발효: 이더리움이 최대 수혜자가 될까?

- 핵심 견해: 미국의 '디지털 자산 시장 명확성 법안'(CLARITY Act)은 엄격한 탈중앙화 테스트를 확립함으로써, 이더리움을 미국 법체계 하에서 유일하게 프로그래밍 가능성과 규제 명확성을 동시에 갖춘 디지털 상품으로 만들 것입니다. 이는 오랫동안 ETH를 억눌러온 두 가지 주요 하락 논리(규제 리스크와 경쟁 위협)를 종식시키고, 현금 흐름이 아닌 통화 프리미엄에 기반한 가치 평가 체계로 진입하게 하여 잠재적으로 수조 달러 규모의 재평가를 촉발할 것입니다.

- 핵심 요소:

- 법안 내 '조정된 통제'에 관한 다섯 가지 테스트(예: 탈중앙화, 오픈소스, 허가 등) 중 49%의 토큰 또는 의결권 집중도 기준선이 핵심 분기점입니다. 비트코인과 이더리움은 쉽게 통과하는 반면, 솔라나(Solana), BNB 체인, 수이(Sui) 등 주요 스마트 컨트랙트 플랫폼은 구조적 이유로 테스트를 통과하지 못하여 '부속 자산'으로 분류됩니다.

- '부속 자산' 분류는 반기별 공시 의무와 현금 흐름 기반 평가 체계를 야기하며, 이는 해당 토큰의 통화 프리미엄을 상실하게 만듭니다. 반면, 테스트를 통과한 자산(예: ETH 및 BTC)은 희소성, 네트워크 효과 등 비근본적 요소에 기반하여 가격이 책정될 수 있어 평가 상한선이 완전히 제거됩니다.

- ETH는 다섯 가지 모든 테스트를 통과함으로써 '증권'으로 분류될 규제 리스크를 직접적으로 제거합니다. 동시에, 테스트를 통과하지 못한 직접적인 경쟁자(예: 솔라나)는 현금 흐름 평가 체계로 전환될 수밖에 없으며, 통화 프리미엄 평가 체계에서 ETH와 경쟁할 수 없게 되어 '이더리움 킬러'라는 서사가 종식됩니다.

- 비트코인과 비교할 때, 이더리움의 네이티브 스테이킹 수익은 양의 순 보유 비용을 제공하며, 작업 증명(PoW)에서 비롯되는 구조적 매도 압력과 장기적인 보안 보조금 리스크를 피할 수 있어, 더욱 경제적으로 우월한 최상위(Tier 1) 통화 자산으로 자리매김합니다.

- 전 세계 통화 프리미엄 자금 풀(약 50조 달러 자산)은 기관 신뢰도 하락과 지정학적 리스크에 대응하여 부동산, 금 등 전통적 매체에서 디지털 자산으로 이동하고 있습니다. ETH는 마이너스 보유 비용, 글로벌 유동성, 암호학적 안전성 및 기관 독립성을 동시에 갖춘 최초의 후보 자산이 되었습니다.

- 솔라나나 앱토스(Aptos) 등이 향후 4년간의 전환 기간 내에 테스트를 통과한다 하더라도, 법적 인증만으로 자동으로 최상위(Tier 1) 평가를 받지는 못합니다. 네트워크 자체, 생태계 및 시장의 '통화 프리미엄' 속성에 대한 합의가 추가로 필요하며, 이는 현재 성능과 애플리케이션 중심의 네트워크에게는 엄청난 도전 과제입니다.

Original Author: Adriano Feria

Compiled by: Jiahuan, ChainCatcher

On May 12, the Senate Banking Committee released the full 309-page revised text of the Digital Asset Market Clarity Act.

Most coverage will focus on which tokens fail the new decentralization test, which issuers will face new disclosure burdens, and which projects need to restructure within the four-year transitional certification window. This reporting is not wrong, but it is incomplete.

The more important story lies in the impact of this Act on the only asset that passes every single criterion of the test and happens to be the only fully programmable smart contract platform.

Once this framework becomes law, Ethereum will occupy a unique regulatory category under the U.S. legal system, one with only a single member. Over the past five years, the two dominant bearish theses on ETH will simultaneously collapse, and the market has yet to price this in.

Two Bills, One Framework

Before delving into the substance, it is necessary to briefly review the broader regulatory architecture, as public discussion often conflates two distinct pieces of legislation.

The GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act) was signed into law by the President on July 18, 2025.

It establishes the first federal regulatory framework for payment stablecoins: requiring 1:1 reserves in liquid assets, monthly reserve disclosures, federal or state licensing for issuers, a prohibition on algorithmic stablecoins, and a critical limitation that stablecoin issuers cannot pay interest or yield directly to holders.

The GENIUS Act covers USDC, USDT, and bank-issued stablecoins. It includes nothing else.

The CLARITY Act covers everything else. It addresses the SEC and CFTC jurisdictional division, the decentralization test for non-stablecoin tokens, exchange registration, DeFi rules, custody rules, and the ancillary asset framework.

These two acts are complementary parts of a broader regulatory architecture.

Most financial media coverage of the CLARITY Act focuses on stablecoin yield, as Chapter 4's section on "Preserving Stablecoin Holder Rewards" was the political flashpoint that nearly killed the bill.

Banks pushed to prohibit indirect yield through exchanges and DeFi protocols because yield-bearing stablecoins compete with bank deposits. Crypto exchanges strongly advocated for preserving this feature. The bipartisan compromise reached on May 1, 2026, cleared the bill's path, but after several delays in consideration, the bill remains in a precarious state.

This debate is important, but it is only one part of a nine-chapter bill. For anyone who actually holds and trades non-stablecoin tokens, the more far-reaching provisions are hidden in Section 104, and almost no one is discussing the second-order effects on asset valuation.

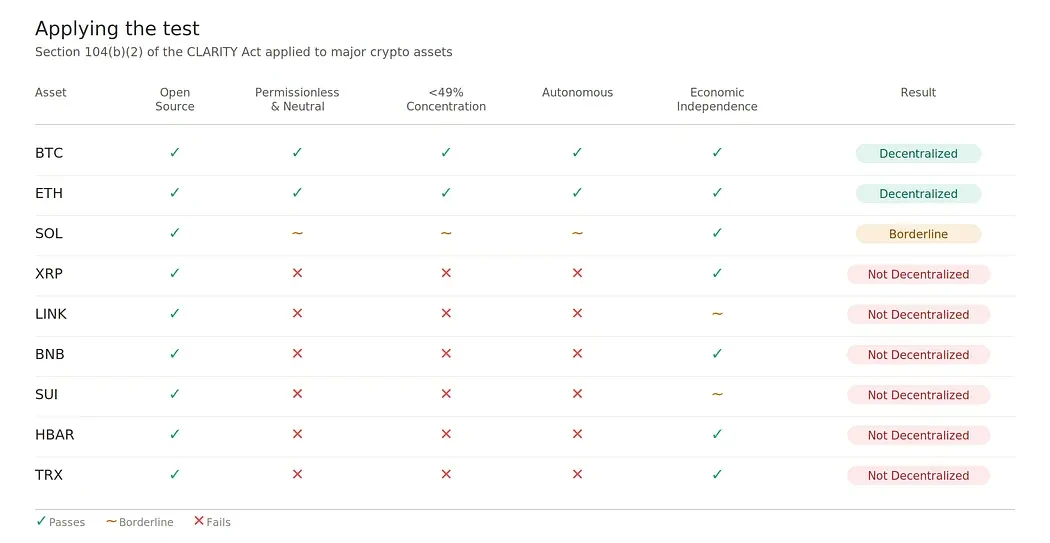

The Five Tests

Section 104(b)(2) of the Act directs the SEC to weigh five criteria when determining whether a network and its token are under coordinated control:

Open digital system. Is the protocol publicly available open-source code?

Permissionless and credibly neutral. Can any coordinated group censor users or grant itself hardcoded priority access?

Distributed digital network. Does any coordinated group beneficially own 49% or more of the circulating tokens or voting power?

Autonomous distributed ledger system. Has the network reached an autonomous state, or does someone retain unilateral upgrade power?

Economic independence. Is the primary value capture mechanism actually functioning?

A network that fails this test will have a "network token" that is presumed to be an "ancillary asset," meaning the token's value depends on the entrepreneurial or managerial efforts of a specific promoter.

This classification triggers semi-annual disclosure obligations, Rule 144-style insider resale restrictions, and initial issuance registration requirements. Secondary market trading on exchanges can continue undisturbed.

The 49% threshold is the core data point; it is much more lenient than the House version of the CLARITY Act's 20% red line. Networks that fail under the 49% threshold do so for genuinely structural reasons, not technicalities.

Bitcoin and Ethereum pass all criteria uncontroversially. Solana hovers at the edge; the Foundation's influence over upgrades, heavy early insider allocation, and a history of coordinated network pauses argue against its autonomy and credible neutrality.

Every other major smart contract platform fails for structural reasons not easily remedied. This list includes XRP, BNB Chain, Sui, Hedera, and Tron, and extends to most other L1 competitors.

Among the assets that pass the test, exactly one has a functioning native smart contract economy.

The Shift in Valuation Regime

Tokens trade on two fundamentally different valuation frameworks.

The first is the commodity/monetary premium regime, where value derives from scarcity, network effects, store-of-value properties, and reflexive demand, with no fundamental valuation ceiling.

The second is the cash flow/equity regime, where value derives from revenue capitalized through standard multiples and bounded by hard limits imposed by realistic revenue projections.

Most non-Bitcoin tokens have existed in a strategic ambiguity between these two regimes, marketing themselves under whichever framework yields a higher valuation. The CLARITY Act ends this ambiguity through three mechanisms.

First, disclosure requirements impose a cognitive framework. Section 4B(d) requires semi-annual disclosures including audited financial statements (over $25 million), a CFO's going-concern statement, a summary of related-party transactions, and forward-looking development costs.

Once a token has an SEC filing akin to a 10-Q, institutional analysts will evaluate it like any entity filing a 10-Q. The filing format dictates the valuation framework.

Second, the statutory definition itself is a qualifier. An ancillary asset is defined as a token "whose value depends on the entrepreneurial or managerial efforts of the ancillary asset promoter." This definition is conceptually incompatible with a monetary premium, which requires value independent of any issuer's efforts.

A token cannot simultaneously satisfy the legal definition of an ancillary asset and credibly claim the pricing power of a monetary premium.

Third, visible scarcity is fragile scarcity. Monetary premiums are reflexive, and reflexivity requires a scarcity narrative that the market can collectively believe.

When a token discloses its treasury, named insider unlock schedules, and quarterly reports on related-party transactions to the SEC, its scarcity story becomes visible; once visible, reflexivity vanishes. Investors can see exactly how much insiders hold and when those tokens will be sold. This visibility kills the bid.

The result is a two-tier market. Tier 1 assets trade on a monetary premium with no fundamental valuation ceiling. Tier 2 assets trade on revenue multiples with a rational valuation ceiling.

Tokens currently priced on Tier 1 logic but relegated to Tier 2 will face a structural re-rating. For tokens with weak fundamentals but valuation driven primarily by narrative, with LINK and SUI being the most typical examples, this re-rating could be dramatic.

The End of Two ETH Bearish Theses

For five years, the bearish case for ETH rested on two pillars.

The first thesis held that ETH would ultimately be classified not as a commodity but as a security. The pre-mine, the Foundation's ongoing influence, Vitalik's public role, and post-merge validator economics all gave the SEC ample grounds to act if it chose.

Every bullish case for ETH had to discount the tail risk that institutional capital channels might be restricted.

The second thesis held that ETH would be replaced by faster, cheaper smart contract platforms. Every cycle births new "Ethereum killers": Solana, Sui, Aptos, Avalanche, Sei, and BNB Chain, each marketed on better user experience and lower fees.

This argument posits that ETH's technological limitations will force economic activity to migrate, diluting its value capture ability.

The CLARITY Act does not just weaken these bearish theses; it structurally overturns them.

The first thesis collapses because ETH cleanly passes all five criteria of Section 104. No coordinated control, ownership concentration far below 49%, no unilateral upgrade power post-merge, fully open source, value capture mechanism functioning normally.

The regulatory tail risk that long justified a discount on ETH disappears completely.

The second thesis collapses in a more interesting way. "Ethereum killers" can only compete with ETH if they adopt the same valuation framework.

If SOL is certified as a decentralized asset, competition continues. If it fails the test (as it currently appears all other major smart contract competitors do), they will be forced into the Tier 2 valuation regime, while ETH remains in Tier 1.

The competitive landscape thus changes. Tier 2 assets cannot compete with Tier 1 assets on monetary premium, because the core meaning of Tier 1 is that it is not bounded by a fundamental valuation ceiling.

Faster, cheaper chains can still win in specific verticals on transaction throughput and developer attention. But they cannot win on the asset valuation framework that determines L1 market caps the most.

The Only Ticket

Among assets passing the Section 104 test, Ethereum is the only one with a functioning native smart contract economy. Bitcoin passes the test, but its base layer does not support programmable finance.

Every smart contract platform with meaningful TVL has one or more material failures in the test. This includes Solana, BNB Chain, Sui, Tron, Avalanche, Near, Aptos, and Cardano.

Thus, the Act creates a new regulatory category: a decentralized digital commodity with a native smart contract economy, and currently, this category has exactly one member.

Every traditional financial institution exploring tokenization, settlement, custody, or on-chain finance needs two things: programmability and regulatory clarity.

Before CLARITY, these attributes were strictly separated. Bitcoin had clarity but no programmability. Smart contract platforms had programmability but legal ambiguity. After CLARITY, Ethereum becomes the only asset offering both attributes within a single statutory category.

Once the framework takes effect, anyone building tokenized treasuries, tokenized funds, on-chain settlement infrastructure, or institutional-grade DeFi onboarding will have a clear preferred base layer.

This preference is not aesthetic or technical. It is compliance-driven. Asset managers, custodians, and bank-affiliated funds operate within legal frameworks that favor commodity-class assets and disfavor security-like assets.

Institutional capital flows follow asset classification, and the classification has now narrowed to a single programmable asset.

The Sound Money Question

Once BTC and ETH share the Tier 1 classification, it is necessary to closely examine their comparison in monetary properties, as conventional wisdom has the causality backwards.

The preference for Bitcoin has always rested on its nominally fixed supply schedule of 21 million and its predictable four-year halving. As a scarcity narrative, this is indeed very valuable, and the simplicity of this story is one reason BTC was the first to achieve a monetary premium.

But BTC's supply model also carries three structural burdens rarely mentioned when discussing scarcity.

First, mining generates continuous structural sell pressure. Network security depends on miners bearing real-world operating costs: electricity, hardware, hosting, and financing.

These costs are denominated in fiat currency, meaning miners must persistently sell a significant portion of newly issued BTC into the market regardless of price.

This selling is permanent, price-insensitive, and embedded in the consensus mechanism itself. It is the cost of maintaining proof-of-work security.

Second, BTC offers no native yield. Holders seeking yield must either lend BTC to counterparties (introducing credit risk) or move it to non-BTC platforms (introducing custody and bridge risk).

The opportunity cost of holding non-yield-bearing BTC compounds over time for holders who could be earning native yield. For institutional holders measuring performance against yield-inclusive benchmarks, this is a real and persistent drag.

Third, the cliff-like decline in mining subsidies is a long-tail risk to the decentralization that qualifies BTC for Tier 1 classification.

Block rewards halve every four years and approach zero by 2140, but the actual pressure arrives much sooner. By the 2030s, subsidy revenue will be a fraction of today's, and the network must rely on fee revenue to maintain security.

If fee markets fail to develop adequately, the lowest-cost mining operators will consolidate, miner concentration will increase, and the credible neutrality valuation prized by Section 104 will begin to erode. This is not an imminent risk but a structural risk that BTC's model has not resolved.

Ethereum reverses each of these properties.

ETH has variable issuance and no fixed cap, the core argument sound money purists use against it. This argument is superficial.

What matters to a holder is the rate of change in their proportional share of total supply, not whether the supply schedule has a fixed terminal value.

Under Ethereum's post-merge design, all issued tokens are distributed as staking rewards to validators. Validators have historically earned yields higher than the inflation rate, meaning anyone who participates in staking can maintain or increase their proportional share of total supply over time.

For anyone participating in a validator node or holding a liquid staking token, the "infinite supply" argument is rhetorically powerful but mathematically unsupported.

The structural sell pressure that burdens BTC does not exist at a comparable scale for ETH. Validator operating costs are negligible relative to their earnings. Solo staking requires a one-time hardware purchase and minimal ongoing electricity. Liquid staking and pooled staking abstract even these costs away.

New issuance accumulates to validators and is largely retained, rather than being sold into the market to cover costs. This same security model that distributes yield to holders also avoids the price-insensitive selling required by proof-of-work.

The subsidy cliff problem also does not apply. Ethereum's security budget scales with the value of staked ETH and is funded through ongoing issuance and fee revenue. There is no predetermined date when security funding suddenly dries up.

This model is self-sustaining, while BTC's model increasingly depends on the development of fee markets, the achievement of which remains uncertain.

None of this argues that ETH will replace BTC. They play different roles in institutional portfolios.

BTC is a simpler, clearer, politically more defensible scarce asset. ETH is productive monetary collateral that pays its holders for participating in its security.

The key point is that the conventional view that BTC has "harder money" properties than ETH because of a fixed supply cap collapses under scrutiny.

ETH's variable issuance combined with native yield provides better economic properties for holders than BTC's fixed supply combined with zero yield, and it does so without structural sell pressure or long-term security funding risk.

For institutional allocators building Tier 1 cryptocurrency exposure, this matters significantly. The case for placing ETH alongside BTC is not just "the programmable one