分发为王:Robinhood正在吞噬预测市场

- 核心观点:Robinhood 通过将事件合约(预测市场)集成到其多资产交易平台,构建了强大的分发护城河。这种交叉销售策略不仅创造了年化超过4亿美元的收入,还使其相对于Kalshi和Polymarket等独立平台具备显著的竞争优势,并可能通过自有清算实体Rothera进一步捕获价值。

- 关键要素:

- Robinhood 的预测市场业务在九个月内交易了120亿份合约,2026年第一季度已录得88亿份,年化收入超4.15亿美元。

- Robinhood 通过集成Kalshi的合约,将其分发至2740万付费用户,贡献了Kalshi第一年50%的交易量,体现了强大的分发能力。

- Robinhood 正在将事件合约嵌入股票、加密货币等资产页面,使用户能在同一屏幕进行跨资产对冲,从被动经纪商转变为信息定价平台。

- Robinhood 通过合资公司Rothera收购了CFTC许可的清算机构,未来可自主上市任何事件合约,经济上能将有效收入翻倍。

- 监管风险对Kalshi和Polymarket构成生存威胁,二者超60%的收入来自体育合约;而Robinhood可通过多样化资产类别降低风险。

- 模型预测,即使是在熊市情景下,Robinhood的预测市场业务到2028年价值可达120亿美元,远超Kalshi当前估值。

- 将预测市场集成到零售经纪商中,不仅服务现有交易者,更成为其他所有用户的信息定价工具,这是独立平台难以复制的优势。

Original Author: @Decentralisedco

Original Translation: AididiaoJP, Foresight News

In a previous article, we explored how HIP-4 brings structured products to Hyperliquid. Robinhood has a similar play through its recent foray into prediction markets. The table below provides some context.

Fidelity, Schwab, and Interactive Brokers grew up in an era before prediction markets emerged. Even spot cryptocurrencies represent only a small fraction of their overall product offerings. In contrast, Robinhood serves a younger demographic who might want to bet on sports events, go long on semiconductor stocks, actively trade Solana, while also holding crude oil positions in the futures market. A generation of users who grew up "monitoring the situation" will flock to platforms like Polymarket or Kalshi if Robinhood fails to offer the same risk assets.

One way to mitigate this risk is to offer event contracts. These are binary instruments that settle on a "Yes" or "No" outcome. Each contract is priced between $0 and $1, reflecting the market's real-time probability of an event occurring. If you are correct, the contract settles at $1; if wrong, it settles at $0. The user's entry cost is effectively the probability of the event. For example, a contract trading at $0.60 for the Strait of Hormuz to be open by May 30 signals the market's belief. If most people are certain an event will happen, there is little room to profit from it.

On Robinhood, these tools can act as hedges. You could go long on the Strait of Hormuz being open while also going long on crude oil prices, assuming that if the strait is not open, oil prices will remain high.

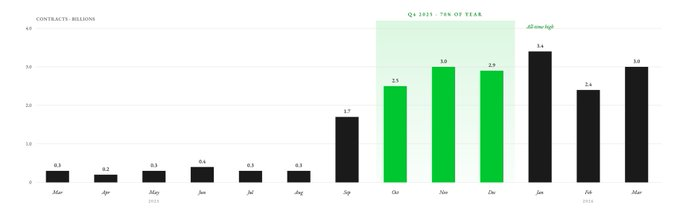

Robinhood first launched its prediction markets business in March 2025, routing orders to clients through KalshiEX. In nine months, users traded 12 billion contracts. Approximately 70% of that full-year volume was concentrated in the fourth quarter. In Q1 2026, Robinhood has already recorded 8.8 billion event contracts.

Over 1 million Robinhood customers traded event contracts in 2025. Rather than launching these markets and building liquidity itself, Robinhood directly integrated Kalshi's prediction markets. Robinhood acts as the distribution layer by providing a dashboard for its customers. The entire infrastructure, at least for now, is still supported by Kalshi (more detail on this later).

Kalshi and Polymarket dominate the market, accounting for over 90% of total prediction market volume. Robinhood distributes Kalshi's contracts to its 27.4 million funded customers, who invest across multiple asset classes including stocks, cryptocurrencies, futures, and options. Kalshi is merely a prediction market platform and cannot match this distribution capability.

In fact, Robinhood contributed 50% of Kalshi's trading volume in its first year.

While Coinbase allows users to trade stocks, cryptocurrencies, futures, and options (via the Deribit acquisition), it only launched its prediction market this January. In comparison, Robinhood's prediction market business has been operating for over a year, already generating an annualized revenue exceeding $415 million. Robinhood also has a significantly higher number of monthly active users (MAUs) than Coinbase, at 13.5 million versus Coinbase's 9.2 million.

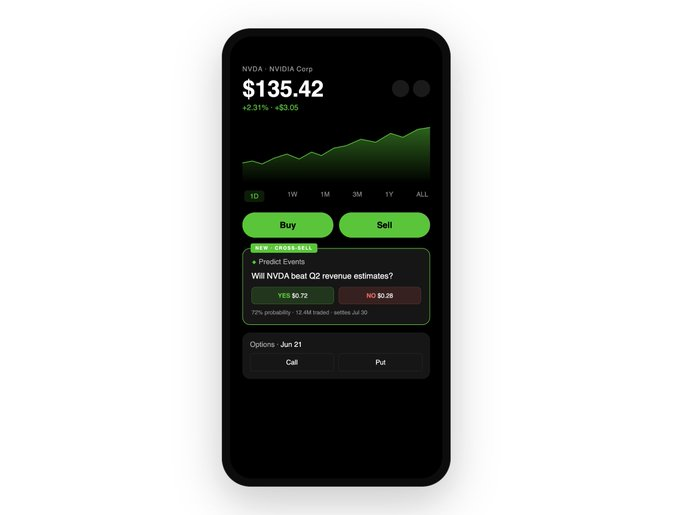

Prediction markets on Robinhood can evolve further. Currently, they exist as a separate Hub within the app, disconnected from the rest of the platform. But soon, they could be cross-linked with assets like stocks, options, and cryptocurrencies – allowing Robinhood's stock traders to directly purchase prediction market event contracts.

Imagine opening the stock page for Nvidia before its earnings report. You see the usual information: stock price and option chain. But now, you also see an event contract right next to it: "Will Nvidia beat Q2 revenue estimates?" The contract is trading at $0.72, implying the market sees a 72% probability of a beat. You think the market is underestimating demand for Nvidia's products.

In this scenario, Robinhood lets you buy the stock, buy call options, or buy 500 "Yes" contracts at $360 – earning you $140 if you are correct ($0.28 profit per contract × 500 contracts).

Robinhood places these three instruments on the same screen, without needing to switch tabs.

As illustrated earlier with crude oil, you can also use these tools to hedge positions. You could bet on Nvidia beating estimates while simultaneously shorting the stock to hedge your prediction market wager. Thus, Robinhood allows you to build a cross-asset hedging strategy on the same screen in under a minute.

So far, this integration on the stock trading page has worked well for Robinhood, but it is still leaving money on the table. That will change soon, as Robinhood is about to take the next step.

Richer Context for Information Pricing

Robinhood's moat lies in providing users with all relevant information right where and when they need it most. The days of buying Bitcoin on Coinbase, trading options on Deribit, holding stocks on Robinhood, and trading crude oil futures on IBKR are over. Users want to avoid switching contexts and platforms.

Once Robinhood embeds prediction markets into all asset pages, it transforms from a passive broker into an information pricing platform. Beyond price and analyst ratings, Robinhood will offer a real-time probability market for events related to that stock. Event contracts reflect the real-time consensus of participants with skin in the game. These contracts help users make better decisions, even if they never trade a single prediction market contract themselves.

Take Nvidia again. The stock price at any moment reflects the sentiment of those holding the underlying equity. Along with equity come legal rights, shareholder reports, analyst Q&A sessions, and a framework for investor protection developed over 400 years. But most of the time, traders might not care about all that. The information they want to price might simply be "Will Nvidia beat revenue estimates?" In this case, prediction markets can (arguably) be a better source of pricing information than the stock price itself. Robinhood's attempt to bring derivatives, event contracts, and equities all under one roof is precisely about capturing value from every user who might want to trade on that event.

But Polymarket and Kalshi have been doing this for years, so where is Robinhood's moat? Why not simply integrate third-party markets into its interface to increase revenue, instead of owning these markets itself? Cross-selling and volume provide a clearer picture of the incentive mechanism.

Cross-Selling as a Regulatory Moat

In March 2026, two bipartisan bills were introduced aiming to ban sports-related event contracts at the federal level. There are also legal hurdles at the state level. This is an existential crisis for platforms like Kalshi – 89% of its 2025 fee revenue came from sports-related event contracts. Similarly, about 60% of Polymarket's open interest also comes from sports-related event contracts.

If sports contracts face legal setbacks, Kalshi and Polymarket would be hit hardest. Without this dominant category, they cannot sustain valuations exceeding $20 billion. Although Robinhood also started heavily with sports markets, its cross-selling capability allows it to diversify revenue into stock and macro events (like earnings, Fed decisions, CPI data, and employment reports).

For Robinhood, sports are just one revenue stream. For Kalshi, the sports category is almost everything. Any regulatory crackdown on sports-related markets could threaten the claims of Kalshi and Polymarket to valuations over $20 billion. Robinhood is now positioning itself higher up the value chain through a joint venture called Rothera.

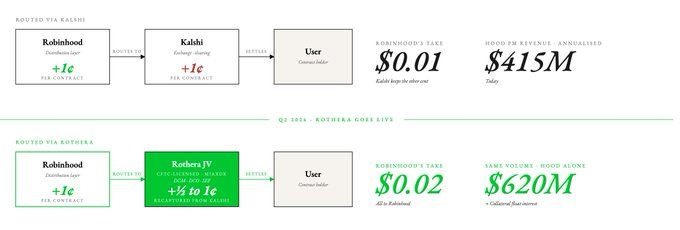

In November 2025, Robinhood formed a joint venture named Rothera LLC. This joint venture subsequently acquired MIAXdx – a CFTC-regulated Designated Contract Market (DCM), Derivatives Clearing Organization (DCO), and Swap Execution Facility (SEF). This fundamentally changes the economics, control, ownership, and clearing/settlement processes for event contracts.

Relying on Kalshi to provide event markets limited the types of contracts Robinhood could list on its prediction market. Rothera allows Robinhood to list any event contract at any time.

From an economic standpoint, this likely means Robinhood can capture the penny currently going to Kalshi, effectively doubling its event contract revenue. If Robinhood can route half of that revenue to its own entity, its prediction market revenue could increase by 50% based on current event contract fee rates, reaching $620 million.

There is reason for optimism regarding this joint venture, as the latest quarterly results show Robinhood has started investing in Rothera. The Q1 2026 results included $14 million in joint venture-related costs. There's also a small additional benefit: once prediction market contracts are routed through Rothera, the collateral backing open positions will sit on Robinhood's balance sheet, adding interest income to its revenue. With open interest collateral reaching around $100 million, this could generate an additional $4-5 million in annual revenue.

Every trading platform has a simple mission: get traders to move money as frequently as possible and charge a small fee on each transaction; or get them to park large amounts of idle capital and retain the interest income. For Robinhood, the latter strategy seems to be taking shape.

Robinhood's cross-selling moat via prediction markets is similar to the moat we previously identified for Hyperliquid through its HIP-4 event contracts. Hyperliquid's unified risk engine integrates primitives like spot, perpetuals, deployment markets, and prediction markets, ensuring capital efficiency in a decentralized marketplace. The same logic applies to Robinhood, albeit within a centralized market.

Kalshi lacks Robinhood's distribution moat across different asset classes. A standalone prediction market product is far less valuable than prediction markets embedded within all other trading products. Coinbase has only just ventured into prediction markets, while Robinhood's advantage of integrating its full asset stack with event contracts on a single screen gives it a step ahead over Coinbase in the prediction market space.

By the Numbers

Any discussion comparing the valuations of Coinbase, Kalshi, and Robinhood essentially tries to answer the same question: What is the lifetime value of a user on each platform? Kalshi users might be fewer, but they pay significantly higher fees. If Robinhood can match Kalshi's liquidity at lower fees, the same user will trade entirely on Robinhood.

The market has already recognized this difference. Kalshi and Robinhood trade at similar valuation multiples (15x), while Coinbase trades at a lower multiple of 7.5x. For Kalshi, prediction markets represent 100% of its revenue. For Robinhood, it's only 7%. For Coinbase, the number is negligible.

Once Rothera is operational, Robinhood can price its offerings more competitively than any standalone prediction market platform. It can undercut Kalshi's fees, absorb the margin hit, and still grow because every prediction market user is also a potential customer for stocks, options, and cryptocurrencies. Kalshi is not remaining silent; it reportedly plans to launch cryptocurrency trading, starting with perpetuals. But transitioning from a prediction market to a multi-asset platform is far more difficult than integrating prediction markets into an existing multi-asset trading platform.

Robinhood has spent over a decade acquiring 27.4 million funded customers and building deep liquidity, market maker relationships, compliance infrastructure, and user trust. Kalshi would have to start from scratch.

One way to understand the value of this business is to hypothetically spin off Robinhood's prediction market business and take it public independently. If it has $415 million in ARR and the same growth trajectory, what would it be worth? The simplest answer is 15x, Kalshi's multiple, which would be $6.2 billion. But all else being equal, a Kalshi with Robinhood's revenue line would be valued much higher.

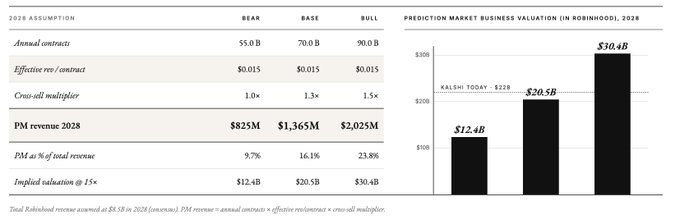

We constructed an estimation model for the next three years using the following assumptions:

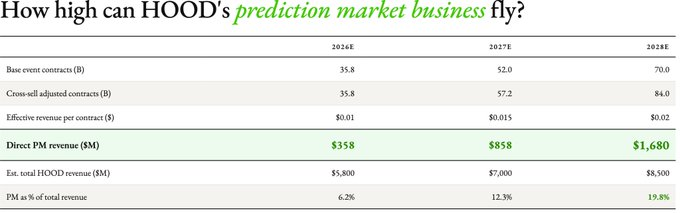

- Contract Volume: 70 billion event contracts in 2028 under the base case scenario. This assumes a CAGR of approximately 40% over the next two years, based on Robinhood having already recorded 8.8 billion contracts in Q1 of this year (annualized to roughly 35 billion).

- Rothera Economics: We expect effective revenue per contract to rise from $0.01 to either $0.015 under a bear case scenario, or $0.02 under the base/bull case scenarios (after three years).

- Cross-Selling Lift: A multiplier of 1.0x in 2026 (cross-linking not yet live), 1.1x in 2027 (initial stock page integration), and 1.2x in 2028 (mature adoption). This assumes cross-selling adds 10-20% incremental volume on top of organic prediction market growth.

- Robinhood Total Revenue: Using consensus estimates of $5.4 billion in 2026, $6.4 billion in 2027, and $7.2 billion in 2028.

We then stress-tested three scenarios for 2028: bear, base, and bull.

Even under the bear case scenario, Robinhood's prediction market business alone would generate $825 million in revenue by 2028 – more than three times Kalshi's 2025 revenue ($260 million). Using Kalshi's current revenue multiple (15x), Robinhood's prediction market business would be worth $12 billion in this scenario. Under the most optimistic scenario, it could be worth $30 billion by 2028.

What we are likely witnessing is a business with a distribution moat carving out a new market and keeping most of the value for itself. The open question now is whether Polymarket and Kalshi are a repeat of OpenSea in 2021, or if they can successfully reinvent themselves when new threats emerge. Polymarket has expanded its perpetual products in recent days, but its users are unlikely to switch to perpetual trading because prediction markets were their original purpose. In contrast, Robinhood benefits from a core user base that came for its high-risk, zero-fee trading tools. The latter seems to have an advantage over the former.

Today, the market views Robinhood as a traditional finance broker with an added prediction market product, which is why prediction markets account for only 7% of its revenue. But if Robinhood CEO Vladimir Tenev delivers on his stated direction, Robinhood will become a platform that simultaneously prices every financial opinion on earnings, interest rates, elections, and commodities in real-time, while also facilitating trades in the assets driven by those opinions.

A standalone prediction market only attracts people who already trade event contracts. In contrast, a prediction market integrated into a retail broker becomes an information pricing machine for everyone else. Vertical integration by capital aggregators is everywhere.