Original title: "The Case for SNX to go back to ATHs"

introduce

Original compilation: 0x9F, 0x214, BlockBeats

introduce

Just like any other OG DeFi project, Synthetix has experienced a plunge in the past few months, with many being liquidated because they did not carefully manage their sUSD debt positions. In fact, as the SNX price collapses, margin calls need to be responded to by increasing SNX collateral or repaying sUSD debt to ensure that the collateral ratio is appropriate.

Synthetix's debt model has always been a double-edged sword: in a bull market, degens use sUSD debt to buy other Tokens or buy more SNX, highly leveraged on their SNX collateral positions.

As the price of SNX Token rises, it brings them additional sUSD fees and more SNX inflation rewards, which drives SNX up. But when the market turns bearish, debt kills all speculators. They gambled away their debts and were unable to repay them, leading to a cascading liquidation of SNX.

first level title

In the end what happened?

You can have any opinion on Synthetix, but it is undeniable that they have the most hardcore project team and one of the most active DAOs in the entire DeFi ecosystem.

Although the sUSD debt model has some shortcomings, it also has great advantages, such as the ability to implement atomic swaps (Atomic Swaps), which allows giant whales to use Synthetix's synthetic assets (sUSD, sETH, sBTC, etc.) benefit from.

Atomic swaps are already being used and, thanks to Curve liquidity pools and DEX aggregators like 1inch, they are giving SNX stakers massive sUSD yields on a weekly basis.

In addition, Synthetix has begun to spin off other projects built on the theory of sUSD's infinite liquidity, and large traders can trade on Synthetix without suffering slippage or spread losses like they do in traditional financial markets.

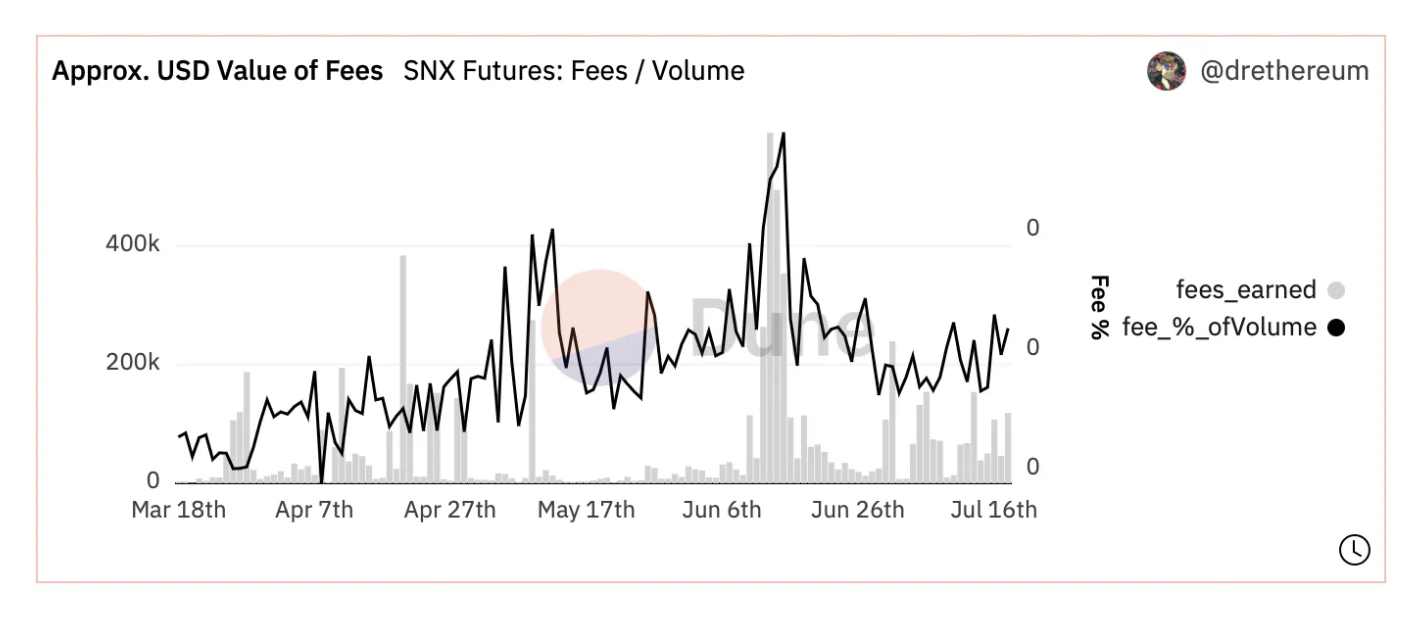

From a fee perspective, the most promising for SNX stakers is Kwenta. It has launched futures trading on Optimism L2, and trading volumes have picked up. Plus, it brings additional benefits to SNX stakers.

So, fundamentally, those two factors are more than enough to justify the recent price surge.

But the problem is,first level title

protocol layer

protocol layer

Synthetix has been in a state of constant transformation over the past few years, as the project team has never rested on its laurels: whether it's responding to crisis situations (leading early), or implementing new features or ideas, such as atomic swaps.

Synthetix started as a DEX for synthetic asset trading, or simply a dApp built on top of Ethereum.

With v3 scheduled to launch in 2023, the project will be considered a protocol layer on top of which other projects will build dApps and use its liquidity. The more it is used and integrated with other DeFi Lego, the more fees it generates. As such, it creates pooled fees for SNX stakers.

From an integration perspective, Synthetix is also the most advanced project on Optimism L2. As Optimism grows, Synthetix grows too. As new projects launch on Optimism, they use Synthetix to enhance their liquidity or activity, creating synergies in various ways, and increasing usage of the Synthetix protocol. Therefore, more costs are incurred.

secondary title

Universal cross-chain bridge

Once Synthetix is deployed on other L1 and L2, it can be used as a general cross-chain bridge or synthetic transmitter (Synth teleporters) to transmit Token and Stablecoin across chains in the most efficient way: unlike the traditional way of relying on liquidity pools to achieve entry and exit Synthetix delivery is faster, safer, and cheaper than cross-chain bridges.

Kain is atSIP-204It is described in this way:

"The vast majority of Token cross-chain bridges rely on a network as the "native" network of each Token. This means that when a token is bridged, the target network will receive the "wrapped" version of the token, while the original token is still stored in the cross-chain bridge contract of the source network. This is not ideal, as cross-chain bridges need to be secured at all times to preserve the value of assets on the target network. Most of these cross-chain bridges rely on multi-signatures for security, putting all assets on the target network at risk. "

Synthetic teleporters are not cross-chain bridges, they are another type of protocol that enables cross-chain transfers by burning and minting assets.

“This ensures that the total supply of each synthetic asset remains the same and does not have to secure two versions of the same asset. In terms of cross-chain messaging, there are generally two approaches: one is to rely on the cross-chain interaction provided by Chainlink. operational agreement; the other uses signed messages generated by transmitters on each network to authorize the transmitter on the other side to mint assets previously destroyed by the source transmitter.”

secondary title

Strong Transaction Protocol

Whether it is spot or leveraged decentralized trading, it has been popular for quite a long time. There is a huge competition between chains and protocols to attract traders.

The most popular exchange by far is likely to be dYdX, which currently runs on its own StarkNet-based L2.

dYdX is the hub of decentralized exchanges, or until recently was. A good product is important, but not everything. Having good token economics is also crucial.

If this is not the case, there will be friction between users and holders. dYdX is a perfect case of "good product + bad token economics". The relative success of dYdX can be attributed to the fact that the protocol provides generous trading incentives for traders at the expense of DYDX Token holders and VCs with a large number of unlocked Tokens.

Contrary to dYdX,Synthetix's products and token economics are very attractive.It rewards SNX stakers with weekly dividends. At present, APY has remained above 100% for several consecutive weeks.

Most importantly, Synthetix is a protocol that not only can host Kwenta, but many other teams are willing to launch derivative products on Synthetix due to no slippage, unlimited liquidity and fully customizable products.

secondary title

two short boards

sUSD Debt

As we all know, in order to participate in SNX staking, you need to stake your SNX and mint sUSD (this is your debt to the Synthetix platform). Once you become a SNX staker, you are in Synthetix's global debt pool.

Effectively, to SNX stakers, they are the counterparty to any trader who takes a position in a synthetic asset (sETH, sBTC, etc.) provided by Synthetix. This means that your debt position will fluctuate, increasing if the trader makes money and decreasing if the trader loses money.

The original idea of Synthetix was that traders tend to lose money on average, so Synthetix would be profitable.

However,

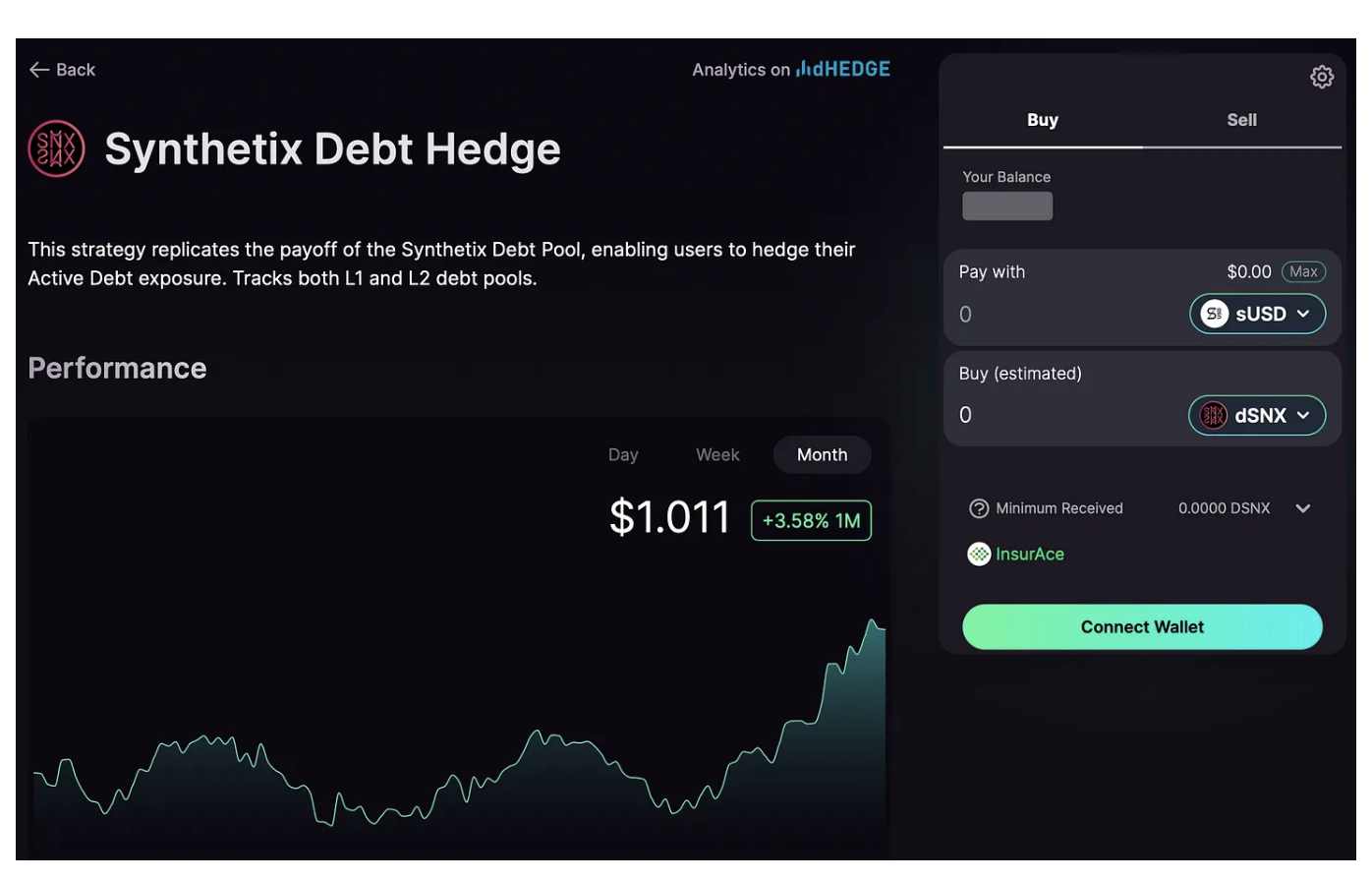

However,It is now possible to fully hedge your debt position on Optimism L2 thanks to dHedge and their spin-off Toros.Toros allow you to buy dSNX with your minted sUSD, so you are not exposed to market volatility and your debt doesn't build up over time.

access.hereaccess.

In our opinion, sUSD debt management has been a major drawback of using Synthetix since many users do not fully understand the concept or meaning of sUSD debt.

secondary title

sUSD Liquidity on Optimism

Do Kwon has a famous saying "your size is not size", and it is even more so on Optimism.

sUSD on Optimism is illiquid, so no whale can execute trades on Kwenta.

However, this is about to change as Synthetix has launched a sUSD cross-chain bridge between Ethereum and Optimism, so now you can buy large amounts of sUSD on Ethereum and bridge it to Optimism to start trading. The only downside is that once you want to bridge back to Ethereum from Optimism, you have to wait 7 days. The synthetic teleporter will not be available for a while.

risktutorial。

risk

The main risks are well known:

Supervision:If Mr. Gensler (Chairman of the US SEC) is responsible for supervising DeFi all over the world, and focuses on Synthetix.

Hacks/Vulnerabilities:in conclusion

in conclusion

Synthetix has put their all into advancing the protocol over the years and it's still amazing to see their dedication. Additionally, the protocol has strong fundamentals, good token economics (will change with the introduction of veSNX) and an ambitious roadmap.

The roadmap is ambitious,The planned launch of Synthetix v3 in 2023 will inevitably result in more fees for SNX stakers.Given Synthetix's progress on all fronts, and their strategy of incurring fees to SNX stakers, it's hard to be bearish on Synthetix. Because this is clearly a winning strategy - more fees mean more dividends for SNX stakers.

We cannot predict the future, so there is no way of knowing whether the current bear market is over or will continue for a year or more. But we believe Synthetix-related transaction volumes across all dApps will skyrocket later this year and into 2023 (even more once v3 goes live).

Original link