SpaceX has rewritten the century-old IPO process with a single offering

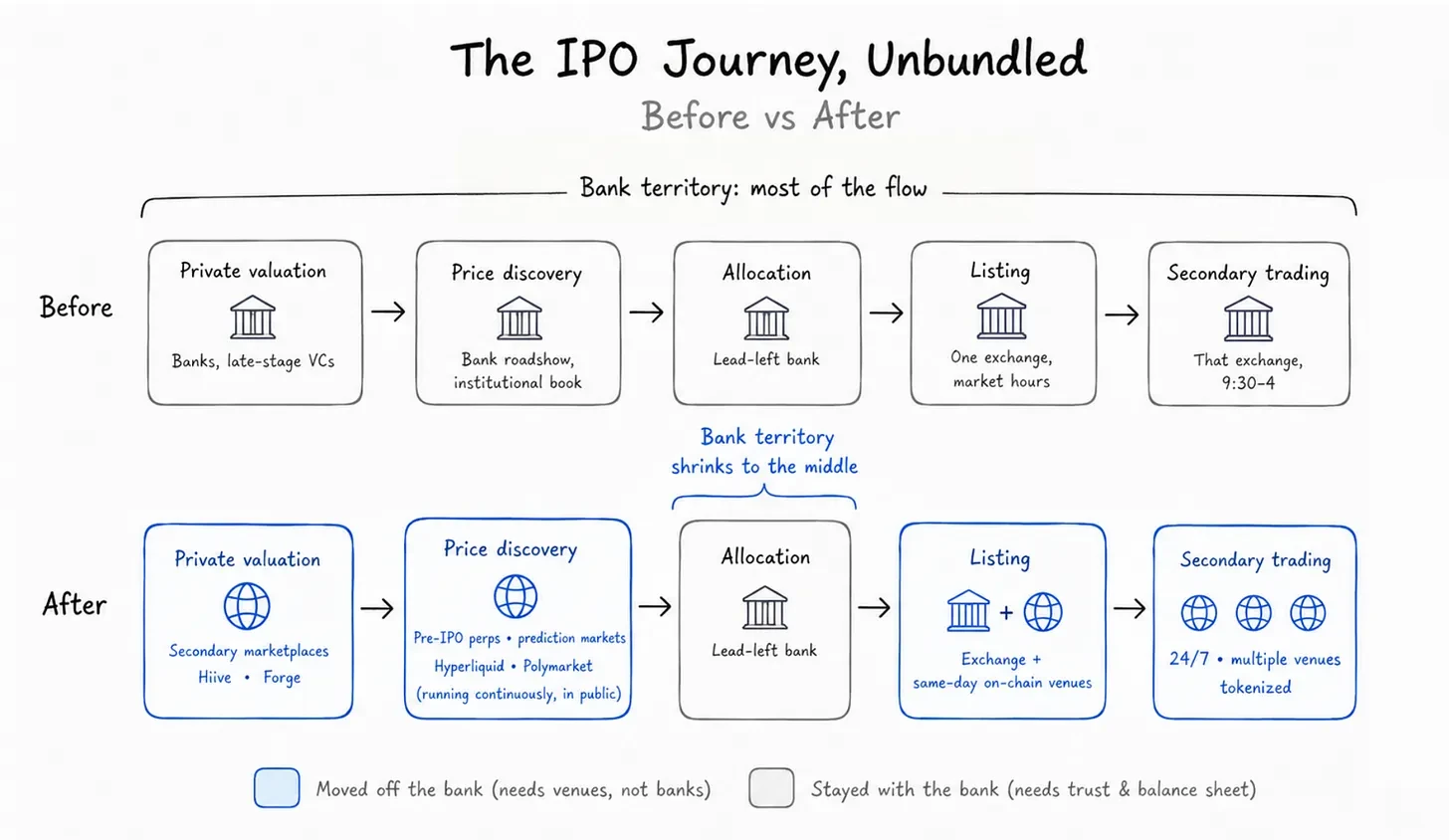

- Core Thesis: By unbundling the three core functions of a traditional IPO (price discovery, distribution and allocation, share settlement), and leveraging new public channels such as the secondary market, prediction markets, and perpetual contracts, SpaceX has completed its listing, challenging the monopoly of investment banks. This reveals that the future core value of investment banks will shift towards credit endorsement, share allocation rights, risk underwriting, and market stabilization.

- Key Elements:

- SpaceX's IPO breaks tradition: Musk directly set the offering price at $135, bypassing the investment banks' pricing process. Before the listing, the market had already formed a fair valuation through multiple public channels (such as Hiive, Polymarket, Hyperliquid).

- Validation of new pricing channel efficiency: For example, during the listing of chip company Cerebras, the price of Hyperliquid's IPO perpetual contract differed from the Nasdaq opening price by only 1.3%, proving that blockchain-based pricing channels can effectively predict stock prices.

- Tokenized share settlement exposes custody vulnerabilities: Platforms like Binance, failing to secure sufficient shares, resulted in a full refund of $557 million. The core issue lies in the actual existence and compliant custody of the underlying assets, not the blockchain technology itself.

- Underwriting fees drop to 0.67%: The extremely low fees for SpaceX's mega-IPO reflect that investment banks' bargaining power in standardized processes like price discovery has weakened. Their profit model is shifting from service fees to earning derivative trading commissions derived from share allocation rights.

- Investment banks' remaining irreplaceable functions: These include credit endorsement (e.g., Goldman Sachs and Morgan Stanley each charging $100 million), firm commitment risk underwriting (fully purchasing the issued shares), and market-making capabilities via the Greenshoe option to stabilize the market. These are functions on-chain platforms cannot replicate.

Original Author: Prathik Desai

Original Translation: Luffy, Foresight News

A company's IPO is a significant ritual in the capitalist system. Executives embark on multi-week roadshows, pitching business plans to fund managers to secure institutional investment. Investment banks act as underwriting intermediaries, aggregating market demand, evaluating company valuations, setting the final offering price, and completing share allocation. On the listing day, the bell rings, transforming a private company into a public one. Subsequently, the secondary market's buy and sell orders engage in continuous price discovery over hours or days.

The enduring existence of this process—roadshows, pricing, and bell-ringing—stems from the core issue that external parties cannot access the real operational data of private companies and must rely on investment bank pricing. In the past, every company had to fully complete this process to list on an exchange.

However, SpaceX, which recently listed on the US stock market, took a completely different path. Elon Musk directly set the offering price before investment banks began their pricing calculations and roadshows.

Traditional IPOs bundle three core tasks—price discovery, investor sourcing, and share settlement—for investment banks to handle collectively, paying them a bundled service fee. In contrast, SpaceX's listing completely decoupled these three stages, assigning them to different channels independently. Before the investment banks officially commenced the listing process, the market had already provided a fair valuation for the company, and a large number of investors were already queued up for subscriptions.

This article will deconstruct how SpaceX is changing the way companies go public and the evolving role of investment banks in this new environment.

The Origin of Investment Bank Underwriting Fees

Investment banks charge underwriting fees to companies planning an IPO. For nearly a century, this fee has typically been calculated as a percentage of the total funds raised.

The complete underwriting process includes: the investment bank organizes global roadshows, collects indications of interest from institutional and retail investors at various price ranges, determines the offering price the market can accept, and ensures the smooth settlement of shares. In a firm commitment underwriting, the bank buys the entire offering of shares from the issuer and then resells them to subscribing investors.

The long-standing bundling of the three functions—price discovery, distribution, and settlement—was a limitation of early market infrastructure. Investment banks were the only institutions with access to comprehensive market information and were best positioned to gauge demand. They had early access to the company's complete financial data and development plans, enabling precise stock price estimation. They possessed vast and diverse client networks and cross-industry channels to allocate shares to top institutions and retail investors, while also having mature clearing and settlement systems to guarantee smooth share delivery.

Therefore, companies going public had no choice but to purchase these services as a package and pay the associated fees.

The unbundled IPO has completely broken the monopoly of investment banks. Before banks even start preparing for the listing, public channels like perpetual contract trading platforms, prediction markets, and pre-IPO secondary markets have already fully displayed genuine market demand. Companies can now independently negotiate underwriting rates and select the most efficient service channel for each stage of the listing process.

The average underwriting fee for a mid-cap US IPO is about 7% of the total funds raised, while fees for large projects are significantly lower. For Alibaba's $25 billion IPO in 2014, the underwriting fee was only 1.2%. For this SpaceX listing, the underwriting fee was as low as 0.67%. While many factors could explain such a low fee for the largest IPO in history, the unbundling of the listing process and the diminished traditional role of investment banks are undoubtedly among them.

Price Discovery: Investment Banks Lose Pricing Power

SpaceX broke the traditional IPO rules from its preparation stage. In traditional processes, the investment bank sets a price range, gradually tests market acceptance, and finally determines the offering price. Musk, however, directly announced a fixed offering price of $135, leaving investors with only the choice to subscribe or pass.

SpaceX could bypass the bank's pricing role because the market had already autonomously valued the company weeks before the listing.

Three types of public markets provided price signals for SpaceX from different dimensions:

- Pre-IPO Secondary Markets (e.g., Hiive, Forge): Employees and early investors traded private shares, with the on-market price for SpaceX stabilizing around $150, close to the first-day opening price.

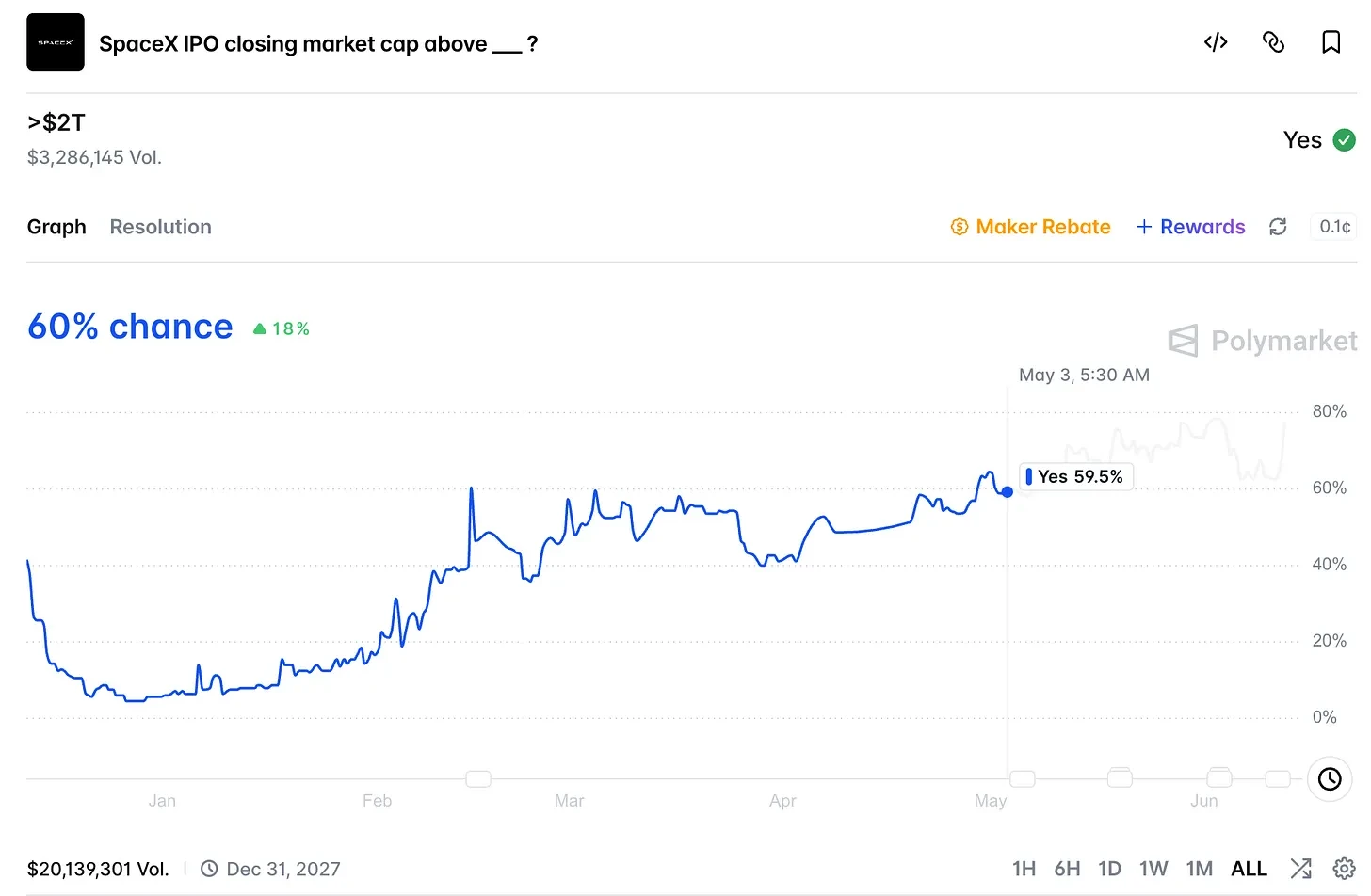

- Prediction Market (e.g., Polymarket): Users bet on the first-day closing price; the highest betting volume corresponded to a company valuation exceeding $2 trillion. On Friday, June 12, SpaceX officially listed, closing the first day at approximately $161, a 20% increase from the offering price, giving it a total valuation of $2.1 trillion.

- Hyperliquid Perpetual Contract Platform: Traded SpaceX synthetic perpetual contracts 24/7, reflecting real-time market valuation expectations for the stock.

Before the official listing, these pre-IPO perpetual contracts, lacking actual underlying stock, were essentially leveraged bets on the first-day stock price. The vast majority of positions on the Hyperliquid platform were concentrated in the SpaceX contract. During early trading on listing day, this perpetual contract price ranged from $174 to $185, a 30%–35% premium over the $135 offering price. Meanwhile, SpaceX stock peaked intraday at $176. After the stock officially began trading on the exchange, the perpetual contract price quickly converged towards the $150 opening price.

Is this just a coincidence? A previous case has proven the reference value of this new pricing channel. Weeks earlier, when chip company Cerebras went public, the corresponding IPO perpetual contract price on Hyperliquid differed from the actual NASDAQ opening price by only 1.3%, with the spread virtually disappearing after the stock opened. At that time, the company hadn't even finalized its offering price, yet the market had already pre-empted the opening price.

By leveraging various public trading markets, SpaceX bypassed the first core task handled by investment banks: price discovery.

Share Settlement: The Tokenization Track Exposes Underlying Custody Vulnerabilities

After pricing, the second core task of traditional investment banks is distributing shares and matching investors. Let's skip distribution for now and dissect the bank's third function: share allocation and settlement.

On the day of SpaceX's listing, stock trading was scattered across multiple platforms, a model completely different from a traditional IPO. Backpack issued tokens on Solana, US-regulated Kraken launched corresponding products, Ondo issued tracking tokens, and Hyperliquid listed synthetic perpetuals—all with SPCX as the underlying asset. Multiple centralized exchanges like Bitget, Bybit, and Binance also opened IPO subscription channels.

On listing day, different platforms saw vastly different outcomes.

Products that directly held physical shares or connected to them via compliant brokerage firms opened on time, with prices tracking the underlying stock. Backpack's Solana token was backed 1:1 by real shares held at a depository broker; Kraken's US segment connected to the stock via Payward Securities; Ondo provided daily asset custody certificates ensuring tokens were fully backed; and Hyperliquid's perpetual contract, which inherently didn't need to hold the stock, automatically synchronized its price after the listing.

Binance, Bybit, and Bitget launched tokenized subscription activities, with the xStocks platform promising tokens fully backed by real stock. However, these platforms ultimately failed to secure sufficient share allocations, resulting in full refunds. Binance alone refunded $557 million.

The root of the problem wasn't blockchain technology itself; compliant custody channels completed settlement without issue. The SpaceX offering was oversubscribed by 3.5 to 4 times the $75 billion fundraising target. Centralized exchanges relying on third-party intermediaries for share allocation experienced settlement failures, forcing full refunds.

When price discovery is completely open and freely accessible, pricing is no longer a scarce, high-value part of the IPO process. The core competitive factor shifts to the ability to deliver the corresponding shares in full.

The challenge of share settlement is not new. Wall Street faced a similar crisis 60 years ago and built the infrastructure to solve it permanently.

In the late 1960s, a surge in US stock trading volume, coupled with paper stock certificates requiring manual searching, checking, and delivery, overwhelmed back offices with mountains of paperwork. Exchanges had to close on Wednesdays just to process the backlog. The industry's eventual solution was to eliminate the circulation of paper documents.

The Central Certificate Service was established in 1968 and reorganized into the Depository Trust Company in 1973. All paper stocks were deposited into a central vault, with ownership recorded only through book-entry changes. With all assets held by a trusted third party, settlement risk was eliminated, as the depository could guarantee sellers held sufficient shares and buyers could complete the transfer.

This is also the core problem that custody infrastructure needs to solve: whether the seller genuinely holds the underlying asset and can complete the transfer.

Tokenization models face the same risk. Tokens can be issued in advance, but the underlying stocks may not be simultaneously deposited with a compliant custodian. If the tokens are backed by real stocks held in sufficient quantity by a brokerage, settlement is guaranteed. If tokens are sold first while the underlying shares aren't secured, the redemption promise becomes unsupported. The incident in 2026 occurred precisely because platforms issued tokens but couldn't obtain the corresponding physical shares afterwards.

The challenge for future IPOs will no longer be price discovery, but verifying the underlying asset's existence and its ability to be transferred smoothly.

What Irreplaceable Value Remains for Investment Banks?

Reviewing the entire new listing process, the three traditional functions have been absorbed by external channels.

Pre-IPO price discovery is no longer monopolized by investment banks. Weeks or even months before listing, pre-IPO secondary markets, prediction markets, and perpetual contract platforms continuously provide public valuations. By the time SpaceX finalized its offering price, multiple channels had already established fair market prices.

Listing and trading channels are no longer singular. While SpaceX listed on NASDAQ, multiple on-chain trading channels opened simultaneously. Blockchain supports 24/7 trading, meaning secondary market liquidity is no longer confined to a single traditional exchange.

The core barrier for share settlement is asset custody qualification. This capability, once exclusively held by investment banks leveraging depository institutions for settlement guarantees, can now be undertaken by any institution with compliant custody qualifications.

So, what still requires investment banks? Currently, they retain four intermediary core functions that are hard to replace.

First is credit endorsement. The name of the lead underwriter on the prospectus acts as a credit guarantee for the project, providing a safety net for conservative institutional investors. This reputation built over decades is something on-chain token platforms cannot replicate, and banks charge fees for this endorsement. In this SpaceX offering, the total underwriting fee paid was $500 million, with Goldman Sachs and Morgan Stanley each receiving $100 million, despite having little involvement in the pricing stage.

Second is share allocation authority. The lead underwriters still hold the power to decide on the allocation of the majority of shares, selecting which investors can participate.

Next is risk assumption. SpaceX used a firm commitment underwriting. The investment banks contracted to buy the entire offering, taking on the risk of distributing it. If market demand collapses and subscriptions are insufficient, the banks bear the loss of unsold shares. On-chain platforms cannot assume this massive downside risk.

Finally is market stabilization. In the early stages of listing with volatile prices, the lead underwriter can use the greenshoe option to overallot shares moderately and then repurchase them in the secondary market to curb extreme price swings. After the SpaceX listing, Morgan Stanley handled this post-market stabilization. This requires a large balance sheet and a professional market-making team, capabilities currently only possessed by investment banks.

Aside from these, the remaining parts of the entire listing process have been taken over by new market channels that are cheaper, offer longer trading hours, and are completely transparent.

Blockchain-based pricing channels have already proven their value, continuously estimating the valuation of companies going public around the clock, far surpassing the efficiency of traditional investment banks. SpaceX's significant oversubscription and nearly 19% first-day gain is a textbook IPO performance, confirming the effectiveness of the new pricing channels.

The traditional IPO model has been completely dismantled. Each function is now handled by the most efficient channel. Similar transformations in division of labor are occurring across industries. As noted in a previous article, "Pricing the Private", the market no longer waits for investment banks to value private companies. In the new listing ecosystem, banks, which once monopolized the core businesses of pricing and share settlement, can no longer charge high fees for these standardized services.

Will Investment Bank IPO Revenue Completely Shrink?

No. SpaceX's 0.67% underwriting fee is not the core source of investment bank income.

Based on the first-day gain, SpaceX raised $75 billion, with a single-day paper profit of approximately $14 billion. The investors who share this profit are mostly existing clients of the underwriting banks. Banks cannot directly hold shares for their own account, but they secure premium IPO allocations for their clients, thereby earning substantial trading commissions.

This is the core reason why nearly twenty investment banks competed for the underwriting role, despite the low 0.67% fee. The underwriting service fee has become a secondary consideration. Share allocation rights, client-derived trading commissions, and long-term wealth management business are the true prizes for which banks compete.

The profit model for investment banks is evolving, shifting from standardized, replaceable pricing services to a scarce resource: the channel for IPO share subscriptions.