火币成长学院|TradFi深度研报:加密与传统金融的融合浪潮

- 核心观点:TradFi加密化正从概念验证进入产品矩阵化阶段,通过永续合约、代币化资产等路径将传统金融引入链上,市场规模快速增长,但合规与流动性风险仍为核心挑战。

- 关键要素:

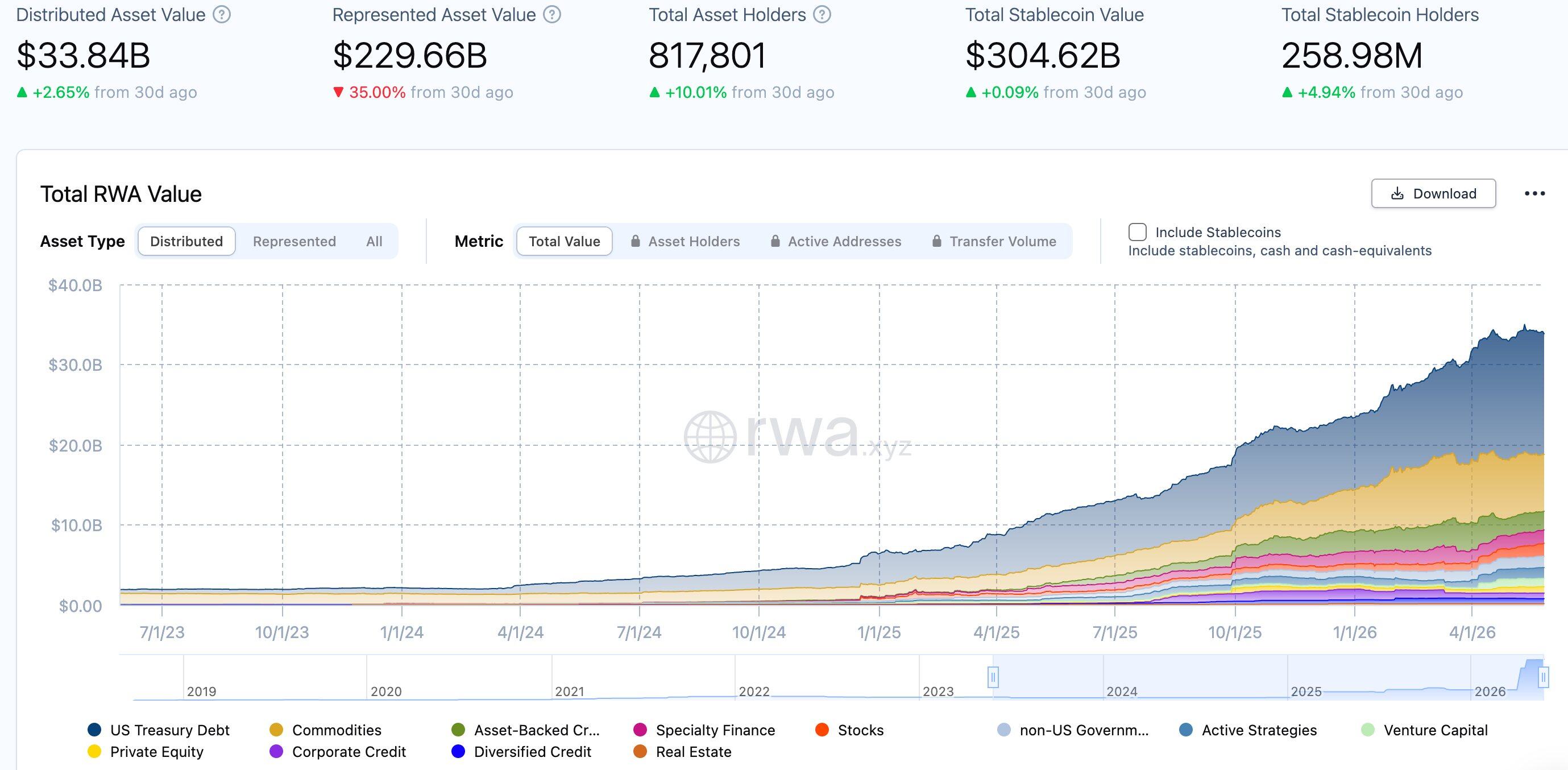

- RWA市场TVL在2026年5月达310-340亿美元,较一年前增长近3倍;RWA永续合约Q1 2026交易量达5248亿美元,超越2025全年。

- BlackRock BUIDL基金以23亿美元AUM占据代币化国债赛道龙头地位,富达、瑞士银行等传统托管机构开始参与。

- Coinbase于2026年3月推出美股永续合约,HTX上线NVDA、AAPL等核心美股永续合约,推动7×24小时链上交易。

- 代币化股票市值从200万美元增至4.86亿美元,增长逾200倍;BCG预测2030年代币化资产市场规模可达16万亿美元。

- 主要风险包括监管碎片化(如SEC态度模糊)、流动性错配(衍生品与现货深度失衡)、智能合约漏洞及托管信用风险。

- 创新趋势包括永续合约矩阵扩展、许可制DeFi池兴起、MiCA等监管框架明确化,以及机构级基础设施成熟。

- 投资者参与路径包括直接交易TradFi永续合约、投资RWA协议代币(如ONDO)及布局提供交易基础设施的交易所平台。

1. Definition of TradFi and the Evolutionary Logic of Crypto

TradFi, which stands for Traditional Finance, in the crypto context specifically refers to the process of introducing traditional financial assets—including stocks, bonds, commodities, foreign exchange, ETFs, etc.—into the crypto market for trading through tokenization or synthetic assets.

This concept did not emerge in 2026, but its development has gone through three distinct phases.

The first phase was the "Synthetic Asset Experimentation Period" from 2020 to 2022. During this time, Mirror Protocol and Synthetix were among the first to launch on-chain synthetic stocks, while FTX and Binance offered tokenized stock trading services through partnerships with licensed brokerages. However, the collapse of FTX in 2022, coupled with a global tightening of crypto regulations, forced most tokenized stock services offline, marking the end of this phase with an industry shakeout.

The second phase was the "Treasury-led Period" from 2023 to 2024. In the environment of aggressive interest rate hikes by the Federal Reserve, DeFi protocols like MakerDAO began using U.S. Treasury bonds as underlying RWA assets. BlackRock launched the BUIDL fund in March 2024 with an initial seed capital of $100 million, which grew to over $1 billion within months, signaling the formal entry of Wall Street giants.

The third phase, from the second half of 2025 to the present, can be described as the "Full Asset Acceleration Period." Tokenized stocks have re-entered a growth trajectory. MyStonks completed U.S. STO compliance filings, Backed Finance issued xStocks backed by real assets across 9 blockchains, and traditional custodians like Fidelity and UBS have begun participating. More importantly, crypto exchanges are no longer satisfied with merely listing tokenized assets; they are directly launching TradFi perpetual contract products, introducing traditional assets like U.S. stocks, gold, and treasury bonds into the 24/7 on-chain trading ecosystem in derivative form.

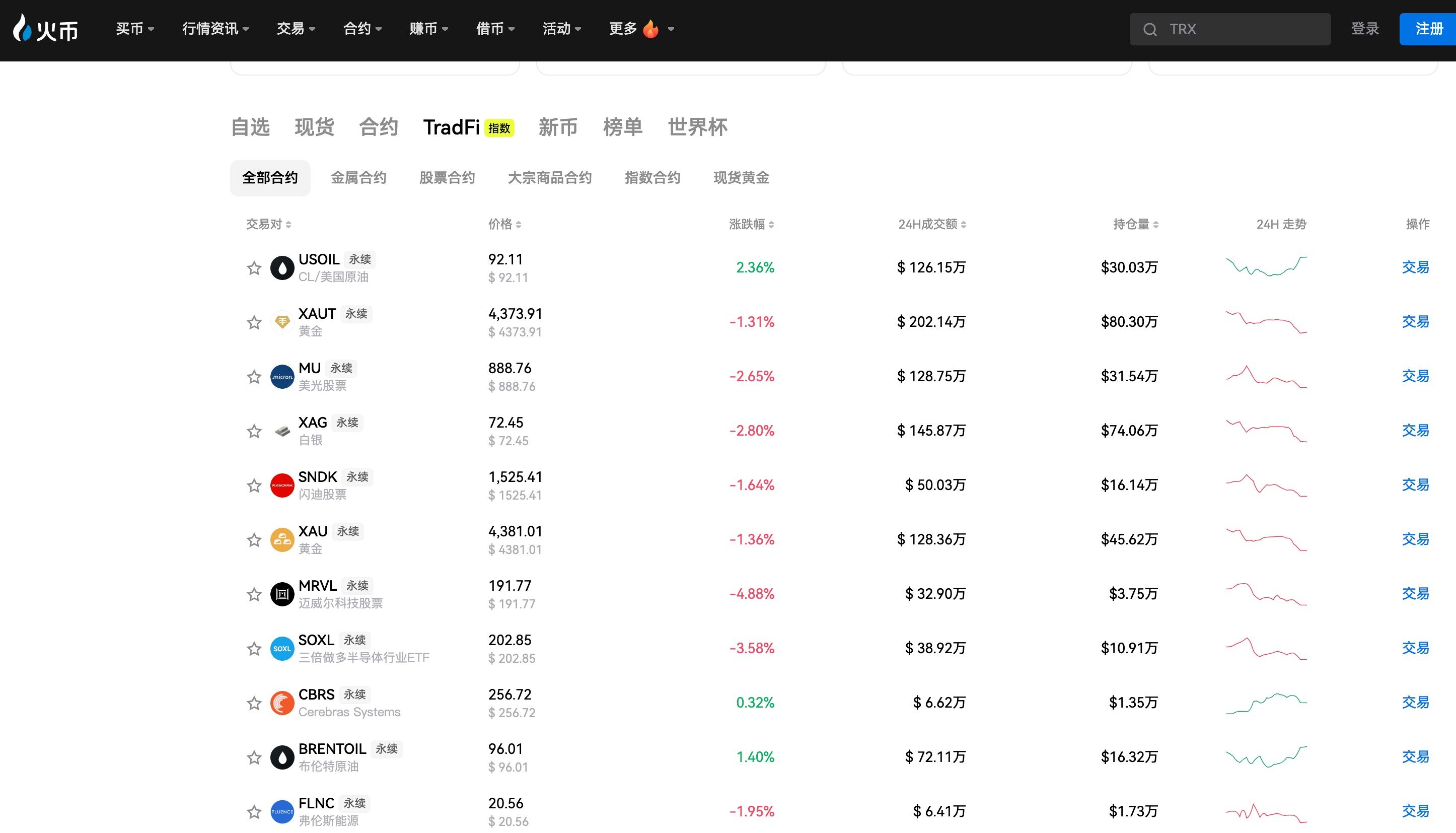

HTX, as an established platform in the crypto industry, took the lead in this phase by deploying its TradFi perpetual contract product line. Starting with core U.S. stock assets like NVDA, AAPL, MSFT, META, and SPY, it provides crypto users a new pathway to trade global core assets without leaving the on-chain ecosystem.

The underlying logic of this evolution is: the crypto market needs new incremental capital and user groups, and traditional financial assets serve as the most effective bridge connecting the world's $75 trillion stock market and $130 trillion bond market. For HTX, the introduction of TradFi assets signifies a strategic upgrade from a crypto-native platform to a comprehensive asset trading platform.

2. Market Structure and Competitive Landscape

Currently, the market for TradFi-on-crypto presents a competitive landscape with three main parallel tracks.

The first track is "Tokenized Real Assets." Led by players like BlackRock BUIDL, Ondo Finance, Backed Finance, and MyStonks, this track features assets existing on-chain as ERC-20 tokens, backed 1:1 by underlying real assets and managed by licensed custodians. BlackRock BUIDL, with $2.3 billion in AUM, holds a dominant position in the tokenized treasury market, commanding approximately 25% to 30% market share. Ondo Finance's OUSG has grown to multi-billion dollar levels. Backed Finance's xStocks operate on 9 blockchains, accessible without KYC but requiring whitelist approval.

The second track is "TradFi Perpetual Swaps." This is the fastest-growing segment in 2026. Coinbase launched U.S. stock perpetuals in March 2026 for non-U.S. users, supporting individual stocks like Apple, Microsoft, Nvidia, and Tesla, as well as ETFs like SPY and QQQ, offering up to 10x leverage for stocks and 20x for ETFs, settled in USDC with 24/7 trading. HTX has also launched TradFi perpetuals for NVDA, AAPL, MSFT, META, and SPY, providing users with USDT-settled globalized derivative trading services for U.S. stocks. Hyperliquid, via the HIP-3 protocol, holds a 28.6% market share in the RWA perpetuals space. The trading volume for RWA perpetuals in Q1 2026 reached $524.8 billion, surpassing the entire 2025 volume of $313 billion.

The third track is "Comprehensive TradFi Trading Infrastructure," aiming to provide a unified interface for trading both traditional and crypto assets. Some leading platforms access CFDs via third-party systems like MT5, while others develop proprietary index perpetual products that bundle multiple traditional assets into an index for trading.

Looking at market data, the tokenized RWA market reached a TVL of $31 billion to $34 billion by May 2026, nearly tripling from approximately $11 billion a year earlier. Tokenized gold grew from $1.43 billion to $5.55 billion, an increase of 289%. Tokenized stocks surged from $2 million to $486 million, a growth of over 200 times. BCG predicts the global tokenized asset market could reach $16 trillion by 2030, representing about 10% of global GDP. McKinsey offers a more conservative estimate of around $2 trillion. Regardless of the forecast, there remains a gap of tens to hundreds of times between the current market size and the long-term potential.

3. Core Risk Analysis

While the tokenization of TradFi holds great promise, the risks involved cannot be ignored. These risks represent potential pitfalls for investors and key challenges that platform operators must prudently manage.

First is compliance and regulatory risk, the largest source of uncertainty. Tokenized securities are fundamentally security offerings and must comply with national securities laws. The U.S. SEC's stance on on-chain securities remains in a gray area. Coinbase's U.S. stock perpetuals are only offered to non-U.S. users, a strategy that itself reflects the complexity of the regulatory environment. The fragmentation of cross-border regulation means the same tokenized asset may face entirely different compliance requirements in different jurisdictions, posing an ongoing compliance challenge for globally operating crypto exchanges. HTX, in deploying its TradFi perpetuals, also needs to navigate the operational complexities arising from differing regulations across regions.

Second is liquidity risk. Although Q1 trading volume for RWA perpetuals reached $524.8 billion, the total market capitalization of tokenized spot stocks is only $486 million, indicating a significant imbalance in liquidity depth between the spot and derivatives markets. This structural liquidity mismatch could lead to severe price deviations during extreme market conditions, increasing the risk of liquidations for traders. Furthermore, the discrepancy between U.S. stock trading hours and the crypto market's 24/7 trading model can lead to insufficient price discovery during off-hours, increasing the risk of slippage and abnormal volatility.

Third is smart contract and technical risk. Tokenized assets depend on the correct execution of smart contracts, and any contract vulnerability could lead to asset loss. While institutional-grade products like BlackRock BUIDL are supported by compliant platforms like Securitize, tokenized assets at the DeFi protocol level still face risks such as inadequate contract audits and oracle manipulation.

Fourth is custody and settlement risk. Real asset tokenization requires reliable custodians as backing. Should a custodian face credit risk (e.g., a repeat of the FTX incident), token holders could find themselves unable to redeem the underlying assets. Although mainstream solutions now use traditional custodians like Fidelity and UBS, the legal correspondence between on-chain tokens and off-chain assets lacks clear legal precedent in many jurisdictions.

Fifth is exchange rate and interest rate risk. TradFi perpetuals are typically settled in USDT or USDC, but the underlying assets are denominated in USD. Exchange rate fluctuations can impact the actual returns of non-U.S. users. Additionally, changes in the Federal Reserve's interest rate policy can directly affect U.S. stock movements, which in turn transmits to price volatility in TradFi perpetuals.

4. Innovation Trends and Track Opportunities

The TradFi-on-crypto track is exhibiting four major innovation trends, which present strategic growth opportunities for exchanges like HTX.

Trend one is the rapid expansion of the perpetual contract product matrix. Following Coinbase's pioneering launch of U.S. stock perpetuals, more crypto exchanges are adding similar product lines. The underlying assets are expanding from an initial 5-10 blue-chip stocks towards semiconductor ETFs, crypto-correlated stocks, and industry-themed ETFs. HTX has already listed contracts for NVDA, AAPL, MSFT, META, and SPY, and has the potential to cover more TradFi assets, building a comprehensive trading matrix for core U.S. stocks. From a competitive standpoint, exchanges that establish a complete TradFi product matrix first will gain a first-mover advantage in user acquisition and trading fee revenue.

Trend two is the maturation of institutional-grade infrastructure. The rapid growth of BlackRock BUIDL from $100 million seed capital to $2.3 billion AUM, along with the filing for two new tokenized funds signaling a move towards product families, demonstrates Wall Street's top-tier long-term commitment to tokenization. The involvement of traditional custodians like Fidelity and UBS, along with compliant platforms like Securitize offering one-stop KYC, whitelisting, on-chain issuance, and redemption services, is lowering the barrier for institutional entry. Franklin Templeton's Benji fund has been operating since 2021, and Ondo Finance's OUSG has reached multi-billion dollar levels, indicating that institutional tokenized product lines are taking shape. This institutional trend means TradFi-on-crypto is moving from "edge experiment" to "mainstream allocation," enhancing the value of crypto exchanges as gateways connecting institutional capital with on-chain assets.

Trend three is the rise of Permissioned DeFi Pools. This is the most noteworthy structural innovation in the RWA space in 2026. Institutions create KYC/AML whitelisted DeFi liquidity pools on public blockchains, allowing qualified participants to trade tokenized treasuries 24/7, while automated compliance checks are executed via smart contracts. This model retains DeFi's composability and efficiency while satisfying regulatory requirements for investor suitability, and is seen as a key bridge for large-scale institutional entry. Trend four is the gradual clarification of regulatory frameworks. The EU's MiCA regulation is fully enforced in July 2026, the U.S. GENIUS Act was enacted in March 2025, 72 jurisdictions globally have established crypto asset regulatory frameworks, and 58 countries have adopted the FATF Travel Rule. Regulatory certainty is shifting from "gray areas" to "clear rules," providing institutional backing for the long-term development of TradFi-on-crypto. For HTX, regulatory clarity means it can invest resources in building its TradFi product line with greater confidence, without as much fear of business disruption from sudden policy shifts.

5. Participation Strategies and Investment Logic

For investors, the TradFi-on-crypto track offers multi-layered pathways for participation.

The first layer is direct trading of TradFi perpetual contracts. Platforms like HTX have listed U.S. stock perpetuals, allowing investors to use USDT as margin for leveraged trading of assets like NVDA, AAPL, and SPY 24/7. The advantage of this path is the low entry barrier—trading global core assets without needing a traditional brokerage account. However, investors must be aware of funding rate fluctuations and the risk of forced liquidation in perpetuals. Specifically, the mismatch between U.S. stock trading hours and the 24/7 crypto market can lead to insufficient price discovery outside U.S. trading hours, increasing trading risk.

The second layer is investing in protocol tokens within the RWA track. Ondo Finance (ONDO), a leading protocol in the tokenized treasury space, has a token value positively correlated with the growth of on-chain treasury scale. Other RWA infrastructure protocols like Centrifuge are also worth attention. The third layer is positioning oneself with crypto exchanges that provide TradFi trading infrastructure.

With explosive growth in TradFi perpetual trading volume—reaching $524.8 billion in Q1 2026—exchanges listing TradFi products will directly benefit from increased trading fees. By listing U.S. stock perpetuals, HTX is opening up the vast incremental market of $75 trillion in U.S. stocks, which holds structural significance for its platform revenue and user growth.

It is particularly important for investors to focus on an exchange's compliance qualifications and risk management capabilities. Coinbase, as a Nasdaq-listed company, has a natural advantage in compliance. Other exchanges may navigate direct regulatory conflicts by targeting non-U.S. users. From a risk perspective, TradFi-on-crypto is still in its early stages. The liquidity depth of tokenized assets is far inferior to traditional markets, and price discovery mechanisms are not yet mature. Investors should strictly control position sizes, prioritize tokenized products backed by real assets, and avoid synthetic assets with high leverage and lacking a compliance foundation. Attention should also be paid to the impact of exchange rate fluctuations on non-U.S. users and the transmission effect of Fed policy changes on U.S. stocks.

6. Conclusion and Outlook

TradFi-on-crypto is reshaping the boundaries of the crypto industry. From the synthetic asset experiments of 2020, to the institutional entry of BlackRock BUIDL in 2024, to the comprehensive deployment of U.S. stock perpetuals by exchanges like Coinbase and HTX in 2026, this track has completed a leap from "proof of concept" to "product matrix" in just six years.

The current key data points are striking: the RWA market TVL has surpassed $31 billion, quarterly RWA perpetual volume has exceeded $500 billion, the market cap of tokenized stocks has grown over 200 times in a year, and Wall Street giants like BlackRock have made tokenization a core product strategy.

Standing at the midpoint of 2026, we judge that TradFi-on-crypto is still in the "early acceleration phase of its growth curve." Although a significant gap exists between BCG's forecast of $16 trillion long-term potential and McKinsey's conservative estimate of $2 trillion, even the conservative figure implies tens of times growth from the current market size. In the short term, the expansion of the U.S. stock perpetual product matrix, the institutional implementation of permissioned DeFi pools, and the full enforcement of regulatory frameworks like MiCA will serve as three major catalysts driving market growth.

HTX, as a significant participant in the crypto industry, has secured a favorable position in this track by launching TradFi perpetuals for NVDA, AAPL, MSFT, META, and SPY. In the medium to long term, when the on-chain trading depth and user experience for TradFi assets reach parity with traditional brokerages, crypto exchanges will truly complete their transformation from "crypto asset platforms" to "comprehensive asset trading infrastructure." This is not merely a technological upgrade but a fundamental change in the paradigm of financial infrastructure. For HTX users, this means the era of trading both crypto assets and global core traditional assets from a single account is arriving.