日元逼近40年最低:日本央行已加至1%,为什么还是挡不住?

- Key Point: The Bank of Japan raised interest rates to 1% and conducted a record currency intervention (11.7 trillion yen), yet the yen still fell to its weakest level since 1986, showing that traditional policy defenses have failed. The yen's fate is now entirely tied to the Federal Reserve's policy cycle, with its future trajectory depending on whether the US continues to raise rates, geopolitical de-escalation, and further tightening signals from the Bank of Japan.

- Key Elements:

- Both Rate Hikes and Intervention Have Failed: The BOJ raised rates to 1% in June 2026 (a 31-year high), and the Ministry of Finance intervened with a record $73.7 billion in May, but the yen continues to trade around 161.57, approaching the 1986 low of 162.25.

- Widening US-Japan Interest Rate Differential is the Core Driver: The Fed's dot plot revised its median 2026 year-end rate up to 3.8%, with the probability of a September hike rising to 34.4%. The nominal US-Japan interest rate differential has reached 263 basis points, making the carry trade's yield attractive.

- Risk of a Carry Trade 'Stampede' is Building: The 5% yen plunge in August 2024 was triggered by a mere 15bp BOJ hike. Current positions and the interest rate differential are even larger. The BIS calls this strategy 'picking up pennies in front of a steamroller,' with significant tail risk.

- Japan Faces an Inflation vs. Debt Dilemma: The PPI surged 6.3% YoY, worsening imported inflation. However, government debt exceeds 250% of GDP, meaning each 1% rate hike increases interest payments by 3.7 trillion yen, straining fiscal sustainability.

- Key Variable 1: Fed Actions. If persistently high US CPI in September forces a rate hike, the US-Japan yield spread could near 300bp, pushing the yen past 162.25 into a 'resistance-free' zone towards 165.

- Key Variable 2: Geopolitical De-escalation. Progress in US-Iran talks on June 22 could lower oil prices, easing Japan's trade deficit and providing structural support for the yen.

- Key Variable 3: The BOJ's July Meeting. While the market prices no further rate hikes this year, a statement containing phrases like 'further adjustments' could marginally alter carry trade expectations, though post-meeting signals from Governor Ueda remain uncertain.

Original Source: Wall Street News

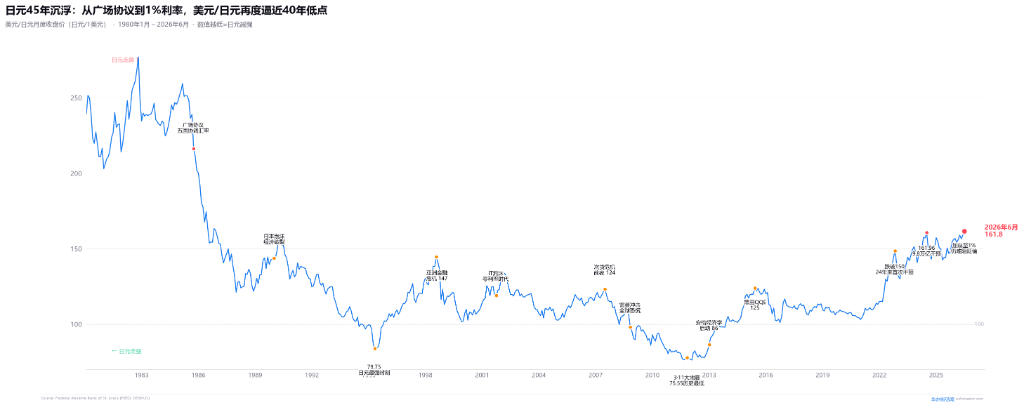

During Asian trading on June 23, the USD/JPY pair traded around 161.57, just a stone's throw away from last week's high of 161.81 — the weakest level for the yen since December 1986.

This came despite the Bank of Japan (BOJ) having just raised its policy rate to 1% the previous Tuesday — the highest level in 31 years.

In other words: the BOJ did the most hawkish thing within its power, yet the yen not only failed to strengthen but weakened further.

Finance Minister Satsuki Katayama has been so desperate that she directly called U.S. Treasury Secretary Scott Bessent to discuss exchange rates. Japan spent a record ¥11.7 trillion (approximately $73.7 billion) intervening in the foreign exchange market in May. The market is now eyeing 161.96 — the previous "defense line" from July 2024. Once breached, the next target is 162.25, the level from December 1986.

But the truly dangerous signal is not the price itself; it's that this time, both defenses — interest rate hikes and intervention — have simultaneously failed.

1% Rate, 350bp Spread

On June 16, the BOJ raised its policy rate from 0.75% to 1%, with a vote of 7 to 1 — only one member opposed. This was the fifth action since the rate hike cycle began in March 2024 and the first time Japan's interest rate has touched the 1% threshold since 1995.

If you look only at the BOJ's actions themselves, what it's doing is already quite aggressive. From -0.1% to 1%, it's a net increase of 110 basis points in 22 months.

But the problem is: you're raising rates, but so is everyone else, and much faster.

The U.S. federal funds rate is currently in the 3.50-3.75% range. The Fed kept it unchanged at its June meeting, but the story behind the surface is much more dangerous.

The Fed's June dot plot showed that 18 of the 19 FOMC participants submitted forecasts, with 9 expecting further rate hikes in 2026. The distribution: 5 predicted two more hikes (25bp each), 1 predicted three more, and 3 predicted one. The median year-end rate jumped from 3.4% in March to 3.8% — the sharpest single upward revision since the dot plot was introduced in 2012. U.S. CPI hit a three-year high of 4.2% in May, and core PCE remains stuck around 3% year-over-year.

Now let's do the math: U.S. rate at 3.63%, Japan rate at 1.00%. The nominal interest rate spread is 263 basis points.

But the long-end spread is even more significant: the 10-year U.S. Treasury yield is around 4.45%, while the 10-year Japanese government bond (JGB) yield is around 2.65% — a gap of about 180 basis points.

Coupled with the fact that the BOJ continues its bond purchases (though reducing by ¥200 billion per quarter, it won't stop completely until April 2027), the upside for JGB yields is artificially suppressed by the central bank itself. This means the annualized interest rate differential return for carry trades (borrowing yen, buying U.S. Treasuries) remains attractive — roughly 263bp on the short end and 180bp on the long end. The BOJ's bond-buying operations artificially depress JGB yields, and market pricing implies no further rate hikes from the BOJ this year, making the carry trade's interest rate differential appear solid.

However, the critical risk isn't whether the BOJ will "hike drastically." The lethality of carry trades has never been about small changes in interest rates, but rather the stampede-like unwinding triggered by crowded positions combined with unexpected catalysts. August 2024 is a case in point: the BOJ raised rates by just 15bp to 0.25%, and combined with weaker-than-expected U.S. employment data, it triggered a chain reaction where the Nikkei plunged 12% in a single day and the USD/JPY plummeted from 156 to 141. In its post-mortem report, the BIS accurately characterized carry trades as "picking up nickels in front of a steamroller" — accumulating steady returns during low-volatility periods, only to suffer massive losses when tail risks concentrate. Today's interest rate differentials are wider than back then, and positions can only be more crowded.

JPMorgan Asset Management's APAC Chief Market Strategist Tai Hui put it more bluntly: "The rate hike itself was within expectations; what was truly surprising was the overwhelming 7-to-1 support — suggesting the committee is more worried about inflation than growth."

Reading between the lines: a consensus has formed within the BOJ — 1% is not enough. But the market doesn't believe it will dare to hike further.

¥11.7 Trillion "Brake Pad"

If rate hikes can't stop the yen's fall, then just buy yen directly.

Official data released by Japan's Ministry of Finance on May 29 showed that between April 28 and May 27, Japanese authorities spent a total of ¥11.735 trillion (about $73.7 billion) intervening in the foreign exchange market — a record for monthly intervention scale.

The largest single-day action occurred on April 30 (eve of Japan's Golden Week): the yen was sharply pulled back from 160.72 to 155.50, with a daily fluctuation exceeding 3%, reversing about 5 yen. Additional operations continued in early May, with the total scale estimated at ¥9.5-10 trillion.

This marks the third consecutive year Japan has deployed large-scale intervention:

April-May 2024: ¥9.79 trillion (approx. $62.3 billion), triggered at 160.25

July 2024: ¥5.53 trillion (approx. $36.8 billion), triggered at 161.76

April-May 2026: ¥11.74 trillion (approx. $73.7 billion), triggered at 160.72

Three-year total: over ¥27 trillion, nearly $180 billion.

But what's the effect? The same every time: a short-term reversal of 3-5 yen, then a return to pre-intervention levels within 4 to 8 weeks.

Jesper Koll, Expert Director at Monex Group, has a vivid analogy: "Intervening in exchange rates without changing domestic monetary policy is like stepping on the brake while your right foot is firmly on the accelerator — at best, passengers feel a slight jolt; at worst, the brake pads burn out."

We are now at the "brake pads burning out" moment.

Compare this to the 1985 Plaza Accord — where G5 countries acted in concert, coordinating policy, interest rates, and fiscal measures comprehensively, moving the yen from 240 to 200 and achieving a permanent trend reversal of about 17%. Today, Japan is fighting alone, and U.S. Treasury Secretary Bessent merely "answered the phone," with no signs of coordinated action.

Warsh's Silence: More Fearsome Than a Rate Hike

The market's faint hope for the yen was that the Fed might cut rates due to economic weakness, thereby narrowing the U.S.-Japan interest rate differential.

The Fed's June meeting completely extinguished that hope.

Fed Chairman Kevin Warsh did two significant things:

First, he refused to submit a dot plot forecast. This is the first Fed chair since the dot plot was introduced in 2012 to not submit a personal forecast. Warsh had publicly criticized the dot plot for creating a "false sense of precision" before his appointment. But the timing of his silence at the June meeting was particularly delicate — precisely when inflation had surged to 4.2% and the committee was deeply divided. The market cannot "position" this chairman on any point of the hawkish-dovish spectrum, and uncertainty itself is a source of pressure.

Second, the meeting statement removed the previous language hinting that the "next move would be a rate cut." Coupled with 9 hawkish dots and the median rising to 3.8%, this is tantamount to saying: "We're not hiking this time, but a rate hike is already on the next table."

Market pricing reflects this anxiety: CME FedWatch shows a 8.8% probability of a rate hike in July, rising to 34.4% in September, and approaching 50% in October. By year-end, the market's implied rate is around 3.95%.

In other words: the current U.S. rate of 3.63% is not only not coming down but has about a one-in-three chance of rising above 4% before year-end.

This means the U.S.-Japan interest rate differential is not only unlikely to narrow but could widen further.

Japan's Own Inflation Ledger

A common counterargument is that a weaker yen is good for Japanese exports, and the Japanese government is actually happy to see it.

This might have held true before 2022. But Japan in 2026 is no longer that deflationary economy.

In May, Japan's Producer Price Index (PPI) rose 6.3% year-over-year, the fastest pace in over three years, mainly driven by surging energy costs. Although April's core CPI fell to 1.4% (suppressed by government policies like gasoline tax cuts and free high school education), the BOJ clearly stated in its June statement: "The cost pass-through from rising crude oil prices is progressing relatively quickly in B2B transactions and may spread into a broad range of consumer price increases."

Behind this is the oil price shock from the Iran conflict. Although U.S.-Iran talks made progress on June 22 (the U.S. announced a 60-day waiver for Iranian oil exports), causing Brent crude to briefly fall below $77, the situation in the Strait of Hormuz is far from truly stabilized.

For Japan, higher import energy costs directly push up domestic costs, and a weaker yen amplifies these import prices. Prime Minister Sanae Takaichi's government has subsidized household energy costs through a ¥3 trillion supplementary budget, but fiscal space is not unlimited.

The deeper issue is the contradiction between Japan's government debt stock and the level of interest rates.

Japan's government debt is approximately ¥1,250 trillion (over 250% of GDP). If interest rates continue to rise from 1%, interest payments alone could consume the fiscal budget. According to BOJ estimates, every 1 percentage point rise in interest rates would increase the government's annual interest payments by about ¥3.7 trillion.

This is the BOJ's dilemma: don't raise rates, and the yen continues to fall, worsening imported inflation; raise rates, and government debt interest payments skyrocket, making fiscal policy unsustainable.

Next Steps: Three Variables Determine Direction

Whether the yen can stop falling does not depend solely on what Japan does unilaterally — both the rate hike and intervention paths have reached their limits. The real variables lie outside Tokyo.

Variable One: Will the Fed really hike again?

This is the most critical variable. Current market pricing shows only an 8.8% probability of a July hike, but this rises to 34% in September and approaches 50% in October. If U.S. CPI and core PCE continue to surprise to the upside over the next two months — the June SEP already sharply revised its 2026 PCE forecast from 2.7% to 3.6% — the probability of a September hike could rapidly move towards 50% or more. At that point, the U.S.-Japan nominal interest rate spread would approach 300bp, and the yen would likely break through 162.25, entering uncharted territory not seen since 1986. Without a Plaza Accord or G5 coordination, the next vague technical reference level only appears around 165.

Variable Two: The actual implementation of the U.S.-Iran agreement.

On June 22, the U.S. announced a 60-day waiver for Iranian oil exports, providing a rare window for de-escalation in the Strait of Hormuz, with Brent crude briefly falling below $77. If a final agreement is reached before August, import-driven inflation pressure for Japan, a net energy importer, would significantly ease. Lower oil prices would directly narrow Japan's trade deficit, providing structural support for the yen — this is the most favorable scenario for the yen among the three. However, geopolitical negotiations are inherently volatile, so this should not be taken as a baseline assumption.

Variable Three: The BOJ's stance at its July meeting.

After the June hike to 1%, market pricing implies no further rate hikes this year — a core premise for the yen's weakness. However, against the backdrop of 6.3% year-over-year PPI growth, if the July statement includes language such as "there is still a need for further adjustment of accommodative policy," even without immediate action, it could marginally change the profit-and-loss calculations for carry trades. However, BOJ Governor Kazuo Ueda has not yet spoken publicly after missing the June meeting (due to hospitalization), creating uncertainty around the policy signals of the July meeting.

Conclusion

The story of the yen has never been just about exchange rates.

It encapsulates Japan's existential dilemma in the era of Globalization 3.0: an aging, high-debt economy dependent on energy imports, whose monetary policy autonomy has been completely hijacked by the U.S. interest rate cycle.

The BOJ raised interest rates to a 31-year high — not enough. Japan's Ministry of Finance spent $180 billion — not enough. The Finance Minister called Washington — the other side merely answered the phone politely.

In 1986, the yen depreciated to its limit around 162, only to appreciate sharply in the aftermath of the Plaza Accord. That year, Japan was still the world's second-largest economy, challenging for the top spot.

In 2026, the yen is back near 162. But this time there is no Plaza Accord, no G5 coordination. Only Japan itself is stepping on the brake — while the accelerator is in Washington.