Institutional outflows and spot selling pressure persist, is $54,000 the potential bottom for Bitcoin?

- Core View: Bitcoin has fallen below $60,000, with the market in a deeply loss-dominated environment. On-chain indicators show prices are significantly below investors' average cost basis. ETFs continue to see outflows, and the options market is defensively positioned. Although early signs of value recognition and selective accumulation are emerging, broad demand has yet to recover. The market is in a tug-of-war between distribution and value-driven demand.

- Key Factors:

- Bitcoin's current trading price is at a 19% discount to the Real Market Price ($77,000), and the short-term holder cost basis has dropped to $71,400.

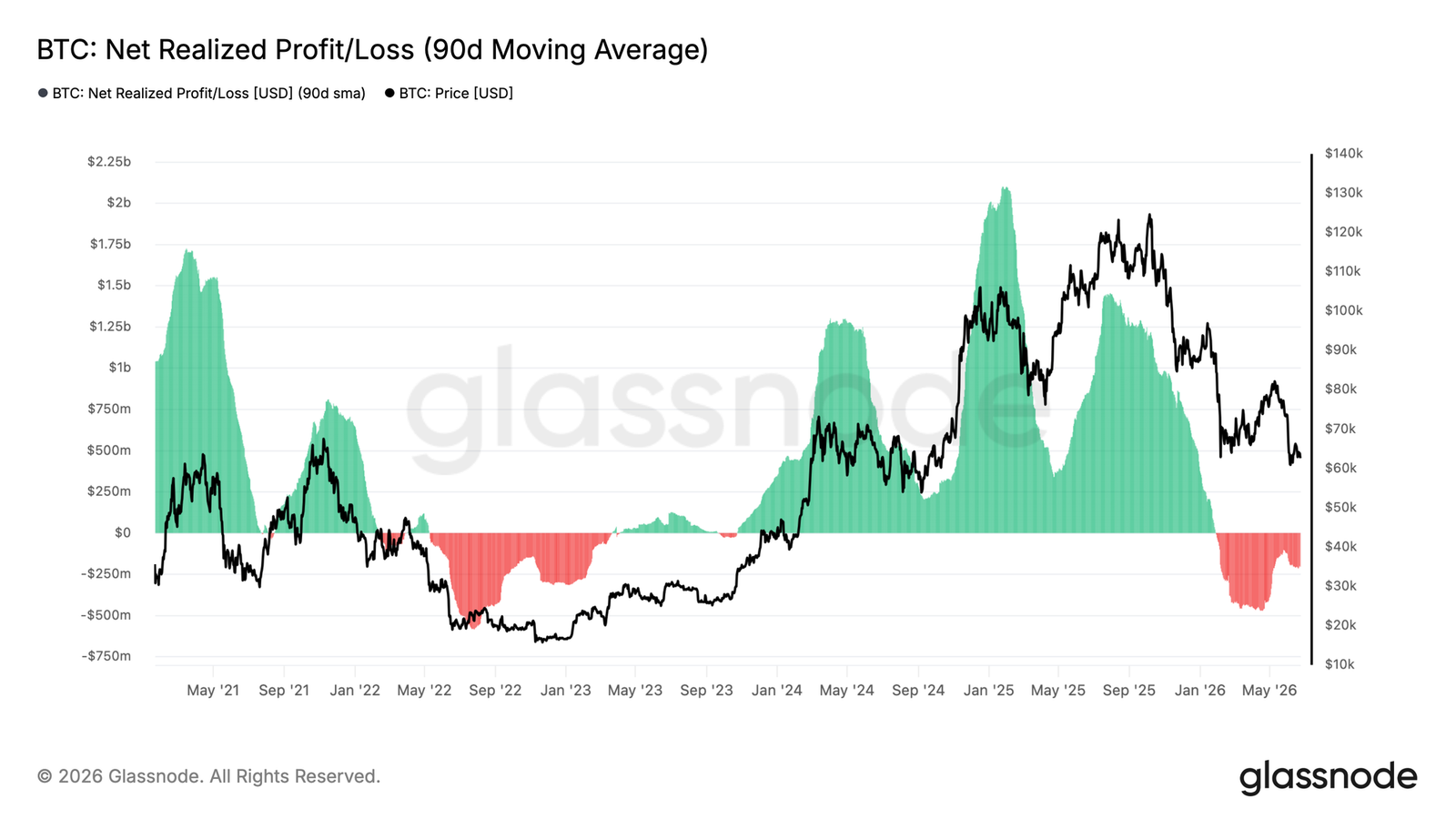

- The 90-day moving average of Net Realized Profit/Loss stands at -$205 million per day, confirming the market is deeply embedded in a loss-dominated environment, with gravity shifting towards the Realized Price of $53,400.

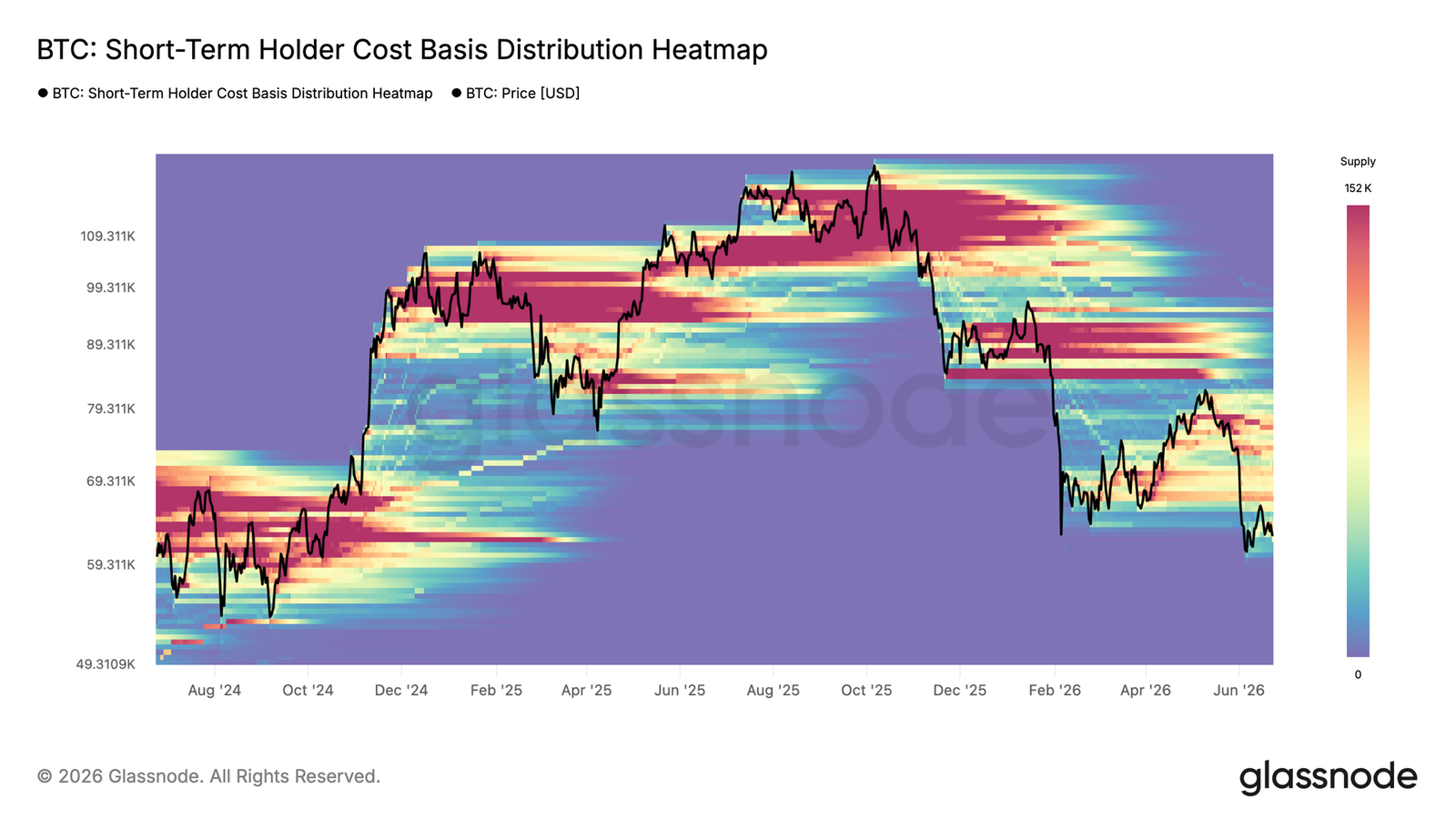

- A dense supply cluster for short-term holders in the $66,800-$70,700 range forms immediate overhead resistance, limiting the upside potential in the near term.

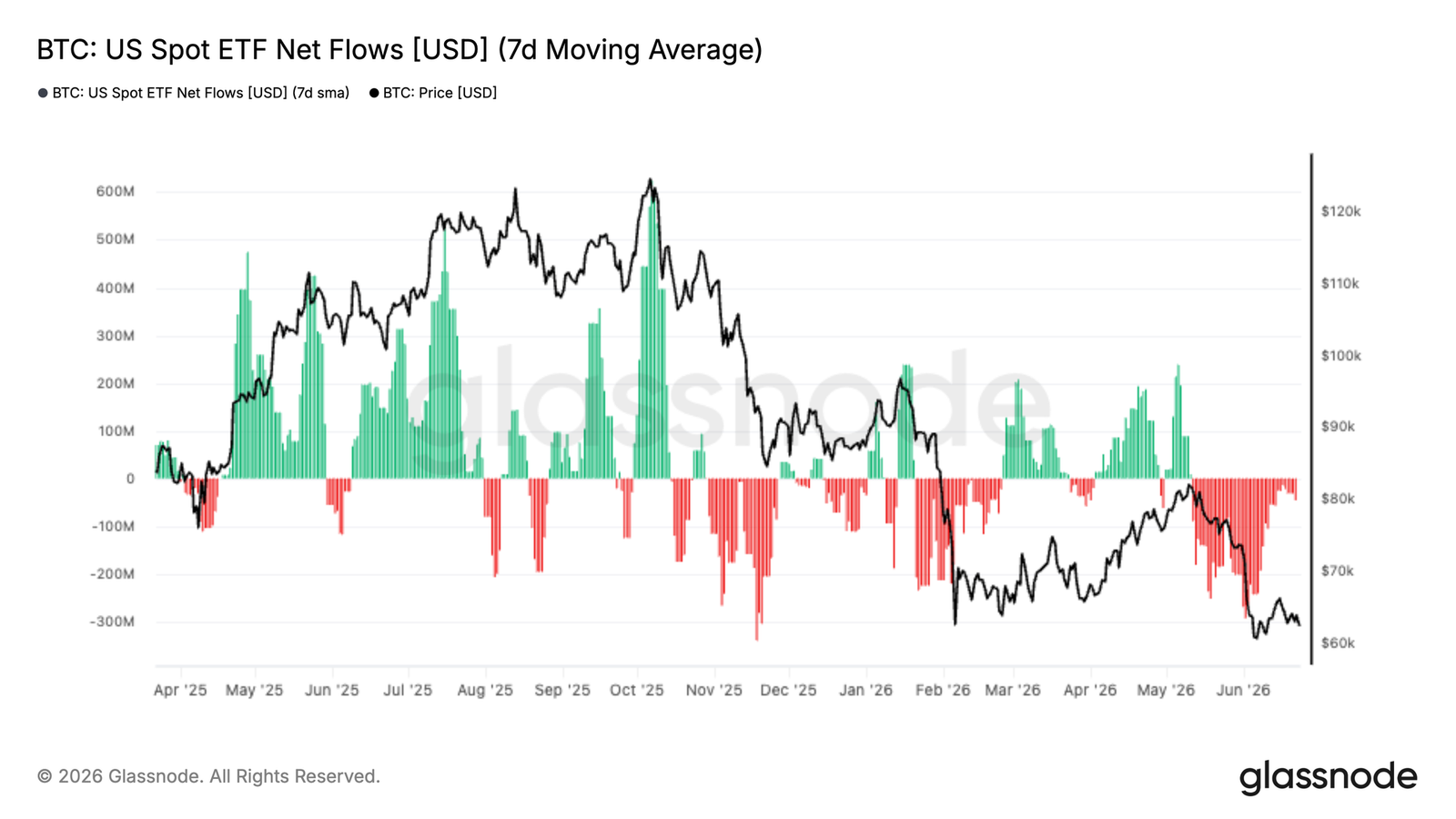

- U.S. spot ETFs continue to see net outflows, with the 7-day average net outflow reaching nearly -$300 million per day. GBTC accounts for the largest share of recent redemptions.

- Coinbase spot CVD shows a return of U.S. buyers, while Binance traders remain in a defensive posture, resulting in a divergence in market structure.

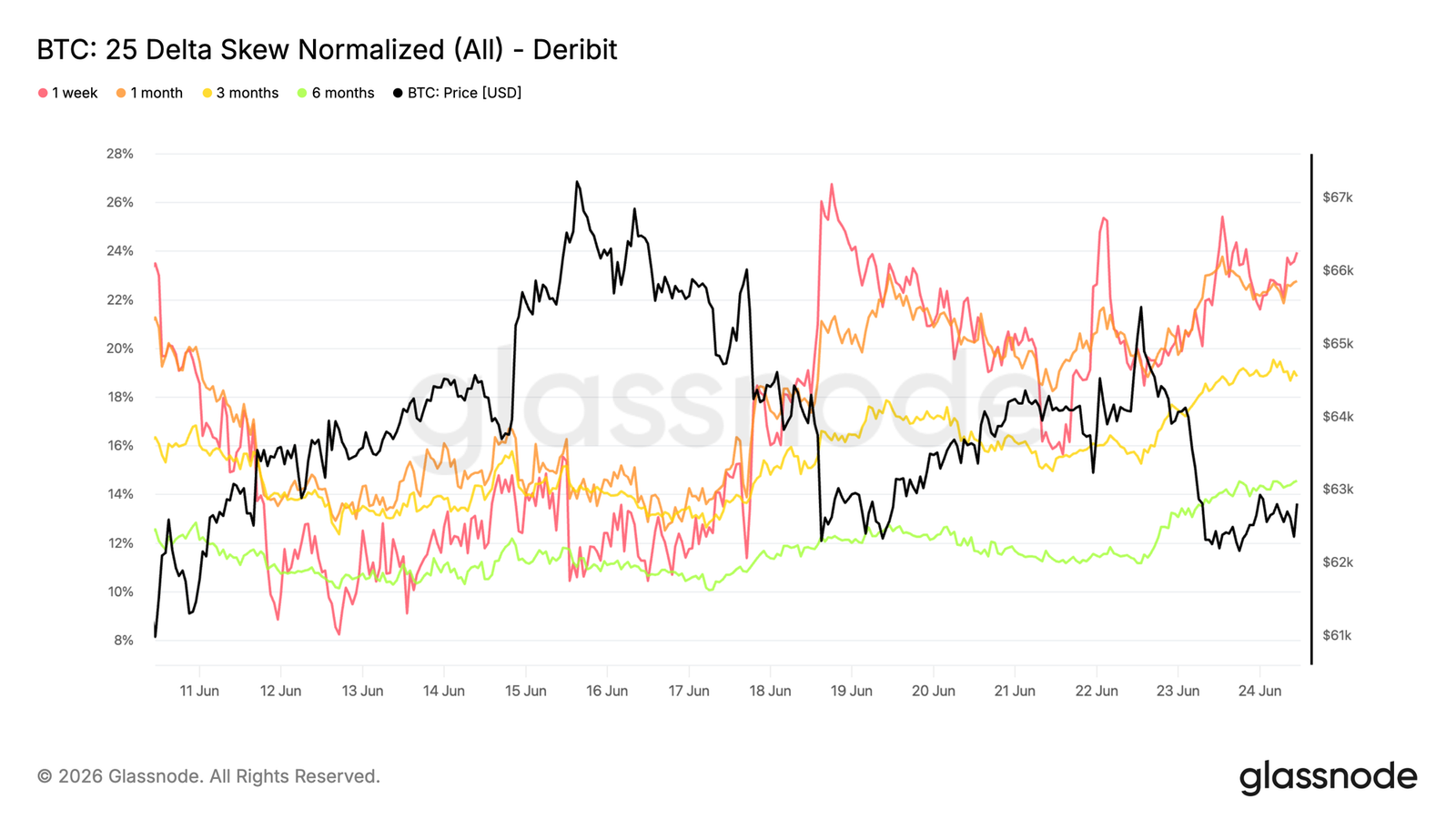

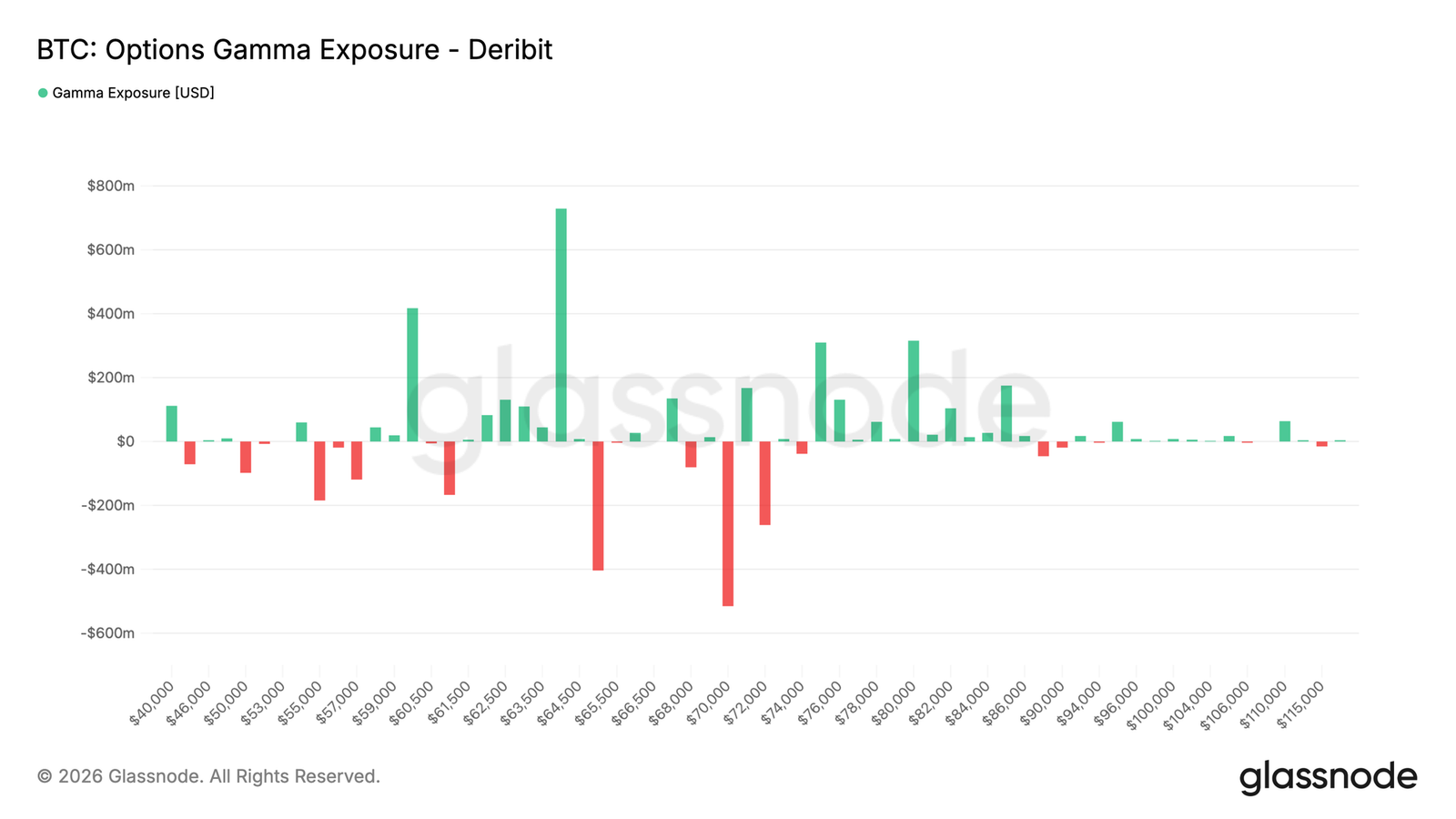

- In the options market, market makers' gamma positioning is concentrated in the 60K-64K range, which may suppress volatility within this range. The rise in skew indicates a rebuilding of downside protection demand.

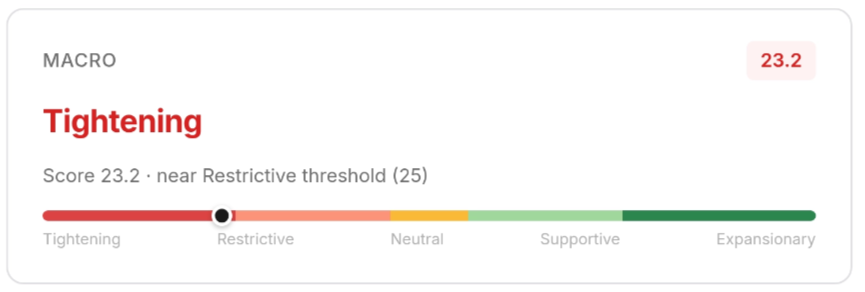

- The U.S. Dollar Index (DXY) has returned above the 200-day moving average, presenting an unfavorable macro signal for Bitcoin. The stock market recovery (S&P 500 up 14%) has not driven BTC.

Original Author: Glassnode

Original Translation: AididiaoJP, Foresight News

Bitcoin has fallen below $60,000, with realized losses, ETF outflows, and defensive options positions continuing to weigh on market sentiment. Although signs of value recognition and selective accumulation are increasing, broad demand has yet to emerge.

Summary

- Bitcoin is currently trading at $62,300, a 19% discount to the True Market Mean Price of $77,000. The Short-Term Holder cost basis has dropped to $71,400, indicating new buyers are accumulating below the cycle average price for the first time—a constructive early step towards bottom formation. (As of press time, Bitcoin has fallen to $60,800)

- The 90-day moving average of Net Realized Profit/Loss stands at -$205 million per day, confirming the market is deeply embedded in a loss-dominated environment, with gravity shifting towards the Realized Price of $53,400 rather than the True Market Mean Price.

- A dense cluster of Short-Term Holder supply sits in the $66,800-$70,700 range, forming the most immediate overhead resistance. Until this area is reclaimed and the path to the Short-Term Holder cost basis is opened, short-term upside remains limited.

- Continued ETF outflows indicate persistently weak institutional demand, with GBTC accounting for the largest share of recent redemptions.

- Coinbase buyers are returning: U.S. investors show buying activity, while Binance traders remain defensive.

- Spot market dominates selling pressure: Selling pressure originates from the spot market, with derivatives primarily following rather than driving the move.

- Implied volatility has stabilized near recent lows, while realized volatility remains elevated, keeping the volatility risk premium negative.

- Demand for downside protection is rebuilding across all tenors, with skew rising sharply, although overall volatility pricing remains relatively restrained.

- Recent flow has shifted towards selling premium, while market maker positioning remains dominated by long gamma in the 60K-64K range, helping to contain volatility near the current spot price.

Macro Insights

The U.S. Dollar Index has reclaimed its 200-day moving average. On June 23, DXY was at 101.37, a significant recovery from 99.24 thirty days prior, and above its 200-DMA of 98.72 for the first time since the April "Liberation Day" shock. The bullish sequence did not materialize.

The 10-year U.S. Treasury yield remained at 4.50%, showing no signs of decline. The VIX rose from 16.2 mid-week to close at 19.49 on Friday. While not panic levels, the directional change is noteworthy. Equities have digested the spring correction, with the S&P 500 at 7,365 points, up 14% from the April low and firmly above its own 200-DMA of 7,007.

Bitcoin has not participated in this recovery. BTC is currently at $62,651, 18% below its 200-DMA of $76,466. The macro recovery remains an equity story, supported by U.S. corporate earnings resilience. For Bitcoin, the renewed strength of the DXY is the dominant signal, and it is not bullish for BTC.

On-Chain Insights

Deep Discount Territory

Bitcoin's current price of $62,300 is well below the True Market Mean Price of $77,000. The True Market Mean Price is the average cost basis of active non-miner investors and a key threshold for distinguishing bull and bear markets. The current 19% discount indicates price is still deeply embedded in a structural bear market range.

Notably, the Short-Term Holder cost basis has dropped to $71,400, reflecting significant accumulation by new buyers below the True Market Mean Price. From a cyclical perspective, this is a constructive development, marking a key step in bottom formation—new capital is being deployed at prices increasingly decoupled from the overheated levels of the recent cycle.

Supply bought during this bear market phase has relatively smaller losses compared to the broader cycle's hanging supply and is expected to show greater resilience to further drawdowns. If a macro-driven decline occurs in the coming weeks, the Realized Price of $53,400 could serve as a reasonable lower bound for the short-to-medium-term bear market range.

Gravity Pulling Towards the Lower Band

Having established the $53,400-$77,000 bear market range, the next question is which end price is more likely to gravitate towards. The Net Realized Profit/Loss metric measures the net difference between profit and loss crystallized in the market (denominated in USD), effectively capturing whether the dominant spending behavior is profit-taking or capitulation.

The 90-day moving average of this metric is currently -$205 million per day, confirming that loss realization has become the dominant force in the broader trend, suggesting market gravity remains tilted towards the lower end of the current range (near the Realized Price).

As this is a slow-moving average, the reading reflects a deeply embedded loss-dominant environment rather than a single stress event. A recovery in this metric towards neutral levels (near zero) would be a strong signal that seller exhaustion is forming, and transitional conditions for a pre-bull market are beginning to emerge.

Overhead Supply Limits Short-Term Moves

Beyond the broader negative capital flow environment, the local concentration of Short-Term Holder supply above the current spot price further weighs on price. The most significant cluster is in the $66,800-$70,700 range, representing recently accumulated coins that are now at a loss and likely to generate selling pressure on any rebound attempt.

This zone effectively defines the most likely ceiling for short-term consolidation or relief rallies, as holders within the range tend to behave like they are exiting near break-even when price approaches their purchase cost. A sustained recovery above $66,800 would significantly alleviate overhead pressure and increase the probability of an extension towards the Short-Term Holder cost basis of $71,400. Until then, this localized hanging supply remains an active anchor suppressing upward momentum.

Off-Chain Insights

Continued ETF Outflows

Institutional demand continued to face pressure this week, with the 7-day average net outflow from U.S. spot ETFs approaching -$300 million per day. This is one of the most sustained periods of capital withdrawal since the ETFs were launched. The scale and duration of outflows indicate that traditional investors remain defensive, even with Bitcoin trading near the lower end of its recent range (~$60,000-$65,000).

Notably, past corrections often attracted ETF buying, providing a significant source of demand during weak periods. This time, the sustained redemptions suggest many investors are choosing to reduce exposure rather than accumulate during the dip.

Despite the overall negative ETF flow, the distribution of redemptions is uneven. Grayscale's GBTC continues to account for the largest share of redemptions, with outflows exceeding 16,000 BTC over the past 90 days. This suggests the weakness is primarily driven by legacy holder liquidation and portfolio rebalancing, rather than a uniform retreat across the entire ETF sector.

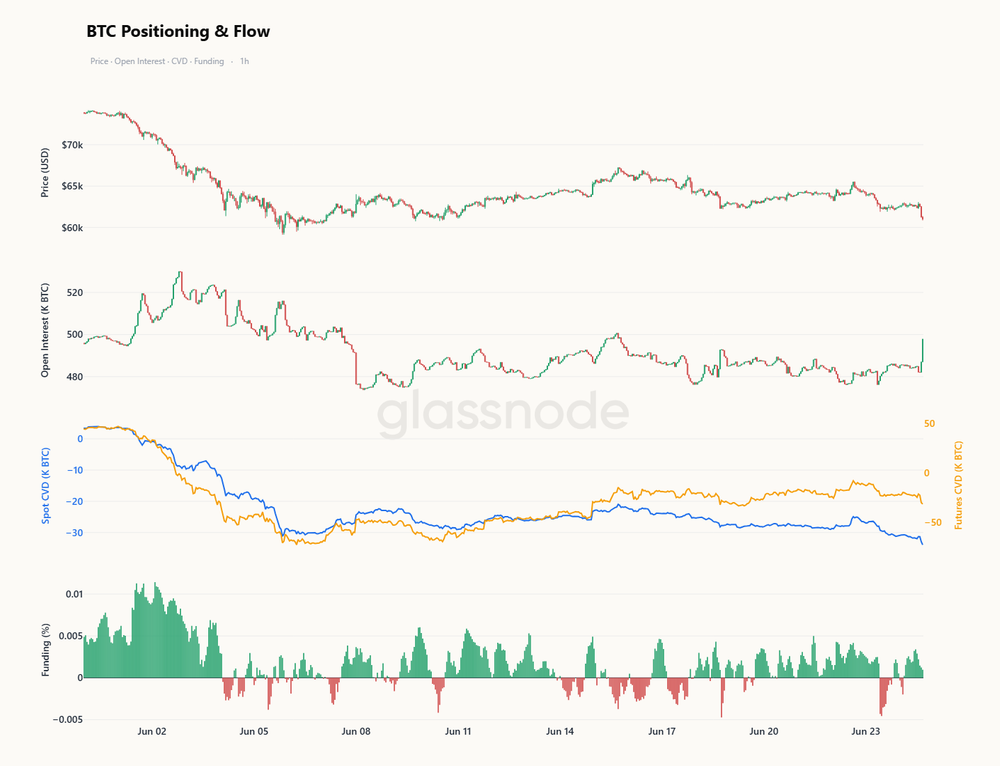

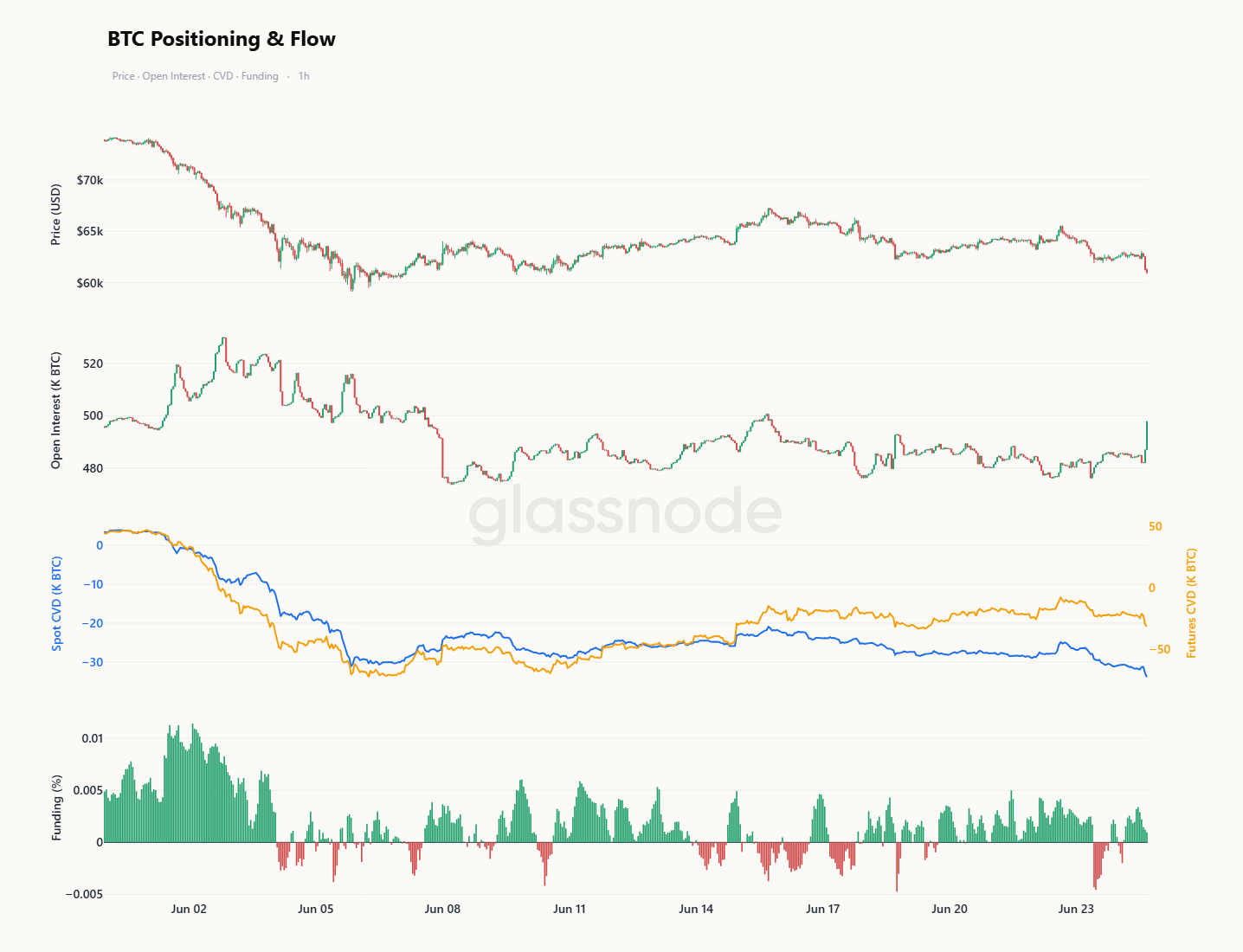

Spot Buyers Begin to Return

Spot market positioning is beginning to improve after an extended period of aggressive selling pressure. While the overall spot CVD bias remains negative, the recent rebound shows that net selling intensity is easing, helping Bitcoin stabilize at the lower end of its trading range.

The most significant development is the divergence between exchanges. Coinbase's spot CVD bias has recovered significantly and turned positive, suggesting buying activity on the platform typically associated with U.S. institutional participants is returning. Binance, however, remains in negative territory, implying overseas traders continue to hold a defensive posture.

This behavioral divergence points to an increasingly uneven market structure. Institutional investors appear to be absorbing supply during the weakness, while speculative participants remain cautious. Although the broader spot market has not yet returned to sustained accumulation, the improvement in Coinbase demand indicates that some investors already view current prices as attractive entry levels.

Futures Follow Spot Lower

On shorter timeframes, the retest of the low $60,000 area was a spot-led move. Over the past ten days, spot CVD declined much faster than futures CVD. This divergence suggests the aggressive selling pressure originated from spot venues, not leverage-driven liquidations. Open interest remained subdued for most of this decline, and funding rates stubbornly stayed positive even as the price fell, indicating perpetual longs were reluctant to capitulate, and the pressure was not stemming from derivatives books.

This situation has begun to change. As Bitcoin retested its lows, open interest surged significantly, and futures CVD has now turned negative in tandem with spot CVD, indicating leverage participants are finally joining the move rather than fighting it. Simultaneously, funding rates have declined from their highs, relieving the long bias that was increasingly out of sync with price action.

Spot carried the heavy lifting during the decline; derivatives are now following, not leading. If open interest continues to increase alongside falling futures CVD and softening funding rates, it will confirm that leverage is capitulating to the lows already sold off in the spot market—a broad-based participation that often marks a more violent, and often more complete, washout phase.

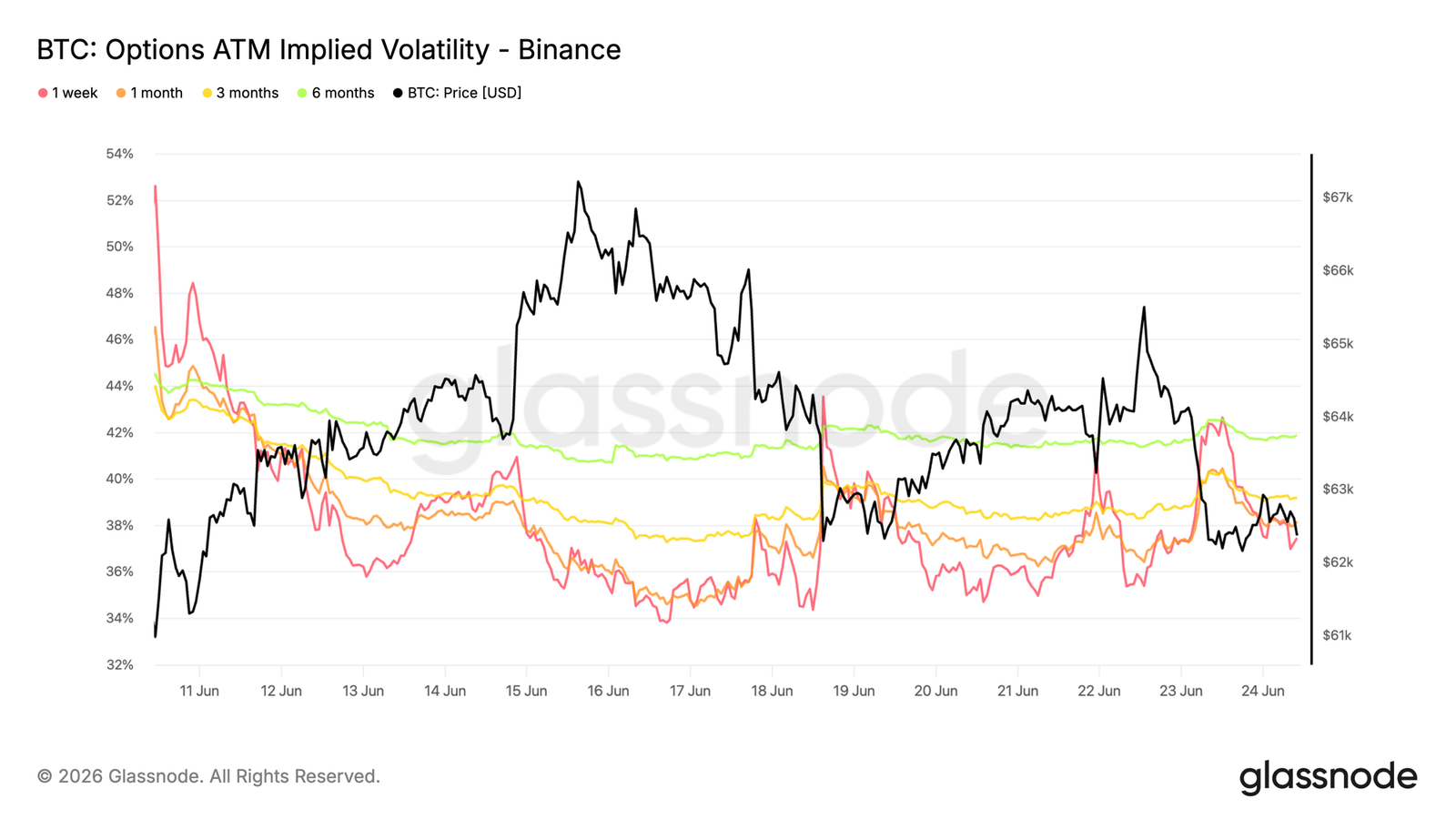

Implied Volatility Stabilizes After Recent Repricing

The options market has entered a calmer range following the sharp repricing triggered by Bitcoin's drop to the June lows.

The front end of the curve remains the most sensitive. One-week ATM implied volatility briefly exceeded 42% during the latest sell-off before retreating to around 37%. The one-month tenor fell from about 40% to 38%, while longer tenors remained relatively stable, with three-month and six-month implied volatility near 39% and 42%, respectively.

This stabilization occurs despite Bitcoin continuing to trade near the key $60K-$63K support zone. The lack of sustained volatility buying suggests traders are no longer aggressively repricing risk, and much of the premium for protection seen during the recent stress period has been removed.

Implied volatility has returned to a stable range, and the options market shows a lower sense of urgency in pricing additional short-term uncertainty.

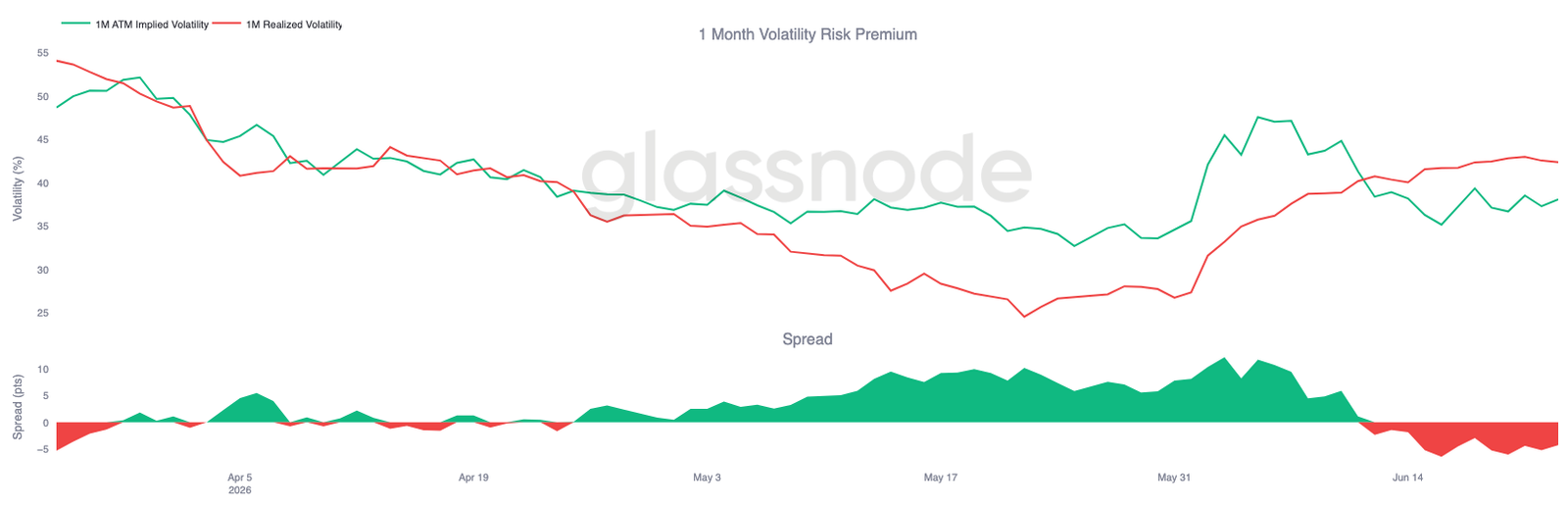

Volatility Risk Premium Remains Negative

With implied volatility stabilizing, the relationship between implied and realized volatility remains inverted, keeping the volatility risk premium negative.

One-month implied volatility is currently around 38%, while realized volatility continues to climb to approximately 42%. Consequently, the volatility risk premium remains negative by about 4 volatility points, extending the inversion that began with the recent market sell-off.

The chart shows that even after implied volatility normalized from its early June peak, realized volatility has remained elevated. In other words, the market is experiencing more actual volatility than options are currently pricing. Although the gap has narrowed slightly from its recent extreme levels, implied volatility has not yet rebuilt enough momentum to push the spread back into positive territory.

Since realized volatility remains higher than implied volatility, the options market continues to price a calmer environment than recent price action suggests.

25-Delta Skew Rebuilds Across Tenors

Following the negative volatility risk premium, the skew indicator reveals how demand for downside protection has evolved as Bitcoin trades near major support.

Skew is calculated as put volatility minus call volatility; a positive value indicates puts trade at a premium to equivalent calls. Over the past week, this premium rose across the entire curve. One-week skew increased from around 12% to 24%, and the one-month tenor rose from approximately 14% to 23%. Three-month and six-month tenors also moved higher, reaching about 19% and 14%, respectively.

The chart shows that despite relatively stable implied volatility, downside protection has undergone a broad repricing. Traders appear less inclined to pay more for overall volatility, but are increasingly willing to pay a premium for downside hedges.

The rebuilding of protection demand across all tenors indicates that while volatility levels are stable, traders have a renewed preference for downside hedging.

Gamma Exposure Concentrated Near Current Spot Price

Beyond pricing and sentiment, gamma exposure helps identify strike levels where market maker hedging may have the greatest impact on market dynamics.

Recent flow shows traders becoming more comfortable selling premium. Over the past seven days, put selling accounted for the largest share of traded premium, at 31.2%. This trend intensified over the last 24 hours, with put selling representing 47.2% of the volume.

This shift is reflected in the gamma profile. The two largest positive gamma clusters are at 60K and 64K, with Bitcoin currently trading between them, around 62.8K. Within a positive gamma zone, market maker hedging tends to suppress volatility, helping to contain spot within the range. In contrast, the nearest negative gamma exposure is at 65K, and its size is significantly smaller than the positive gamma cluster at 64K.

Market maker positioning remains dominated by long gamma near the current level, creating conditions that may help contain volatility within the 60K-64K range.

Conclusion

Bitcoin continues to trade in a market defined by caution rather than conviction. On-chain metrics show the asset is at a deep discount relative to the average investor cost basis, while ongoing realized losses confirm the bear market remains firmly entrenched. Simultaneously, ETF outflows and defensive positioning in the options market highlight a broad lack of risk appetite among institutional and derivatives participants.

However, beneath the surface, there are early signs that the environment is beginning to stabilize. Coinbase spot flows have turned constructive, the Short-Term Holder cost basis is adjusting downwards, and the recent weakness has been primarily driven by spot sellers rather than excessive leverage. While these developments do not signal an imminent reversal, they are characteristic of the early stages of a bottoming process.

For now, the market remains in a tug-of-war between ongoing distribution and emerging value-driven demand. The outcome of this battle will define Bitcoin's next major move.