Bitcoin Encounters Resistance at $79K, $65K-$70K Likely Key Support

- Core Observation: Bitcoin faces strong resistance near the Real Market Price ($79K) and the Short-Term Holder Cost Basis, increasing the medium-term downside bias. Despite easing spot selling pressure and stabilizing institutional inflows, weak demand and record high short positions keep the market in a range-bound consolidation pattern, with the $68K-$70K zone as key support.

- Key Factors:

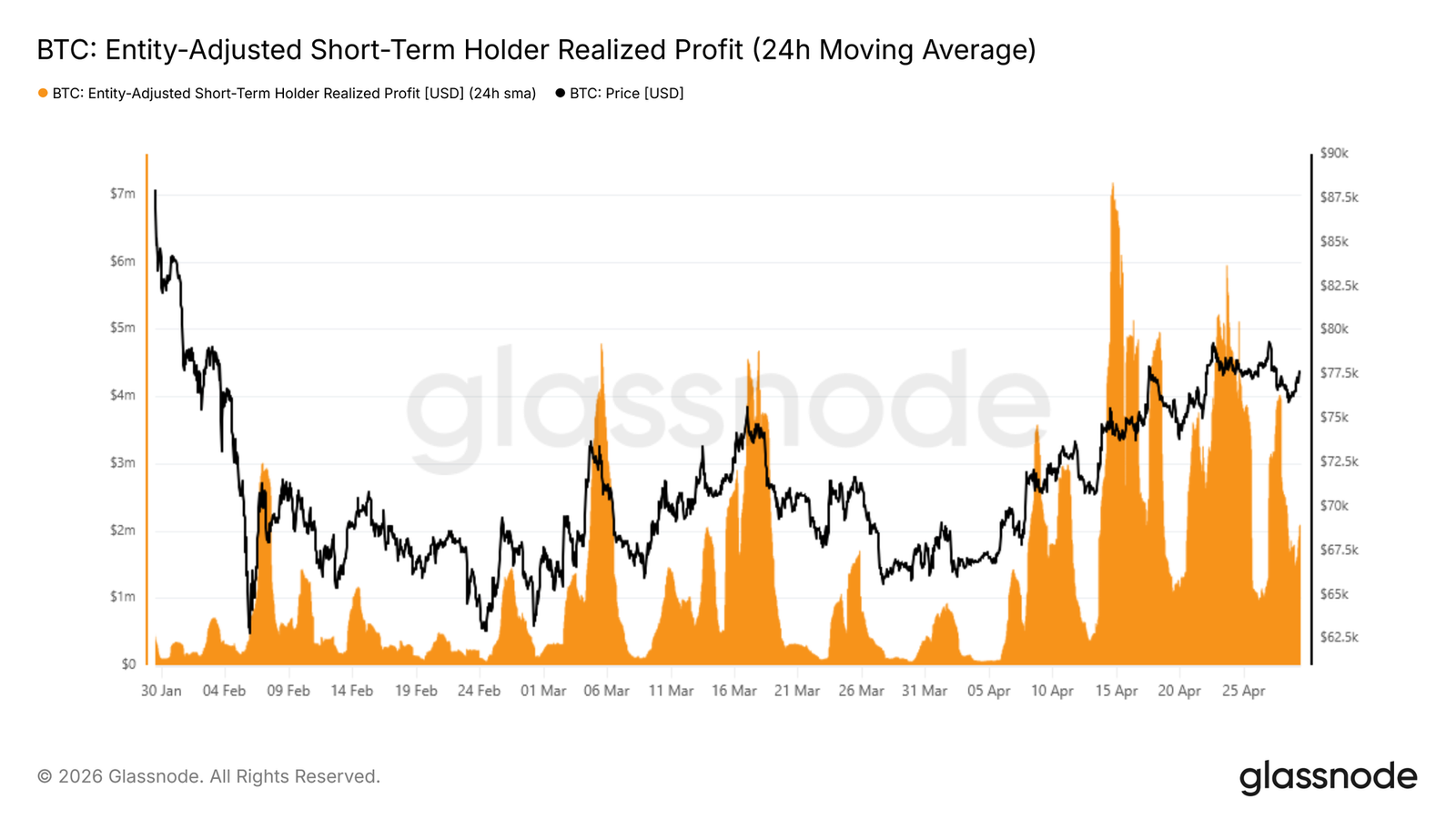

- Price is rejected at the Real Market Price (~$79K) and Short-Term Holder Cost Basis, with STH profit-taking surging to $4 billion per hour, creating substantial selling pressure.

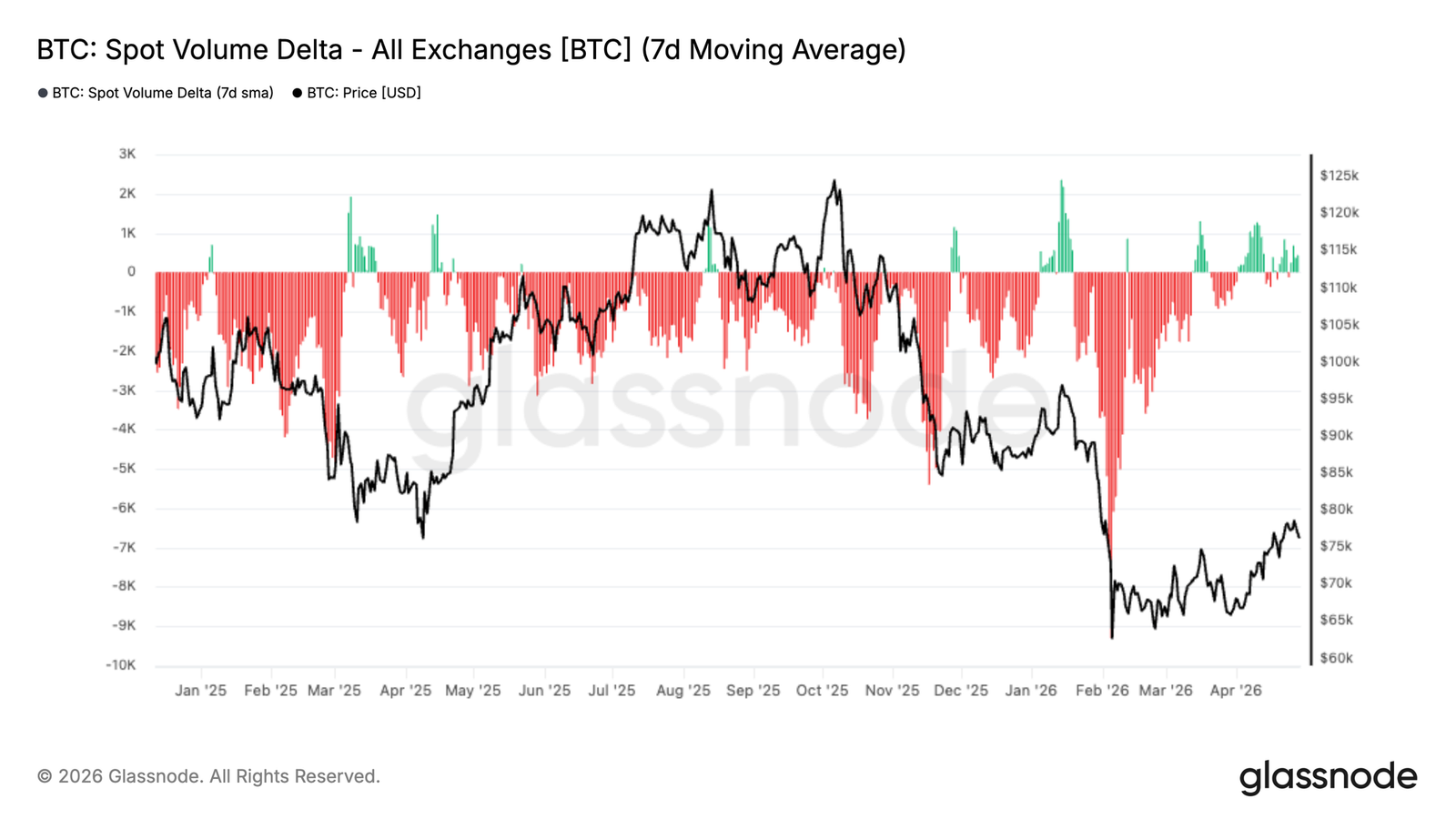

- Spot Volume Delta has recovered from deeply negative levels to near-neutral, indicating reduced selling pressure and renewed buyer interest, but demand has not yet achieved a sustained breakout.

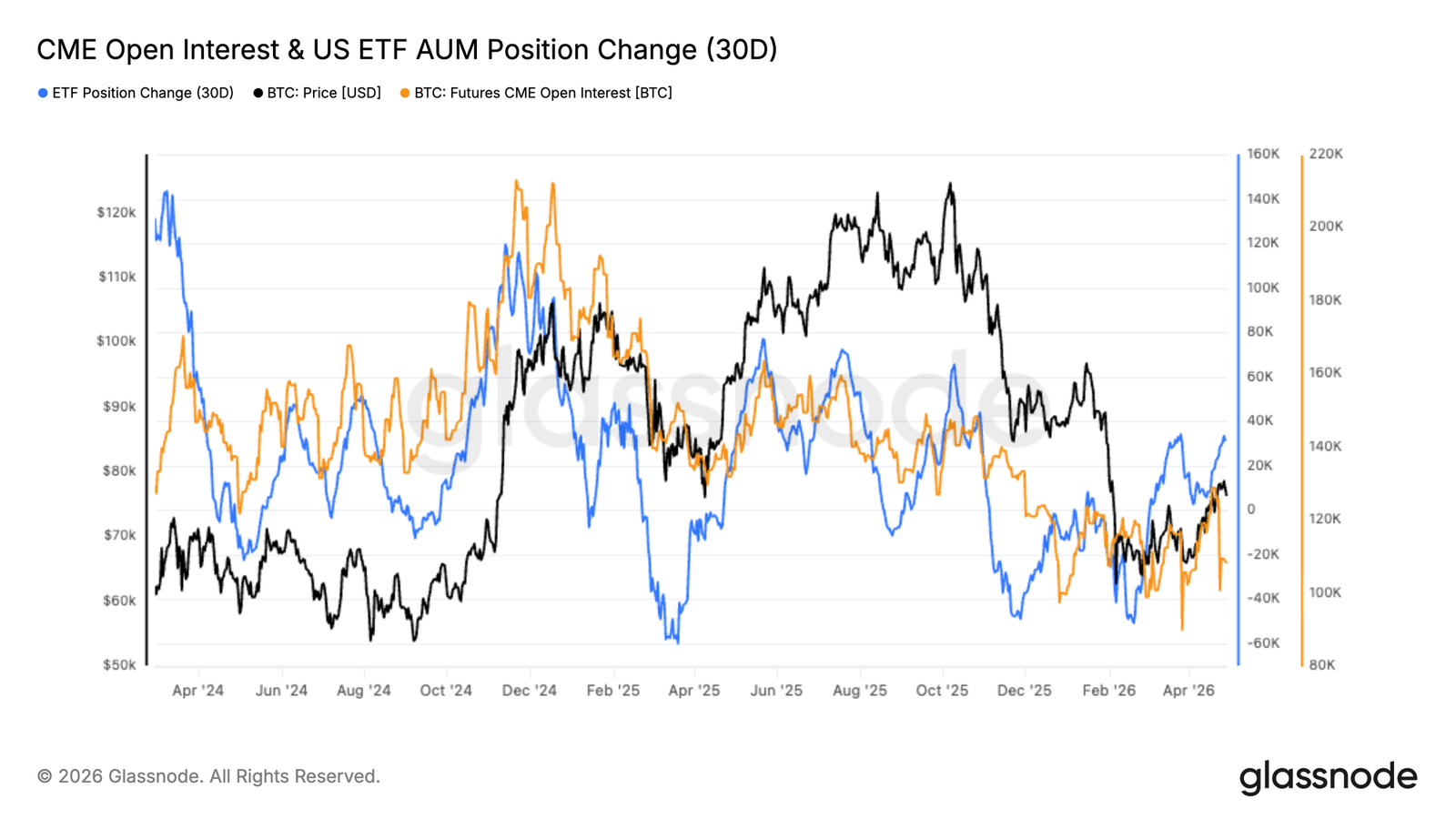

- Institutional positioning shows early signs of recovery: US spot ETF AUM has bounced, and CME open interest is beginning to bottom after persistent outflows.

- Net short positions in the perpetual swap market are at record highs, with extreme discounts reflecting a high degree of hedging and defensive positioning, setting the stage for a potential short squeeze.

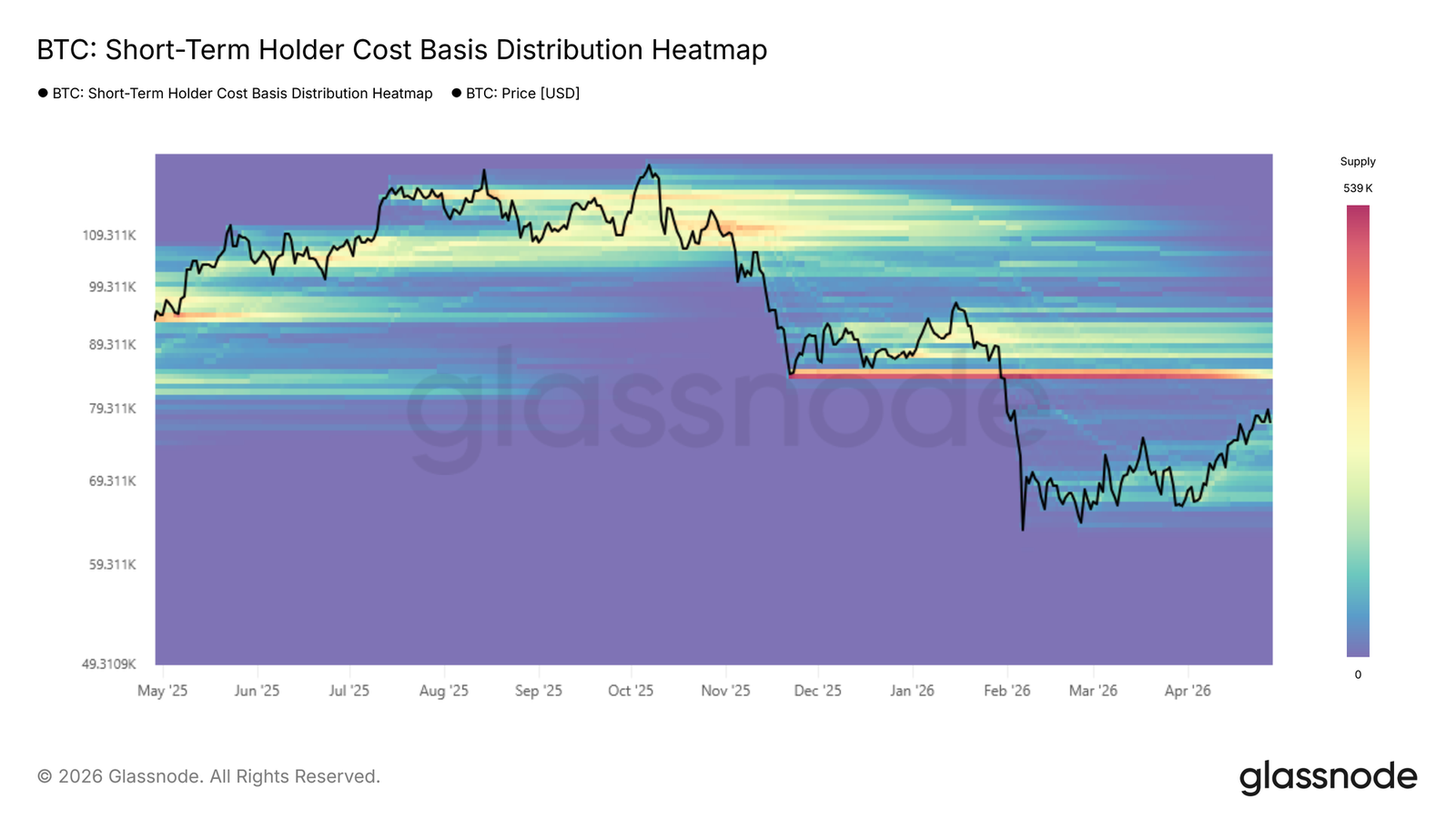

- The dense accumulation cluster formed in the $65K-$70K range provides short-term support, but a breakdown would weaken the market structure; watch the STH Cost Basis -1 Standard Deviation (~$68K).

- Implied volatility continues to compress across all tenors; 1-month realized volatility has dropped to 36, close to implied volatility (38), suggesting market pricing is stabilizing but directional conviction is limited.

- Persistent buying interest at the $80K strike price, combined with negative gamma zones at $76K and $82K above and below, suggests that a breakout above $80K could trigger a sharp upward reaction.

Original Author: Glassnode

Original Translation: AididiaoJP, Foresight News

Bitcoin remains suppressed below the Real Market Price, with support located in the $65k to $70k range. Spot selling pressure is easing, capital flows are stabilizing, but demand remains weak. Heavy short positioning leaves room for a squeeze in a range-bound market.

Summary

- Price rejection at the Real Market Price (~$79k) and Short-Term Holder Cost Basis reinforces a mid-term bearish bias.

- Short-Term Holder realized profit surged to $40 million per hour historically associated with local tops, reflecting significant profit-taking selling pressure that limits rally sustainability.

- A dense accumulation cluster between $65k and $70k provides short-term support, but a breakdown would weaken the short-term structure.

- Spot selling pressure is easing, with volume delta recovering towards neutral and early signs of buyer re-engagement.

- Institutional flows are stabilizing; ETF AUM is rebounding, and CME open interest is bottoming after sustained outflows.

- Perpetual positioning has shifted to a record net short bias, highlighting increased hedging activity and potential for a squeeze.

- Volatility continues to compress; protection demand is rising but conviction is weak, reinforcing a cautious, range-bound environment.

- Realized volatility is closely aligned with implied volatility, confirming a calmer market backdrop with limited directional conviction.

On-Chain Insights

Rejection at Resistance, Focus Shifts to Support

Last week, this report identified the Short-Term Holder Cost Basis and Real Market Price as the most likely resistance zones for the current bear market rally, with profit-taking by recent buyers surging to levels historically consistent with local top formations. Price subsequently rejected precisely in this area, failing to hold above the Real Market Price at $78k and the Short-Term Holder Cost Basis at $79k. This behavior is a textbook pattern in bear markets: price nears the breakeven point of the most price-sensitive cohort, where exit incentives overwhelm growth demand, exhausting upward momentum.

With this rejection confirming overhead resistance, the mid-term bias shifts toward further downside pressure. Attention now turns to the -1 standard deviation level around $68k as the most immediate structural support level to monitor.

Analyzing the Decline

The rejection at the Short-Term Holder Cost Basis wasn't just a price observation; on-chain spending data precisely captures how it unfolded. The 24-hour simple moving average of Short-Term Holder realized profit volume serves as a real-time gauge of how aggressively recent buyers convert unrealized gains into exits.

As price approached $80k, this metric surged to roughly $4 million per hour, approximately four times the baseline level established since mid-April, confirming that Short-Term Holders used the rally as a distribution opportunity. Buyer liquidity was simply insufficient to absorb this wave of profit-taking, capping momentum and triggering the subsequent rejection.

This metric is most useful when analyzing two dimensions simultaneously: the baseline (as a proxy for the broader trajectory of buyer liquidity), and the peaks (which have served as reliable local top indicators during the current bear cycle).

Two Scenarios, One Cluster

Resistance at the Real Market Price and Short-Term Holder Cost Basis reinforces the broader structural weakness characteristic of this bear market. However, the picture is not entirely bearish.

The dense accumulation cluster built between $65k and $70k over the past two months reflects significant buyer conviction at these levels, providing a foundation for a short-term bounce towards the lower edge of the overhead supply cluster around $84k.

Conversely, if the market fails to absorb sustained selling pressure from the Real Market Price region, then this same $65k-$70k accumulation cluster, more specifically the -1 standard deviation level of the Short-Term Holder Cost Basis around $68k, would become the primary support reference for the short-to-medium term. Therefore, the path forward depends on whether buyers within this range can maintain enough conviction to overcome distribution pressure from above.

Off-Chain Insights

Selling Pressure Eases, Buyers Re-emerge

Spot volume delta has spent most of the past few months in deeply negative territory, reflecting sustained net selling pressure on exchanges. This persistent seller dominance aligns with the broader correction, particularly during the sharp drop into the ~$60k-$70k range.

However, recent data shows a clear shift. The 7-day moving average has recovered to near neutral and is beginning to show intermittent positive delta spikes. This indicates that selling pressure is easing while buyers are starting to re-engage at current levels.

From a market structure perspective, this shift is significant. While not yet signaling strong accumulation, the move towards balance suggests improved spot demand and reduced seller urgency. A sustained recovery would require continued expansion into positive territory to confirm buyers are regaining control of the order book.

Institutional Liquidity Rebuilding

Institutional positioning is beginning to stabilize. Both CME open interest and US spot ETF AUM show early signs of recovery after a period of outflows. ETF positioning has rebounded from deeply negative levels, while CME open interest appears to be bottoming, suggesting early re-engagement.

The earlier decline reflected broad risk aversion, with capital exiting both futures and ETF channels simultaneously during the correction. The recent uptick points cautious re-accumulation rather than aggressive positioning.

Sustained inflows will be needed to support a stronger trend. For now, the data suggests early institutional re-entry but not yet full conviction.

Record Short Bias

The directional premium in the perpetual swap market has fallen to its most negative level on record, marking the deepest sustained short bias in this dataset. Unlike short-lived negatives in previous cycles, this move reflects a more persistent defensive posture.

This extreme discount is driven by several factors. Recent price weakness has spurred increased hedging and outright shorting in the perpetual market, while the liquidation of previously crowded longs accelerated the move via deleveraging. Meanwhile, subdued spot demand and soft ETF flows reduced natural buying pressure, allowing derivatives to dominate short-term price action.

Historically, such extremes have occurred during periods of high uncertainty and often precede turning points. While near-term uncertainty remains, the market is increasingly positioned for a potential squeeze if sentiment or spot demand improves.

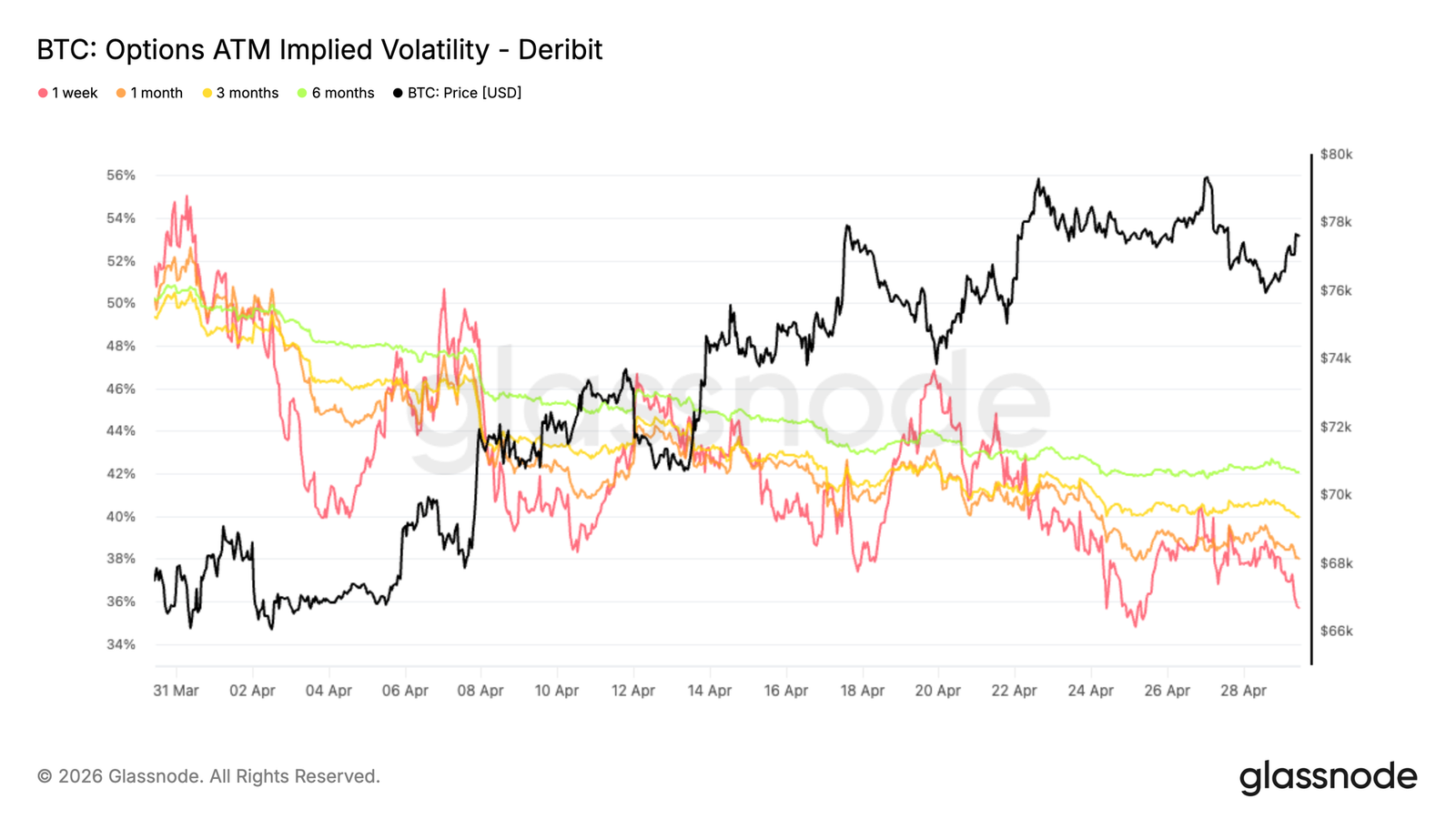

Implied Volatility Declines Across the Curve

Looking at April starting with implied volatility, the dominant theme was broad compression across all tenors.

The 1-week at-the-money volatility fell by approximately 16 percentage points, while the 6-month tenor declined by roughly 8 percentage points. Other tenors fall within this range, averaging a decline of about 10 vol points.

The curve remains in contango, meaning longer-dated options still trade at a premium to shorter-dated ones, but at lower levels. This reflects market pricing for a more stable environment ahead.

Lower implied volatility reduces the cost of options, particularly upside calls. At the same time, protection demand appears to have eased. Traders are no longer willing to pay a high premium for volatility exposure, which aligns with the recent price recovery pointing to expectation normalization rather than conviction accumulation.

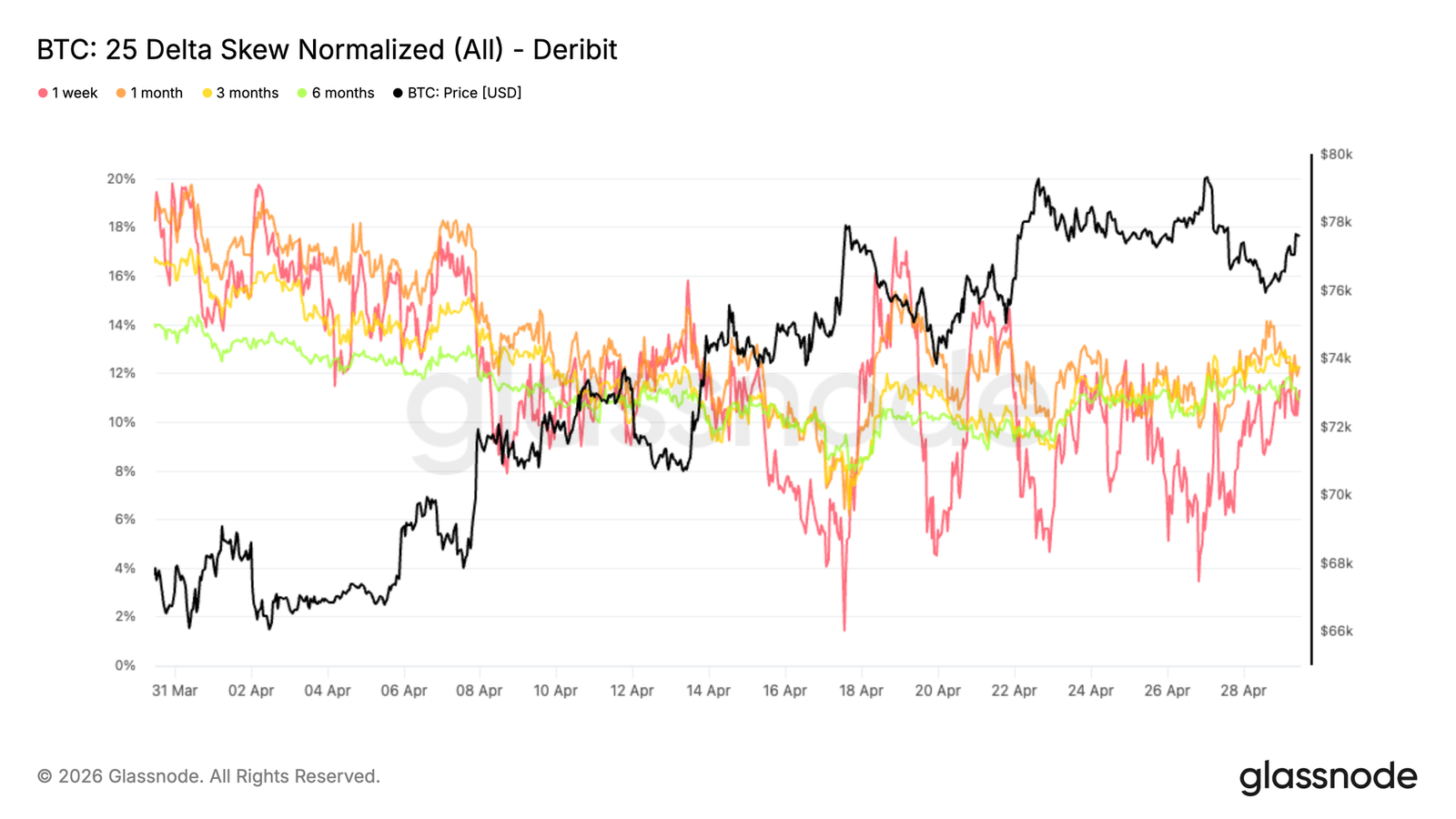

25-Delta Skew Trends Lower, But Protection Remains

As implied volatility compressed, the skew shows how protection demand evolved in April. The broader trend is a steady decline in put premiums, with 1-month skew falling from around 18% to 12%. This reflects a notable reduction in demand for downside protection as conditions stabilized.

At the short end, the 1-week skew reacted more violently, with several spikes towards neutral (2%-4%) at various points in April. These moves were primarily tactical, as pullbacks were used to buy calls and sell downside, temporarily flattening the skew.

More recently, as price approached the $80k resistance, put demand picked up again, pushing skew across tenors back into the 11%-12% range. Protection remains, with the market making tactical adjustments at the short end while maintaining a cautious stance further out the curve.

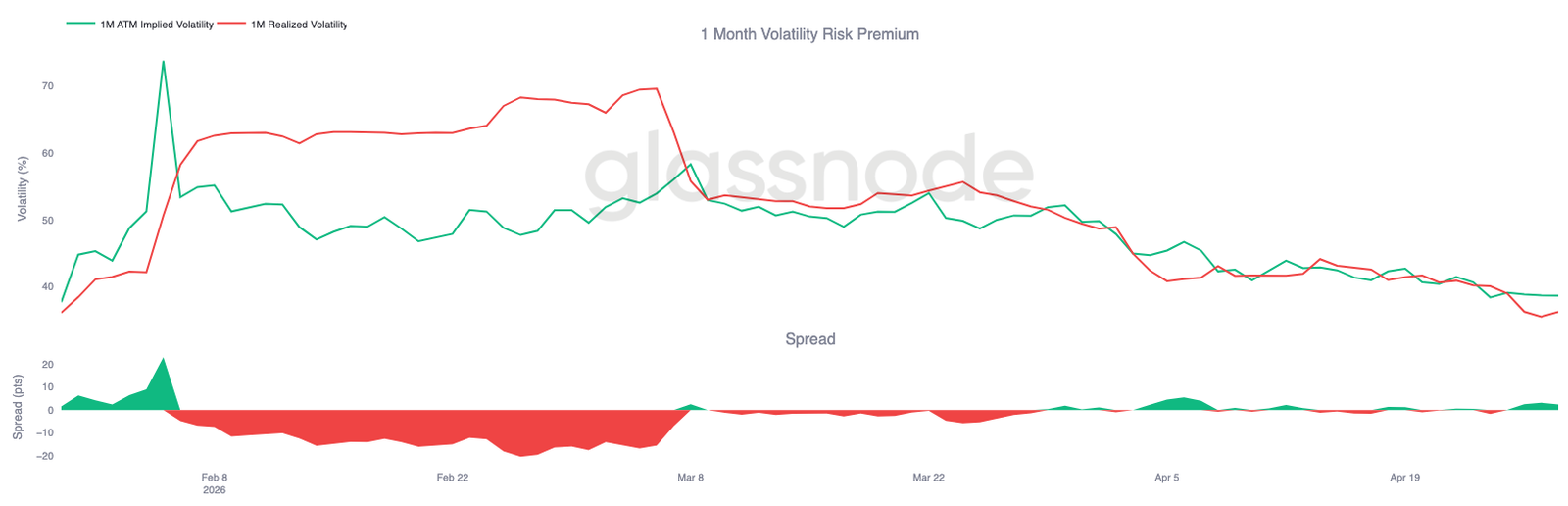

Realized Volatility Confirms Downward Shift

As implied volatility continues to compress, realized volatility has also moved in the same direction and reinforces the trend. Bitcoin's realized volatility has steadily declined. This is significant because realized volatility anchors how options should be priced. When realized volatility falls, it naturally pulls implied volatility lower, as the need to price large price swings diminishes.

This creates a feedback loop: cheaper options reduce the urgency to hedge, leading to less hedge-driven price movement.

The 1-month realized volatility sits around 36, while implied volatility is near 38, leaving only a small premium for volatility sellers to assume risk.

The current environment reflects a shift from stress towards a more balanced state. Volatility is no longer being aggressively bought, and the market appears comfortable with the expectation of a narrower range for future price swings.

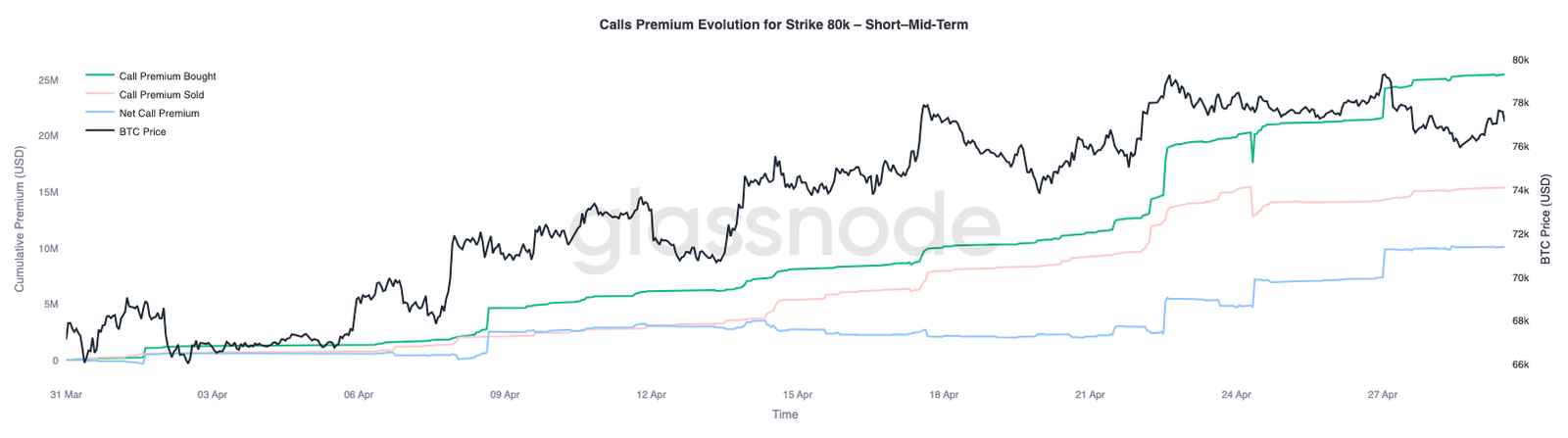

$80k Strike Premium Accumulation Becomes Key Pivot Point

With volatility and skew both easing, positioning becomes the next layer to monitor, with the $80k level emerging as the next key focal point.

Short and medium-term tenors show consistent buying at the $80k strike, indicating growing interest in exposure above this level. This suggests traders are positioning for a test of resistance rather than shorting into it.

Meanwhile, two key negative gamma zones stand out: $76k on the downside and $82k on the upside. These levels could become areas where hedging flows amplify price action, especially in low-liquidity environments.

A break above $80k would bring spot closer to the $82k area, where negative gamma could force market makers to buy strength, reinforcing the move. Positioning remains cautious, but it is increasingly set up for a more violent upside reaction if resistance is cleared.

Conclusion

In summary, the market remains trapped below key resistance, with the Real Market Price continuously capping upside attempts while the support cluster near $65k-$70k provides a floor. Spot selling pressure is beginning to ease, and early signs of institutional re-engagement are appearing, but demand has yet to show the strength needed for a sustained breakout.

Meanwhile, derivatives positioning has turned decisively bearish, with record net short exposure and elevated protection demand reflecting a defensive mindset. This leaves the market in a finely balanced state. While positioning weights tilts toward caution, it also leaves room for sharp upside dislocations if capital flows turn.

Until a clear expansion in spot demand or institutional inflows emerges, the most likely outcome remains a choppy, range-bound environment. The next directional move will likely not be driven by positioning alone, but will depend on whether real capital steps in to absorb supply and reclaim higher levels.