Crypto Market Macro Report: Bitcoin Returns to $80,000, Dramatic Reversal in US-Iran Situation, and Fed Leadership Change

In early May 2026, the global crypto market exhibited extreme divergence and high uncertainty under the combined influence of three major macro variables. On the geopolitical front, Trump grandly announced the launch of "Operation Freedom" on May 4th to escort commercial vessels in the Strait of Hormuz, only to dramatically suspend it a day later, claiming "significant progress has been made towards a comprehensive US-Iran agreement." However, Iran insists it remains in a state of war with the US and continues to close the Strait, demanding that all transiting vessels obtain permission from Iran. On the Federal Reserve front, around May 15th, Kevin Warsh is officially set to replace Jerome Powell as Chair, while the April 30th FOMC meeting left rates unchanged as expected.

- 核心观点:2026年5月,加密市场处于地缘政治(美伊冲突)、货币政策(美联储换帅)与机构化深化(ETF逆势吸筹)三重主线交织的复杂节点。尽管宏观逆风持续,但机构与长期持有者的锁仓行为及减半周期规律,表明当前更可能为牛市中的深度调整,而非熊市开端。

- 关键要素:

- 地缘博弈剧变:美伊“自由计划”护航行动戏剧性暂停,但霍尔木兹海峡实质封锁风险未消。油价飙升已推高高盛核心PCE通胀预测至2.6%,形成“滞胀式”宏观环境,双向压制比特币的避险属性和风险资产估值。

- 美联储政策十字路口:沃什接替鲍威尔任主席,其“鹰鸽混合”立场及内部分歧加剧政策不确定性。褐皮书显示能源成本全线上涨侵蚀企业利润,降息路径将更曲折,对流动性敏感的加密市场构成中期压制。

- 机构逆势吸筹信号明确:在价格回撤至76,000-81,000美元区间时,现货BTC ETF单日净流入高达6.3亿美元。截至5月初,ETF总资产净值达1,037.85亿美元,占BTC总市值的6.66%,表明机构在弱势中稳健建仓。

- 供需结构深刻变化:自ETF获批以来,已累计吸收超58万枚BTC(约三年产量),叠加长期持有者供应量持续上升,双重锁仓格局导致实际流通供应收缩,为价格提供隐性底部支撑。

- 减半周期规律验证:当前时点(2026年5月)处于2024年4月减半后的12-18个月价格发现窗口内。历史规律显示此阶段多为“洗盘蓄势”,而非周期顶部,但机构化新环境下的有效性存不确定性。

1. Geopolitical Chess Game: The "Operation Freedom" Reversal in the Strait of Hormuz and the Resurgence of Inflation

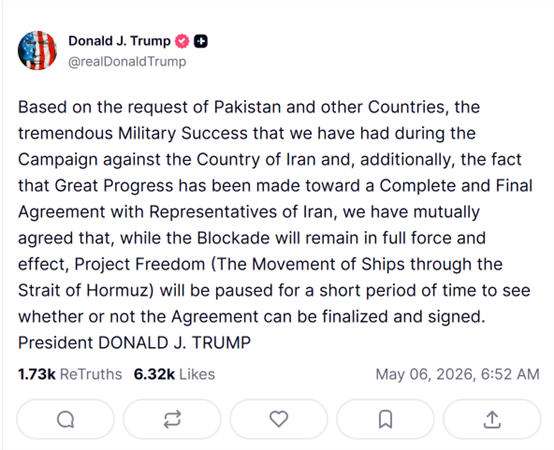

On May 4, 2026, US President Donald Trump announced on Truth Social that the United States would officially launch "Operation Freedom," a convoy escort mission for commercial vessels in the Strait of Hormuz, starting that morning Middle East time. The operation would involve guided-missile destroyers, over 100 land-based and sea-based aircraft, multi-domain unmanned platforms, and 15,000 active-duty troops. The US characterized it as a "defensive humanitarian operation," ostensibly to bypass the 60-day authorization limit for presidential military action under the War Powers Act. However, just one day later, Trump posted again, stating that due to "major progress in the comprehensive US-Iran agreement," he decided to suspend "Operation Freedom," but emphasized that the naval blockade of Iran "will continue to be fully and effectively implemented." This dramatic reversal caught global markets off guard, causing crude oil prices to fluctuate violently following the announcement.

Iran's stance was significantly more rigid than the US portrayal. Ali Akbar Velayati, a foreign affairs advisor to Iran's Supreme Leader, explicitly stated that the Strait of Hormuz is closed and will not reopen unless "the national will of the Islamic Republic of Iran decides otherwise." He added that all vessels planning to transit the strait must submit an application via official email and obtain an Iranian permit before passage. The head of Iran's National Security and Foreign Policy Committee warned that any foreign armed forces, especially the US military, approaching or entering the Strait of Hormuz would be attacked. On key issues such as the nature of the ceasefire, the right of passage through the strait, and whether "Operation Freedom" is truly suspended, the US and Iranian positions are starkly divided, indicating that the market's pricing of geopolitical risk is far from a point where one can relax.

The immediate consequences of this geopolitical struggle are already partially visible in global inflation data. Driven by the dual shock of escalating US-Iran military conflict and the UAE's announcement on May 1st to leave the OPEC+ alliance, international oil prices continued to rise from late April to early May, significantly pushing up energy costs. Goldman Sachs subsequently raised its year-end core PCE inflation forecast from 2.5% to 2.6% and its overall PCE forecast from 3.1% to 3.4%. More concerning is that this inflationary push does not stem from overheated demand but from supply-side shocks (oil prices) compounded by tariff effects. This makes the Fed's monetary policy response mechanism far more complex – hesitant to raise interest rates for fear of exacerbating downward economic pressure, yet unable to initiate rate cuts due to the rising risk of de-anchored inflation expectations. For Bitcoin, this "stagflationary" macro environment has historically exerted downward pressure from both sides: its safe-haven status remains without broad consensus, while expectations of tightening liquidity continue to suppress risk asset valuations.

2. On the Eve of a Fed Chair Change: Beige Book Warnings and the Crossroads of Policy Independence

In mid-May 2026, the Federal Reserve is set to witness its most controversial leadership transition in modern history: Kevin Warsh will officially succeed Jerome Powell as Chair. In a break with a 75-year tradition, Powell will remain on the Board of Governors after stepping down as Chair. The market broadly interprets this arrangement as a political compromise signifying an "incomplete decoupling" between the White House and the Fed. Warsh's policy stance presents a nuanced "hawkish-dovish mix." He leans hawkish on inflation control and balance sheet management, emphasizing monetary policy discipline and framework restructuring, and has publicly criticized the Fed's ultra-easy policies over the past 20 years as having "seriously strayed from its mission." However, he leans dovish on the long-term interest rate path, acknowledging technology's natural dampening effect on inflation and supporting rate cuts when data permits. This mixed stance creates significant divergence in market views on the monetary path under the "Warsh era," making it a key source of uncertainty for macro pricing in the crypto market in May.

The FOMC meeting concluding on April 30th was Powell's last as Chair. As widely anticipated, the Committee held the federal funds rate steady at 3.50% to 3.75%. The post-meeting statement and Powell's press conference conveyed a complex picture. On one hand, the impact of rising energy prices on inflation "has already begun to materialize and could broaden further in the near term." Powell explicitly stated that "no officials currently favor a rate hike, but some favor paring back the easing bias in the statement." On the other hand, Powell emphasized he would "not be a shadow chair" after stepping down, attempting to soothe market concerns about impaired Fed independence. However, just days after the meeting, internal Fed divisions became apparent: Stephen Miran, a Trump-nominated governor, dissented in favor of a rate cut, while hawkish figures like Cleveland Fed President Beth Hammack and Minneapolis Fed President Neel Kashkari also dissented, but in favor of holding rates steady (a different direction than Miran's). This deep internal rift casts a shadow of extreme uncertainty over Warsh's first FOMC meeting.

The Fed's Beige Paper released on April 16th provides valuable grassroots insight into the current state of the US economy. The report indicated that eight of the twelve Federal Reserve Districts experienced modest to moderate growth, activity was essentially flat in two districts, and two districts reported modest to moderate declines. The most noteworthy inflation-related statement was: "Energy and fuel costs rose substantially across all 12 Districts," with businesses broadly reporting that input cost increases outpaced selling price increases, compressing profit margins. Firms are finding decisions on hiring, pricing, and capital investment more complex, with "wait-and-see" becoming the most common business strategy. For crypto assets, the core signal from the Beige Book is that while the US economy isn't falling into recession, growth momentum is being eroded by energy inflation. The Fed's path for rate cuts will be more circuitous than previously anticipated by the market, creating a continued overhang for the liquidity-sensitive crypto market in the medium term.

3. The Deep End of Institutionalization: ETF Inflows Buck the Trend and Mining Companies Optimize Balance Sheets

Amidst Bitcoin's significant pullback from its highs, contrarian institutional buying represents the most noteworthy structural signal in the crypto market for May 2026. According to SoSoValue data, on May 1st (EST), US spot Bitcoin ETFs recorded a net inflow of $630 million in a single day. BlackRock's IBIT led with $284 million, followed by Fidelity's FBTC with $213 million. On May 4th, spot ETFs recorded another $532 million in net inflows. This capital flow showed a significant divergence from BTC's price action. While the price oscillated repeatedly in the $76,000 to $81,000 range, ETFs consistently recorded net inflows, indicating steady accumulation by institutions during price weakness – a pattern distinct from retail FOMO buying. As of early May, the total net asset value of US spot BTC ETFs reached $103.785 billion, representing approximately 6.66% of BTC's total market cap. The rising share of institutional holdings is fundamentally reshaping Bitcoin's price discovery mechanism – transitioning from a retail-driven, highly volatile speculative asset towards an institutional allocation asset.

From a broader perspective, deepening institutionalization is reshaping Bitcoin's supply-demand dynamics. Since the approval of US spot Bitcoin ETFs in January 2024, these ETFs have cumulatively absorbed over 580,000 BTC, roughly equivalent to three years of Bitcoin's network issuance. Concurrently, the supply held by long-term holders has been rising steadily since mid-February 2026, indicating that long-term investors' willingness to hold increases, rather than decreases, during price corrections. This dual "institutional + long-term holder" lock-up pattern is causing the actual circulating supply of Bitcoin to contract continuously, providing tacit support for prices amidst the macro headwind.

4. Bitcoin Back at $80,000: Halving Cycle Patterns and the Bull-Bear Dialectic at the Current Juncture

As of early May 2026, Bitcoin is staging a critical comeback from a deep correction. BTC fell to a low near $60,000 in early February, then rebounded strongly to reclaim the $80,000 level in early May, representing a gain of over 33% from the cycle low. This "return to $80,000" still represents roughly a 46% retracement from the all-time high set in October 2025. However, compared to the panicked retail selling and mass mining farm shutdowns of the 2018 and 2022 bear markets, this 2026 correction exhibits starkly different structural characteristics: sustained ETF net inflows, rising long-term holder supply, and top mining companies optimizing their balance sheets rather than cutting production or exiting. These signals collectively point to the assessment that the current phase is more likely a "deep correction within a bull market" rather than the beginning of a "new bear market."

Looking at halving cycle patterns, Bitcoin completed its fourth halving in April 2024 (block reward dropping from 6.25 BTC to 3.125 BTC). Historical data shows that the 12-to-18 month period following a halving is typically the most intense phase of price discovery. BTC broke its prior all-time high roughly 12 months after the 2012 halving; entered its main bull run about 17 months after the 2016 halving; and peaked roughly 12 months after the 2020 halving. Using this historical pattern as a reference, the 12-to-18 month window after the April 2024 halving corresponds to the period from April 2026 to October 2026 – precisely where we are now. This suggests the current price correction is highly likely part of a "shakeout and accumulation" phase post-halving, rather than a cyclical top reversal. Of course, significant uncertainty exists as to whether this historical pattern holds in the new environment of deepening institutionalization.

Technically, the core trading range after Bitcoin's "return to $80,000" is $76,000 to $83,000. The $80,000 level itself represents a key psychological barrier and short-term support, while $83,000 is the location of the 200-day simple moving average (SMA) – a critical "bull-bear line" fiercely contested by both sides. A decisive daily close above $83,000 would open the path towards the $89,000 to $94,000 range. To the downside, $76,000 is the low tested multiple times in April 2026. A breakdown below this level would set a technical downside target towards the $70,000 to $65,000 range. Regarding momentum indicators, the 7-period RSI has risen to 71.27, nearing overbought territory, suggesting potential for a short-term technical pullback. However, the MACD formed a bullish crossover in mid-April, providing some momentum support for mid-term upward movement. Synthesizing these technical signals, the most reasonable assessment at the current juncture is that BTC is in a "confirmation phase after reclaiming $80,000." Range-bound consolidation could persist for another 2 to 4 weeks until clear macro catalysts emerge.

5. Outlook: Three Scenario Projections and Key Observation Points

Combining the three main themes of geopolitics, Fed policy path, and institutional capital flows, the crypto market from May to July 2026 could evolve along the following three scenarios.

Scenario 1 (Probability ~35%): Geopolitical Détente + Dovish Fed Signals → BTC Challenges $89,000 - $94,000. If the US and Iran reach a substantive framework agreement within the negotiation window opened by the suspension of "Operation Freedom," the Strait of Hormuz returns to normal traffic, oil prices fall from highs, and inflation expectations cool. Concurrently, Warsh delivers dovish signals in his first major public speech after assuming office on May 15th. A simultaneous improvement along both fronts would trigger a "double boost" effect on the macro level: risk appetite improves significantly, ETF inflows accelerate, and BTC could break above $83,000 (200-day SMA) within 2 to 4 weeks, challenging the $89,000 to $94,000 range. Key observation points for this scenario: Warsh's inaugural speech around May 15th, the April US non-farm payrolls report released around May 8th, and interim statements from US-Iran negotiations.

Scenario 2 (Probability ~45%): Geopolitical Stalemate + Fed Maintains Wait-and-See → BTC Oscillates in $70,000 - $85,000 Range. This is the most fully priced neutral scenario. The US and Iran cannot reach a comprehensive agreement within the 4-week ceasefire period, but no new large-scale military conflict erupts, leaving the Strait of Hormuz in a "semi-blockaded" state. After taking office, Warsh maintains a "data-dependent" stance. In this scenario, BTC is most likely to trade in a wide range. ETF flows will be the most direct driver of short-term price action. If weekly net inflows stay above $300 million, prices will gravitate towards the upper end of the range. If weekly net outflows reappear, prices will test the lower end. In this scenario, range trading is the most suitable strategy for most investors.

Scenario 3 (Probability ~20%): Geopolitical Conflict Escalates + Inflation Spirals → BTC Retraces to $65,000 - $70,000 Range. If the ceasefire collapses completely, Iran declares a full blockade of the Strait of Hormuz, oil prices break above $120 per barrel, forcing Goldman Sachs to further raise its year-end PCE forecast. Hawkish Fed officials publicly discuss the possibility of "raising rates to combat inflation if necessary." This macro "perfect storm" would simultaneously crush liquidity expectations and risk appetite, potentially causing BTC to break below the $70,000 psychological level. While less probable, if triggered, leveraged positions in the crypto market would face systemic liquidation pressure. In this scenario, cash and short-term Treasuries are the optimal holdings. Bitcoin positions should only be rebuilt after a clear macro turning point is confirmed.

6. Conclusion: Identifying Structural Signals in the Macro Fog

The crypto market in May 2026 stands at a historic confluence of three main themes: geopolitics, monetary policy, and institutionalization. The dramatic reversal of "Operation Freedom," the policy uncertainty from the Fed chair transition, the validation period of the post-halving cycle for Bitcoin, and the structural shift of sustained contrarian accumulation via ETFs – all these create an exceptionally complex and significant macro chessboard. For investors, navigating this phase requires distinguishing "noise" from "signals." The back-and-forth of geopolitical events, the hawkish-dovish debates among Fed officials – these are essentially short-term noise. They impact prices intra-day to weekly but cannot change the medium-term trend direction pointed to by the structural signals of deepening institutionalization and post-halving supply contraction.

Macro headwinds are often long-term allocators' best friends. The macro pressures Bitcoin faces in May 2026 – rising oil prices, a Fed uncertain between hawkish and dovish stances, ongoing geopolitical conflict – are, in reality, much milder compared to the dark days of the March 2020 "liquidity crisis" and the 2022 "FTX collapse + aggressive Fed rate hikes." Meanwhile, the continued rise in institutional holdings, the expanding lineup of ETF products, and the fact that top miners can still optimize their capital structures during a downturn all quietly tell a larger narrative: Bitcoin is gradually evolving from a fringe speculative asset into a permanent member of the global asset allocation landscape. This process is volatile, but the direction is clear. We recommend focusing on three key variables: First, Warsh's inaugural speech around May 15th will determine the direction of the repricing of rate cut expectations. Second, the substantive progress of US-Iran ceasefire talks within the 4-week window will shape the trajectory of oil prices and inflation expectations. Third, if US spot BTC ETFs record net inflows exceeding $500 million for two consecutive weeks, it will be the most direct signal of accelerated institutional accumulation. The macro fog will eventually lift, and those investors who maintain composure and identify structural signals within the fog will be the most composed winners in the next market upswing.