ArkStream Capital 2026년 1분기 보고서: 지정학적 갈등과 유동성 후퇴 속 암호화폐 업계의 구조적 정리

- 핵심 의견: 2026년 1분기, 암호화폐 시장은 지정학적 갈등, 무역 전쟁, 매파적 연준 정책의 다중 압력 속에서 전반적인 매도세를 경험했습니다. 비트코인은 93,000달러에서 63,000달러로 하락했고, 디지털 골드 서사는 반증되었으며, 알트코인 시장은 유동성 고갈에 직면했습니다. AI 산업의 블랙홀 효과는 자금 분화를 더욱 심화시켰고, 시장 정리는 아직 끝나지 않았습니다.

- 핵심 요소:

- 거시적 압박: 트럼프의 관세 정책, 미-이란 군사 충돌, 연준의 금리 인하 기대 붕괴 (2회에서 거의 0으로 축소)는 삼중의 시스템적 위험을 구성하여 위험 자산 전반에 부담을 주고 정책 불확실성 프리미엄을 발생시켰습니다.

- 비트코인 서사 무력화: 데이터에 따르면 비트코인은 나스닥과 높은 상관관계를 보이고 금과의 상관관계는 극히 낮아, 극단적인 위험 상황에서는 안전 자산이 아닌 '유동성 압력 완화 밸브' 역할을 합니다. ETF 투자자들의 평가 손실이 약 23%에 달해 매도를 가속화했습니다.

- 알트코인 시장의 구조적 위축: 알트코인은 주기 고점 대비 60%-80% 하락했고, BTC Dominance는 높은 수준(56%-59%)을 유지하고 있습니다. ETF 및 DAT 자금은 모두 BTC에 고정되어 있으며, 중소형 알트코인은 혁신과 자금 유입 부족으로 가치 회귀와 투기 고갈 현상을 겪고 있습니다.

- AI 블랙홀 효과: AI 산업은 경제성 주도 단계(API 비용 80% 감소)에 진입하여 주식 부문 수익률이 Crypto+AI 토큰을 크게 앞지르며 지속적인 자금 유출을 초래하고 있습니다. Crypto+AI의 대부분의 서사는 여전히 과장 단계에 머물러 있습니다.

- VC 투자 딜레마: 프로젝트 언락 규칙으로 인해 VC는 '후순위' 지위에 놓이게 되어 1차 투자 손실이 확대되고 회수 난이도가 높아졌습니다. 거래소 상장 전략은 죄수의 딜레마를 심화시켜 중소형 알트코인 공매도가 소수의 긍정적 기대치를 가진 헤지 수단으로 남아 있습니다.

Prologue

In the first quarter of 2026, the global financial market entered its most severe risk repricing cycle since 2022. The continued escalation of geopolitical conflicts, the full-fledged return of trade protectionism, and the wavering monetary policies of major economies have collectively created a macro environment characterized by high uncertainty and low liquidity preference. The crypto market experienced a systemic sell-off during this quarter, with Bitcoin dropping from around $93,000 at the beginning of the year to the $63,000 range, a maximum drawdown exceeding 38%. The altcoin market suffered even more severely, with many tokens losing 60%–80% from their cycle highs.

The deterioration of the market environment was not an accident but the result of multiple overlapping structural pressures. On one hand, the Trump administration's aggressive tariff policies and the US-Iran military conflict pushed geopolitical risks to new heights, putting general pressure on risk assets. On the other hand, the crypto market's own narrative fatigue and the fragility of its liquidity structure were fully exposed during the downtrend. Bitcoin's "digital gold" narrative failed to deliver on its safe-haven function in a wartime environment, instead behaving like a high-beta risk asset. Altcoins, lacking new capital inflows and fundamental support, fell into a sustained value regression.

Meanwhile, the rapid evolution of the AI field is profoundly reshaping the intersection of technology and finance. The continuous iteration of large language model capabilities, the explosive growth of open-source AI Agent frameworks, and the initial integration of AI with Crypto payment scenarios offer noteworthy new variables for the medium to long-term development of the industry.

The following sections will dissect the core variables of Q1 across four dimensions: the macro environment, Bitcoin and capital structure, AI development trends, and altcoin market divergence, concluding with ArkStream Capital's framework for future direction.

Macro Environment: Systematic Suppression from Geopolitical Conflicts and Trade Wars

Accelerated Fragmentation of the Global Trade System

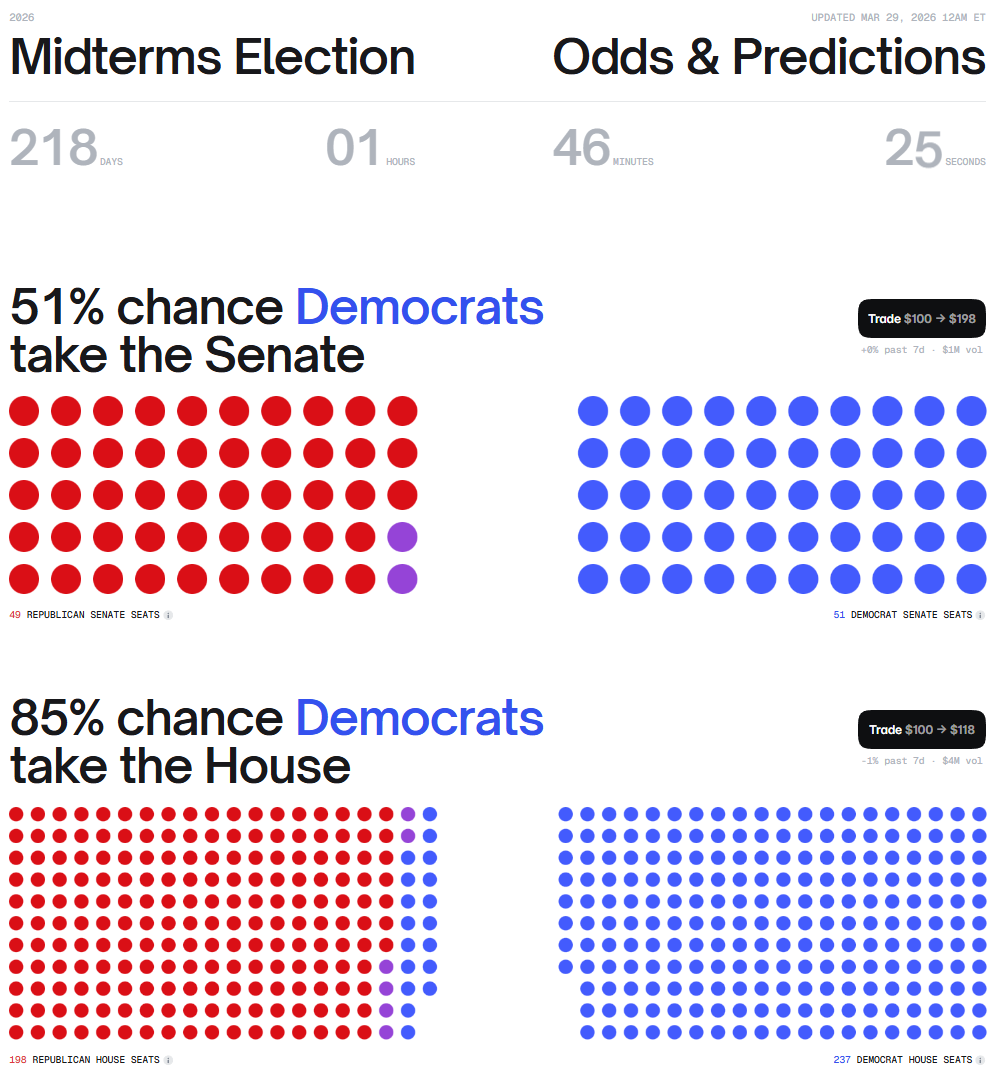

The primary analytical framework for understanding Q1 policy actions is the November 2026 US midterm elections. The Republican Party's slim majority in both the Senate and the House faces significant challenges. Historically, the incumbent party almost invariably loses seats in midterm elections. Under this pressure, the Trump administration's intensive rollout of强硬 tariffs, the Greenland sovereignty narrative, and military strikes against Iraq in Q1 all serve essentially the same political logic: consolidating the Republican base through aggressive foreign and economic policy postures, and crafting a "strong president" narrative in an election year. This means that at least until the November vote, policy unpredictability and aggressiveness are unlikely to cool down substantially. The political uncertainty premium faced by risk assets will persist throughout the year.

Projected seat distribution for the 2026 US midterm elections (Senate and House)

https://polymarket.com/predictions/midterms

Driven by this political logic, the global trade order experienced its most severe shock since the founding of the WTO in Q1. In mid-January, the Trump administration announced tiered tariffs of 10%–25% on eight countries (Denmark, Norway, Sweden, France, Germany, the UK, the Netherlands, and Finland), using the Greenland sovereignty dispute as a bargaining chip. At the end of January, a bill imposing 500% punitive tariffs on countries purchasing Russian oil (directly targeting BRICS nations like China, India, and Brazil) gained bipartisan support and entered the voting process. After the US Supreme Court struck down the IEEPA-based tariff rationale on February 20th, Trump immediately invoked Section 122 of the Trade Act of 1974 to re-impose a 10% global temporary tariff (valid for 150 days).

The repeated and escalating tariff policies impacted markets from three dimensions: Cost side, import tariffs directly push up commodity prices and inflation expectations, compressing the Fed's room for rate cuts; Supply chain side, retaliatory measures from trading partners exacerbate global supply chain uncertainty, dampening corporate capital expenditure intentions; Risk premium side, the inherent unpredictability of the policy itself becomes the biggest pricing problem, systematically raising implied volatility across various risk assets. ArkStream Capital believes that the market-suppressing effects of the latter two are far more difficult to quantify than the tariff rates themselves and are harder for the market to fully price in.

📊 [Chart Placeholder] News screenshot or map related to the Greenland sovereignty dispute

https://truthsocial.com/@realDonaldTrump/posts/115925897257210763

The fundamental difference between this round of trade conflict and past tariff confrontations is that the scope of the conflict has expanded from bilateral to multilateral. The repeated changes in the legal basis indicate that policy-making has itself deviated from the institutional track, entering a new phase of "instant executive power." Its suppressive effect on risk assets far exceeds the direct economic impact of the tariff rates themselves.

The Tail Risk of US-Iran Military Conflict

On February 28th, the US and Israel launched coordinated military strikes against Iran. Oil prices surged within hours, and global financial markets shifted into risk-off mode. With traditional markets closed for the weekend, the crypto market, being the only major asset class trading 24/7, bore the brunt of the safe-haven selling pressure. Bitcoin dropped from $65,500 to $63,000 within an hour, leading to the liquidation of over $515 million in leveraged positions.

This event once again confirmed a reality: Under the current institutional participation structure, crypto assets in extreme risk events play more of a "liquidity relief valve" role than a safe-haven tool. When traditional markets are closed, the crypto market becomes the only operational channel for global capital to release risk. Its price action reflects liquidity structure more than fundamental logic.

Q1 Crude Oil Price Trend

https://www.tradingview.com/chart/WZsS9J3A/?symbol=NYMEX%3ACL1!

The impact went far beyond the price level. Within hours of the strikes, the Iranian leadership announced a blockade of the Strait of Hormuz, one of the most critical arteries for global oil transportation, through which nearly 20% of the world's seaborne oil trade passes. This super tail risk layered an energy supply shock onto already high global inflation, directly impacting European and Asian economies heavily reliant on imported photovoltaic energy. Even though a ceasefire was ostensibly reached through negotiations days later, the pricing of this tail risk has not been fully eliminated. If the conflict escalates again, the market's reaction could be far more severe than the initial shock.

For the crypto market, this shock bore a dual burden: first, rising oil prices increased inflation expectations, further compressing the Fed's room for rate cuts; second, the pre-market anxiety of investors could only be released through the crypto market. Meanwhile, Iran's uncertain subsequent situation remains the core macro variable for geopolitical risk signals in Q2. If the conflict escalates further under the political logic of the midterm election year, the suppression of risk assets will be more than a repeat of Q1.

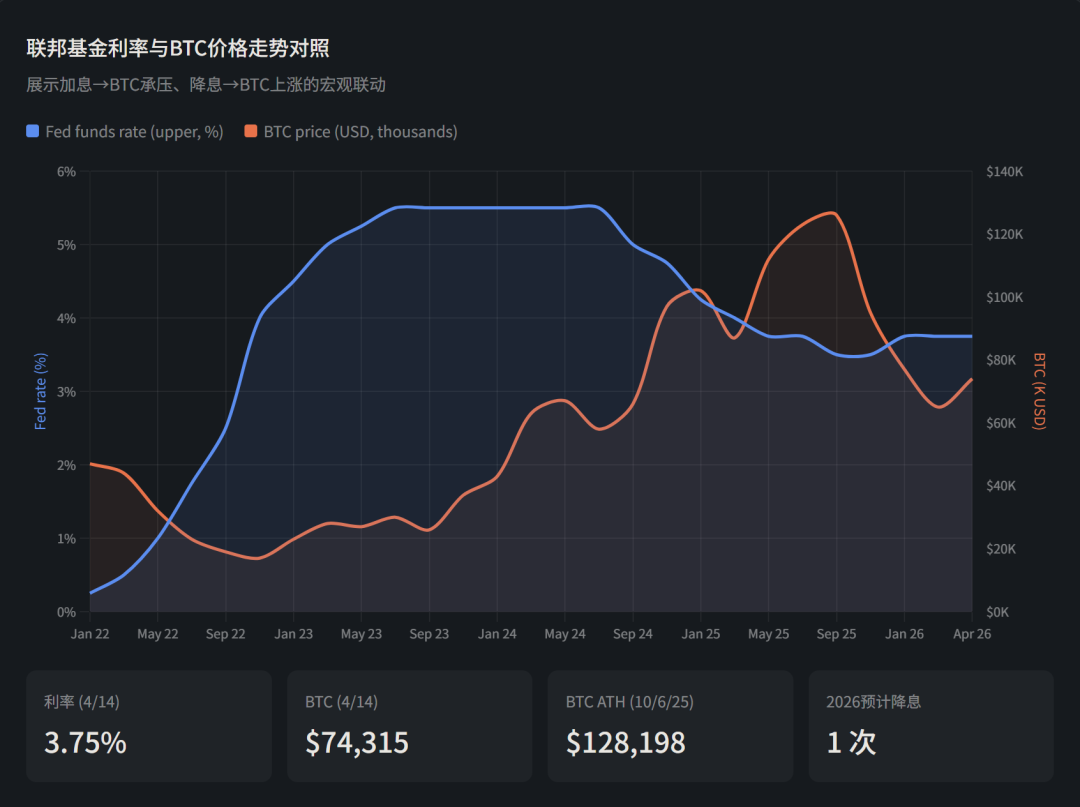

The Federal Reserve: Reversal of the Rate Cut Path and Delay of the Liquidity Inflection Point

Macro-wise, BTC, as a peripheral market within the financial sector, has historically shown significant correlation with the Fed's interest rate policy.

Fed Funds Rate vs BTC Price (2022–2026)

Starting from 2022, roughly 4 distinct cycles are observable.

2022-2023: Hiking Cycle → BTC Under Pressure

The Fed began aggressive rate hikes from early 2022, moving from near-zero to 5.5%. During the same period, BTC plummeted from ~$47K to $16K. High interest rates increased the opportunity cost of holding non-yielding risk assets like BTC, leading to capital outflows.

Late 2023 - Early 2024: Pause in Hikes → BTC Bottoms and Recovers

While rates remained in the 5.25%-5.50% range, the market began pricing in rate cut expectations. BTC recovered from $16K to over $60K. Concurrently, the SEC approved 11 spot BTC ETFs in January 2024, marking BTC's official entry into mainstream finance.

September 2024 - October 2025: Rate Cutting Cycle → BTC Surges

The Fed cut rates by 50 basis points for the first time in September 2024, followed by three consecutive cuts totaling 100 bps that year. Three more cuts in 2025 brought the cumulative reduction to 1.75%. During this period, BTC skyrocketed from $66K to its all-time high of $128,198.

Late 2025 - Present: Rate Cut Pause + Geopolitical Conflict → BTC Correction

The Fed held rates steady at 3.50%-3.75% at both its January and March 2026 meetings, citing rising oil prices pushing up inflation expectations. PCE and core PCE forecasts were both revised up to 2.7%. Combined with heightened tensions in the Middle East, BTC has fallen from $126K to its current level around $74K.

Current Rate Cut Expectations

Rate cuts lower the opportunity cost of holding BTC and increase market liquidity, historically showing a strong positive correlation with BTC's rise. The Fed's dot plot indicates one rate cut expected in 2026, which is not good news for BTC's price.

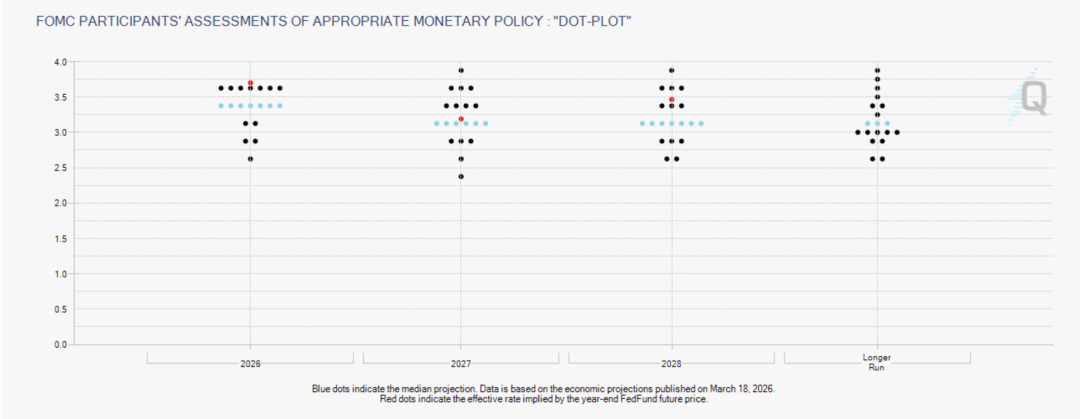

The Fed's policy path underwent a gradual hawkish shift in Q1. Rate cut expectations were progressively compressed from 2 cuts expected at the start of the year to near zero.

Dot Plot

https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

The January 28th FOMC meeting kept the federal funds rate unchanged at 3.5%–3.75%, the first pause after three consecutive cuts in 2025. Powell reiterated the need for "more data to confirm inflation is sustainably moving down," his tone cautious but neutral. However, the minutes released on February 18th revealed far deeper internal divisions than the statement suggested. Several officials explicitly mentioned the possibility of a rate hike scenario, the first such language in the minutes since 2023, creating cracks in market confidence regarding rate cuts.

On January 30th, Trump announced the nomination of former Fed Governor Kevin Warsh to replace Powell as Chair (the nomination was formally submitted to the Senate on March 4th), with an expected start date in May. During his tenure as a Fed governor from 2006 to 2011, Warsh was one of the youngest and most hawkish members of the committee, having resigned in opposition to QE2. Notably, his recent public statements have softened somewhat, arguing that AI-driven productivity gains have a structural deflationary effect, thus supporting lower interest rates. However, his most prominent label remains "balance sheet reduction before rate cuts." Warsh has frequently criticized the Fed for maintaining a bloated balance sheet that blurs the lines between monetary and fiscal policy, advocating for significant balance sheet reduction before discussing rate cuts. Even if nominal rates edge down, aggressive balance sheet reduction could tighten liquidity, potentially offsetting the effects of rate cuts (some analysts estimate that shrinking the balance sheet by roughly $1 trillion has an effect equivalent to a 50bp hike). The market interpreted his nomination as generally hawkish. Some institutions labeled it an "intriguing choice for a president who wants lower rates." Following the nomination news, precious metals fell first (gold dropped 1.9% in a week), the dollar strengthened, and the market began repricing what a Fed chaired by someone like this would mean.

The situation grew more complex in February. The US-Israel military strikes against Iran on February 28th (see Section 1.2) caused oil prices to surge past $100/barrel, fundamentally altering the inflation landscape. Before the cost-push inflation from tariffs could be digested, a supply-side shock from energy prices was layered on top, creating dual inflationary pressures. The policy space for rate cuts was severely compressed. The market began seriously discussing a previously absurd possibility: the next move might not be a cut, but a hike.

The March 18th FOMC meeting put this into black and white. The committee voted 11:1 to hold rates steady (the January meeting was 10:2, with Miran and Waller dissenting; in March, Waller switched to the majority, leaving only Miran dissenting, a shift notable in itself as a hawkish convergence signal). The post-meeting statement notably included new language about "uncertainty regarding the implications of developments in the Middle East for the U.S. economy," officially incorporating the war factor into the Fed's decision-making framework. The updated Summary of Economic Projections (SEP) and dot plot released a clear hawkish signal: the 2026 inflation forecast was raised to 2.7%, the median dot plot maintained one rate cut for the year (unchanged from December; Powell stated explicitly "the median hasn't changed"), but 14 out of 19 committee members expected only 0–1 cuts for the year, a clear hawkish shift in distribution; CME FedWatch showed the market compressed year-end rate cut expectations from 2 at the start of the year to at most 1, with the probability of zero cuts rising significantly.

The unemployment rate forecast remained at 4.4%, and GDP growth was revised slightly higher, painting a picture of growth resilience + inflation stickiness – a stagflationary prototype. BTC responded by dipping from $74,000 to $70,900, with ETFs seeing a net outflow of $129 million on the day. Some market analysts pointed out that Warsh's first move upon taking office might not be a rate cut, but a hike.

Looking back at the entire first quarter, the collapse of rate cut expectations was not a single event but a process – from the discussion of hikes in the January minutes, to the hawkish personnel expectations raised by the Warsh nomination, to the secondary inflation shock from the Iran war, to the March dot plot compressing year-end cuts to just one. The market's expectation of two cuts at the start of the year was progressively stripped away. The "Higher for Longer" narrative reasserted its dominance. Previously, the market broadly believed that "the interest rate inflection point was established, and the liquidity inflection point was only a matter of time." However, the developments of Q1 offered a more extreme answer. Not only is the liquidity inflection point far off, but the interest rate inflection point itself faces the risk of being overturned. If Warsh's advocated combination of rate cuts and balance sheet reduction materializes, it would mean that even if nominal rates decline, the actual liquidity environment could actually tighten, and its suppressive effect on risk assets should not be underestimated.

Against this macro backdrop, global risk assets came under broad pressure: the S&P 500 is down over 5% year-to-date, with the Nasdaq declining even more; gold ETFs absorbed over $160 billion in inflows; Bitcoin ETFs saw net outflows of $3.8 billion in February alone. The signal of capital migration from digital gold to physical gold is exceptionally clear. ArkStream Capital will continue to monitor the evolution of rate cut expectations and the geopolitical situation, which are core variables for judging the timing of the subsequent liquidity inflection point.

Bitcoin and Capital Structure: Narrative Falsification, ETF Divergence, and Institutionalization Process

Stress Test for Digital Gold

One of the most notable structural changes of Q1 is the significantly increased correlation between Bitcoin and the Nasdaq index during periods of stress. In market stress tests, Bitcoin not only failed to provide a hedging function but moved almost in lockstep downwards with tech stocks.

From a behavioral finance perspective, this is unsurprising. Since the approval of ETFs, institutional investors have placed Bitcoin within the same risk budget framework as growth tech stocks. When macro risk appetite contracts, deleveraging and reducing positions are systematic actions that do not differentiate by asset class. This jump in correlation marks a new phase in Bitcoin's identity shift during institutionalization: it is evolving from an independent alternative asset into a high-beta subset within global risk asset portfolios.