From Crypto Exits to Stock Market Picking Up the Tab: Seeing Through Capital's Universal Cash-Out Playbook

- Core Thesis: Venture capital institutions, by extending the privatization cycle of enterprises and designing compliant exit pathways, redirect the growth dividends that should have flowed to public market retail investors to insiders. This systematically undermines the original "universal participation" covenant of the US capital market.

- Key Elements:

- Traditional Covenant Broken: The US 401k pension system once relied on public market dividends for all. However, companies now delay IPOs until they reach trillion-dollar valuations, meaning growth-stage gains are exclusively captured by pre-IPO shareholders. The public market is left only to execute the payout, not to create value.

- The Trap of "Democratizing Private Equity": To find liquidity for insider stakes, the industry promotes the idea of "democratizing private investment." In reality, this allows retail investors to buy assets accumulated cheaply by insiders at the peak of a bull market. Examples include Figma and Klarna, which saw their valuations halve or crash post-IPO.

- Crypto Industry Precedent: DeFi projects repackage failed locked-up tokens from retail investors into compliant equity assets. Distributed through institutional access, these deals obtain tacit SEC approval for an exit. This model has now been scaled to trillions of dollars by venture capital.

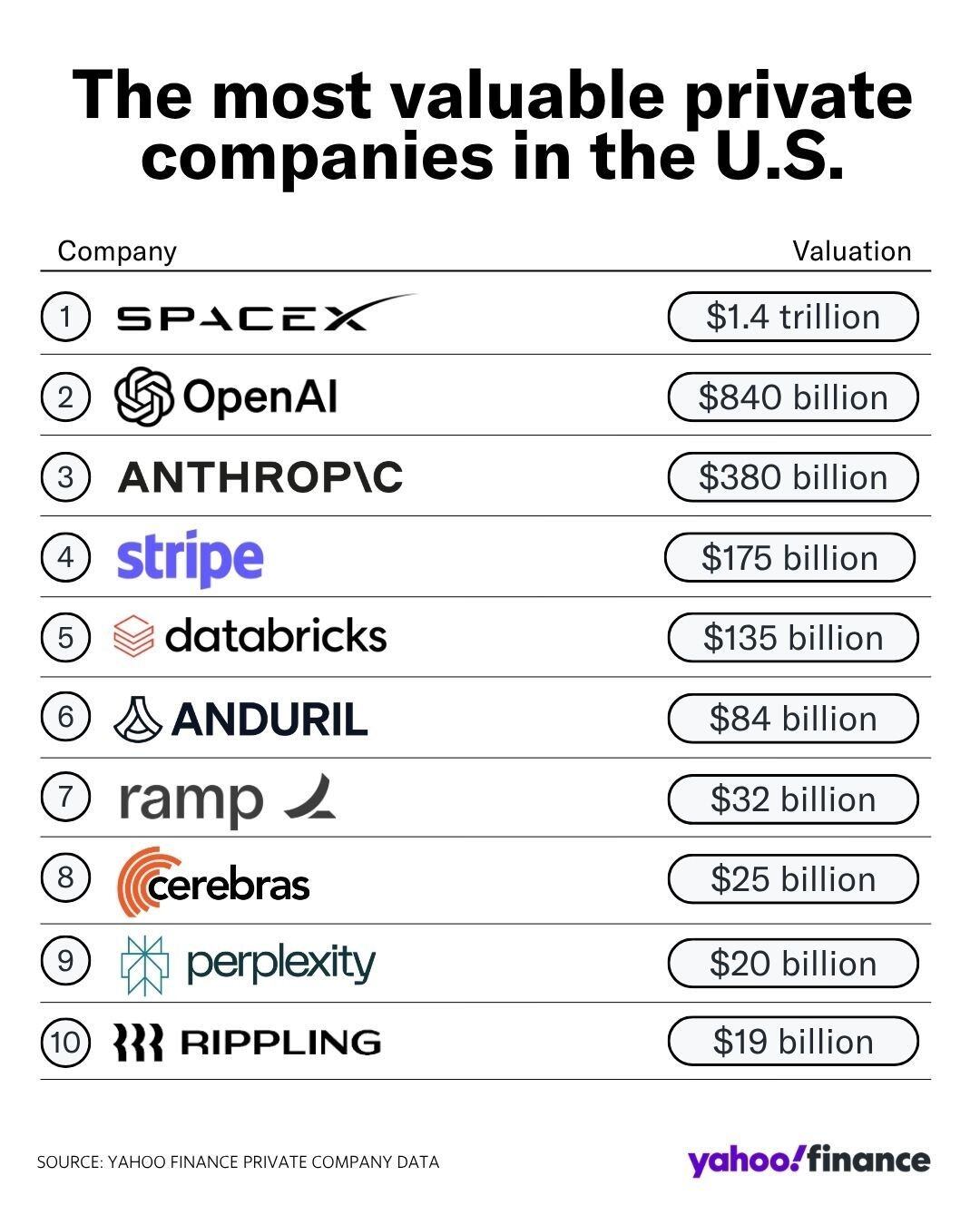

- Nasdaq Rule Loophole: Plans to allow new listings to amplify index weighting by 5x with extremely low public float (e.g., 5%). This forces passive funds to buy without price consideration. Combined with the precise timing of insider lock-up expirations, this enables a neat cash-out. The scenario of a SpaceX listing mid-year with portfolio rebalancing at year-end serves as a case study.

- Societal Consequences: Ordinary workers perceive a class divide between "early insiders" and "late-stage bag holders." This leads to political backlash against the elite technocratic class (e.g., Sam Altman), including public criticism, vandalism, and other forms of resistance. The K-shaped divergence of wealth intensifies.

Original Author: Tulip King

Original Translation: Saoirse, Foresight News

You may have already noticed that after inflating the valuations of private companies to trillions of dollars, venture capital firms are finally ready to cash out. Their only problem is finding enough liquidity for their exit.

Let's be clear: I am not accusing the San Francisco venture capital circles of engaging in illegal activities. What I am criticizing is that their actions are extremely unethical and have destroyed the original social contract of capitalism.

The Original Agreement

The Baby Boomer generation is the last cohort to benefit from a tailwind of their era.

The United States does not have a European-style high-welfare state system, nor was it originally intended to need one. The old social contract was: the stock market is America's welfare system. Traditional defined-benefit pensions were phased out, replaced by individual contribution accounts; the pension system was supplanted by the 401(k) plan; social security serves only as a safety net, and no one expects to retire solely on it.

The implicit rule was: every ordinary worker would become a shareholder, and the dividends of capital appreciation would lift ordinary workers as well. Even if wage growth stagnated and wealth inequality widened, it didn't matter because everyone's retirement account was compounding in the background. Everyone was on the same wealth train, and the final outcome wouldn't be too bad.

This is also why the wealth gap in the US is politically tolerable. You can accept that your boss earns four hundred times your salary, as long as your retirement account appreciates along the same curve as your boss's assets. Passive index funds are the purest embodiment of this agreement. A supermarket cashier, a teacher, a plumber, can all enjoy the market returns generated by professional capital's value discovery for free, securely sharing in the dividends. At that time, the capital market was a public dividend pool for everyone.

But for this agreement to hold, prerequisites were necessary: the public market must be the true place where value is created; the dividends of wealth appreciation must benefit the general public; every new increment of capital growth must be includable in index funds. These conditions once held true for a long time, but now they have all failed.

This is everything they have stolen from you.

When companies remain private until they reach trillion-dollar valuations before going public, the public market no longer creates value; it only cashes out value. Everything that happens in the stock market today is merely wealth distribution, not compounding growth. Every dollar of returns that should have flowed into ordinary retirement funds during a company's growth phase now ends up in the pockets of pre-IPO shareholders. Figma's valuation was halved just weeks after its IPO compared to its private valuation; Klarna's valuation plummeted by 90%. And this was the intended outcome all along, by design.

The industry also noticed that ordinary retail investors were being shut out from these gains, so it offered a narrative: democratize investing, broaden investment channels, bridge the wealth gap, open the private market to retail investors. But the reality is the exact opposite: they are only allowing retail investors to buy the chips that insiders accumulated when the companies were valued at a thousandth of their current price, at the peak of a decade-long private market bull run. Private venture capital products for retail investors are not investment opportunities; they are simply tools for insiders to offload their positions at high prices. Even Naval's own logic confirms this.

(Note: Naval Ravikant is the leading spokesperson for the democratization of private markets in Silicon Valley's venture capital circle. The author directly points out that his advocacy for private investment by ordinary people is a public relations force driving venture capital's high-priced exit and harvesting retail liquidity.)

A Carefully Designed Exit Strategy

Historically, the cryptocurrency circle was the first to fully understand this harvesting routine.

Early-stage crypto project foundations held large amounts of locked native tokens. Retail buying power was already exhausted, token unlock dates were approaching, and no one was there to buy.

So they devised a solution: package these unwanted locked tokens as compliant equity assets that traditional financial institutions could purchase. Tokens that retail investors would never have bought directly were transformed into stocks. Institutions bought compliantly, and retail investors could also enter via brokers to take the other side of the trade. The chips were smoothly distributed, the SEC silently acquiesced, the project successfully cashed out, and the buyers were marked as exit liquidity from the very beginning.

As an aside, Naval was an early participant in the crypto space and is deeply familiar with this game.

After witnessing this strategy succeed, the San Francisco venture capital circle directly scaled this model to the trillion-dollar capital market. Private venture capital products for retail investors were the first channel; Nasdaq's modification of listing rules was the second.

Nasdaq's proposed new rule: for newly listed companies with very few public float shares, the index weight will be directly amplified by 5x, updated during the quarterly index rebalancing. Take SpaceX as an example: upon listing, it is expected to have only 5% of its shares in public float, with a total valuation of $1.75 trillion. Under the new rule, passive index funds would be forced to buy the stock based on a $438 billion valuation, executed 15 days after the listing, completely bypassing market price discovery. The internal share lock-up period would precisely expire at the next index rebalancing date. At that point, the weight is maximized, passive funds buy in huge amounts unconditionally, and insiders can legally cash out. SpaceX is expected to list mid-year, with the year-end coinciding with the index rebalancing—the entire process fits perfectly.

Index funds, once a protective shield for ordinary retail investors against insider capital harvesting, have now become a tool for capital to exit. Your retirement savings are being harvested by this mechanism for nothing.

The logic of the crypto circle and the venture capital circle is completely identical: insiders first accumulate positions at low prices in markets retail investors cannot access; the asset appreciates; the buying power of the native market cannot support selling at high prices; then they create a new packaging vehicle to tap into another pool of funds—namely, pension funds and passive index funds that strictly follow rules and buy without price consideration; insiders successfully exit, and new retail investors take on the high-priced positions. The entire process is completely legal because the packaging is compliant; the regulatory agencies are ineffective because this institutionalized harvesting is not against the rules.

The Ultimate Consequences

Many current chaotic phenomena stem from this: Sam Altman faced public backlash, autonomous vehicles were vandalized, data centers met with public protest. The ordinary people initiating these revolts have no understanding of liquidity exit theory, but they feel it acutely: society is divided into two classes—early entrants and late bag holders. The speed at which this class divide is expanding far exceeds what can be compensated for by personal effort, talent, or opportunity.

The elite tech class has proven with reality that ordinary people's public capital is being continuously harvested to create extraordinary wealth for an already advantaged group.

The K-shaped divergence of wealth will become increasingly extreme. What follows will not be a normal market correction, because a correction presupposes that participants still believe the existing rules are fair.

The current uprisings and conflicts among the people have essentially evolved into a political conflict at the societal level.