Strategy Q1 Earnings Report: Book Loss of $14.4 Billion, Possibility of Selling Bitcoin to Pay Interest Not Ruled Out

- Key Takeaway: Strategy's Q1 2026 earnings report shows a net loss of $12.54 billion, primarily due to unrealized losses from the decline in BTC price. However, the company still increased its BTC holdings and relied on STRC preferred stock financing. At the same time, it hinted for the first time at the possibility of selling BTC to pay dividends, attracting market attention.

- Key Elements:

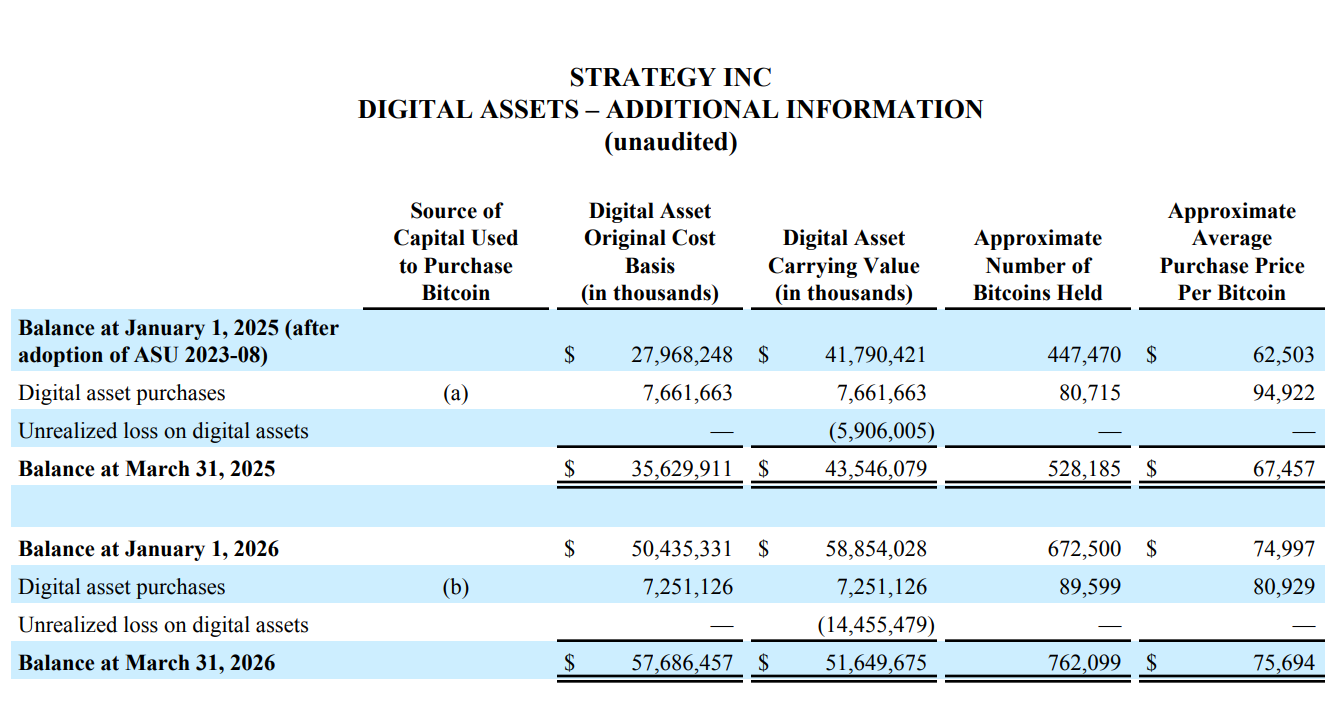

- Q1 net loss of $12.54 billion, mainly from $14.46 billion in unrealized losses; holds 818,300 BTC at an average price of approximately $75,537.

- The company explicitly mentioned the possibility of "selling BTC to pay dividends" for the first time. Current net debt stands at $8.17 billion, with cash reserves of only $2.21 billion.

- STRC preferred stock reached a market value of $8.5 billion within 9 months, becoming the world's largest preferred stock. Q2 financing structure shifted, with STRC accounting for over 80%.

- Purchased 89,599 BTC in Q1 (average price $80,929), but the net loss of $12.54 billion reflects the impact of the BTC price decline.

- Software revenue was only $124.3 million, completely marginalized; historical retained earnings turned negative for the first time, with a cumulative deficit of $6.47 billion.

- In the DeFi ecosystem, $270 million of STRC was absorbed by protocols like Apyx for use as on-chain collateral assets.

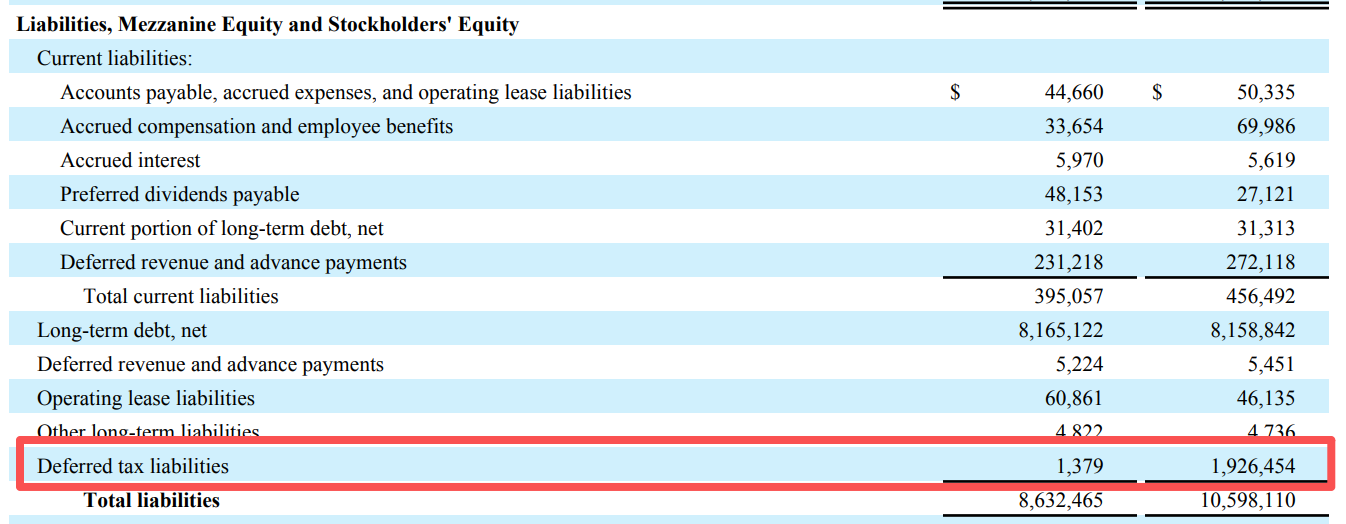

- Deferred tax liabilities decreased from $1.93 billion to $1.38 million. It is estimated that there will be no taxable profit for the next ten years, making tax credits effectively useless.

Original by Odaily Planet Daily (@OdailyChina)

Author: Wenser (@wenser 2010 )

In the early hours of today, the 2026 Q1 earnings call of Strategy officially concluded, and the Q1 financial report was released. Thus, the real operational status of this "industry heart," holding 818,300 BTC, was once again exposed to the market. Behind the net loss figure of $12.54 billion lies the fact that the BTC price once dropped to around $62,000, the continuous accumulation of 63,400 BTC, and the STRC market cap growing to $8.5 billion.

Of course, the most intriguing part of the financial report and Michael Saylor's public statements revolves around the suggestion that "Strategy may sell some BTC to pay dividends." Perhaps influenced by this news, despite Q1 performance falling short of market expectations, the capital market looked favorably upon it, with Strategy's stock price rising slightly by 3%.

Odaily Planet Daily summarizes the key points and future potential highlights from the Q1 financial report as follows.

Q1 Book Net Loss of $12.5 Billion; Possibility of Selling BTC to Pay Dividends Not Ruled Out

Key Point 1: Selling BTC is No Longer Impossible, But an Option

Looking closely at the Q1 financial report and earnings call content, Strategy repeatedly mentions in its forward-looking statements and KPI descriptions: "If convertible notes mature or are redeemed without being converted into common stock, the company may need to sell common stock or Bitcoin to generate sufficient cash to meet these obligations."

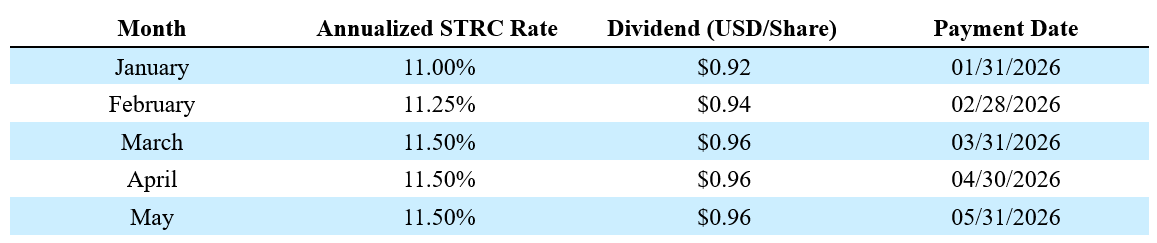

As of the end of Q1, Strategy had net long-term debt of $8.17 billion, preferred stock redemption value of $10 billion, and only $2.21 billion in cash. Meanwhile, the company needs to continuously pay preferred stock dividends (currently STRC annualized rate of 11.5%) and has already begun issuing common stock to finance dividends. If BTC prices continue to face pressure, leading to constrained financing windows, selling coins to repay debt will transition from a theoretical assumption to a practical possibility, which will inevitably have a knock-on effect on the market.

Strategy founder Michael Saylor stated, "This is just to send a message to the market that this model (referring to verifying that Bitcoin assets can support shareholder returns within a corporate treasury framework) has been realized."

It is worth noting that, unlike traditional companies' "KPI indicators," Strategy has created its own set of KPIs, including: BPS (Bitcoin Per Share), BTC Yield (9.4%), BTC Gain (63,410 BTC), and BTC$ Gain ($4.97 billion in USD Bitcoin Gain) (Odaily Note: All data as of May 3rd). However, in the disclaimer, it also points out that these indicators do not consider debt, do not consider the senior liquidation preference of preferred stock, do not represent return on investment or fair value gains, and "BTC dollar gains can be positive while the company is recording significant fair value losses." In fact, Strategy's Q1 business performance corroborates this mechanism: KPIs show $4.97 billion in BTC dollar gains, but under GAAP accounting, an unrealized loss of $14.46 billion was recorded. The core function of this KPI system is to maintain the capital market narrative, not to reflect the true financial condition. Simply put, "spinning bad news into good news" or "reporting only the good news while hiding the bad" is a common tactic Strategy employs in the capital market.

As of May 3, 2026, Strategy held 818,334 Bitcoin, a 22% increase year-to-date. However, the Q1 financial report recorded a net loss of $12.54 billion, almost entirely from unrealized losses on digital assets ($14.46 billion). The total cost basis for the 818,334 BTC is $61.81 billion, corresponding to an average purchase price of approximately $75,537 per BTC. Notably, thanks to the recent market rebound, the unrealized gain for Q2 stands at $8.3 billion.

Key Point 2: Spent $7.25 Billion Buying BTC in Q1, But Book Value Shrank by $7.2 Billion at Quarter End

Simply looking at the buying and selling figures, Strategy's Q1 statement barely qualifies as "breaking even."

Financial data shows Strategy purchased 89,599 BTC in Q1 at a cost of $7.25 billion, averaging around $80,929 per BTC. However, due to the decline in BTC, the book value of digital assets fell from $58.85 billion at the start of the year to $51.65 billion, a net decrease of approximately $7.2 billion.

Admittedly, continuously leveraging up (through financing and dividends) to buy the dip on BTC during a bear market and achieving this result is quite commendable.

Key Point 3: The Impact of AI on Strategy is Objectively Present; Software Business Revenue is Completely Marginalized

Nominally, Strategy still publicly insists it is an "AI-driven enterprise analytics software company," evidenced by the software subscription service revenue, license revenue, and product support revenue present in its income structure.

However, comparing the structure, Strategy's total Q1 software revenue was only $124.3 million, with a gross profit of just $83.35 million. In contrast, its BTC holdings' market value was a staggering $64.1 billion, a quarterly revenue difference of over 500 times, clearly signaling to the market: In the era of significant AI development, the software business, merely tangentially related to AI, has been completely marginalized.

Key Point 4: STRC Becomes the Highlight Business, Reaching $8.5 Billion Market Cap in 9 Months

As Strategy's "financing weapon," STRC's market performance during the protracted bear market has been a true "lifeline."

Currently, STRC (Variable Rate Series A Perpetual Preferred Stock) has grown to a scale of $8.5 billion in just 9 months, becoming the largest preferred stock by market cap globally. Year-to-date, Strategy has raised $5.58 billion through STRC, a growth rate of 189%.

Furthermore, Strategy indicated that STRC's Sharpe ratio is 2.53, volatility is only 3%, and average daily trading volume is $375 million. This means that through STRC, a low-volatility, high-yield, high-liquidity fixed-income product, a new BTC reserve-backed asset has emerged in the traditional financial market.

Key Point 5: Major Shift in Q1/Q2 Financing Structure; STRC Becomes the Main Financing Tool

In the financial report, of the $7.37 billion in financing completed by Strategy in Q1, MSTR common stock ATM contributed $5.3 billion, while STRC contributed $2.07 billion, a ratio of roughly 72% to 28%. However, after entering Q2 (April 1st to May 3rd), this structure reversed – STRC contributed $3.51 billion in financing, while MSTR only contributed $810 million.

This indicates that the financing gap left by common stock is shrinking, and Strategy is increasingly relying on preferred stock offering fixed income to maintain its capital reserves, thereby continuously driving BTC accumulation.

Additionally, perhaps considering STRC's stellar performance and strong capital appeal, Strategy is actively promoting this "wealth management fixed-income product" in traditional financial markets. The company has launched a proposal for semi-monthly STRC dividend payments, aiming to shorten the dividend payment cycle to attract more capital for purchases.

Key Point 6: Strategy Posts First-Ever Accumulated Historical Earnings Deficit

In traditional financial markets, retained earnings are an important indicator of a company's financial health, representing the cumulative result of all net profits minus all dividends since the company's inception. In other words, it's the company's "cash reserve."

From its founding in 1989 to the end of 2025, after over three decades of operation, Strategy had accumulated profits of $6.32 billion on its books. However, by the end of the first quarter of this year, this figure had turned negative, leaving an accumulated deficit of $6.47 billion.

This is a direct consequence of the ASU 2023-08 accounting standard (Odaily Note: This standard requires listed companies to measure BTC at fair value from 2025 onwards, with price changes directly impacting the income statement). From the perspective of GAAP, commonly used in traditional financial markets, Strategy's accumulated historical profits over more than three decades have been completely wiped out by one quarter's BTC decline.

Of course, what goes down can come up. If BTC prices recover subsequently, this figure can turn positive again. This indicator once again highlights the high risk and high volatility of crypto assets compared to traditional financial assets.

Key Point 7: DeFi Ecosystem Centered on STRC is Under Construction

Strategy's Q1 financial report mentioned that DeFi protocols like Apyx and Saturn have absorbed over $270 million worth of STRC assets; $150 million worth of STRC assets have been incorporated into corporate treasury reserves by listed companies like Prevalon, Strive, and Anchorage.

In other words, STRC is evolving from a simple preferred stock financing tool into a foundational collateral asset for the on-chain ecosystem of the cryptocurrency market. If STRC's appeal to capital markets and the crypto ecosystem continues to grow (Odaily Note: Fixed income is quite attractive in the wealth management space, whether in traditional financial markets or crypto markets), STRC could gradually surpass MSTR (traditional preferred stock).

Of course, there are trade-offs. As the proportion of STRC increases, the demands on Strategy's dividend-paying capacity will be higher, and the potential risk transmission to the broader market will be more extensive.

Key Point 8: Tax Deduction Potential Exists, But Will Not Be Utilizable for Over a Decade

Aside from operational data, Strategy's Q1 financial report also mentioned a drastic change in deferred tax liabilities.

According to the table data, Strategy's deferred tax liabilities plummeted from nearly $1.93 billion at the start of the year to just $1.38 million at the end of Q1, nearly zeroing out.

In other words, Strategy previously had a "provision for income tax" of nearly $1.93 billion due to unrealized gains from its business profits. However, because business losses driven by the BTC decline offset these gains, the company's asset income statement recorded this unpaid tax as an "income tax benefit." Furthermore, Strategy's $14.46 billion unrealized loss in Q1 should theoretically offset some taxes, meaning the company's operating losses reduced its tax payable, creating a "tax shield."

The problem, however, is that this tax shield is only effective if Strategy actually has taxable profits in the future. Yet, it indicated it does not expect to have taxable profits for over ten years. In other words, Strategy gained a $1.9 billion "tax deduction benefit" due to the BTC decline, but because it likely won't have taxable income in the foreseeable future, this benefit will probably not be realized.

Finally, aside from buying Strategy-related stocks, a prediction market event on "Whether Strategy will sell Bitcoin by the end of the year" has gone live, with the "Yes" probability currently at 44%.