铠侠年报里的「存储超级周期」:苹果订单暴增、原料库存激增,整条产业链都在抢先布局

- ประเด็นหลัก: รายงานจาก Morgan Stanley ชี้ว่า อุตสาหกรรมจัดเก็บข้อมูลกำลังเข้าสู่ “วงจรซูเปอร์” โดยยักษ์ใหญ่ด้านอุปกรณ์อิเล็กทรอนิกส์เพื่อผู้บริโภคอย่าง Apple กำลังกว้านซื้อสินค้าอย่างตื่นตระหนก เนื่องด้วยคาดการณ์ว่าราคาจะปรับตัวสูงขึ้น ในขณะที่ผู้ผลิตต้นน้ำก็เร่งกักตุนวัตถุดิบเช่นกัน ห่วงโซ่อุตสาหกรรมจึงเข้าสู่โหมดเตรียมสินค้าคงคลังรับมือราคาขาขึ้นอย่างเต็มรูปแบบ

- ปัจจัยสำคัญ:

- รายได้จาก Apple พุ่งขึ้น 58% สู่ระดับ 4.76 แสนล้านเยน เทียบกับอัตราการเติบโตโดยรวมของ Kioxia (37%) ซึ่งบ่งชี้ว่าราคาจัดเก็บข้อมูลในกลุ่มผู้บริโภคได้ปรับตัวสูงขึ้นอย่างมีนัยสำคัญแล้ว

- สัดส่วนรายได้จาก Apple เพิ่มขึ้นจากประมาณ 18% เป็นประมาณ 20% และมีการสั่งซื้อล่วงหน้า (pull-in procurement) เพื่อล็อกราคาต้นทุนและรับประกันอุปทาน

- ณ สิ้นเดือนมีนาคม 2026 สินค้าคงคลังวัตถุดิบของ Kioxia เพิ่มขึ้นอย่างมีนัยสำคัญ สาเหตุหลักมาจากการจัดซื้อ DRAM สำหรับ SSD ล่วงหน้า สะท้อนถึงความคาดหวังถึงภาวะขาดแคลนอุปทานในต้นน้ำ

- โครงสร้างรายจ่ายด้านทุนของ Kioxia เปลี่ยนจากการก่อสร้างโรงงาน (รายการก่อสร้างระหว่างดำเนินการลดลงอย่างรวดเร็วเหลือ 6.2 พันล้านเยน) ไปสู่การลงทุนในอุปกรณ์การผลิตขั้นต้นอย่าง BiCS-8 (รายการเครื่องจักรระหว่างดำเนินการเพิ่มขึ้นเป็น 2.598 แสนล้านเยน) อย่างเต็มรูปแบบ

- Morgan Stanley คงอันดับความน่าเชื่อถือของ Kioxia ที่ “Overweight” โดยกำหนดราคาเป้าหมายที่ 1.1 แสนเยน โดยอ้างอิงจากอัตราผลตอบแทนกระแสเงินสดอิสระประมาณ 10% และอัตราส่วนราคาต่อกำไร (P/E) โดยนัยที่ 11 เท่า

Original author: Dong Jing

Original source: Wall Street News

Morgan Stanley's latest analysis of Kioxia's annual report reveals a "super cycle" brewing in the storage industry.

On June 25th, according to information from the Zhui Feng trading desk, the core conclusion of Morgan Stanley's latest research report points to a clear signal: the super cycle in the storage industry is accelerating towards realization, with consumer electronics giants panic-buying, and upstream manufacturers hoarding raw materials aggressively. Kioxia's annual report data serves as the clearest footnote to this cycle.

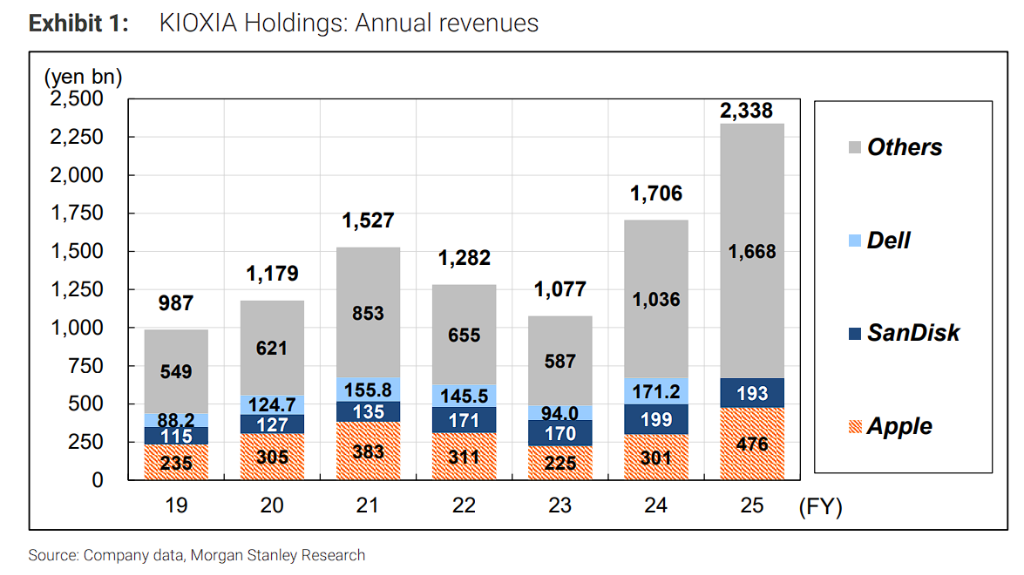

The report states that revenue contributed by Apple surged 58% year-over-year to 476 billion yen, significantly outpacing Kioxia's overall growth rate. This not only suggests that storage prices at the consumer end have risen substantially, but also indicates that major customers are "stocking up in advance" in anticipation of price hikes.

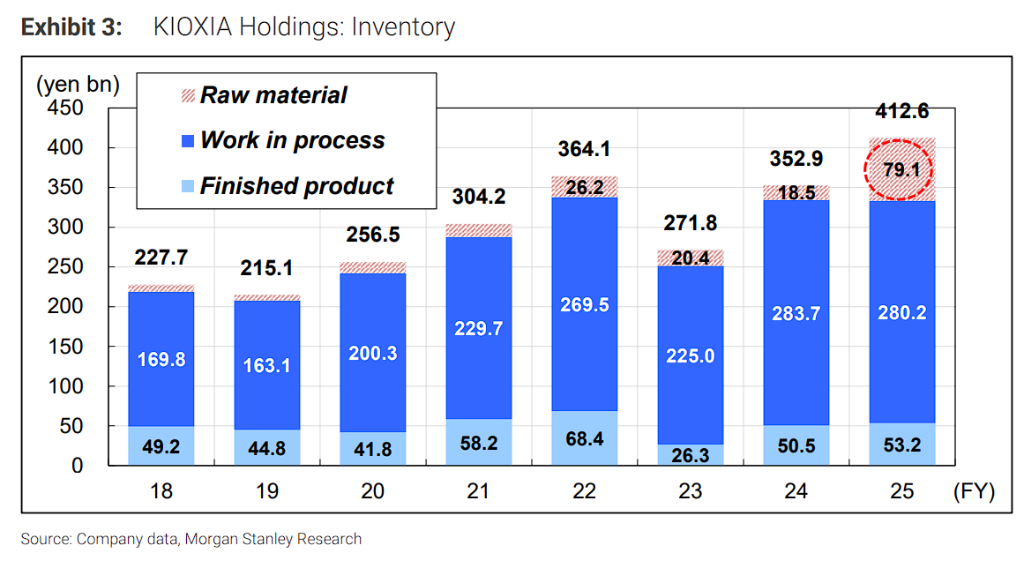

Meanwhile, Kioxia's raw material inventory surged as of the end of March 2026, primarily used for pre-purchasing DRAM needed for SSDs, confirming the expectation of tight supply upstream in the industry chain. Additionally, the company's capital expenditure is shifting entirely from factory construction to front-end equipment investments like BiCS-8.

Morgan Stanley maintains an "Overweight" rating on Kioxia with a target price of 110,000 yen, stating that AI-driven demand and strong free cash flow will provide solid support for the stock price.

Apple Orders Surge 58%, Consumer Giant Enters "Stockpiling in Advance" Mode

The biggest highlight of the annual report data lies in the sharp divergence in major customer orders.

For the fiscal year ending March 2026, annual revenue from Apple reached 476 billion yen, a 58% increase year-over-year. This growth rate not only significantly surpasses the company's overall revenue growth (+37%) but also exceeds the growth rate of the SSD and storage business segment (+40%).

Morgan Stanley believes this data supports two important judgments:

- First, the storage price increases in the March 2026 quarter have spread to the consumer end. The market previously focused on storage demand driven by data center customers, but the rapid growth in Apple's orders indicates that the consumer electronics sector also experienced substantial price increases. Kioxia implemented significant price hikes for consumer-side clients as well.

- Second, Apple engaged in pull-in procurement behavior. Against the backdrop of continuously strengthening expectations of sustained storage price increases, Apple likely conducted pull-in procurement of components to lock in lower costs or ensure supply security. This behavior itself is a direct reflection of the "stockpiling in advance" logic running through the entire industry chain.

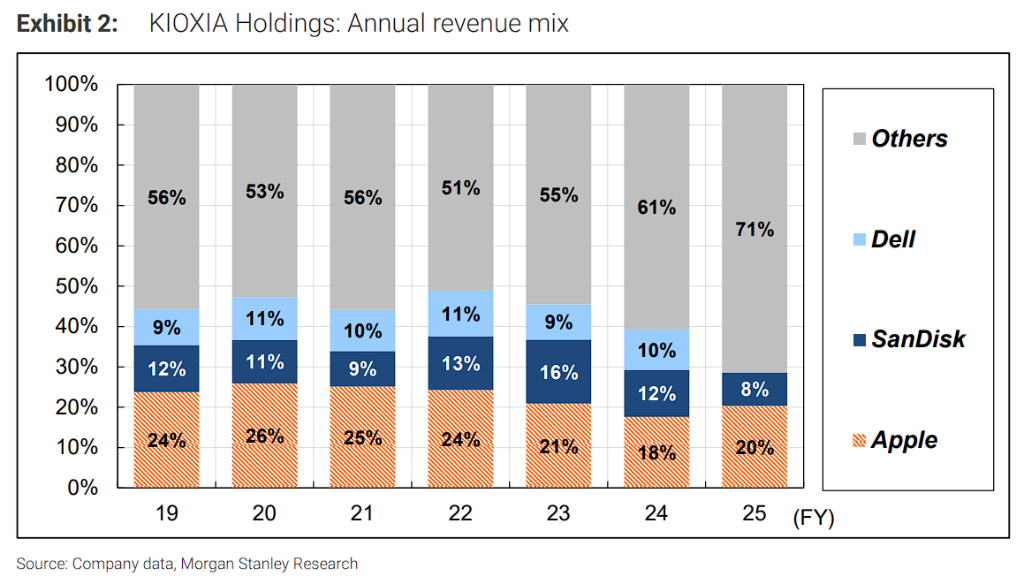

Based on historical data, Apple's share of Kioxia's revenue has jumped from approximately 18% in the fiscal year ending March 2024 to about 20% this fiscal year, with the absolute amount rising sharply from approximately 301 billion yen to 476 billion yen.

It is worth noting that two major customers disclosed in the previous fiscal year's annual report (ending March 2025) — SanDisk and Dell — are no longer listed separately in this year's report as their revenue shares fell below the 10% threshold. SanDisk's revenue was already disclosed in the quarterly report as 193.4 billion yen (-3% year-over-year).

Raw Material Inventory Surge: The Entire Industry Chain is Stockpiling in Advance for the Next Round of Price Hikes

Morgan Stanley believes Kioxia's annual report inventory data reveals another key signal.

As of the end of March 2026, Kioxia's finished goods and work-in-process inventories were roughly flat year-over-year, but raw material inventory saw a significant increase.

Morgan Stanley judges that this change likely stems from the pre-purchase of DRAM for SSDs. DRAM is a crucial raw material for SSD production, and locking in raw material supply in advance is a rational choice for manufacturers during an upward storage price cycle.

This change in inventory structure echoes Apple's pull-in procurement behavior — from terminal brand owners to storage manufacturers, the entire industry chain is positioning itself in advance in its own way, betting on continued storage price increases.

In terms of total inventory, Kioxia's total inventory at the end of the fiscal year ending March 2026 reached 412.6 billion yen, an increase from 352.9 billion yen in the fiscal year ending March 2025, with the increase in raw material inventory being the most prominent.

Capital Expenditure Structure Shift: From "Building Factories" to "Installing Equipment," BiCS-8 Production Ramps Up

The report points out that Kioxia's capital expenditure structure has undergone a significant shift this fiscal year, directly reflecting the company's transition from the capacity construction phase to the equipment investment and production ramp-up phase.

FY3/25 (Previous Fiscal Year): In tangible fixed assets, transfers-in from construction in progress for buildings and structures were 109.9 billion yen, and for machinery and equipment were 192.7 billion yen, indicating major investments in factories and infrastructure for projects like the K1 factory in Kitakami.

FY3/26 (Current Fiscal Year): Transfers-in for buildings and structures plummeted to 6.2 billion yen, while transfers-in for machinery and equipment rose to 259.8 billion yen. Morgan Stanley believes this shows the capital expenditure focus has clearly shifted towards BiCS-8 front-end wafer fabrication equipment at the Yokkaichi and Kitakami factories.

Looking ahead to FY3/27 (Next Fiscal Year), Kioxia plans capital expenditure of 450 billion yen, an increase of 166 billion yen year-over-year. Morgan Stanley judges that although there may be investment in cleanroom construction within existing factories, the main direction will still be front-end equipment investments for BiCS-8 and BiCS-10.

This capital expenditure path clearly indicates: Kioxia is fully committed to building mass production capacity for next-generation NAND flash technology, preparing the supply side for the upcoming demand peak.

Morgan Stanley maintains an "Overweight" rating on Kioxia, with a target price set at 110,000 yen, representing approximately 19% upside from the current stock price (closing price of approximately 92,290 yen as of June 23, 2026), and names Kioxia as a Top Pick in the Japanese semiconductor sector.

Morgan Stanley uses an expected free cash flow (FCF) yield of approximately 10% for FY3/28 as a valuation anchor, believing this level provides ample support for the stock price. The implied price-to-earnings ratio (P/E) based on the FY3/28 EPS forecast is 11 times.