Strategy Q1 재무 보고서: 장부상 손실 144억 달러, 코인 매각을 통한 이자 지급 가능성 배제하지 않아

- 핵심 의견: Strategy사의 2026년 1분기 재무 보고서에 따르면 순손실 1254억 달러를 기록했으며, 이는 주로 BTC 가격 하락으로 인한 미실현 손실에 기인한다. 하지만 회사는 여전히 BTC를 추가 매수하고 STRC 우선주 자금 조달에 의존하고 있으며, 동시에 처음으로 배당금 지급을 위해 BTC를 매각할 가능성을 시사하여 시장의 주목을 받고 있다.

- 핵심 요소:

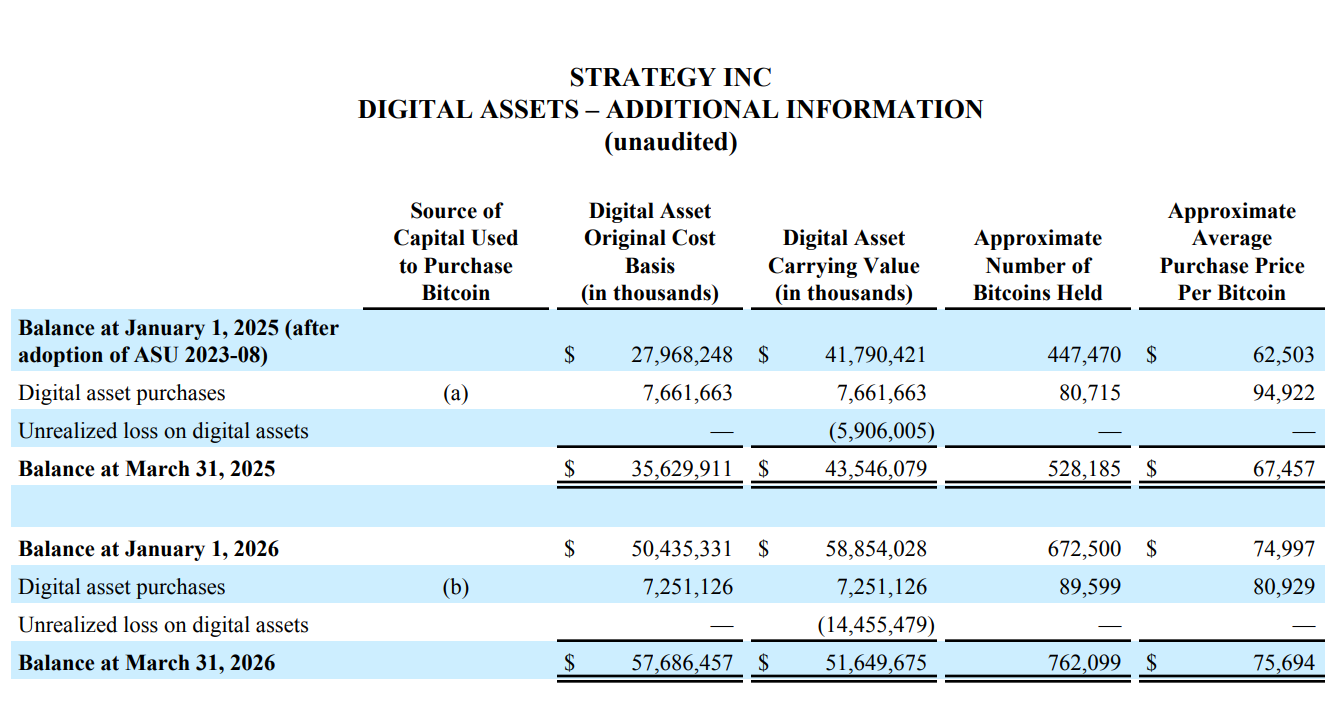

- 1분기 순손실 1254억 달러는 주로 1446억 달러의 미실현 손실에서 비롯되었으며, 81만 8300개의 BTC를 보유하고 평균 단가는 약 75,537달러이다.

- 회사는 처음으로 '배당금 지급을 위한 BTC 매각' 가능성을 명확히 언급했으며, 현재 순부채는 817억 달러, 현금 보유액은 22억 1000만 달러에 불과하다.

- STRC 우선주는 9개월 만에 시가총액 850억 달러를 달성하며 세계 최대 규모의 우선주가 되었고, 2분기 자금 조달 구조가 전환되어 STRC 비중이 80%를 초과했다.

- 1분기 동안 89,599개의 BTC(평균 단가 80,929달러)를 매수했지만, 1254억 달러의 순손실은 BTC 가격 하락의 영향을 반영한다.

- 소프트웨어 수익은 1억 2430만 달러에 불과하며 완전히 주변화되었고, 역사적 이익잉여금이 처음으로 흑자에서 적자로 전환되어 누적 적자는 647억 달러에 달한다.

- DeFi 생태계 구축 과정에서 STRC는 Apyx와 같은 프로토콜에 의해 27억 달러 규모로 흡수되어 온체인 담보 자산으로 사용되었다.

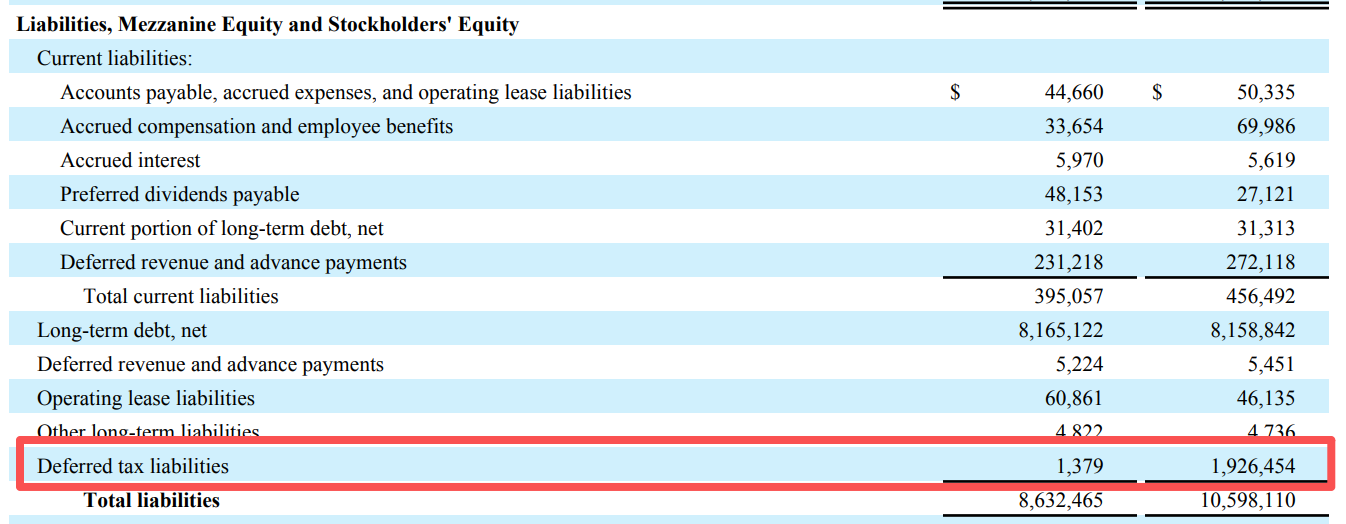

- 이연법인세 부채는 193억 달러에서 138만 달러로 감소했으며, 향후 10년간 과세 대상 이익이 없을 것으로 예상되어 세액 공제가 사실상 무효화되었다.

Original|Odaily Planet Daily (@OdailyChina)

Author|Wenser (@wenser 2010 )

Early this morning, Strategy's Q1 2026 earnings call officially concluded, and its Q1 financial report was released. Thus, the true operational status of this "industry heart," holding 818,300 BTC, was once again exposed to the market. Behind the net loss of $12.54 billion lies the fact that BTC prices briefly dropped to around $62,000, 63,400 BTC were continuously accumulated, and the STRC scale grew to $8.5 billion.

Of course, the most intriguing part of the financial report and Michael Saylor's external statements revolves around the possibility of "Strategy selling some BTC to pay dividends." Perhaps influenced by this news, despite Q1 performance falling short of market expectations, capital markets reacted favorably, with Strategy's stock price rising slightly by 3%.

Odaily Planet Daily summarizes the key points and future potential highlights from the Q1 financial report as follows.

Strategy's Q1 Digital Ledger: Book Net Loss of $12.5 Billion, Not Ruling Out BTC Sales for Dividend Payments

Key Point 1: Selling BTC is No Longer Impossible, but an Option

Looking closely at the Q1 financial report and earnings call content, Strategy repeatedly mentions in its forward-looking statements and KPI explanations: "If convertible notes mature or are called for redemption without conversion into common stock, the company may need to sell common stock or Bitcoin to generate sufficient cash to fulfill these obligations."

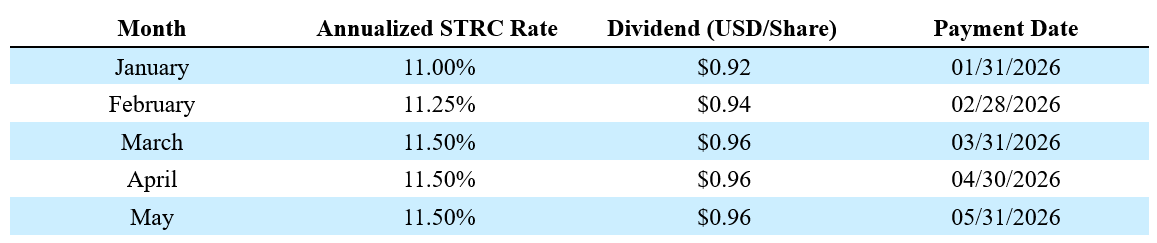

As of the end of Q1, Strategy had $8.17 billion in net long-term debt, $10 billion in preferred stock redemption value, and only $2.21 billion in cash. Meanwhile, the company needs to continuously pay preferred stock dividends (currently STRC's annualized rate is 11.5%) and has already begun financing dividends through issuing common stock. If BTC prices continue to face pressure, leading to constrained financing options, selling BTC to repay debt would transition from a theoretical assumption to a realistic possibility, inevitably impacting the market.

Strategy founder Michael Saylor stated, "This move is merely to convey a message to the market that this model (referring to verifying that Bitcoin assets can support shareholder returns within a corporate financial system) has been realized."

Notably, unlike traditional companies' "KPI metrics," Strategy has created its own KPI system, including: BPS (Bitcoin Per Share), BTC Yield (9.4%), BTC Gain (63,410 BTC), and BTC$ Gain ($4.97 billion) (Odaily Planet Daily Note: Data as of May 3). However, in the disclaimer, it also points out that these metrics do not consider debt, do not consider the priority claim of preferred stock, do not represent return on investment, do not represent fair value gains, and that 'BTC$ Gain can be positive while the company is recording significant fair value losses.' Indeed, Strategy's Q1 business performance confirms this mechanism: KPIs show $4.97 billion in BTC dollar gains, but under GAAP, the company recorded $14.46 billion in unrealized losses. The core function of this KPI system is to sustain the capital market narrative, not to reflect true financial health. To put it bluntly, 'spinning bad news into good' or 'reporting only the good news while omitting the bad' is a common tactic for Strategy in capital markets.

As of May 3, 2026, Strategy held 818,334 Bitcoin, a 22% increase year-to-date. However, the Q1 financial report recorded a net loss of $12.54 billion, almost entirely from unrealized losses on digital assets ($14.46 billion); the total cost basis for the 818,334 BTC was $61.81 billion, corresponding to an average purchase price of approximately $75,537 per BTC. Notably, thanks to the recent market rebound, the Q2 unrealized gain stands at $8.3 billion.

Key Point 2: Spent $7.25 Billion on BTC in Q1, but BTC Book Value Shrank by $7.2 Billion at Quarter-End

Purely from a buying and selling perspective, Strategy's Q1 balance sheet barely qualifies as "breaking even."

Financial data shows that Strategy purchased 89,599 BTC in Q1, spending $7.25 billion at an average price of approximately $80,929. However, due to BTC's decline, the book value of digital assets dropped from $58.85 billion at the start of the year to $51.65 billion, a net decrease of about $7.2 billion.

It must be said that continuously leveraging (financing + dividends) to buy the dip on BTC during a bear market and achieving such results is already quite commendable.

Key Point 3: AI's Impact on Strategy is Real, Software Business Fully Marginalized

Nominally, Strategy still insists it is an "AI-driven enterprise analytics software company," as evidenced by its revenue structure including software subscription service revenue, license revenue, and product support revenue.

However, from a structural comparison, Strategy's Q1 total software revenue was only $124.3 million, with gross profit of just $83.35 million. Compared to its BTC holdings market value of $64.1 billion, this over 500x quarterly revenue gap clearly tells the market: In the era of AI development, the software business, barely touching AI, has been completely marginalized.

Key Point 4: STRC Becomes the Star Business, Reaching $8.5 Billion Market Cap in 9 Months

As Strategy's "financing tool," STRC's market performance during the ongoing bear market can be considered a "lifeline."

Currently, STRC (Variable Rate Series A Perpetual Preferred Stock) has grown to $8.5 billion in just 9 months, becoming the world's largest preferred stock by market cap. Year-to-date, Strategy has raised $5.58 billion through STRC, a growth rate of 189%.

Additionally, Strategy stated that STRC's Sharpe ratio reached 2.53, with volatility of only 3%, and an average daily trading volume of $375 million. This means that through STRC, a low-volatility, high-yield, high-liquidity fixed-income product, a new type of BTC reserve-backed asset has emerged in traditional financial markets.

Key Point 5: Major Financing Structure Shift in Q1 and Q2, STRC Becomes the Main Financing Force

In the financial report, of the $7.37 billion raised in Q1, MSTR common stock ATM contributed $5.3 billion, and STRC contributed $2.07 billion, a ratio of about 72% to 28%. However, entering Q2 (April 1 to May 3), this structure reversed, with STRC contributing $3.51 billion in financing and MSTR only $0.81 billion.

This means the financing gap for common stock is narrowing, and Strategy is increasingly relying on preferred stock that provides fixed income to maintain capital reserves, thereby continuing to drive BTC accumulation.

Furthermore, perhaps considering STRC's stellar performance and strong capital appeal, Strategy is actively promoting this "wealth management fixed-income product" in traditional financial markets. The company has initiated a proposal for semi-monthly STRC dividend payment votes, aiming to shorten the dividend payment cycle to attract more capital for purchase.

Key Point 6: Strategy Records First-Ever Accumulated Deficit in Retained Earnings

In traditional financial markets, retained earnings are a key measure of a company's financial health, representing the cumulative result of all net profits minus all dividends since its inception. In other words, it's a company's "savings pot."

From its founding in 1989 to the end of 2025, over thirty years of operations, Strategy had accumulated $6.32 billion in cumulative profits. However, by the end of the first quarter of this year, this figure turned negative, resulting in a cumulative deficit of $6.47 billion.

This is a direct consequence of the ASU 2023-08 standard (Odaily Planet Daily Note: This standard requires publicly traded companies to measure BTC at fair value from 2025, with price changes directly recorded in the income statement). From the GAAP perspective commonly used in traditional financial markets, the historical cumulative profits Strategy built over thirty years have been completely wiped out by one quarter of BTC decline.

Of course, what goes down can come up. If BTC prices recover later, this figure could turn positive again. This metric once again highlights the high risk and high volatility of crypto assets compared to traditional financial assets.

Key Point 7: STRC-Centered DeFi Ecosystem Under Construction

Strategy's Q1 financial report mentioned that DeFi protocols like Apyx and Saturn have absorbed over $270 million in STRC assets, while $150 million in STRC assets have been incorporated into the corporate asset treasuries of listed companies like Prevalon, Strive, and Anchorage.

In other words, STRC is evolving from a single preferred stock financing tool into a foundational collateral asset for the on-chain ecosystem of the cryptocurrency market. If STRC's appeal to capital markets and the crypto ecosystem continues to grow (Odaily Planet Daily Note: Fixed income is quite attractive in the wealth management sector, whether in traditional finance or crypto), STRC will gradually surpass MSTR (traditional preferred stock).

Of course, there are trade-offs. As STRC's proportion increases, the requirements for Strategy's dividend-paying capacity become higher, and the reach of market risk transmission will broaden.

Key Point 8: Tax Deduction Credit Exists, but Useless for the Next Decade

Beyond operational data, Strategy's Q1 financial report also mentioned drastic changes in deferred tax liabilities.

According to the table data, Strategy's deferred tax liabilities plummeted from nearly $1.93 billion at the start of the year to just $1.38 million at the end of Q1, nearly zero.

In other words, Strategy previously had a nearly $1.93 billion "accrued tax bill" due to profits from its business operations. However, due to the business losses caused by the BTC decline, the company's asset income statement recorded this unpaid tax as "income tax benefit." Additionally, Strategy's $14.46 billion unrealized loss in Q1 could theoretically offset part of its tax liability, meaning the business losses reduce the taxes payable, creating a "tax shield."

The problem, however, is that this tax shield, which can offset taxes, is only effective if Strategy has taxable profits in the future. Yet, the company stated it does not expect taxable profits for at least ten years. In other words, Strategy gained a "$1.9 billion tax deduction benefit" from the BTC decline, but since future taxable profits are unlikely, this benefit will probably never be realized.

Finally, aside from purchasing Strategy-related stocks, a prediction market bet on "whether Strategy will sell Bitcoin before the end of the year" has gone live, with the probability of "Yes" currently at 44%.