framework. Regarding adoption rates, USDC is widely integrated by Coinbase, Visa, Stripe, Robinhood, and numerous exchanges, wallets, and payment institutions, creating a significant network effect. For latecomers, merely launching a new stablecoin is not difficult; the real challenge is getting the entire industry to use it.

However, the situation for Open USD is different. Unlike past stablecoins that relied on a single company and needed to build adoption from scratch, Open USD boasts a prestigious partnership list covering the payment, banking, internet, and crypto industries from its inception. Enterprises like Visa, Mastercard, Stripe, BlackRock, Coinbase, Google, and Shopify are themselves among the most important potential users and promoters of stablecoins.

More importantly, many of these enterprises were already significant participants in the USDC ecosystem. For instance, Coinbase has long maintained deep collaboration with Circle, jointly promoting USDC's development. Meanwhile, payment giants like Stripe and Visa have been key drivers behind the recent real-world adoption of stablecoin payments.

Now, these enterprises collectively joining Open Standard undoubtedly means that Open USD, from the very beginning, stands on a starting point far higher than ordinary new projects in terms of compliance, channels, and adoption rates. For Circle, this might be the true challenge.

One of USDC's greatest past advantages was being the default choice for institutions entering the on-chain dollar ecosystem. However, when a large group of heavyweight players collectively chooses to forge a new path and create a new open standard, the market begins to reassess a critical question: If an enterprise can achieve comparable compliance capabilities, similar network coverage, and also share in the returns generated by the stablecoin reserves, why would it continue to help Circle build the USDC network?

CRCL Plunges Over 17%, Can It Be Held?

Following the Open USD announcement, Circle's stock (CRCL) plummeted over 17% overnight — besides the competitive pressure from Open USD, CRCL's removal from the Russell indices was another key bearish factor.

FTSE Russell, in its latest annual index reconstitution, removed Circle (CRCL) from five major Russell growth index benchmarks. This is a direct blow to institutional holdings.

Considering that Open USD won't be launched until later this year, USDC's market share is unlikely to face a severe short-term impact. However, the market's real concern is whether USDC's moat, built on first-mover advantage, compliance framework, and liquidity network, remains as solid as before.

The emergence of Open USD has led the market to reassess Circle's business model — when enterprises can co-issue stablecoins and share reserve returns, can Circle continue to exclusively enjoy the dividends from stablecoin growth?

These questions may not have answers yet, but the sharp decline in CRCL indicates that the capital market is beginning to reprice this possibility.

As a holder of CRCL, I will not choose to reduce my position at a time when FUD sentiment prevails. However, I will definitely reassess my expectations for this position after CRCL stabilizes.