休市定价误差0.13%,最后两分钟抢跑反弹:TradeXYZ的海力士周末

- Core Insight: The SK Hynix perpetual contract on the Hyperliquid chain achieved continuous trading during the Korean stock market closure and highly accurately predicted the Monday market open decline, demonstrating the potential of on-chain derivatives markets as a venue for price discovery ahead of traditional financial market closures.

- Key Factors:

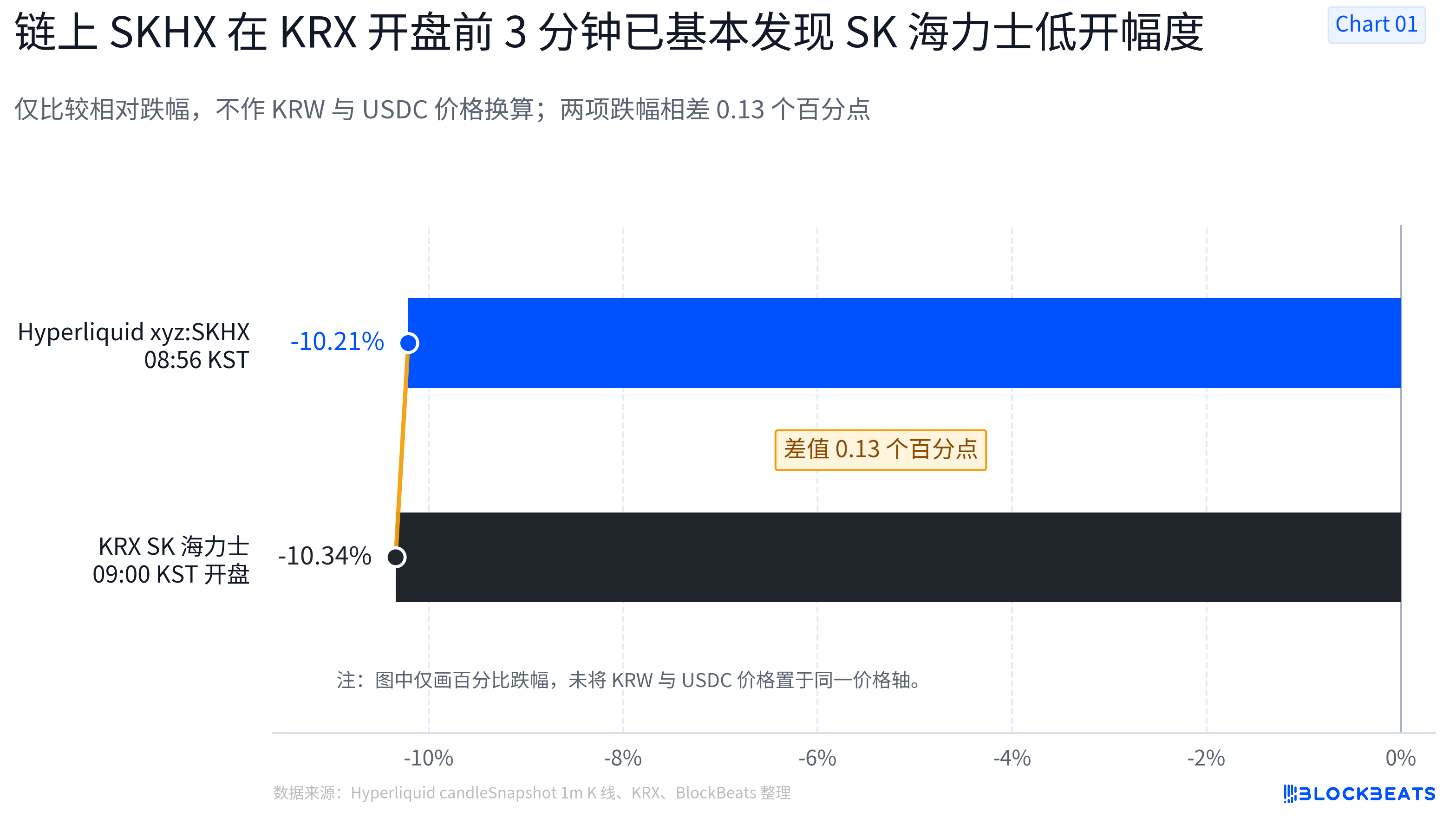

- On-chain price discovery accuracy reaches 0.13%: 3 minutes before the KRX opened, the lowest price decline of xyz:SKHX (-10.21%) differed from the actual opening decline (-10.34%) by only 0.13 percentage points.

- On-chain market pre-trades post-open trajectory: In the final 2 minutes before the market opened, the on-chain price rebounded +2.31%, highly synchronized with the rapid recovery of the underlying stock after the open (+2.64%), demonstrating its dynamic path discovery capability.

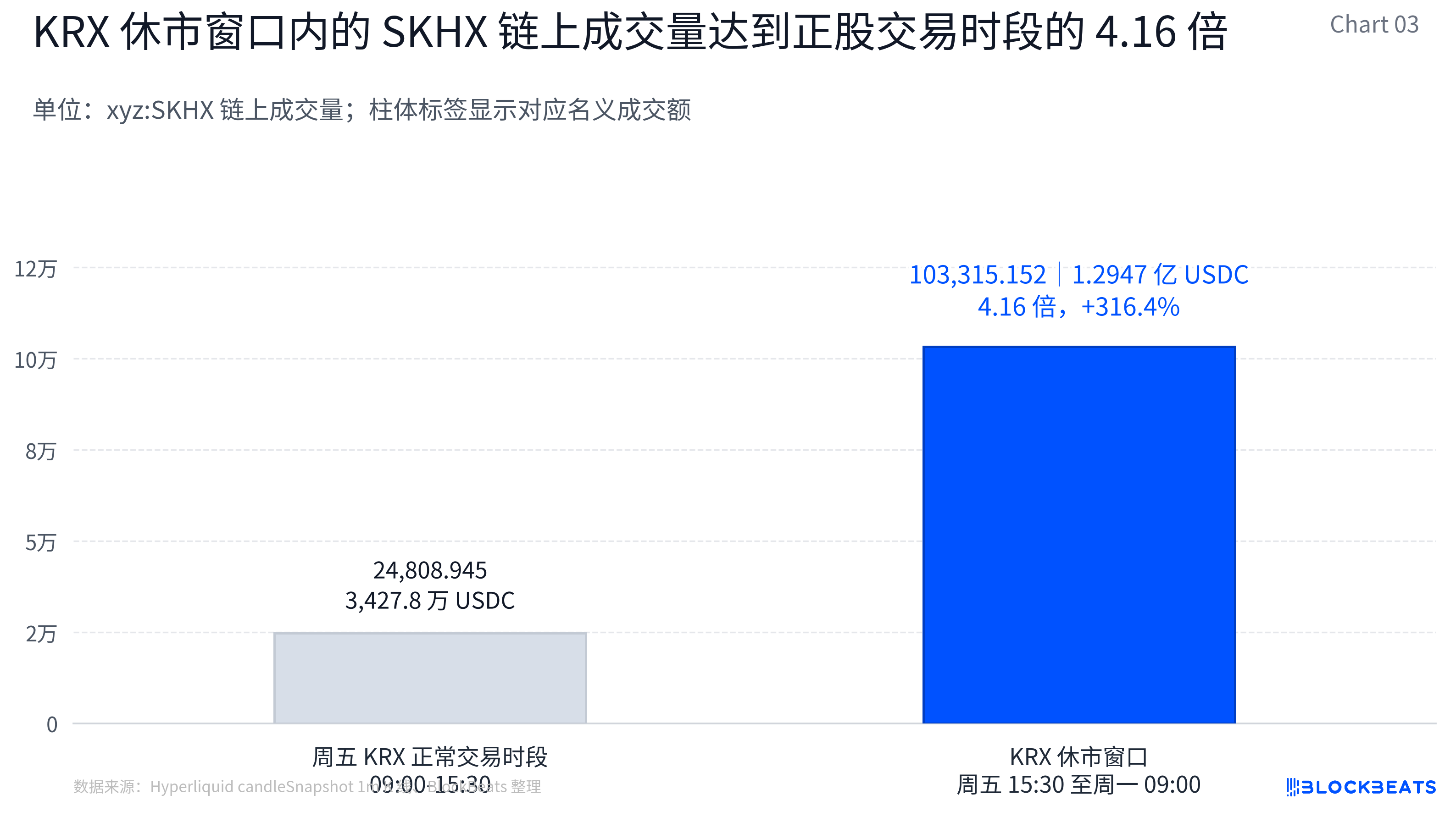

- Surge in trading volume during market closure: During the closure window from Friday's close to Monday's open, on-chain trading volume reached 129.47 million USDC, which is 4.16 times the on-chain trading volume during Friday's Korean stock market trading session.

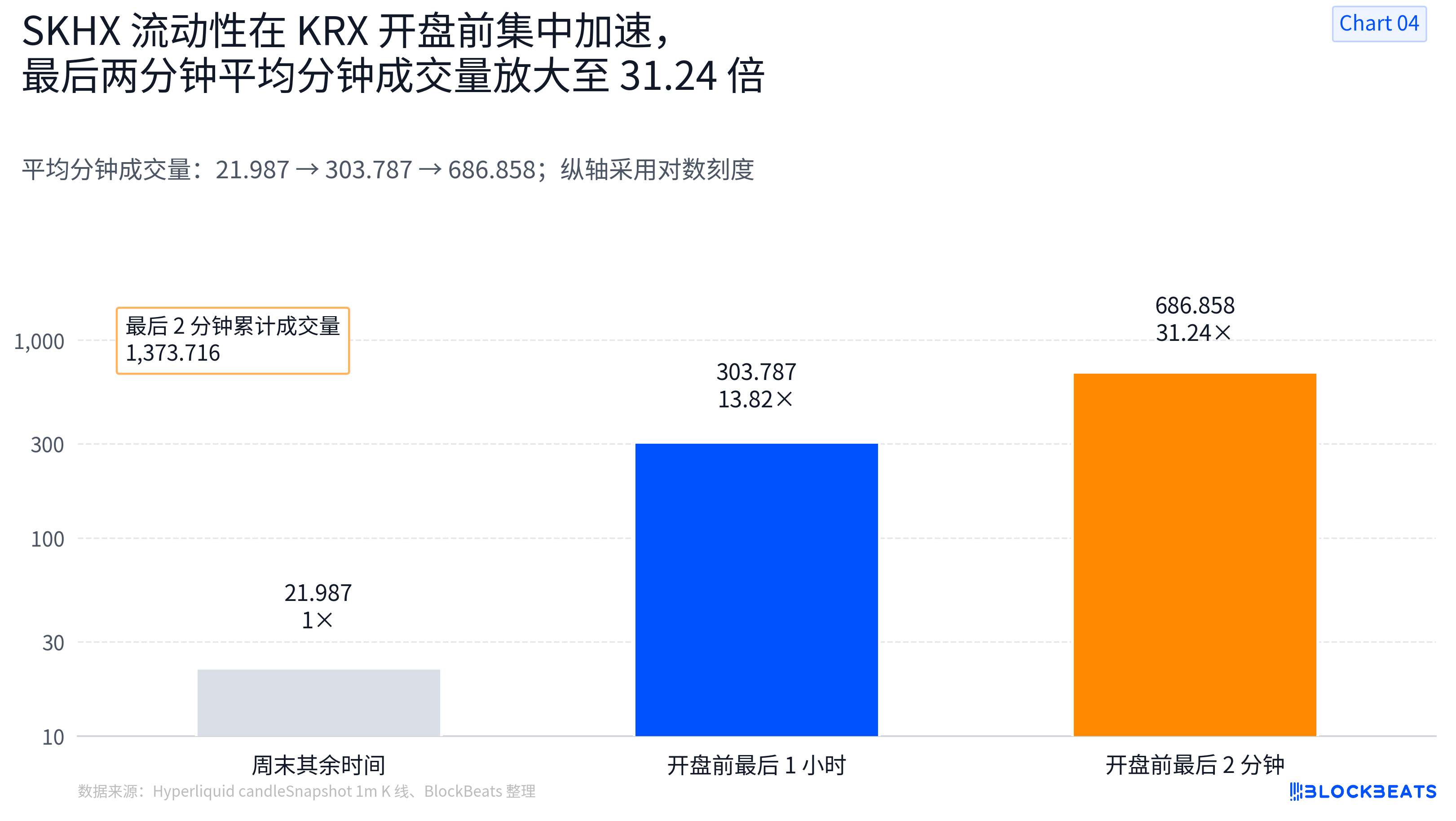

- Concentrated liquidity burst before the open: The average trading volume per minute in the final hour before the open was 13.82 times that of the rest of the weekend, and in the final 2 minutes it magnified to 31.24 times, indicating that concentrated pricing had already occurred before the market opened.

- Reasons for the strengthening of on-chain TradFi: 1) Meeting the demand for continuous expression of expectations during market closures; 2) On-chain pricing transcends emotional trading, providing precise quantitative reference value; 3) Traders utilize on-chain instruments for early hedging and arbitrage.

TL;DR

- During the Korean stock market holiday, the Hyperliquid SK Hynix perpetual contract continued trading continuously, pre-reflecting most of Monday's opening decline.

- Three minutes before the market open, the difference between the on-chain price decline and the actual opening decline was only 0.13 percentage points; the volume-driven rebound in the final two minutes was later confirmed in the underlying stock market.

- Related assets: SK hynix, Hyperliquid, TradeXYZ

In the past, traditional financial market closures typically meant a pause in price discovery. Assets like stocks, commodities, and ETFs would enter a quiet state after Friday's close, forcing investors to wait until the next trading day's open to see the true price impact of events.

But the on-chain derivatives market, pioneered by Hyperliquid, is changing this structure.

With Hyperliquid HIP-3 allowing external builders to deploy RWA perpetual contracts for stocks, commodities, and indices, certain traditional assets, represented by the XYZ market, can now trade 24/7 on-chain. While traditional markets are closed, on-chain markets continue matching orders, potentially becoming a front-end venue for risk expression and price discovery.

This past weekend, the on-chain price action of South Korean chipmaker SK Hynix provided a clear case study. The Hyperliquid xyz:SKHX contract did not just see sporadic trading during the KRX holiday. According to 1-minute candlestick snapshot data, both long and short sides executed a significant exchange of positions over the weekend.

By Monday, June 8th, just before the KRX officially opened, the on-chain market had already charted a complete weekend price trajectory.

Precision at 0.13%: SK Hynix's Weekend Price Discovery

On June 5th, the KRX-listed SK Hynix stock closed at 2,070,000 KRW. Subsequently, the Korean stock market entered its weekend closure.

According to Hyperliquid's 1-minute candlestick data, after Friday's close, the benchmark price stabilized around 1336.5 USDC. On Monday morning, just before the KRX open, the on-chain price showed significant volatility:

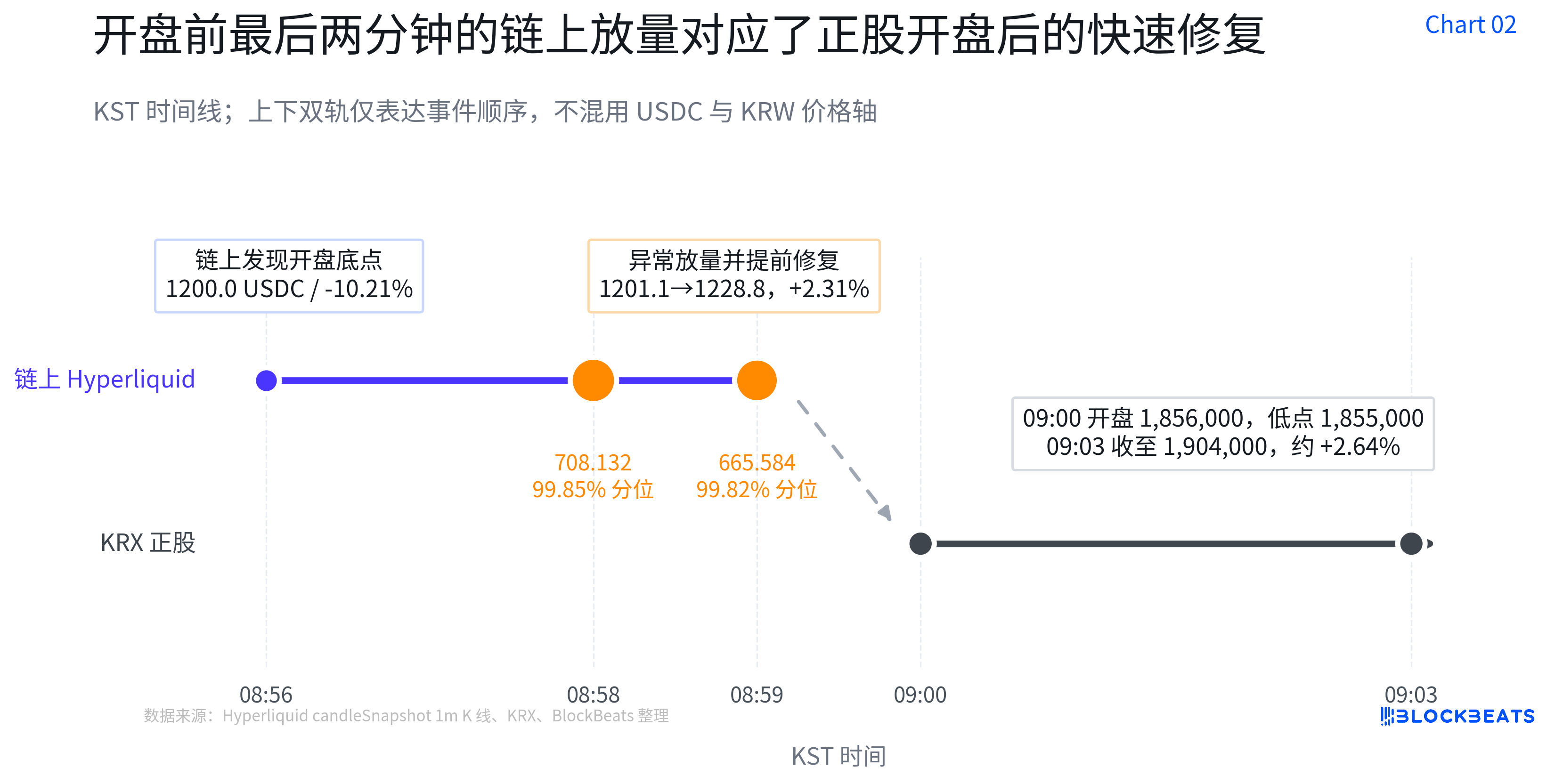

- Monday 08:56 KST (Korean Standard Time): xyz:SKHX dropped to a low of 1200.0 USDC, corresponding to a decline of -10.21%.

Three minutes later, the traditional KRX market officially opened, with the actual data being:

- Monday KRX Official Open: 1,856,000 KRW, corresponding to a decline of -10.34%.

The difference was only 0.13 percentage points.

This means that just 3 minutes before the KRX officially opened, capital in the on-chain market had almost perfectly discovered the magnitude of Hynix's Monday opening decline. It didn't vaguely signal a 'downward' direction; it precisely priced the decline near 10%, aligning remarkably closely with the actual opening result.

Key Reversal: Not a Prediction Failure, but Early Trading of Post-Open Moves

A second phase of market behavior then emerged, concentrated in the final 120 seconds before the open.

Between 08:58 - 08:59 KST, xyz:SKHX showed an abnormal surge in volume:

- 08:58: Minute volume reached 708.132, placing it in the 99.85th percentile of all weekend minute volumes;

- 08:59: Volume remained high at 665.584 (99.82nd percentile), with the price rising from 1201.1 USDC to 1228.8 USDC, a +2.31% rebound in two minutes.

If you only looked at the final price at 08:59, the on-chain price was about 2 percentage points higher than the subsequent actual KRX opening price. However, this doesn't mean on-chain price discovery failed. A more plausible explanation is that the on-chain market was already trading the anticipated post-open buying support for the underlying stock.

Looking at the actual KRX action after the open:

- KRX opened and dipped to a low of 1,855,000 KRW;

- 09:03 KST: The underlying stock price had recovered to 1,904,000 KRW, a rebound of approximately +2.64%.

BlockBeats Note: Superficially, the on-chain closing decline (-8.06%) differed from the underlying stock's opening decline (-10.34%) by about 2%. However, analyzing the timeline reveals a different conclusion. The on-chain market had completed its discovery of the 'opening low' by 08:56 (with a mere 0.13% error), and by 08:58, it had already switched to trading the 'post-open recovery' (with a highly synchronous rebound magnitude and pace).

On-chain market price discovery is not a static, single-point prediction; it demonstrates a continuous, dynamic path discovery capability.

Data Review: 4x On-Chain Volume Compared to Regular Trading Hours

Analyzing specific transaction data reveals a clear contrast in the Hynix on-chain perpetual contract's performance between regular Korean stock market hours and the weekend closure window.

During Friday's regular Korean stock market hours (09:00-15:30 KST), the Hynix on-chain perpetual saw 24,808.945 contracts traded. Estimated using minute-by-minute transaction prices, this corresponds to a volume of approximately 34.278 million USDC.

During the closure window from Friday's Korean market close to Monday's open (15:30-09:00 KST), the cumulative contract volume reached 103,315.152 contracts, corresponding to approximately 129.47 million USDC.

This means that during the period when Hynix's underlying stock was untradeable over the weekend, its on-chain perpetual contract's trading volume was 4.16 times the on-chain volume seen during Friday's regular Korean stock market trading session, an increase of approximately 316.4%.

An even more significant acceleration in liquidity occurred just before Monday's open:

- Last 1 Hour Before Open: Excluding the final hour, the Hynix on-chain perpetual averaged about 21.987 contracts per minute over the weekend. In the final hour before Monday's open, the average minute volume surged to 303.787 contracts, a 13.82x increase (approximately 1281.7%).

- Last 2 Minutes Before Open: The cumulative volume from 08:58-09:00 KST was 1,373.716 contracts, averaging about 686.858 contracts per minute. Compared to the average minute volume during the rest of the weekend, this represents a 31.24x increase (approximately 3024%).

This data indicates that price discovery does not happen only in the instant of the traditional market's open. In the on-chain market before the open, trading volumes had already dramatically expanded, and concentrated pricing had already occurred in advance.

Why is On-Chain TradFi Becoming Powerful?

First, there is a continuous need for directional expression during market closures.

Previously, when the KRX closed, the underlying stock price stopped moving, and market participants had to wait for the next trading day to digest information. However, volatility in the US semiconductor sector, changes in macro liquidity, and sentiment around the AI supply chain continued to evolve. The on-chain perpetual market provided a continuous trading window for this void, allowing traders to continue expressing their price expectations during the traditional market closure.

More notably, on-chain pricing has already moved beyond mere emotional reaction.

If it were purely sentiment-driven, prices would only roughly reflect the direction of risk. However, the lowest price of xyz:SKHX three minutes before the KRX open differed from Monday's actual opening price by only 0.13 percentage points. This level of precision suggests that capital participating in on-chain trading may include high-net-worth individuals or quantitative strategies, whose sophisticated pricing models give on-chain prices genuine reference value.

Furthermore, the pre-open volume surge reveals the market's ability to proactively process complex information.

The significant volume increase in the final hour, especially the final two minutes, indicates that certain traders or quant strategies were pre-digesting the price reaction for the open. They were not passively waiting for the KRX to open; they were proactively hedging and arbitraging potential opening volatility on the chain.

In summary, the power of on-chain TradFi is gradually emerging. It not only provides a continuous trading channel when traditional markets are closed but also begins to shoulder part of the price discovery function. Its precision and information-processing capabilities are increasingly approaching traditional market reference standards.

Limitations and Future Potential

Undeniably, current on-chain TradFi still has significant limitations.

First, liquidity distribution is highly uneven. The massive volume in the final two minutes suggests that capital concentrates only during critical moments. At other times, the order books may be thin and susceptible to price distortion by a small number of players. Second, asset coverage is limited. The precision demonstrated here is currently confined to popular heavyweights like Hynix, Samsung, and major US tech stocks. Long-tail assets often lack sufficient liquidity for on-chain perpetuals. Additionally, due to the lack of tick data and more granular taker/maker depth profiles, it remains impossible to fully reconstruct the entire dynamic of aggressive buying and selling.

However, the future potential it exhibits is also clear.

As more professional liquidity providers (LPs) and cross-market arbitrageurs enter the HIP-3 market, minute-level on-chain volumes may become more stable. As more stocks, ETFs, commodities, and indices are connected, the on-chain market could gradually evolve into a cross-asset, cross-timezone, uninterrupted price discovery network.

The weekend market is no longer silent. As the traditional financial world closed on Friday, the market had already completed its first round of pricing on-chain and began trading the next phase of the post-open movement. On-chain perpetuals are becoming an unavoidable 'front-end oracle' in the global asset pricing system.