从Coinbase到Upbit:一个代币如何走完28天的接盘之路

- Core Thesis: In the 2026 bear market, CEX listings have shifted from being traffic-driven to verification-driven, forming a structured path: Coinbase/ByBit (Discovery) → Binance Perps (Verification) → Binance Spot (Confirmation) → Korean Exchanges (Late-Stage Entry). Listing events now represent a redistribution of existing capital rather than a catalyst for new inflows. Investors can use this pattern to identify Alpha opportunities.

- Key Elements:

- Coinbase, ByBit, and Binance Perps are the first-tier listing venues, with 67%, 39%, and 48% of their listed tokens being debut listings respectively, serving the function of price discovery. Binance Spot listed only 19 tokens, with a debut rate of 28%, prioritizing security verification.

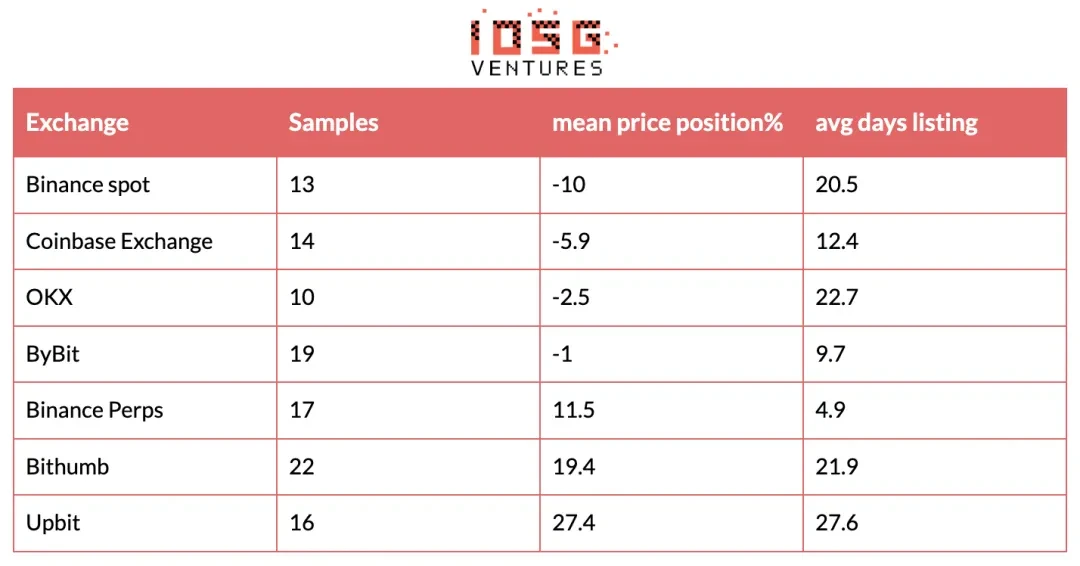

- Korean exchanges (Bithumb, Upbit) are systematically positioned at the end of the listing path, with an average delay of approximately 28 days from the debut. Their follow-on listing rates are as high as 85%, often at elevated price levels, causing users frequently to buy at the peak (Upbit's entry premium can reach 27.4%).

- The key signal preceding a Binance Perps listing is the listing activity on Coinbase and ByBit (with conversion rates of 75% and 70%). Binance Perps responds swiftly (average of 4.9 days) and preferentially selects trending projects with stable price performance, avoiding tokens that are consistently weakening or are excessively speculative.

- Price performance post-listing is generally under pressure: the 30-day average return across all exchanges is negative, with losses gradually deepening, reflecting liquidity distribution rather than growth. First-mover exchanges (e.g., ByBit) see average peak returns of +86%, while subsequent exchanges (e.g., OKX) achieve only +25%.

- The choice of exchange significantly impacts the risk-return profile. Users on first-mover exchanges (Coinbase/ByBit) enjoy the lowest entry prices and highest peak potential, while users on Korean exchanges face the risk of buying at the top and experiencing deep drawdowns (30-day return of -25.7%). The difference in profit and loss can reach 4.5 percentage points.

Original Author: Xinyang & Ethan @ IOSG

Every bear market quietly reshapes the listing logic of CEXs. When liquidity tightens and retail enthusiasm wanes, every listing decision by exchanges becomes more prudent, and thus carries more signal value. We have systematically tracked the new listing data from six major first-tier exchanges — Coinbase, Binance Spot, ByBit, OKX, Bithumb, and Upbit — as well as Binance Perpetual, from 2026 to mid-May. This dataset comprises 207 listing records covering 92 unique tokens. The data clearly reveals a core fact: listings follow a highly structured path of validation and liquidity transmission.

Who discovers and prices a project first? Who picks up and amplifies liquidity in the middle? Who completes market coverage at the end? Different exchanges play distinctly differentiated roles along this chain. By the time a token is finally listed on Binance Spot, it has often undergone multiple rounds of exchange validation. This report will break down this listing path from three core dimensions:

- Landscape and Pathways: The differentiation of exchange roles in listings and the rules governing token flow between exchanges

- Binance Perps' Screening Logic: What types of tokens are more likely to enter Binance Perp

- Price Impact: How listing timing determines investors' entry positions, and the actual return differences after listings on various exchanges

For projects, understanding this path means more precise and efficient exchange listing strategies; for investors, recognizing positional differences along the path could be one of the most important Alpha sources in 2026.

2026 CEX Listing Landscape and Pathways

Overview of Listings by Exchange

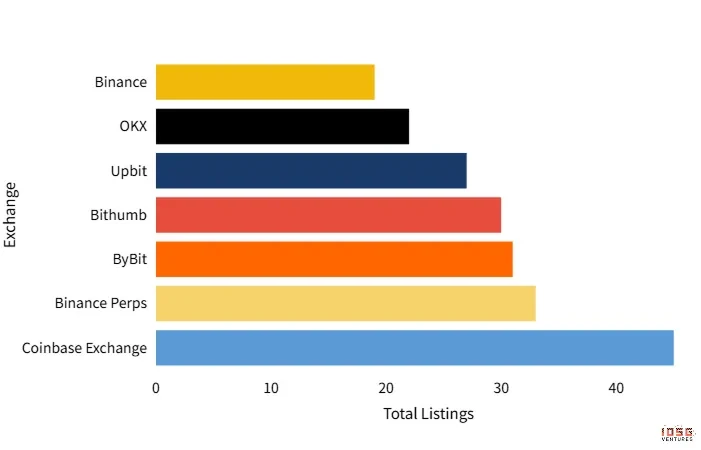

▲ Total Listings by Exchange

From 2026 to date, we have tracked new listing data from the six major first-tier exchanges (Coinbase, Binance Spot, ByBit, OKX, Bithumb, Upbit) and Binance Perp, totaling 207 listing records covering 92 unique tokens.

The number of listings by exchange shows a clear stratification. Coinbase leads firmly with 45 new listings, followed closely by Binance Perps (33) and ByBit (31). Bithumb (30) and Upbit (27) form the second tier, OKX has 22 listings, while Binance Spot has listed only 19, the fewest among all observed exchanges.

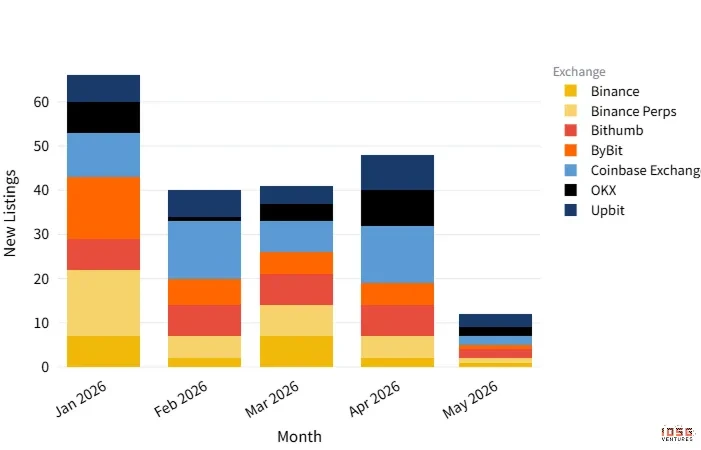

From a monthly perspective, January was the peak period for listings across the year. Binance Perps listed 15 tokens in a single month, and ByBit listed 14. Since February, the overall pace has slowed significantly, with the average monthly listings per exchange dropping to 5-8, entering a more cautious and stable selection phase. Coinbase, however, has shown a listing rhythm out of sync with other exchanges, experiencing two concentrated listing peaks in February and April (13 listings per month), demonstrating its independent and swift listing decision-making characteristics.

▲ Monthly Listings by Exchange

Simple quantitative differences only reflect surface-level activity. More important is the profound differentiation in listing timing and roles among different exchanges, which will be further analyzed in subsequent sections.

Role Differentiation in Listings: Discoverers, Screeners, and Confirmers

For tokens listed on multiple exchanges, there is a significant order of precedence. We define the earliest listing exchange within our tracking scope as the "Pioneer" and the rest as "Followers".

Coinbase is the most prominent pioneer listing venue in 2026. 67% of its tokens were pioneers among the tracked exchanges, bearing the function of the market's first round of price discovery. ByBit (39% pioneer rate) and Binance Perps (48% pioneer rate) also maintain high activity levels. These three often intensively list the same token within the same week, collectively forming the first tier for new project listings.

Korean exchanges (Bithumb and Upbit) are systematically at the end of the listing path. Bithumb's Follower ratio is as high as 85%, and Upbit has an average rank of 4.44, with a high probability of being the last to list among all exchanges, averaging about 28 days after the pioneer exchange. This is closely related to the lengthy regulatory review process in Korea and the local exchanges' preference for introducing projects only after they have gained widespread consensus.

Binance internally forms a clear funnel-like division of labor: Binance Perps initiates listings half the time, while the other half it follows up extremely quickly after the spot listing (average of only 4.9 days), making it the most responsive of all exchanges. Its main role is to quickly test liquidity and market demand through the derivatives market. Meanwhile, Binance Spot lists the fewest tokens (only 19), with a pioneer rate of only 28%, clearly tending to wait for sufficient market validation before selectively listing.

OKX, on the other hand, shows a relatively strong independent token selection ability, with a pioneer rate of 55%. However, its overall number of listings is relatively restrained (22), with an average rank of 3.58, indicating a high screening threshold and a more prudent strategy.

Listing Path Paradigm

From the sample of tokens covered by 3 or more exchanges, the listing order exhibits highly stable tier characteristics: early discoverers represented by Coinbase and ByBit initiate listings first, Binance Perps follows up within days for rapid validation, then Binance Spot selectively lists for confirmation, while OKX, Bithumb, and Upbit mainly provide supplementary coverage later in the path.

Typical Case: ROBO (Fabric Protocol)

On February 27th, the DePIN project Fabric Protocol (ROBO) was first listed on Binance Perp. Coinbase and ByBit followed up on the same day. The opening price was $0.022, and it surged over 80% on its first day. The next day's opening price had already risen to $0.0405, nearly doubling from the initial listing price. The project, led by Pantera Capital with a $20 million investment, focuses on the intersection of blockchain and the robotics economy. It quickly gained market attention, combined with the Kaito public sale hype and the "AI + Robotics" narrative.

On March 5th, Binance Spot officially listed ROBO, with the closing price reaching $0.0493 on that day. This became the all-time high price for ROBO during this cycle. Subsequently, when OKX listed, the opening price was already lower than the Binance Spot price. On March 18th, Bithumb listed at a price of $0.0303. Although it briefly sparked a rally, the token price has since declined continuously and is currently below the initial listing opening price.

From the first listing to the Bithumb listing, ROBO took only about 20 days to complete a typical 2026 listing path:

Binance Perps, Coinbase & ByBit pioneer → OKX & Binance Spot confirm at the peak → Korean exchanges catch the tail end.

ROBO is not an isolated case. In the sample from the first five months of 2026, 28 tokens completed listings on 3 or more exchanges. The rank distribution of these cross-exchange cases consistently shows the same tier regularity as ROBO. Although the specific order may vary slightly depending on project attributes, the overall path structure is stable and predictable.

This path clearly reflects the differing risk appetites of each exchange: Coinbase, ByBit, and Binance Perps tend to proactively seize the early window, Binance Spot emphasizes post-validation safety, while Korean exchanges and OKX prefer to enter only after the market has formed sufficient consensus.

Binance Perps Listing Conditions

As a key entry point for the derivatives market, Binance Perps' listing decisions directly influence the flow direction of significant leveraged capital. Through the analysis of 33 Perps listing cases, we can clearly distill the core logic behind Binance's token selection in a bear market environment.

Leading Signals: Listings on Coinbase and ByBit

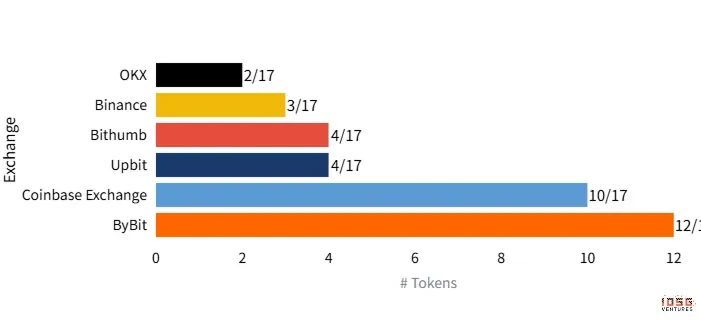

▲ Exchanges Listed Before Perps

Of the 33 tokens that entered Binance Perps, 17 were first listed on other spot exchanges before being included in Perps. Tracking these tokens shows that Coinbase and ByBit are the most significant leading signals for Perps.

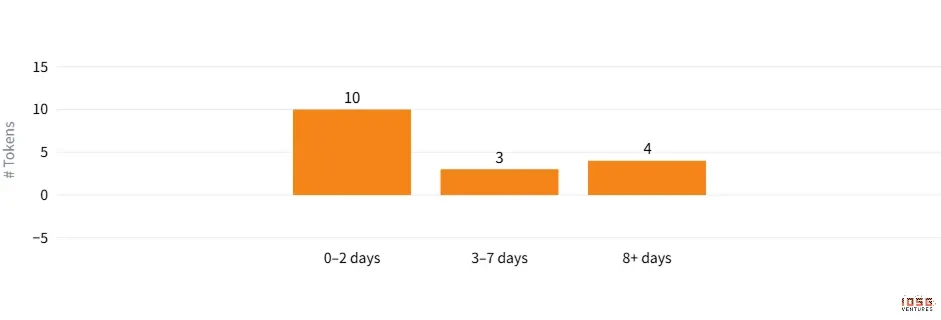

▲ Days from First Spot to Perps

Among them, ByBit listed before Perps in 71% of cases, and Coinbase in 59% of cases. More importantly, the response speed is critical: in the 17 follower listing cases, 10 were listed on Perps within 0-2 days after the spot listing, with an average delay of only 4.9 days. This extremely rapid follow-up indicates that Binance Perps closely monitors the listing activities of Coinbase and ByBit, using them as important decision-making references.

Looking at a broader sample, 75% of tokens listed on Coinbase eventually entered Binance Perps, compared to 70% for ByBit. When a token simultaneously gains support from both Coinbase and ByBit, and its price performance is relatively stable, it is highly likely to land on Binance Perps within a week. This is currently one of the strongest and most directly observable leading signals in the market.

Price Performance is the Most Critical Screening Standard

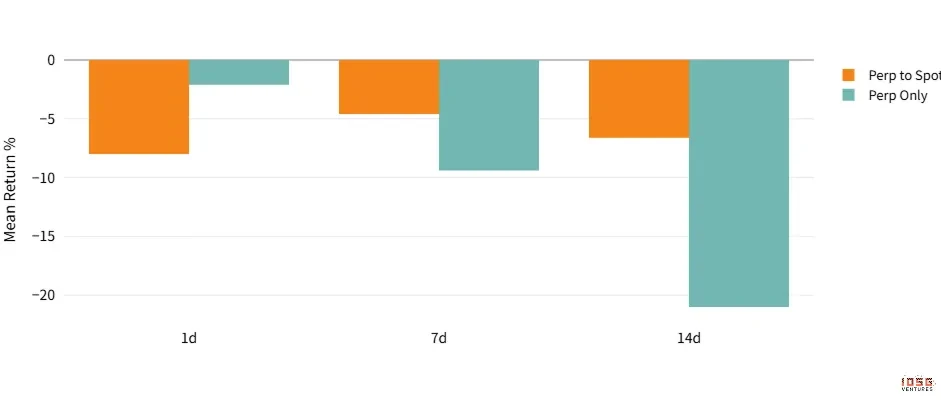

▲ Post-Listing Mean Return (Converted vs Perp Only)

The opening FDV of projects listed on Coinbase and ByBit is generally above $100M, so FDV itself does not constitute a differentiating factor. What truly determines whether a token can enter Perps is its price performance after listing.

Looking at tokens listed on Coinbase and ByBit but which did not enter Perps, they primarily exhibit three characteristics:

- Projects with continuously weakening prices and lacking market heat after listing;

- Meme coins with excessively strong speculative attributes (e.g., WHITEWHALE, ELON), where Binance's screening is significantly stricter than ByBit's;

- Tokens that have not passed through Binance Alpha. Alpha serves as a pre-screening channel within the Binance system and is an important prerequisite step for entering Perps.

The impact of price performance extends beyond "whether it can get into Perps" to the subsequent "Perps to Spot" transition. Data shows that tokens that eventually successfully transitioned to Binance Spot (Converted group) had a 7-day return of -4.6% and a 14-day return of -6.6% after Perps listing. In contrast, tokens that did not transition to Spot (Perp Only group) had a 7-day return of -9.4% and a 14-day return that fell sharply to -21.0%. Although both groups show negative returns due to the bear market, the price maintenance ability of the Converted group is significantly stronger, indicating that Binance uses "sustainability" as an important consideration during the Perps phase.

Price Impact of Listings

The actual impact of a listing event on a token's price is the most concerning issue for projects, institutions, and traders. We analyze this from two core dimensions: Price Position (the relative price level at the time of listing) and Post-Listing Return (returns 7, 14, and 30 days after listing).

Price Discovery Concentrated in the Pioneer Window, but Significant Differences in Entry Prices Across Exchanges

▲ Price Position at Listing

Price discovery mainly occurs during the pioneer window. When ByBit and Coinbase act as followers, their entry prices are roughly the same or slightly lower than the pioneer price, indicating rapid price convergence among first-tier exchanges.

When Binance Perps acts as a follower, its average price is already 11.5% higher than the pioneer. However, thanks to its extremely fast follow-up speed (only 4.9 days), it remains in a relatively early position. Binance Spot's Price Position is -10%, indicating a tendency to list only after a price correction, allowing users to potentially get a relatively better entry price.

Korean exchanges face the most unfavorable entry positions: Bithumb averages 19.4% higher, and Upbit is as high as 27.4%. Due to an average delay exceeding three weeks, users often buy at significantly inflated prices.

Overall Post-Listing Pressure in 2026: Liquidity Release, Not Growth Catalyst

▲ Mean Return by Exchange 7d/14d/30d

In the 2026 bear market environment, the overall price performance after new listings is weak, with no exchange achieving a positive 30-day average return.

The decline deepens progressively from 7d to 30d, indicating that the price drop after listing is not a short-term fluctuation but a sustained downward trend. In the current market environment, new listings primarily act as a mechanism for liquidity distribution — providing an exit window for early holders (including project teams, investment institutions, and early traders) rather than attracting sustained inflows of new capital.

The performance of the two Korean exchanges is particularly noteworthy: Upbit's 7d return is already -13.5%, and its 30d return reaches -25.7%. Combined with its +27.4% price position, this means Upbit users not only entered at the highest price but also suffered the deepest declines.

Peak Price Performance Under the Listing Path

Although the final return after 30 days is generally negative, the rebound peak (Peak Return) in the initial period after listing shows a distinctly different distribution structure. By breaking down the price data of tokens, we find that the listing sequence directly determines the upper limit of short-term speculative space.

▲ Peak Return by Exchange (14d High)

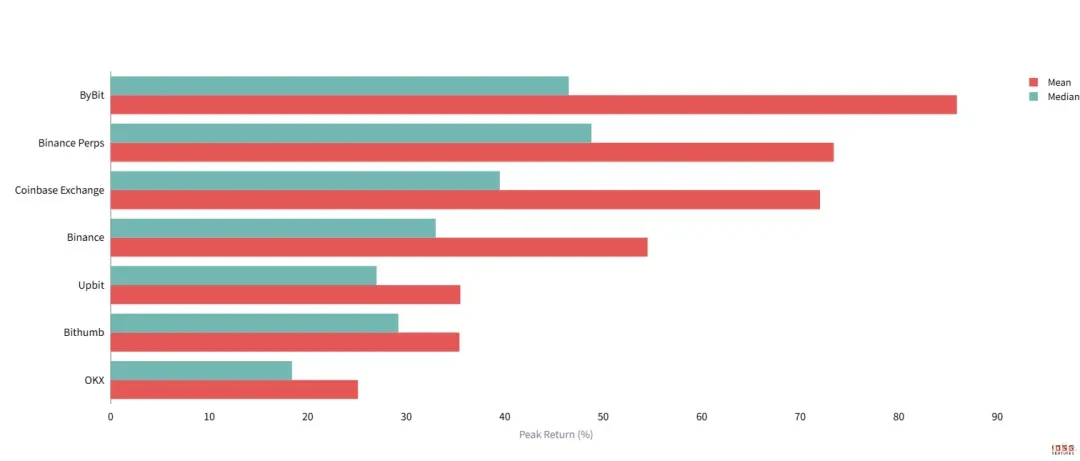

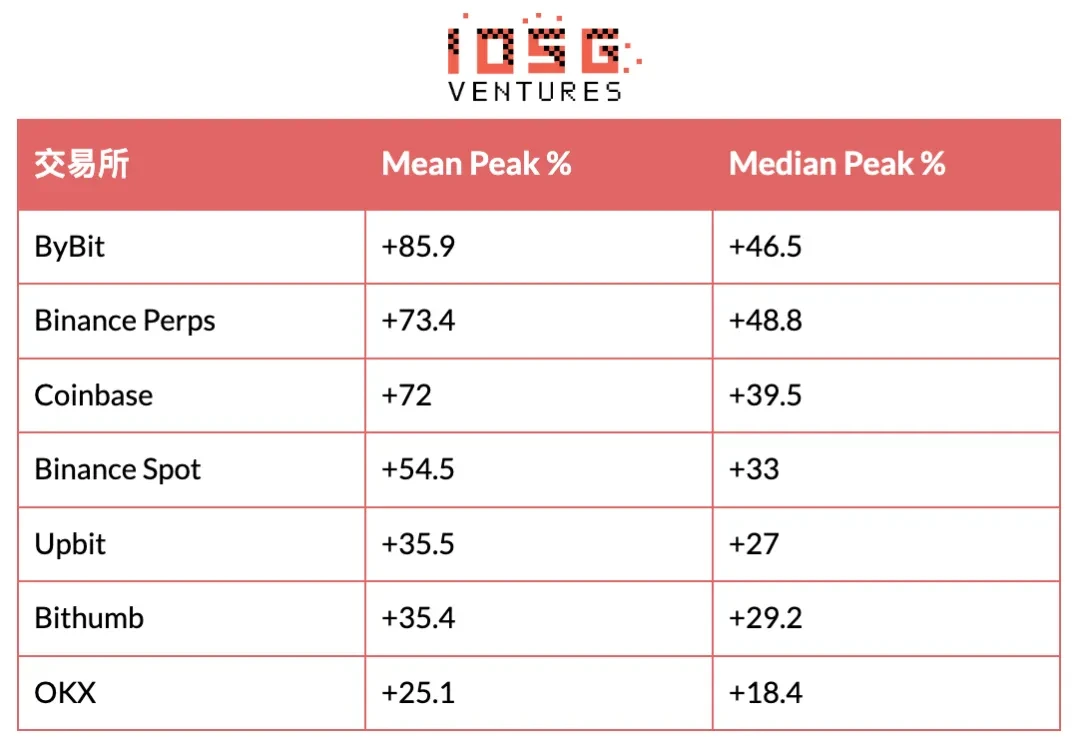

Pioneer exchanges hold an absolute advantage: ByBit's average peak reaches +86%, and Binance Perps' median is the highest (+49%). The first tier of listings (ByBit, Coinbase, Binance Perps) captures the highest price elasticity, providing a significant liquidity premium for early chips. Even if the price eventually goes to zero, there is ample time to exit at the peak.

Late followers have limited space: The peaks for Bithumb and Upbit are constrained to around +35%, while OKX's is only +25%. Due to delayed entry timing, the buying pressure on these platforms mainly serves to absorb profit-taking from earlier holders rather than initiating a rally.

This difference confirms the transmission path of liquidity: Pioneer exchanges bear the main function of price discovery, providing the best exit liquidity for early holders. As time passes, the buying pressure on subsequent exchanges is more about absorbing already realized gains, leading to diminishing marginal utility. For traders, this means the later one enters the listing cycle, the lower the probability of capturing excess returns.

Exchange Choice Determines Risk-Return Structure

Combining the three indicators — Price Position (entry point), Peak Return (peak space), and Mean Return (final return) — users on different exchanges face entirely different risk-return structures.

Users on pioneer exchanges (Coinbase/ByBit) also face negative returns but have the best risk buffer. With the lowest entry prices (-10% to -5.9%) and the highest peak space in the market (average of +70% or more), even without perfectly timing the top exit, the absolute loss from the pioneer price is relatively controllable. They even have an opportunity to take profits during the uptrend.

In contrast, users on Korean exchanges face a classic "buy high, suffer deep