摩根士丹利解读:AI网络市场冲向700亿美元,先吃红利的为何还是铜缆?

- 핵심 의견: 모건스탠리는 2030년 AI 스케일링 네트워크 시장 기회를 약 700억 달러로 상향 조정했지만, 단기적으로(2026-2027년)는 구리 케이블이 여전히 지배적이며, CPO(공동 패키징 광학) 기술은 2029-2030년이 되어야 20-30%의 의미 있는 보급률을 달성할 수 있을 것으로 지적합니다.

- 핵심 요소:

- 시장 기회 상향 조정: 모건스탠리는 2030년 AI 스케일링 네트워크 시장 기회를 약 700억 달러로 예상하며, 이는 작년 추정치보다 4배 이상 확대된 것입니다. 주요 동인은 멀티 랙 GPU 클러스터로 인한 연결 수요입니다.

- 기술 로드맵 타임라인: 2026-2027년 CPO 보급률은 거의 0에 가깝고, 2028년부터 소규모 도입이 시작되며, 2029-2030년에야 20-30%의 보급률을 달성할 것으로 예상됩니다. 구리 케이블은 단거리 연결(7-9미터 이내)에서 여전히 비용 및 전력 소비 측면에서 이점을 가지고 있습니다.

- 수혜 순서 명확: 단기적으로는 칩 및 모듈 회사(Astera Labs, 브로드컴, Semtech)가 구리 케이블의 성능을 연장하기 때문에 우선적으로 수혜를 입습니다. 중장기적으로 광학 부품 업체(코닝, Lumentum, Coherent)의 변동성은 CPO 도입 속도에 따라 달라집니다.

- 엔비디아 로드맵이 핵심 변수: Vera Rubin Ultra NVL576 및 Feynman Kyber NVL1152와 같은 플랫폼은 GPU당 광학 엔진 수요를 약 2개에서 17-70개로 증가시킬 것이지만, 실제 증가분은 플랫폼의 양산 일정에 따라 달라집니다.

- 테스트 장비 업체의 수혜 확실성 높음: 키사이트 테크놀로지는 AI 네트워크 아키텍처의 다양화(NVLink, UALink 등)와 고속 테스트 수요(800G/1.6T/3.2T)로 인해 모건스탠리로부터 등급이 상향 조정되었으며, 단일 기술 경로에 베팅할 필요가 없습니다.

TL;DR

- Morgan Stanley expects the AI-scale networking market opportunity to be approximately $70 billion by 2030, expanding more than four times compared to last year's estimate.

- From 2026 to 2027, scale networks will still primarily use copper cables; CPO is unlikely to reach a meaningful 20%-30% penetration until 2029-2030.

- Keysight Technologies, Astera Labs, Broadcom, and Semtech are positioned to benefit earlier, while the upside for Corning, Lumentum, and Coherent comes later.

In its latest report, Morgan Stanley estimates the 2030 AI-scale networking market opportunity at roughly $70 billion, bringing the lifecycle of copper cables within AI clusters back into focus.

This isn't a story of an "immediate CPO explosion." AI clusters are evolving from single racks to multiple racks, requiring denser, higher-speed connections between GPUs, thereby enlarging the total backend network TAM. However, until power, distance, and bandwidth density truly hit their limits, short-reach connections still have strong inertia favoring copper cables.

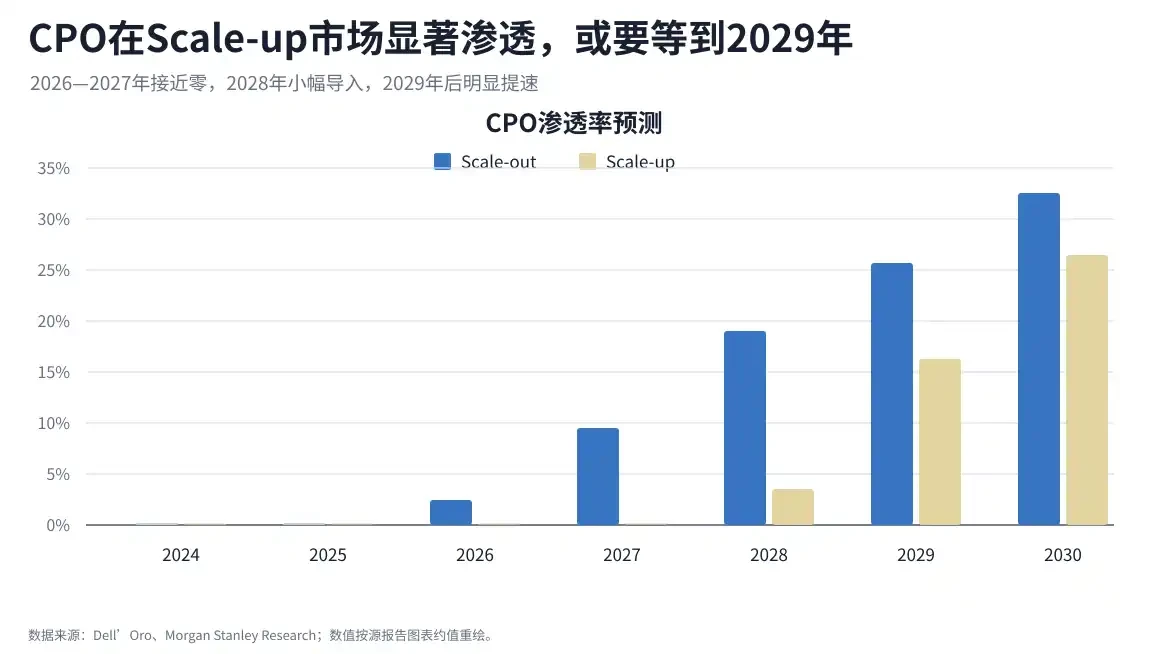

The timeline presented in this report is relatively conservative: CPO penetration in scale networks is near zero from 2026 to 2027; small-scale introduction begins in 2028; and a meaningful penetration level of 20%-30% is only expected by 2029-2030. While the market opportunity has been significantly revised upward, optical solutions won't capture the lion's share of scale networks until larger GPU domains and more mature supply chains are simultaneously in place.

The $70 Billion Opportunity Comes from Multi-Rack, Not Primarily Optical Modules

The core driver for this upward revision is the significant increase in connectivity demands within servers and between racks as AI clusters expand.

In traditional single-rack scenarios, the distance between GPUs is short, and copper cables maintain advantages in cost, latency, and power consumption. For short-reach connections, especially within 7-9 meters, copper remains the most straightforward solution. Over the past few years, advancements like stronger SerDes, retimers, and PAM4/PAM6 technologies have continuously extended the lifecycle of copper, repeatedly postponing the timing for optical substitution.

The change occurs as clusters grow larger. Training and inference clusters expand from one rack to multiple racks, requiring communication across racks. Signal speeds also progress from 100G to 200G, 400G. As distances lengthen and speeds increase, challenges related to electrical loss, insertion loss, and noise management escalate, pushing copper closer to its performance limits.

Backend network revenue forecast for 2024-2030; scale network revenue rises rapidly, with a market opportunity of approximately $70 billion by 2030.

For investors, this determines the order of beneficiaries. The initial beneficiaries are likely not CPO suppliers, but chip and module companies that enable copper to run faster and over longer distances. The upside for optical engine, passive photonics, laser, and test equipment companies becomes more apparent only after multi-rack clusters become more prevalent.

2026-2027 Remains a Copper Window; CPO Won't Explode Until After 2029

CPO's appeal lies in bringing optical components closer to the switch ASIC or compute chip, reducing the travel distance for high-speed electrical signals on the PCB, thereby improving power efficiency and bandwidth density. The challenge is that this isn't just about swapping a cable; it involves fundamental changes to packaging, manufacturing, testing, maintenance, and supply chain responsibility allocation.

This is precisely why CPO won't see widespread adoption in 2026. CPO penetration in scale networks is near zero from 2026-2027, with small-scale introductions in 2028. Truly meaningful adoption is anticipated between 2029-2030. By then, if the expansion of multi-rack GPU domains proceeds as planned, CPO penetration in scale networks could potentially reach 20%-30%.

CPO penetration forecast split by scale networking/enterprise; scale CPO only rises to 20%-30% by 2029-2030.

This leaves a window of at least two years for the copper ecosystem. Astera Labs' Scorpio X-Series has already entered initial volume shipments. Broadcom has connectivity opportunities within the AMD MI400/Helios and custom ASIC ecosystems. Semtech participates in the transition phase through its CopperEdge low-power copper cables and linear optical solutions.

More importantly, copper and optics are not a simple replacement. Hyperscale cloud providers will likely use a mix of DAC, ACC, AEC, AOC, NPO, and CPO based on distance, power, cost, serviceability, and reliability. Short-reach, intra-rack, and near-rack connections may retain significant copper usage, while CPO takes on more roles in high-density, longer-reach, and power-constrained environments.

Nvidia's Roadmap Boosts Optical Demand, But the Pace Depends on Platform Rollout

CPO becomes truly important in direct correlation with Nvidia's next-generation AI platform roadmap.

According to Nvidia's official technical blog, the Vera Rubin Ultra NVL576 will combine eight 72-GPU racks into a single 576-GPU NVLink domain, using copper cables and direct optical connections. The Feynman-era Kyber NVL1152 targets an even larger interconnect scale, also utilizing similar direct optical schemes.

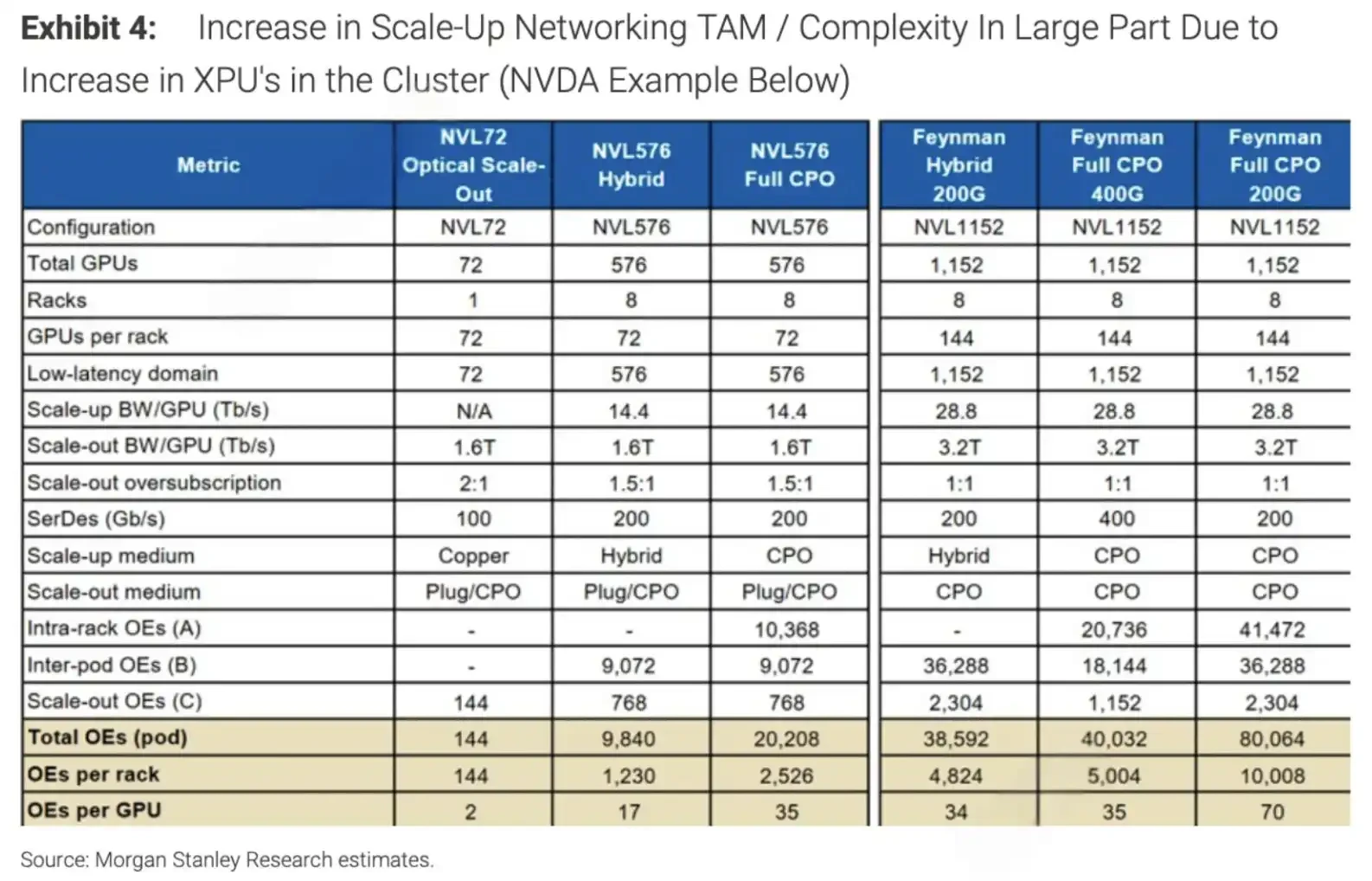

As the GPU domain expands, the demand for optical engines won't just increase linearly. In this report's estimation, the number of optical engines per GPU could rise from approximately 2 today to a range of 35-70. In other words, once the architecture shift occurs, the optical content per GPU will increase significantly.

Comparison of XPU cluster scale and OE requirements; as the GPU domain expands from 72 to 576/1152, the number of OEs per GPU increases from 2 to 17-70.

This is why companies like Corning (GLW), Lumentum (LITE), and Coherent (COHR) are included in this thematic chain. Corning benefits from passive photonics and glass-related content, while Lumentum and Coherent are more associated with lasers, optical engines, and optical components. After incorporating scale CPO adoption rates into its model, Morgan Stanley finds that the earnings upside for related companies depends more on the pace of adoption.

However, this remains a potential upside "if adoption happens," not already realized revenue. Nvidia's own roadmap faces market debate. Some industry analysts suggest potential delays for certain configurations of Kyber or Rubin Ultra, while Nvidia maintains its roadmap remains unchanged. For the optical ecosystem, the key factor isn't the name of a specific product generation, but whether large GPU domains enter volume production as planned, and whether the non-Nvidia XPU ecosystem adopts similar connectivity paths.

Keysight is More Like a 'Pick-and-Shovel' Player; Test Equipment Doesn't Bet on a Single Route

Within this thematic chain, the logic for Keysight Technologies (KEYS) differs from optical module companies. It doesn't need to bet on whether copper or CPO ultimately wins because the more diverse the AI networking architectures become, the higher the demand for testing and validation.

The current AI backend network lacks a unified standard. Nvidia has NVLink and its subsequent expansion roadmap, while the non-Nvidia camp includes UALink, SUE, PCIe, and custom interconnect solutions from various cloud providers. Each architecture requires signal integrity, bit error rate, interoperability, power, and reliability testing.

According to a report from Investing.com, Morgan Stanley has upgraded Keysight from Equalweight to Overweight, raising the target price from $350 to $400. Reasons cited include AI investment, diversification of network architectures, and increased testing demand for 800G, 1.6T, and 3.2T technologies. Keysight's AI-related revenue accounts for approximately the mid-teens percentage of total revenue.

In contrast, the upside for optical component companies is more concentrated on CPO adoption rates and specific platform timelines. If Nvidia's roadmap progresses smoothly, Corning, Lumentum, and Coherent will benefit more directly. If copper's lifecycle continues to extend through 2026-2027, the near-term certainty is higher for companies like Astera Labs, Broadcom, and Semtech.

CPO Will Eventually Take Center Stage, But Cloud Providers Aren't Ready for a Full Leap

The counter-intuitive aspect of this report is that it simultaneously acknowledges CPO's long-term centrality while emphasizing the short-term difficulty of underestimating copper.

CPO faces significant hurdles. Hyperscale cloud providers fear vendor lock-in. Deeply integrating optical components into switch or compute packages complicates future replacement, repair, and multi-vendor sourcing. Manufacturing yield, thermal management, maintainability, and quality risks also influence the adoption timeline. If the cost premium isn't offset by power savings and bandwidth density improvements, adoption will be further delayed.

There are also architectural divergences. While Nvidia's roadmap may drive a higher proportion of optical connectivity, custom architectures like Google's TPU use different topologies that could reduce reliance on traditional CPO solutions. Although the non-Nvidia XPU ecosystem creates opportunities for companies like Broadcom and Astera Labs, the lack of standardization means the supply chain cannot rapidly scale around a single solution.

Therefore, the upward revision to the $700 billion market opportunity reflects a larger total TAM for AI backend networks, not a definitive victory for a single technology path. From 2026-2027, copper will still dominate intra-rack and short-reach scenarios. From 2028 onwards, optics begin to move into more central roles. By 2029-2030, CPO might achieve truly meaningful penetration in scale networks. The area most prone to market misinterpretation is equating "CPO will eventually arrive" with "CPO is about to explode immediately."