XRP短暂胜诉,判决书透露了哪些重要信息?

出品 | Odaily 星球日报

作者 | 秦晓峰

2020 年 12 月,Ripple 遭美国 SEC 起诉。经过三年艰苦的法律斗争后,Ripple 终于迎来了「短暂」的胜利。

今晚,美国联邦法官裁定 Ripple 公司通过交易所以及算法程序出售 XRP 代币并不构成投资合约(不违反证券法),但法院同时也支持了 SEC 提出的动议,即机构销售代币确实违反了联邦证券法。消息一出,XRP 价格从 0.473 USDT 一度暴涨至 0.64 USDT, 1 小时最高涨幅超过 35% 。

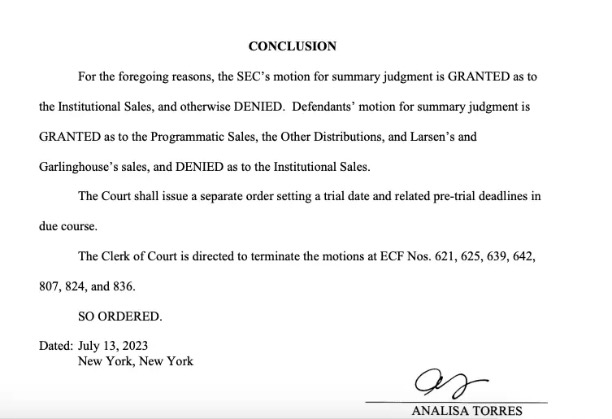

最终结论

在这场判决中,SEC 与 Ripple 都不是真正意义上完全赢家。关于 XRP 究竟是否属于证券,目前并没有清晰的定论。不过,该消息还是被迅速传播,也被视为加密市场反抗 SEC 的一大利好。特别是当前 Coinbase 以及 Binance 等加密巨头遭遇 SEC 起诉,给整个加密市场蒙上了一层阴影,Ripple 的胜利在此时显得尤为振奋人心。加密社区高喊,XRP 的一小步,加密的一大步。

Odaily 星球日报注意到,在法院的判决书中也有一些值得关注的细节。

首先是法院支持 SEC 的动议部分,即 Ripple 的机构销售代币构成了未注册的要约和销售投资合同,违反了《证券法》第 5 条。法院是根据 Howey 测试的三个方面进行判定的:

Howey 测试第一步检查“资金投资”是否属于相关交易的一部分;被告并不否认支付了金钱,因此法院认为这一要素成立。

Howey 测试第二步,即是否存在“共同企业”;法院认定存在一个共同企业,因为记录表明存在一个资产池,并且机构买家的命运与企业的成功以及其他机构买家的成功联系在一起。

Howey 测试第三步,研究 Ripple 机构销售的经济现实是否导致机构买家“对从他人的创业或管理努力中获得利润有合理的预期”。法院认为,处于机构买家地位的合理投资者会购买 XRP,并期望他们能从 Ripple 的努力中获得利润。”

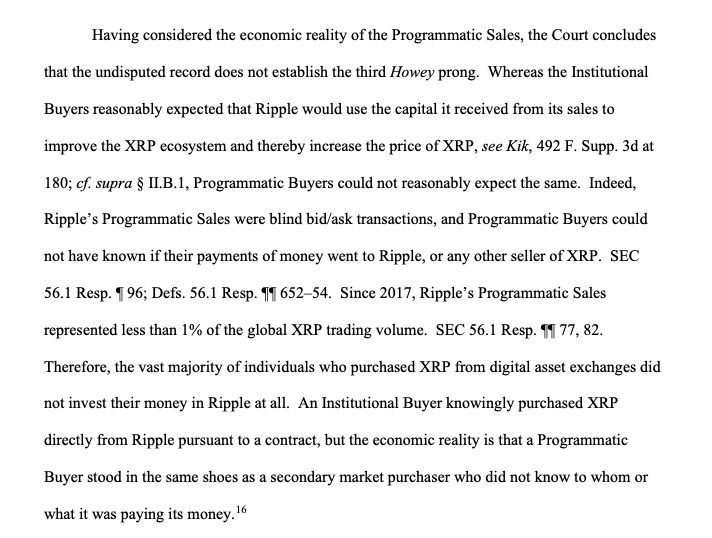

有意思的,法庭之所以裁决 Ripple 通过交易所以及程序销售 XRP 代币不构成投资合约,是因为程序化销售不符合 Howey 测试第三点,即对利润的合理预期。

法庭认为,机构买家合理地预期,Ripple 将利用其从销售中获得的资金来改善瑞波币的生态系统,从而提高 XRP 的价格。但是,程序化买家不可能合理地期望同样的结果。“Ripple 的程序化销售是盲目的买卖交易,程序化买家不知道他们的钱是否流向了 XRP 或任何其他 XRP 的卖家。自 2017 年以来,Ripple 的程序化销售额占全球 XRP 交易量的比例不到 1% 。因此,绝大多数从数字资产交易所购买 XRP 的个人根本没有投资瑞波币。机构买家根据合约直接从 Ripple 购买 XRP,但经济现实是程序性的买家和二手市场(即交易所)的买家不知道自己的钱是给了谁。”

(关于程序销售的内容)

最终,法院作出 Ripple 的程序化销售 XRP 不构成投资合约,不违法证券法。并且,法院还裁决使用 XRP 对其他人的投资、赏金、赠款以及向高管转让等均不构成投资合约,不违法证券法。

美国作为海洋法系集大成者,此番 XRP 裁决也为后续其他加密货币项目案件提供判例依据。特别是通过程序销售代币不违法证券法,也直接证明了交易所开设代币交易并不违反证券法,但是最好不要通过 ICO/IEO 等形式销售代币,因为这可能会被认定为符合机构销售的条件。关于 Ripple 案件后续进展,Odaily 星球日报也将持续关注。