6月,ศูนย์ซื้อขายแบบรวมศูนย์เผชิญบททดสอบครั้งใหญ่

- ประเด็นหลัก: ในเดือนมิถุนายน 2026 จุดศูนย์กลางการแย่งชิงกระแสผู้ใช้ของศูนย์ซื้อขายคริปโตจะเปลี่ยนไปที่หุ้นสหรัฐฯ แบบโทเค็น (SpaceX IPO) และตลาดทายผล (ฟุตบอลโลก) และต้องเผชิญกับแรงกดดันหลายด้านจากการไหลออกของเงินทุนจากโบรกเกอร์แบบดั้งเดิมที่ถูกลงโทษ และการแข่งขันจาก Hyperliquid โปรโตคอลสัญญาซื้อขายล่วงหน้าแบบถาวรแบบกระจายศูนย์

- ปัจจัยสำคัญ:

- มุมมองร่วมเรื่องการเติบโตของตลาด: ปริมาณผู้ใช้ใหม่ที่ศูนย์ซื้อขายคริปโตแย่งชิงในปี 2026 ส่วนใหญ่มาจากการทำโทเค็นหุ้นสหรัฐฯ (เช่น SpaceX Pre-IPO) และตลาดทายผล (เช่น การทายผลฟุตบอลโลก) โดยอย่างแรกสร้างความรู้สึกกลัวตกขบวน (FOMO) และอย่างหลังมอบประสบการณ์การซื้อขายที่สั้น เร็ว แรง

- แรงกดดันด้านสภาพคล่องจาก SpaceX: IPO ของ SpaceX (12 มิถุนายน) คาดว่าจะทำให้ผู้ใช้เทขาย BTC/ETH/SOL เพื่อแลกเป็น Stablecoin และถอนออกไปเข้าร่วม ซึ่งถือเป็นการทดสอบแรงกดดันด้านสภาพคล่องต่อตลาดคริปโต

- ประโยชน์จากกฎระเบียบโบรกเกอร์: การที่ Futu, Tiger Brokers และ Longbridge ถูกลงโทษทำให้ช่องทางสำหรับนักลงทุนในประเทศในการซื้อหุ้นสหรัฐฯ แคบลง เงินทุนส่วนนี้อาจไหลออกไปยังโบรกเกอร์สัญชาติฮ่องกงหรือศูนย์ซื้อขายแบบรวมศูนย์ ซึ่งจะนำผู้ใช้ใหม่มาให้แก่ฝ่ายหลัง

- มิติการแข่งขันของศูนย์ซื้อขาย: การแข่งขันหลักอยู่ที่ความเร็วในการเปิดตัว (คว้ากระแสคลื่นลูกแรก), ความเสถียรของระบบ (รองรับการใช้งานพร้อมกันสูงในชั่วขณะ), การปรับปรุงผลิตภัณฑ์ (ทำให้เส้นทางการซื้อขายง่ายขึ้น) และกิจกรรมการดำเนินงาน (สร้างบรรยากาศ FOMO)

- ภัยคุกคามจาก Hyperliquid: ในฐานะตัวแทนของ Perp DEX Hyperliquid ได้วางแผนล่วงหน้าเกี่ยวกับสัญญาซื้อขายล่วงหน้าถาวรของ SpaceX และสัญญาทายผลฟุตบอลโลกแล้ว ด้วยทีมงานขนาดเล็กและประสิทธิภาพการตัดสินใจที่สูง ซึ่งถือเป็นความท้าทายด้านความเร็วต่อศูนย์ซื้อขายแบบรวมศูนย์

- ฟุตบอลโลกกับกลยุทธ์ของศูนย์ซื้อขาย: ศูนย์ซื้อขายใช้การเชื่อมต่อโปรโตคอลตลาดทายผลภายนอกเพื่อนำทางผู้ใช้ให้ใช้กระเป๋าเงิน Web3 โดยมีเป้าหมายเพื่อเพิ่มกิจกรรมบนเชน ฟุตบอลโลกถูกมองว่าเป็นศึกการดำเนินงานระยะยาว ไม่ใช่กระแสคลื่นในวันเดียว

In the first half of 2026, the crypto market can only be described in two words: agonizing.

Once considered "blue-chip assets," BTC, ETH, and SOL have been on a relentless decline. Activity on public chain ecosystems has dropped, and the community has lost its ability to create new hotspots. Meme coins tirelessly perform their pump-and-dump routine of "news - price surge - price crash." By the time retail investors rush in, project teams are already popping champagne.

When the market is bad, it's not just users who suffer; exchange founders are equally troubled. If users lose money on spot trading, their trading frequency drops. Lower trading frequency means reduced fee revenue. And when fees shrink, founders' OKRs start flashing red. Perpetual futures provide even more direct feedback. In a bear market, a single liquidation often leads a user to quit, and the cost of winning back a major client is extremely high.

Acquiring new users, retaining them, and boosting engagement—this operational chain from the internet industry of the past few years—is now slowing down in the crypto space. Essentially, investors only have so much attention to give. Without a wealth effect in crypto, investors naturally shift their focus to other profitable industries.

Thus, a question lies before every exchange: Where will the next wave of growth come from?

US Stock Tokenization and Prediction Markets

The market has largely reached a consensus that the main growth drivers for 2026 will be two areas: US stock tokenization and prediction markets. The former is responsible for generating FOMO, while the latter fuels dopamine rushes. Memory chip stocks like SanDisk, SK Hynix, and Western Digital have surged powerfully, creating a strong wealth effect. For the first time, many crypto users realize that "US stocks are easier to profit from than altcoins." Prediction market trading, on the other hand, is short and fast. Users don't need to analyze on-chain data; they just place bets: Will the Strait of Hormuz remain open? Will the Fed cut rates? Compared to the torment of holding BTC or ETH through volatile swings, prediction markets are clearly more addictive.

Consequently, US stock tokenization and prediction markets have quickly become a new battleground for major exchanges, with competition intensity escalating. June is not only the month of Gaokao for senior high school students, but also a crucial "exam" period for all exchanges.

The SpaceX IPO

First up is the biggest IPO in human history, the most brilliant creation of the Silicon Valley iron man, the architect of the Starlink era, the igniter of the space AI narrative, the behemoth valued at nearly $2 trillion — SpaceX.

The SpaceX IPO is not just a major event on Wall Street; it's a liquidity stress test for the entire crypto industry. Predictably, many users will start selling BTC, ETH, and SOL, converting them into USDT or USDC. They will then withdraw from exchanges, exchange for fiat dollars, and dive into the secondary market to participate in SpaceX.

In other words, for the past few years, exchanges have been trying to turn dollars into stablecoins. Now, SpaceX might cause stablecoins to turn back into dollars.

But within great crises often lie great opportunities. Bitget has offered its answer: listing SpaceX's Pre-IPO shares early. (This is truly not an advertisement, just stating facts; other exchanges will be mentioned later.)

This move has already put Bitget a step ahead of other exchanges in channeling traffic their way. For many ordinary users, the real barrier isn't knowledge, but the complex processes involving US dollar accounts, cross-border brokerages, and compliance procedures. What the exchange does is: "You don't have to leave crypto to participate in SpaceX." However, new problems have also emerged. The number of SPV shares released by SpaceX is simply too small. The total allocation is only $61 million. Consequently, there are many eager buyers in the market, but very few shares available for sale.

How Can Exchanges Capture the SpaceX Traffic?

Personally, I think Bitget has made a smart move here, but what will truly determine which exchange captures the biggest traffic dividend isn't the Pre-IPO event, but the day SpaceX officially goes public on June 12th.

First and foremost, it's a race for listing speed. The exchange that can list SpaceX-related spot trading first will capture the most explosive initial wave of traffic. This logic is very similar to the MEME wars of the past. Why did TRUMP bring massive new user growth to exchanges? Because user FOMO is strongest in the first few hours. The first one to list wins; those who are slow will find users have already opened accounts on competitor exchanges. Of course, how quickly SpaceX stock can be tokenized depends on the likes of Ondo and xStocks. For these two, the SpaceX IPO might define who becomes the top player for on-chain US stocks.

Secondly, on the product and engineering side, the pressure from the SpaceX listing represents a tough battle for exchanges. No user wants to miss out on listing day because of a laggy app, delayed charts, or inability to place orders. However, such incidents have not been uncommon among exchanges in recent years. When a major event hits, a massive influx of users will simultaneously refresh charts, place and cancel orders, and open leveraged positions. The backend's market data push, matching engine, database reading/writing, and WebSocket real-time communication will all come under instant pressure. Any small issue will result in a terrible user experience.

Thirdly, on the product side, making the trading process smoother for users directly determines conversion rates. Every additional click a user makes cuts the conversion rate in half. How product managers design the trading interface to make it easier for users to buy SpaceX, reduce slippage, and provide a better trading experience is crucial. Details like homepage resource placement, whether the chart page allows one-click trading, the simplicity of the order placement process, and whether users can "mindlessly buy" after viewing charts will all affect final transaction volumes.

Finally, the key on the operational side is turning "SpaceX" into a massive FOMO event. Trading competitions, airdrop rewards, deposit bonuses, referral programs, and KOL collaborations will all be deployed simultaneously. Large exchanges have natural advantages in operations, higher visibility, and more distribution channels. But smaller exchanges aren't without opportunities. If they can create campaigns that resonate deeply with users, they can also achieve massive growth. Users may not remember which exchange listed SpaceX first, but they will definitely remember where they made their first windfall.

Fines for Futu, Tiger Brokers, and Longbridge: Where Will China-Based US Stock Investors Go?

At the end of May, three Chinese internet brokers—Futu, Tiger Brokers, and Longbridge—received regulatory penalties in succession. For many users within mainland China, the impact of this is actually greater than many imagine. Simply put, existing users can only sell, not buy, for the next two years, and the platforms cannot add new users from mainland China. Many people's first reaction is: "Isn't this just broker rectification?" But if you consider this alongside the SpaceX IPO, things start to get interesting.

Over the past few years, numerous mainland investors have gone through the hassle of getting Hong Kong bank cards and opening overseas accounts, all for one fundamental reason: to buy US stocks. And this year, SpaceX has emerged as one of the world's strongest wealth narratives. Many were planning to jump in on IPO day. Now, this traditional internet broker channel is suddenly tightening. This means a large amount of capital originally poised to flow into US stocks hasn't disappeared but is simply looking for a new outlet. However, much of this capital won't flow back into A-shares. Thus, a very realistic question arises: Who can capture this capital spillover?

The answer is becoming quite clear: Hong Kong-funded brokers and centralized exchanges (CEXs).

Both have their advantages. The biggest advantage of Hong Kong-funded brokers is that they offer a "complete US stock market." While platforms like xStocks and Ondo have tokenized many US stocks, they currently cover mainly the most liquid core assets like Tesla, Nvidia, and Google. Compared to the tens of thousands of stocks on the entire US market, the currently tradeable tokens cover less than 5%. This means if users want to buy relatively less popular Chinese concept stocks like KE Holdings, Full Truck Alliance, Atour, or even some small-cap growth stocks, they ultimately have to return to the traditional broker system.

However, exchanges have their own killer feature: user experience. As mentioned earlier, every additional step in a trade cuts conversion in half. Most Hong Kong broker apps require about 6-7 clicks to reach the US stock trading page, and US stock trading permissions need separate activation. In contrast, US stock trading on centralized exchanges is often placed in the most prominent position. It takes at most 3 clicks to trade tokenized US stocks. Most users still tend to choose based on: which one is simpler, faster, and feels more like an internet product.

Of course, whether opening an account with a Hong Kong broker or registering for a CEX, both operate in a grey area. Users will need to find their own way, which we won't delve into here. DDDD (those who know, know).

When the World Cup Collides with SpaceX

What a coincidence; the 2026 World Cup kicks off on June 12th, which happens to be the day of the SpaceX IPO. As for whether this timing was intentional by the US, think about it, think carefully. One is the most anticipated IPO in human history, the other is the world's biggest sports event. When the "rocket" and the "football" collide on the same day, the global spotlight will be on the United States.

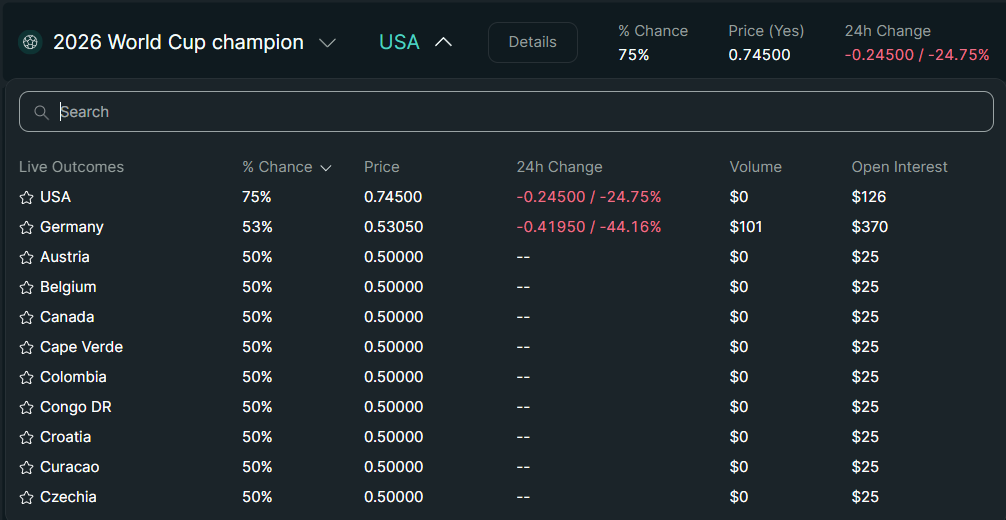

The commercial value of the World Cup needs no explanation; it's already the world's largest traffic portal for betting. According to Forbes, global betting volume during the 2022 World Cup reached $160 billion. And in 2026, the World Cup will be even crazier. On one hand, the tournament expands from 32 to 48 teams, significantly increasing the number of matches, discussion heat, and demand for bets. On the other hand, the on-chain prediction market is no longer Polymarket's exclusive domain. Platforms like Kalshi, Myriad, and Predict.fun have all entered the fray. In other words, the 2026 World Cup is very likely the first true instance of "large-scale user education" for on-chain prediction markets.

Exchanges certainly won't miss this opportunity. However, regulatory risks for this type of business always exist, as betting is highly sensitive in many regions. Therefore, most exchanges won't run prediction markets themselves but will choose "indirect strategies." Many exchanges, including Binance, OKX, and Bybit, currently prefer to connect with prediction market protocols like Polymarket, Kalshi, and Predict.fun, allowing users to participate in World Cup betting via Web3 wallets. What exchanges truly want isn't just the betting itself, but to cultivate the habit of users using Web3 wallets.

Because in most exchanges, the proportion of users who actually open their Web3 wallet with high frequency is relatively low. If users start getting used to connecting wallets, signing transactions, and interacting on-chain for World Cup betting, then the exchanges' own on-chain Dapps will naturally see increased activity. Especially after the initial hype surrounding Binance Alpha, OKX Boost, and other on-chain products has cooled, the World Cup might become the catalyst for many users to re-open their Web3 wallets.

Of course, looking at the challenges for exchanges, the World Cup and SpaceX are not of the same magnitude. Even for exchanges like Gate, which aggressively promotes prediction markets, they ultimately direct users to Polymarket. Thus, the pressure falls on the prediction market protocol itself, not the exchange backend. Secondly, most World Cup bets can be placed in advance. It's not like the SpaceX IPO, requiring users to frantically place orders at a single moment. Therefore, for exchanges, the World Cup is more of a "steady and continuous" operational campaign rather than a sudden traffic surge on one specific day. Compared to a one-day stress test, exchanges need to think more about how to continuously convert World Cup hype into user engagement and on-chain trading volume over the next 40 days.

The Looming Threat of Hyperliquid

Now, centralized exchanges are not just fighting each other. What really keeps them up at night is the threat of Perp DEX unicorns like Hyperliquid.

If you compare the centralized exchange giants like Binance, OKX, and Bybit to elephants, then Hyperliquid is more like a cheetah hiding in the shadows. It's not as large, but it's incredibly fast. It's more sensitive to hot topics and can react quicker to market moves. Often, while centralized exchanges are still in meetings assessing risks, Hyperliquid has already launched its product.

For the two most important hot topics in June—the SpaceX IPO and the World Cup—Hyperliquid has already prepared in advance. Regarding SpaceX, Hyperliquid listed a pre-IPO perpetual contract for SpaceX (SPCX-USDC) via Trade.xyz. Users can directly trade with leverage even without actually holding SpaceX stock. On the World Cup front, on May 26th, Hyperliquid's HIP-4 testnet launched a "2026 World Cup Winner" prediction contract, signaling Hyperliquid's formal entry into the on-chain prediction market and betting arena.

Hyperliquid has always been known for its "small team, high efficiency." In the crypto industry, smaller organizations often mean fewer processes, shorter decision-making chains, and faster product response times. While many centralized exchanges are still waiting for approvals from legal, risk control, operations, and marketing departments, Hyperliquid has already built the trading market.

But elephants have their advantages too. The large operational, customer support, content, and channel teams of centralized exchanges can still cover a wider range of ordinary users. For many newcomers, they may not care whether it's native on-chain or truly value "decentralization." They care more about: how to open an account, how to buy, why they can't buy, and who to contact if they get liquidated. Often, a customer support agent who responds promptly can be more important than the "fully decentralized" narrative.

Even though the HYPE token has performed exceptionally well in 2026 while platform tokens like OKB, BGB, and KCS have been weak overall, the author still doesn't believe Hyperliquid will completely replace all centralized exchanges. In both stock markets and crypto markets, truly professional high-frequency traders and quantitative funds are always a minority. The vast majority of users are still ordinary retail investors.

Epilogue

US stock tokenization is undoubtedly a crucial branch of RWA. It possesses high standardization, high liquidity, and relatively large volatility, making it naturally suitable for the Crypto world. Prediction markets, in a sense, are the on-chain mapping of real-world events. From the US elections to World Cup betting, they essentially move the emotions, opinions, and odds from the real world onto the chain.

In 2023, the crypto circle was buzzing about 5% on-chain US Treasury yields. In 2024, BlackRock issued the on-chain US Treasury fund BUIDL. By 2025, stablecoins, on-chain US stocks, and on-chain gold began entering mainstream financial perspectives.

Soon, the "rocket" and the "football" from the real world will arrive in Web3.

The traffic war for exchanges kicks off in June.