七周吸金13亿,SpaceX权重却腰斩:NASA ETF的稀释陷阱

- 核心观点:NASA ETF通过“唯一持有SpaceX”的叙事吸引大量资金,但实际持仓中SpaceX权重被快速稀释,投资者实际买到的是其他太空股。文章揭示了叙事溢价、估值倒挂与散户预期落空的风险。

- 关键要素:

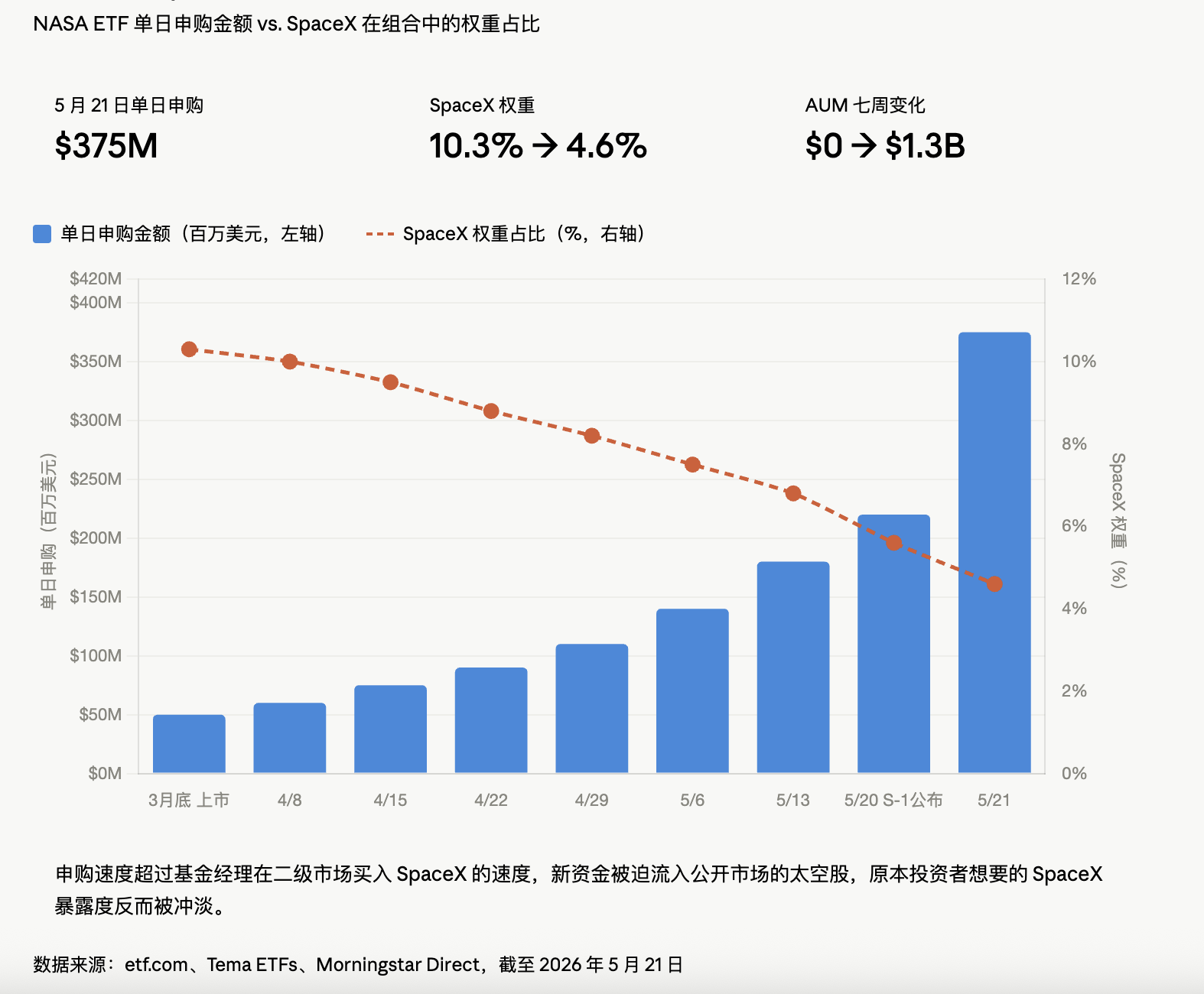

- NASA ETF七周内成为全球最大太空主题ETF,AUM一周翻三倍,但SpaceX持仓占比从10.3%降至4.6%,新资金被迫投向Rocket Lab等公开标的。

- SPV持仓估值机制不透明,仅在Tema自行交易时更新,且SpaceX IPO后有6个月锁定期,可能延迟反映市场价格波动。

- 赛道内其他标的已大幅上涨,如Planet Labs一年涨979%,Rocket Lab涨357%,基本面线性增长与股价指数增长形成估值倒挂,由叙事溢价填补。

- SpaceX 2024年营收186.7亿美元,但由盈转亏亏损45.9亿美元,因xAI和X(Twitter)被并入,形成“太空+AI+社交媒体”四合一打包叙事。

- SpaceX预计6月12日IPO,募资400-800亿美元,若破发则SPV头寸无法及时止损;若暴涨则进一步稀释ETF中SpaceX权重,形成反向飞轮。

Original Author: TechFlow

On May 20, SpaceX's S-1 filing appeared on the SEC's official website. The next day, a fund with the ticker symbol "NASA" attracted $375 million in a single day, tripling its AUM within a week. Just seven weeks earlier, this fund had barely been launched.

Seven weeks later, it has become the world's largest space-themed ETF, leaving the veteran UFO fund, which has been running for seven years, far behind. The amount it raised in seven weeks exceeds what UFO raised in seven years combined.

Everyone piling into NASA wants to buy SpaceX. But the actual SpaceX they end up owning is getting smaller and smaller.

Where Did the Money Go?

The NASA ETF markets itself as "the only pure-play space ETF holding SpaceX in the market." As of May 21, NASA indirectly held 232,000 SpaceX common stock equivalents through an SPV, with a book value of $147.4 million, implying a valuation of approximately $1.51 trillion.

The numbers look solid. But there's a detail most retail investors would miss. According to ETF.com, a week earlier, NASA's allocation to SpaceX was 10.3%. A week later, it had been diluted to 4.6%.

Because subscription money poured in too fast, the fund manager couldn't quickly acquire enough SpaceX shares in the secondary market. A flood of new capital was forced into publicly traded space stocks, diluting the very SpaceX exposure investors originally sought.

Retail investors rushing in to buy SpaceX ended up buying Rocket Lab, AST SpaceMobile, and a basket of other names.

Even more nuanced is the valuation mechanism. The SPV holdings are only updated when Tema (the issuer) executes trades. In other words, regardless of how SpaceX's secondary market quotes fluctuate, the book value of NASA's SPV holdings remains static.

This setup goes unnoticed in a bull market. But if SpaceX tanks after its IPO, the SPV portion will exhibit an almost eerie "delayed reaction." Worse, this SPV is subject to a 6-month lock-up period after SpaceX's official IPO. If the stock crashes on opening day, retail investors can flee; the SPV cannot.

The ETF charges a 0.87% management fee annually, but the surface-level 65% gain comes from already surging holdings like Rocket Lab and Intuitive Machines. SpaceX? It contributed very little.

NASA, in its current form, is essentially a thematic fund using SpaceX as bait, filled with small-cap space stocks. The bait's allure is crucial, but what's served on the plate is something else entirely.

Inverted Valuation

What many don't realize is that many major stocks in this sector have already had their run.

Rocket Lab is up 357% over the past 12 months; Planet Labs is up 979%; LUNR is up 212%. ARKX is up 62% over the past year, and ROKT is up 75%. SpaceX merely ignited dry tinder that was already smoldering.

Laying these numbers out raises a question. Planet Labs surged 979% in a year, but its core business is selling satellite imagery data. Does its fundamentals justify a near 10x stock price increase?

Global orbital launches numbered 102 in 2019 and 342 in 2025, double the peak of the 1967 space race. Grand View Research projects the global space industry will grow from $466 billion in 2024 to $769 billion by 2030.

But the question remains: why should an industry growing from $466 billion to $769 billion correspond to a 10x surge in the secondary market?

This is a classic case of valuation inversion. Fundamentals follow linear growth, stock prices follow exponential growth, with the gap bridged by "narrative premium." And that narrative premium has only one source: SpaceX's impending IPO.

What Are The Real Bagholders Actually Buying?

Let's return to SpaceX itself.

Revenue in 2024 was $18.67 billion, up from $10.3 billion in 2023. But 2024 saw a loss of $4.59 billion, compared to a $791 million profit in 2023—a direct swing from profit to loss.

CNN reported a nearly $5 billion loss last year, attributed to its AI division burning cash on building data centers.

SpaceX disclosed in its S-1 filing that xAI has been consolidated into SpaceX, and X (formerly Twitter) is also included. This so-called "space IPO" is essentially a massive bundle of all Musk's assets. The filing also reveals Musk controls 85% of voting rights; unless he votes to fire himself, no one can remove him.

The $1.75 trillion valuation for SpaceX corresponds to a "Space + AI + Satellite Internet + Social Media" four-in-one narrative. The bigger the narrative, the more inflated the price.

But the secondary market doesn't care about this. What it cares about is that everyone is scrambling to get on board, so they must too.

Circling back, the biggest winners aren't SpaceX's retail shareholders (they haven't boarded yet), nor the ETF investors pouring into NASA (their SpaceX exposure is being diluted).

The biggest winners are the ETF issuers. NASA's expense ratio is 0.87%, the third highest among peer funds. With $1.3 billion in AUM, that means $11 million in annual management fees.

Issuing an ETF is fundamentally the same as issuing a token: you need a story, timing, and a seemingly reasonable benchmark. SpaceX provides all three.

Before the IPO

On June 12, SpaceX is expected to list on the Nasdaq under the ticker SPCX. The underwriting syndicate is led by the world's largest investment banks, targeting a fundraising size of $40 billion to $80 billion, far exceeding the record set by Saudi Aramco in 2020.

This will be the largest IPO in human history.

If it tanks on its first trading day, all ETF investors who bought into the SpaceX story will find their SPV positions still valued at "stale prices" from months ago. They can neither immediately stop losses nor exit quickly.

If it soars, those who missed out on the ETF will pile in, further inflating the ETF's premium, further diluting SpaceX's actual weight within the ETF, creating a comical reverse flywheel: the more people buy, the less SpaceX each person actually owns.

After SpaceX, a host of industry giants are lined up for IPOs. Each flagship "concept sector" IPO will spawn a new wave of ETFs. Each new batch of ETFs will repeat the same dilution game.

The industry doesn't lack new stories; it lacks people who will ask, "Am I actually getting what I think I'm buying?" After June 12, there will be an answer. But by then, those who rushed into NASA today won't care about the answer anymore. They'll either be counting their money or fighting for their rights.