Who is selling, who is holding, and who is still buying? Diverging crypto ETF positions among old American money

- Core Thesis: In the first quarter of 2026, different institutions adopted differentiated strategies amid the crypto ETF downturn: university endowments like Harvard actively reduced positions to pivot toward AI, investment banks like Goldman Sachs scaled back crypto ETF exposure and shifted toward selected stocks, while sovereign wealth funds like Abu Dhabi's and major banks like JPMorgan increased their holdings counter-cyclically, signaling that institutions are applying a more refined risk-sorting approach to crypto assets.

- Key Elements:

- Harvard University's endowment cut its IBIT holdings by 43% and fully exited its Ethereum ETF position, while simultaneously increasing allocations to AI and computing-related stocks, reflecting a structural rebalancing strategy of "reducing crypto, adding AI."

- Goldman Sachs significantly reduced its Bitcoin and Ethereum ETF positions in Q1 2026, completely liquidated all XRP and Solana-related ETF holdings, while increasing its stakes in Circle (+249%) and Coinbase (+65%), demonstrating an internal rotation from ETF risk toward selected stock picks.

- Abu Dhabi's sovereign wealth fund Mubadala increased its IBIT holdings by approximately 15.9% against the trend, despite the market value declining from $631 million to $566 million due to price drops, reflecting the long-term allocation patience typical of sovereign capital.

- JPMorgan increased its IBIT holdings by 174% to approximately 8.3 million shares while also boosting its Ethereum ETF exposure, reflecting the strategy of a major bank expanding its product shelf and meeting client allocation needs.

- US university endowments (Brown, Dartmouth) chose to stay put or make moderate adjustments. For instance, Dartmouth College maintained its Bitcoin core position while switching its Ethereum product to a staking-enabled ETF, demonstrating long-term allocation discipline.

Original Authors: KarenZ, Foresight News

The most noteworthy aspect of the first quarter isn't how much prices fell, but how institutions navigated this pullback.

Looking solely at price action, Q1 2026 wasn't easy for crypto ETFs. Bitcoin and Ethereum faced downward pressure during the quarter, leading to a broad decline in the book value of spot ETF holdings. Even for positions that weren't sold, the quarter-end picture looked bleak. However, the truly interesting part of a market downturn is never the net asset value curve itself, but rather the different actions taken by various types of institutions while facing the same drawdown chart.

As of the latest round of 13F filings disclosed by mid-May 2026, the market can now see the quarter-end holdings of a range of institutions as of March 31, 2026. University endowments, major investment banks, sovereign wealth funds, market makers, and wealth management firms have presented several distinctly different answers.

Some Reduced Positions: Risk Contraction First

Let's first look at the sellers.

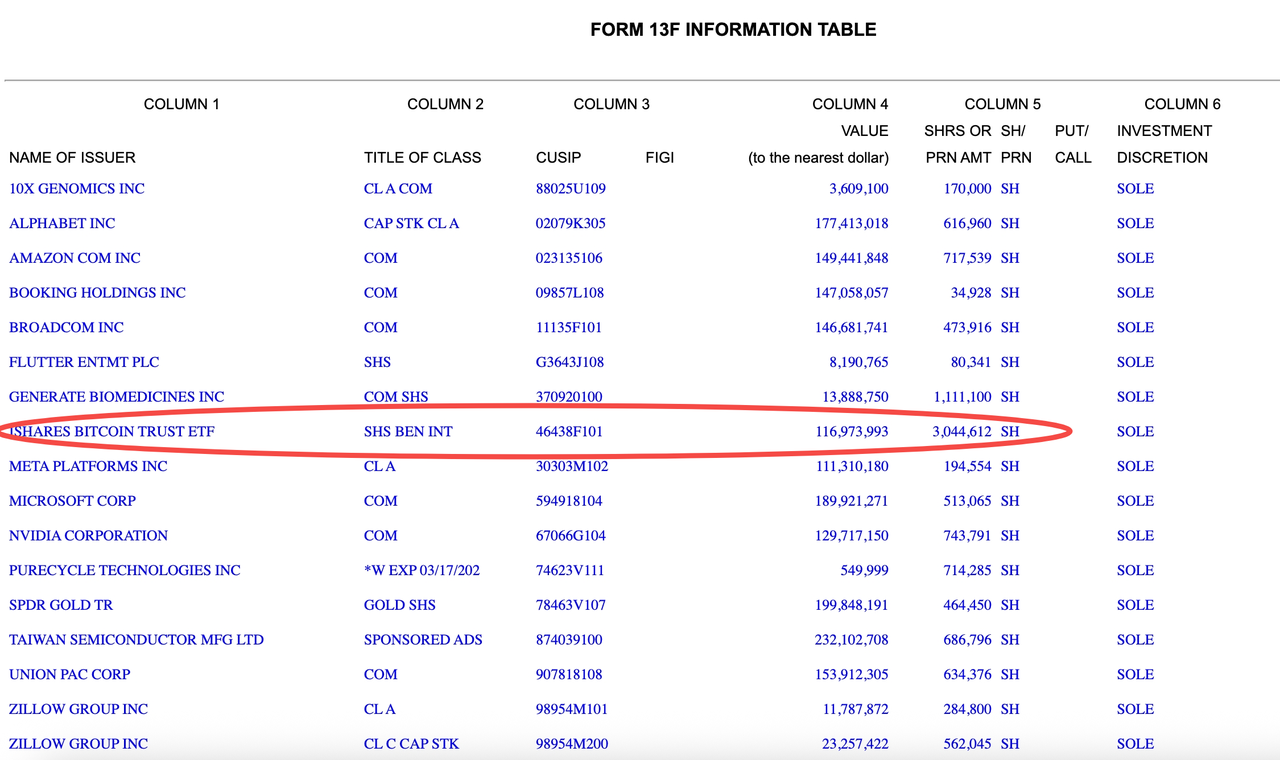

Harvard Management, which manages the Harvard University endowment and related financial assets, is one of the most typical examples in this round. According to its 13F filing, its IBIT (iShares Bitcoin Trust ETF) holdings decreased from 5,353,612 shares at the end of Q4 2025 to 3,044,612 shares at the end of Q1 2026, a reduction of approximately 43%. The corresponding book value also fell from about $266 million to around $117 million. Simultaneously, its ETHA (iShares Ethereum Trust) holdings from the previous quarter were completely exited. This suggests Harvard wasn't merely reacting to price declines but actively compressing its public exposure to spot Bitcoin and Ethereum ETFs.

This change in holdings also conveys another message. Harvard didn't turn entirely defensive. Instead, it reallocated a portion of its capital to assets in the AI and computing chain, increasing positions in stocks like NVIDIA, Broadcom, and TSMC. Viewed together, these actions resemble a structural rebalancing of "reducing crypto, adding AI," rather than a comprehensive risk contraction.

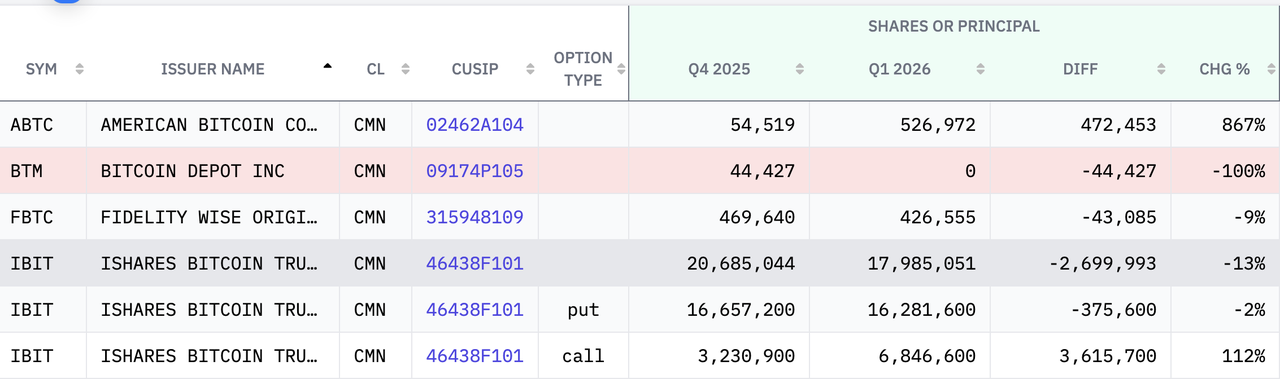

Goldman Sachs employed a broadly similar strategy, albeit with more complex tactics. Comparing the last two 13F filings, Goldman Sachs held approximately $690 million in IBIT and about $25.18 million in FBTC (Fidelity Wise Origin Bitcoin Fund) at the end of Q1 2026, both down from the previous quarter. More noteworthy than the simple reduction is the structure of its positions: Goldman Sachs held spot positions, call options, and put options in IBIT simultaneously, indicating this wasn't just a directional bet but also had clear trading and hedging characteristics.

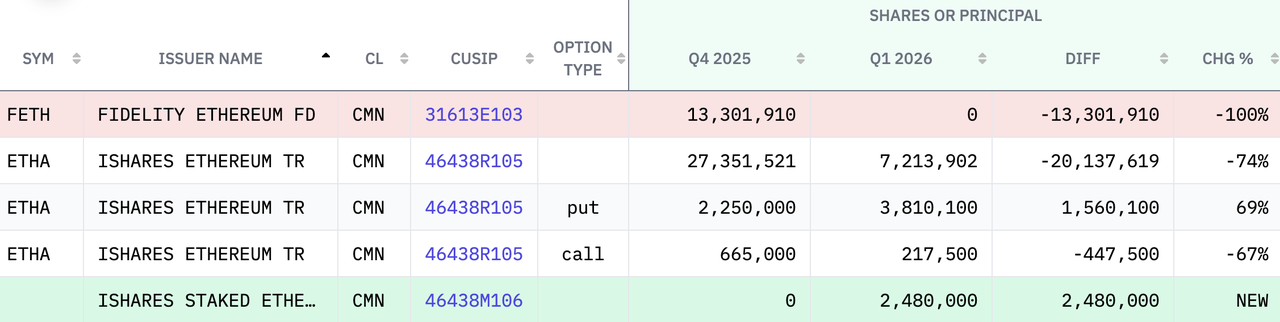

Goldman's approach to Ethereum was more aggressive. It not only fully exited its position in the Fidelity Ethereum Fund (valued at $394 million at the end of Q4 2025) but also significantly reduced its spot position in the iShares Ethereum Trust (ETHA), cutting approximately 74% to leave a remaining position of about $114 million. Additionally, it newly held $66.885 million in the iShares Staked Ethereum Trust ETF.

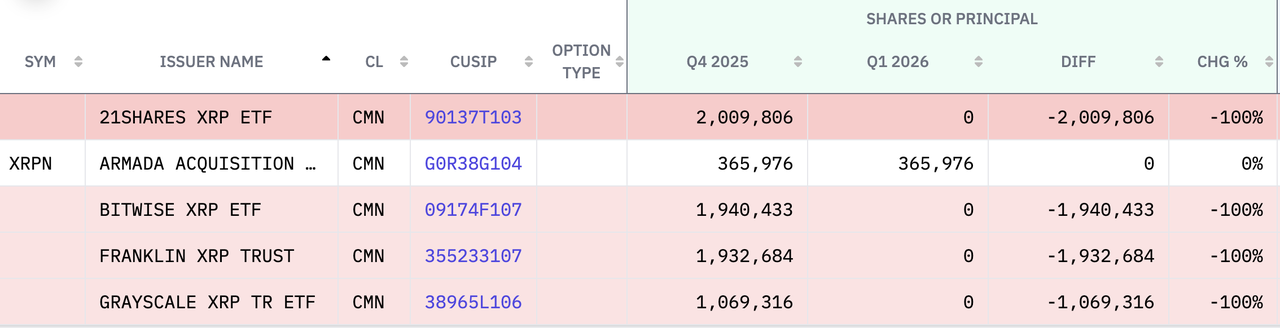

Concurrently, Goldman Sachs fully liquidated all its XRP and Solana-related ETFs. As of the end of Q4 2025, it held XRP ETFs from Bitwise, Franklin Templeton, Grayscale, and 21shares totaling approximately $152 million. It also exited all its Solana ETFs/trusts from Grayscale, Bitwise, and Fidelity, which were valued at $109 million at the end of Q4 2025.

Regarding crypto equities, Goldman increased its Circle position by 249% to around $140 million, and its Galaxy Digital holding also jumped 205% to $41.48 million. Positions in Coinbase (+65%), Robinhood (+35%), and PayPal also increased. During the same period, it reduced holdings in Strategy and Riot Platforms. Overall, this looks more like an internal rotation of "compressing ETF risk, shifting to selected individual stocks."

Among hedge funds, Millennium Management also sent a similar signal. Public filings show its IBIT holdings dropped from 34.334 million shares to 19.287 million shares, a decrease of about 43.8%. ETHA holdings also fell concurrently (down about 34.3%), indicating a clear reduction in exposure to both spot Bitcoin and Ethereum ETFs.

Capula Management Ltd, a London-based hedge fund manager, was even more extreme. As of December 30, 2025, it held $470 million in IBIT, $160 million in FBTC, $207 million in ETHA, and $61.43 million in FETH. However, its latest 13F report shows that all these ETF positions have been completely liquidated. Furthermore, Capula Management Ltd has fully exited its Coinbase position (retaining a small options position).

Holding Steady: An Attitude in Itself

The second category comprises those who held their ground.

Brown University's IBIT holdings remained at 212,500 shares, unchanged. Based on disclosed market value, this position fell from approximately $10.551 million at the end of 2025 to roughly $8.164 million at the end of Q1 2026. These university endowments did not translate a single quarter's price volatility into trading instructions but instead emphasized portfolio discipline and long-term allocation pacing.

Dartmouth College's handling of crypto assets in Q1 2026 looked more like a measured expansion than a radical turnover. Comparing its Q1 and Q4 2025 13F filings, the college maintained its core Bitcoin ETF position, with IBIT share count essentially unchanged, although the book value dropped from over $10 million to about $7.7 million due to the quarter's price decline. For Ethereum exposure, it executed a product switch, moving from the Grayscale Ethereum Mini Trust to the staking-enabled Grayscale Ethereum Staking ETF, holding approximately 178,100 shares. Additionally, it established a new position in the Bitwise Solana Staking ETF, holding about 304,803 shares valued at roughly $3.3 million.

The Other Playbook: Buying the Dip

The third category involves those who increased positions against the trend.

Abu Dhabi's sovereign wealth fund, Mubadala, is one of the most prominent names. Its IBIT holdings increased from 12,702,323 shares to 14,721,917 shares, a gain of about 15.9%. However, despite the higher share count, the quarter-end market value of the position still fell from roughly $631 million to about $566 million. This set of numbers is quite telling. The act of adding shares does not automatically lead to profitability, especially when the market is still in a pullback channel. Increasing allocation first brings larger exposure, and only potentially, higher upside later.

JPMorgan's actions can also be understood within this logic. Its latest 13F data shows JPMorgan increased its IBIT holdings from about 3.028 million shares to about 8.3 million shares, a 174% increase, while also adding some exposure to FBTC, BITB, and Ethereum ETFs. Looking at the change in share count, it was clearly more aggressive. However, this doesn't mean it has locked in excess returns during this volatile period. For a major bank, increasing ETF positions often serves multiple purposes like expanding its product shelf, meeting client allocation needs, balancing liquidity, and managing book risk, rather than simply being a directional bullish bet.

Wells Fargo's position changes are also worth noting independently. Comparing periods, the bank retained its core IBIT position while adding products like BITB and the Grayscale Bitcoin Mini Trust. More significantly, it notably increased its Ethereum ETF allocation, boosting its ETHA holdings from about 672,600 shares to roughly 1.1 million shares, and similarly increasing its ETHW holdings. In other words, Wells Fargo adopted a strategy of "maintaining the Bitcoin core position while raising Ethereum's weight."

Market maker Jane Street showcased another typical style. Comparing its two 13F filings, it substantially reduced its spot Bitcoin ETF exposure in Q1, with IBIT holdings dropping from about 20.3 million shares to roughly 5.9 million shares, and FBTC also declining significantly. However, during the same period, it added roughly $82 million in new Ethereum ETF exposure. Regarding crypto equities, Jane Street increased its positions in Galaxy Digital (+8746%), Circle (+1162%), Coinbase (+14%), and BitMine (+47%). This combination looks more like a classic trading rebalance: reducing Bitcoin ETFs, adding Ethereum ETFs, while seeking higher elasticity in individual stocks.

Bitcoin, Ethereum, and Solana: Institutions Are Refining Risk Prioritization

This round of 13F filings also presents another noteworthy signal: institutional attitudes towards BTC ETFs, ETH ETFs, and even Solana ETFs are no longer uniform. The more pertinent question now is which crypto asset institutions intend to keep as a core holding, which goes into an elastic position, and which is removed entirely.

Take Harvard Management as an example. It simultaneously reduced IBIT and completely exited ETHA. This resembles a form of risk prioritization. The Bitcoin ETF maintained a relatively core position, while the Ethereum ETF was the first to be cut during the portfolio rebalancing.

Goldman Sachs' approach also shows that large financial institutions are taking this prioritization to an extreme. It retained a substantial Bitcoin ETF exposure in Q1 but contracted its Ethereum-related products much faster, while basically liquidating all XRP and Solana-related ETFs. Viewed together, Goldman Sachs is re-concentrating its positions into the asset layer it deems most liquid, easiest to hedge, and simplest to incorporate into institutional risk models. Bitcoin here acts more like a "base position," Ethereum is a compressible position, and products like Solana and XRP are closer to marginal experimental bets. When market volatility increases, these are often the first parts to be cut.

However, on the other hand, Wells Fargo and Dartmouth College presented entirely different answers. Wells Fargo proactively increased the weight of its Ethereum ETFs, suggesting that within its internal framework, Ethereum is viewed more as a secondary position worth increasing allocation during pullbacks to seek elasticity. Dartmouth's strategy is perhaps more representative: it didn't touch its Bitcoin ETF core position but extended new elasticity into Solana-related ETFs, particularly those with staking attributes.

13F Provides the Market a Snapshot, But Also Leaves Blanks

This is where the most restraint is needed when interpreting institutional holdings.

13F filings allow the outside world to see, under a standardized reporting framework, how mainstream institutions allocate to crypto ETFs. However, they also have very clear limitations. Firstly, there is a time lag. Investors seeing the data in May are only looking at a quarter-end snapshot from March 31. If significant portfolio adjustments were made in Q2, the table won't show it early. Secondly, 13F only displays holdings, not the actual cost basis. A decline in an institution's position value over a quarter doesn't necessarily mean it incurred an overall loss, as it might have bought at lower levels or engaged in intra-quarter reductions and re-additions.

Furthermore, for institutions like Goldman Sachs, positions beyond spot ETFs often involve overlays of options, hedges, and market-making related holdings. Looking solely at the table can easily lead to misinterpreting trading behavior as a long-term stance.

Yet, precisely because of its incompleteness, the 13F serves more as a window into institutional sentiment than a final conclusion sheet. Seeing Abu Dhabi's Mubadala increase its position while its book value falls reveals sovereign patience. Seeing Brown University hold steady and absorb the drawdown shows long-term allocation discipline. Seeing Harvard reduce Bitcoin and exit Ethereum ETFs reveals the genuine sensitivity of university endowments to volatility. And seeing JPMorgan, Wells Fargo, and Jane Street continue to adjust their exposures in certain products demonstrates that Wall Street still treats crypto ETFs as a product category that needs to be constantly stocked on the shelf and continually re-priced.