IOSG:SpaceX上場当日、3つの永久メカニズムの初めての実地テスト

- 核心的な見解:IPO前永久契約は、オンチェーンでの価格発見メカニズムを通じて、一般投資家にSpaceXなどの未上場企業に対する上場前の方向性のある投資機会を提供し、伝統的な市場の時間外取引の空白を埋める。しかし、株式分割などのコーポレートアクションの処理に関しては、深刻な未解決リスクが存在する。

- 重要な要素:

- IPO前永久契約は、現物価格がないという価格決定の難題を解決する。内部オラクルと価格レンジを通じて、市場が外部の参照価格がない状態で自ら価格を発見することを可能にし、Cerebrasの初値予測誤差を1.3%以内に抑えた。

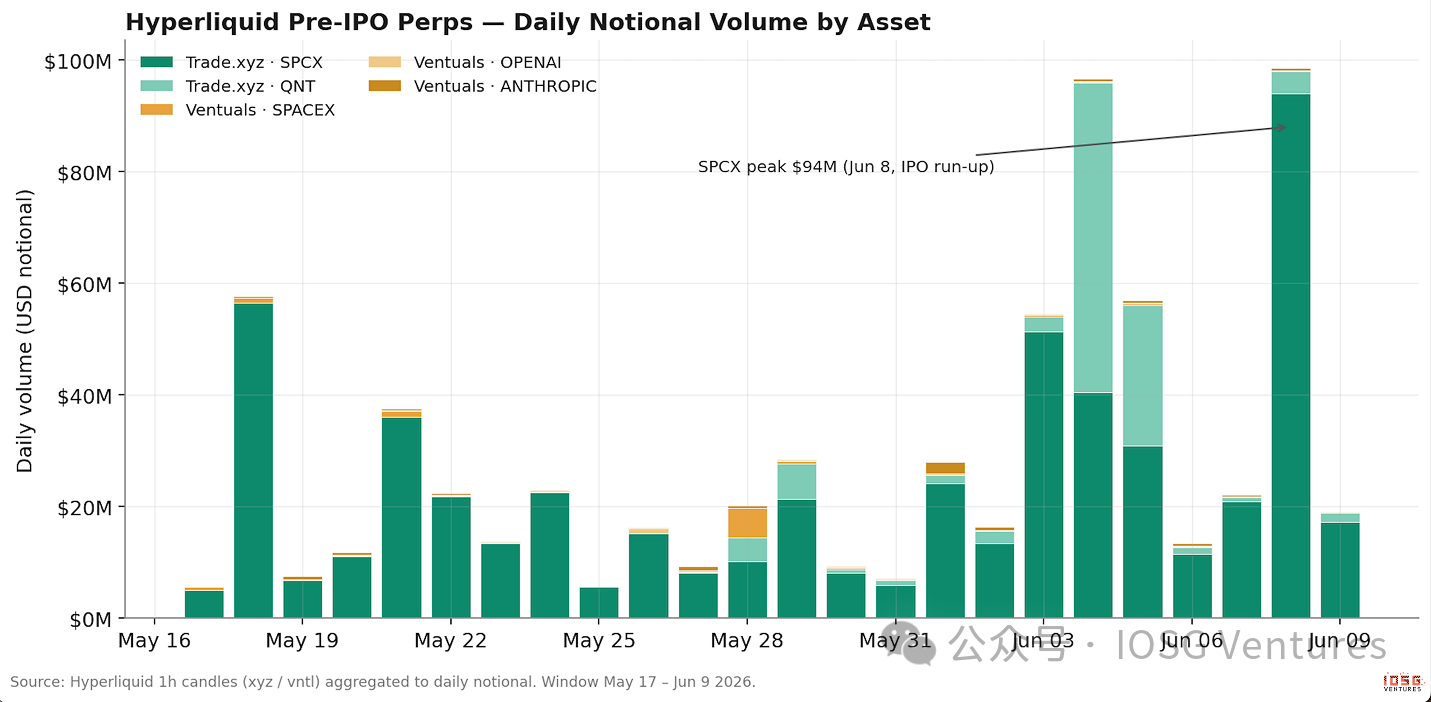

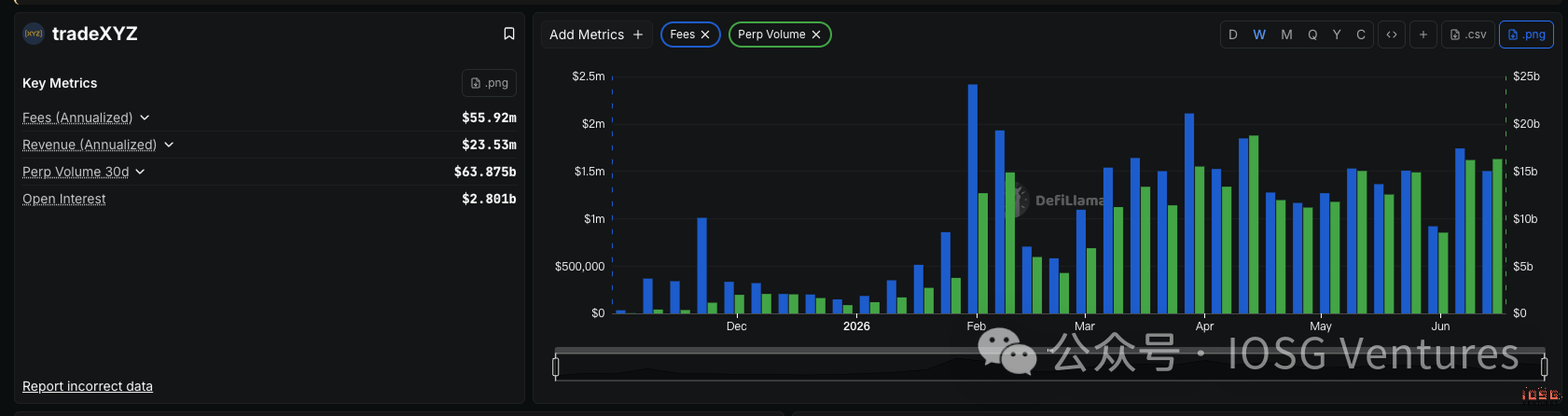

- この市場の出来高は現在、伝統的な金融の永久契約の出来高の約1%に過ぎず、大きな成長余地がある。大手プロジェクトであるTrade.xyzは、ほぼゼロの資金調達コストとIPOのタイミングを活かし、オンチェーン出来高の約96.5%を占めている。

- ポジション保有コストの違いが出来高の二極化の鍵である。Trade.xyzのほぼゼロの手数料により、市場は長期保有が可能となる一方、競合のVentualsの高額手数料(年率45%)は、累積コストで約350倍もの差を生み出している。

- コーポレートアクションの処理が最大の弱点である:Trade.xyzには分割リベースメカニズムがなく、Ventualsは単一のデータソースが期限切れの分割データを参照したことで市場が45%暴落した。リスクは、標準化されたオンチェーンイベント処理レイヤーの欠如に集中している。

Original Author: Mario Chow

Original Source: IOSG Ventures

TL;DR

- Why is Pre-IPO perpetual important? It pries open two doors that were previously shut to almost everyone: firstly, betting on the direction of private companies like SpaceX and OpenAI *before* their IPO, and secondly, obtaining a real-time price during nights, weekends, and pre-market hours when stock markets are closed but news continues to move prices. Now, anyone with a wallet can place this bet, continuously, permissionlessly, just in time for the biggest wave of IPOs in history.

- Without a public spot price, how do you price something? This is the core challenge for the entire asset class. With no external price to copy (which can sometimes be months), exchanges must rely on their own order books to generate a price, changing it only when real capital is willing to trade at a deviation: slow and expensive to fake. trade.xyz uses an internal oracle plus a price range, while Ventuals partially relies on primary market data. Surprisingly, this works: the perpetual predicted Cerebras' opening price within 1.3%, and even priced crude oil over a weekend when traditional venues were completely down.

- What worked in the SpaceX case? trade.xyz captured the on-chain market (~96.5% of volume), not because its oracle is smarter, but because near-zero funding rates make holding the position almost costless, it launched *pacing* the IPO catalyst, and its per-share pricing enabled cross-exchange arbitrage. The transition from synthetic perpetual to tracking the spot on the listing day, June 12th, was clean: no oracle gap, no liquidation cascade. On the listing day, the perp closely tracked the Nasdaq real-time price, within 1% (approx. $152 vs. a $150 match price); its pre-market mark price also landed right on Nasdaq's indicative opening price (approx. $175), while the final match price cleared lower at $150.

- What risks remain unresolved? This asset class excels at handling price but remains primitive at handling events. Corporate actions, especially a post-conversion stock split, have no pipeline on-chain: trade.xyz has no published rebase mechanism, while Ventuals outsources this to a single data provider, which has already failed once (an expired split data caused its market to flash crash 45%). The bottleneck isn't price discovery, but the mundane "corporate action" processing layer: traditional markets took a century to standardize it, but no one has rebuilt it on-chain. Whoever can reliably deliver it fills the last gap between these markets and the ones they aim to replace.

Background: The Two Locked Doors Crypto Just Kicked Open

Pre-IPO perpetuals sit at the intersection of two things that, until recently, were almost entirely inaccessible. Now, the crypto rails have pried both doors open.

First Door: Pre-IPO Exposure, Finally Open to Retail

Pre-IPO shares of SpaceX or OpenAI were only accessible to accredited investors, VCs, and a few secondary desks, with opaque valuations re-priced only during funding rounds. Pre-IPO perpetuals have torn down this wall. With just a wallet, anyone can bet on the direction of a private company's valuation, anytime, permissionlessly, without touching any shares, quotas, or voting rights. The timing is impeccable, coinciding with the largest wave of IPOs in history. SpaceX listed on Nasdaq on June 12th at an ~$1.77T valuation, with OpenAI and Anthropic expected to follow. For the first time, retail can position before the opening bell, rather than chasing prices post-IPO.

Second Door: After-Hours Trading, Now Taken Over by Crypto

Traditional exchanges still keep "banker's hours". Stocks and futures are completely halted overnight, on weekends, and holidays. When news breaks after hours, there's nowhere to hedge real risk. Crypto never closes. This time gap hands the entire after-hours window to crypto, and most price discovery now happens on Hyperliquid.

A key premise of this report is: the after-hours quote is not random guessing; it often lands exactly where the real market reopens. One Saturday, Middle East conflict drove up oil prices, and Hyperliquid was the only market trading; when CME crude oil futures reopened Sunday evening, the opening price was exactly what Hyperliquid perps had discovered. TD Securities estimates that this platform absorbed ~80% of the recent oil price move before traditional exchanges even opened. The same applies to stocks: trade.xyz's Cerebras perpetual tracked within ~1.3% of Nasdaq's final opening price. During after-hours, the perpetual contract itself *is* the market.

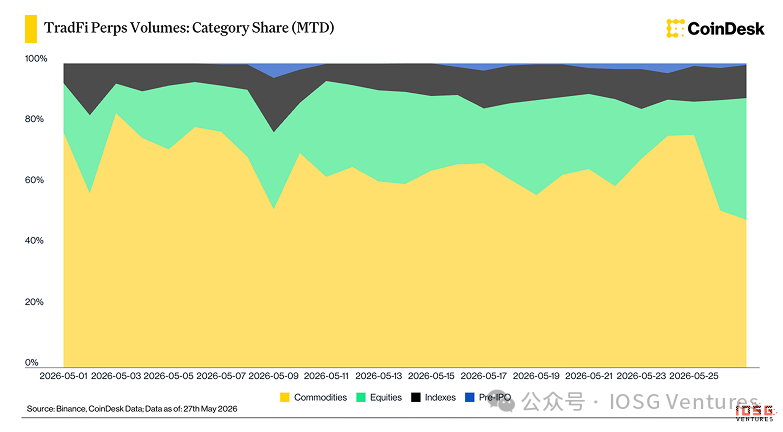

How Early Are We? Only ~1% of TradFi Perpetual Volume

CoinDesk data shows how nascent this market is. On Binance and similar platforms, TradFi perpetuals are dominated by commodities and stocks. Pre-IPO is just the thin top slice of the stack, accounting for just over 1% of total TradFi perpetual volume since its launch around May 21st.

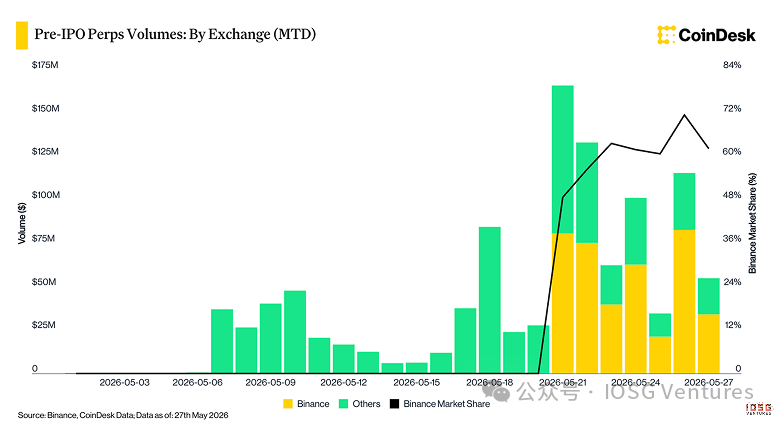

On Binance, Pre-IPO volume is equally concentrated: SpaceX accounts for ~79%, OpenAI 11%, and Anthropic 9%. This asset class launched around May 20th, and Binance quickly captured over 60% of its share. Pre-IPO on CEXs is still embryonic, dominated by SpaceX. The truly interesting activity is on-chain.

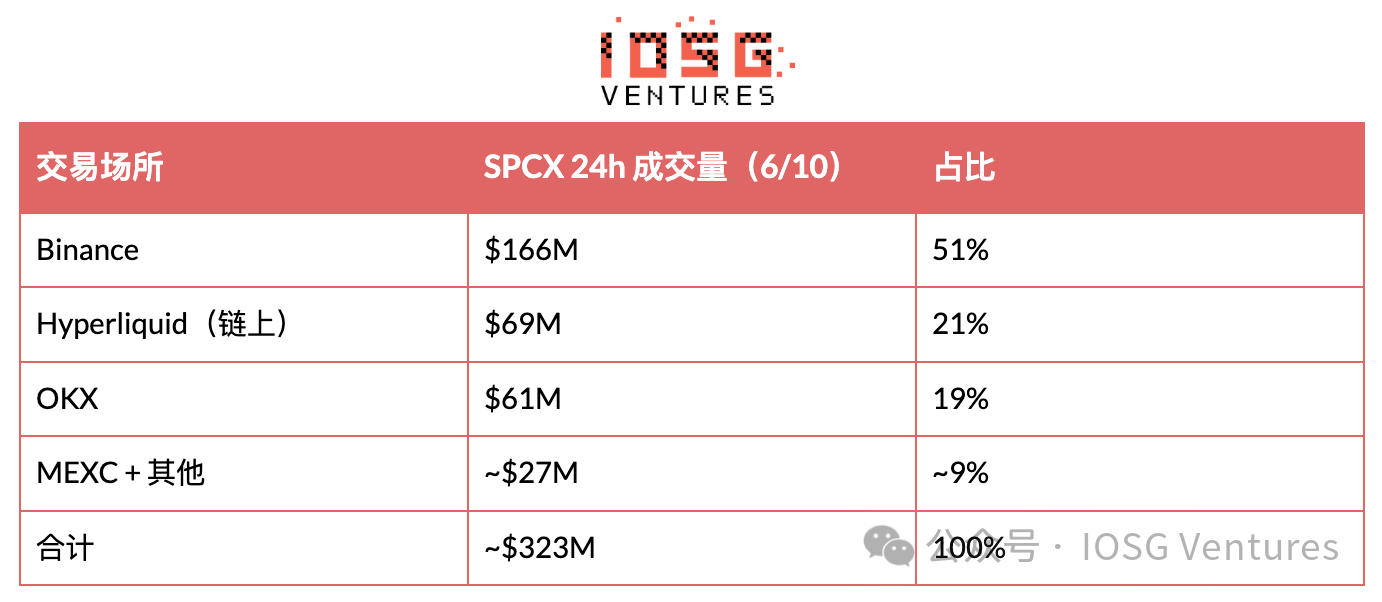

SPCX Landscape Across Venues: Binance Leads, Hyperliquid Holds On-Chain Home Turf

Market Snapshot on June 10th

Focusing on SpaceX, it *is* the Pre-IPO market. In this snapshot from June 10th, total 24-hour volume for SPCX perpetuals across all venues was ~$323M. Binance led with $166M (51%), followed by Hyperliquid with $69M (21%), OKX with $61M (19%), then MEXC and smaller venues.

On-Chain Landscape: A Market with Essentially One Builder

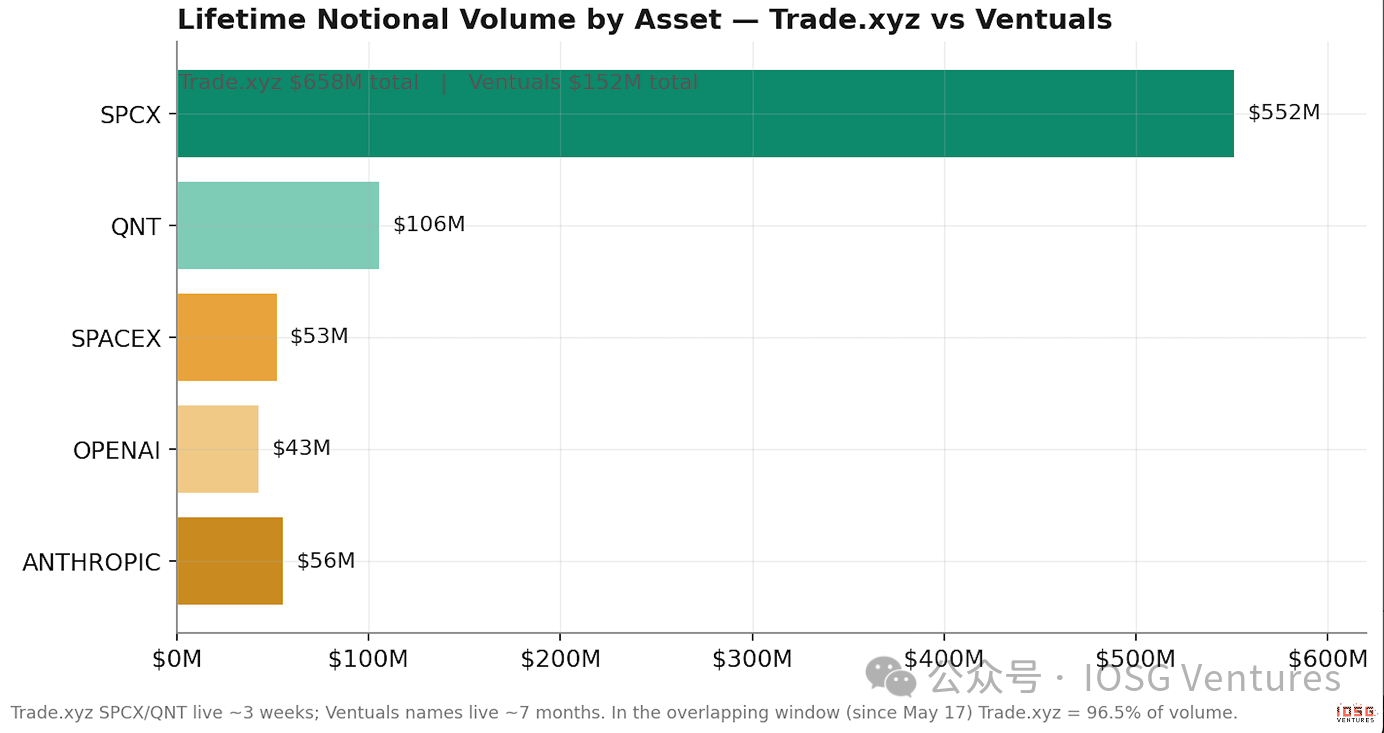

Data Comparison: Trade.xyz vs. Ventuals - 96.5% to 3.5%

Trade.xyz's cumulative volume is ~$658M, with SPCX at $552M and its second ticker QNT at $106M, all crammed into about three weeks. Ventuals' cumulative volume is ~$152M, spread more evenly across SPACEX ($53M), OPENAI ($43M), and ANTHROPIC ($56M) over about seven months.

Placing them on the same timeline, the gap is stark. During the overlapping window after SPCX launched, trade.xyz accounted for ~96.5% of on-chain Pre-IPO volume, consistent with third-party trackers estimating it at "approximately 95% of the Hyperliquid Pre-IPO basket." Ventuals lists more tickers, including the only currently live Anthropic and OpenAI contracts, but captures only a tiny fraction of flow. Listings aren't a moat; liquidity is.

HIP-3: The Platform Layer Underpinning This

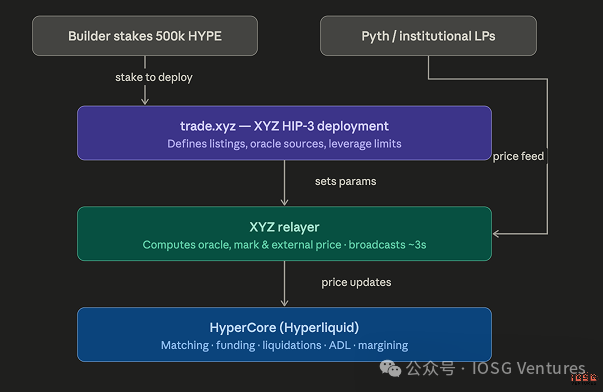

HIP-3 is a Hyperliquid upgrade that transformed the single perpetual venue into a platform for builders to deploy perpetual DEXs. Any team staking 500,000 HYPE tokens can deploy their own perpetual market on Hyperliquid's matching engine, HyperCore. Builders control listings, oracles, leverage limits, and contract parameters; HyperCore controls execution, funding rates, liquidations, and margin. Trade.xyz is a HIP-3 deployment focused on traditional assets: turning stocks, indices, and commodities into 24/7 perpetual contracts, margined and settled in USDC, cross-margining only.

How Trade.xyz Prices a Market Without External Truth

Let's start with the problem, because only by feeling the problem does the design make sense. Normal perpetuals copy a real-time spot price from an exchange; Pre-IPO perpetuals have no spot price to copy and may not have one for months. So the venue must use its only tool, its own order book, to create a credible price, and make it expensive to manipulate. This section answers one question: How do you price an asset when it doesn't have a price yet?

Two Oracle Mechanisms for After-Hours Stock Perpetuals

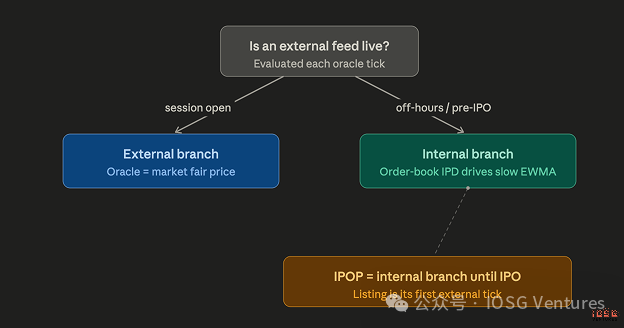

To understand Pre-IPO perpetuals, first understand after-hours stock perpetuals. Crypto perpetuals have real-time external prices around the clock; stocks don't. AAPL only has a real market price during US trading hours. So the oracle feeding the mark price and funding rate needs two mechanisms: one when external data is available, another when it's not. When external markets are open, a relayer directly feeds an institutional fair value (sources include Pyth) as the oracle. When closed, the oracle must continue using the perpetual's own order book. This is where the design gets sophisticated.

Internal Oracle: Three Core Ideas

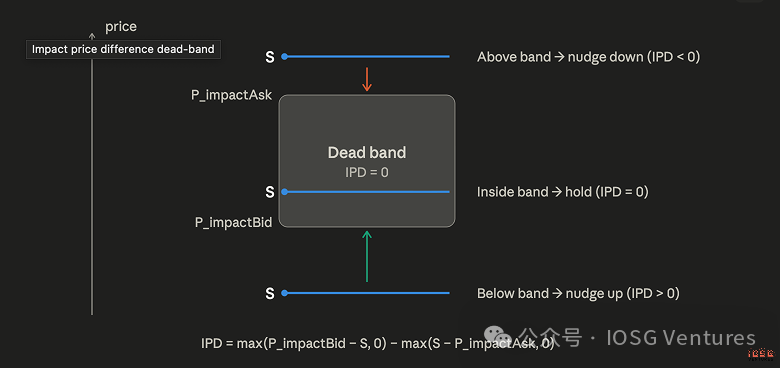

Look at the executable order book.

The relayer calculates the average execution price of pushing a fixed $1,000 order into each side of the order book, yielding an executable bid and ask price. If the current oracle price falls within this range, nothing happens—the order book and oracle are aligned, the oracle stays put. Only when the oracle price falls outside this range, meaning real depth is willing to trade at a deviation, does the oracle move towards the order book. Heavy buying pressure pulls it up, heavy selling pressure pushes it down; noise within the range is completely ignored. To move this oracle, you must deploy real liquidity, not just print trades.

The oracle never jumps.

It converges slowly towards the order book with a thirty-minute time constant, and a hard cap ensures each update can only close about 9.5% of the remaining distance, regardless of time elapsed since the last update. Trading halts and irregular updates cannot cause it to gap.

The mark price is the median.

The mark price, which drives margin and liquidations, is the median of three candidates: the oracle itself, the oracle plus a short-term moving average of the perpetual's basis, and the order book snapshot (best bid, best ask, last price). The median structure means the fast variable alone can never drag the mark price too far from the slow oracle. Hourly funding rates then push the market back towards the oracle, with standard multipliers and caps ensuring any single hour's payment is small.

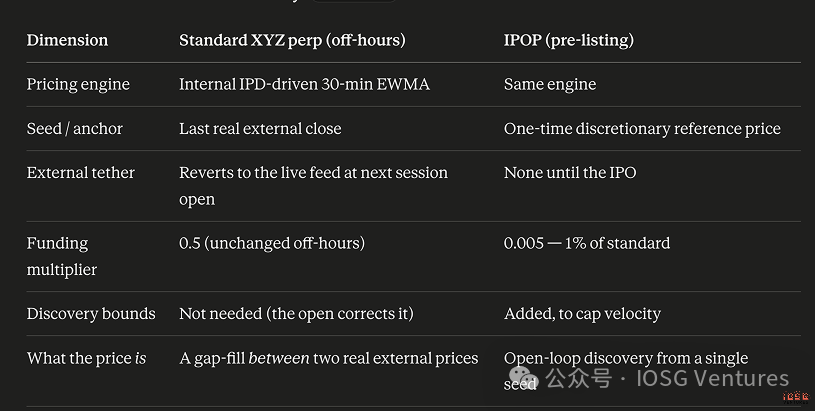

Pre-IPO Perpetuals: Same Engine, Three Modifications

IPOP (Pre-IPO Perpetuals) are essentially after-hours stock perpetuals that never get a "Friday close" to rely on. Before listing, there is no external price, so the market must run its internal pricing mechanism continuously, sometimes for months. Trade.xyz made three changes, each revealing the essence of the problem.

- The funding rate is slashed to 1% of the standard rate. Weekend perpetuals can drift at most two days and get corrected on Monday's open, so normal funding is tolerable. IPOP can trade for over sixty days without any anchor, and markets tend to settle into persistent premiums or discounts reflecting pure sentiment. Under standard rates, anyone positioning against the prevailing sentiment would be drained by funding long before the IPO arrives. Slashing the multiplier to near zero makes this contract truly holdable. Our view: more than any oracle ingenuity, it's this single parameter that made trade.xyz's product tradeable; the funding data later in this report confirms it.

- Initial seed price. Weekend markets initialize with the last real external price. IPOP has no history, so trade.xyz sets an initial reference price. It's not a prediction, just a mathematical starting point. For SPCX (launched late UTC on May 17th), the reference price was set at $150 per share: the midpoint of SpaceX's publicly reported $1.75T–$2T target valuation, divided by an assumed 11.87 billion fully diluted shares.

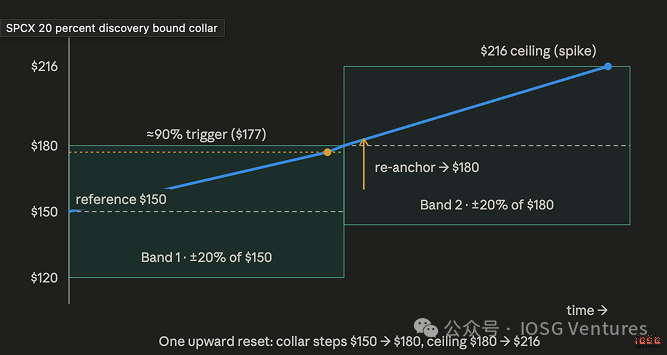

- Discovery bound. A price collar around the reference price that the mark price cannot breach, with a rule that positions with a liquidation price currently outside the collar will not be liquidated while the collar is active.

For 5x leverage SPCX, the collar width is ±20%. A static collar would either freeze price or be meaningless, so this collar is stair-stepped: when the slow oracle climbs to within 90% of the upper bound, the reference price re-anchors to that upper bound, and a new ±20% collar opens around it.

SPCX has seven such steps in each direction. Compounding them, the contract's hard lifetime range from the $150 seed price is approximately $25 to $645 per share.

The Cost to Manipulate This Market: Expensive, Obvious, Slow

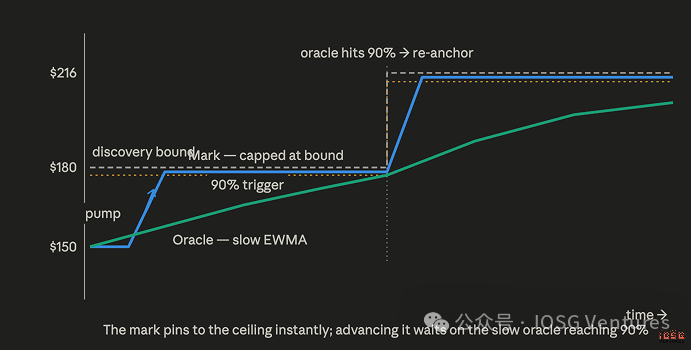

This division of labor is crucial for anyone trying to manipulate. The mark price reacts fast but has a hard ceiling; a pump can quickly hit the ceiling and then freeze there.

The oracle is a thirty-minute slow average; it's the gatekeeper. Only when the oracle touches the 90% trigger line does the step move up. To push the price up one step, an attacker must hold the entire order book elevated against arbitrageurs for nearly an hour, then repeat for the next step. Expensive, obvious, slow. That's the design intent, and so far, it has held up robustly.

Two Builders: Trade.xyz vs. Ventuals

Ventuals: Partially Trusting External Data

Pre-IPO perpetuals on Hyperliquid come from two HIP-3 builders that answer the same question from opposite directions. Trade.xyz trusts its own order book; Ventuals partially trusts external data. Ventuals prices valuations, not share prices: a SPACEX price of 1,989 implies a market-implied company valuation of $1.989T. Its oracle is a weighted blend: one-third from external valuation estimates by Notice.co, two-thirds from a two-hour moving average of Ventuals' own mark price.

Notice aggregates secondary trades, indicative bid/ask quotes, funding announcements, mutual fund valuations, 409A valuations, and public comparable data, polling at least once per minute. That deliberately set one-third weight is Ventuals' answer to the "IPO spike problem": anchor to primary market reality while giving the market mathematical room to price upwards. Also worth noting: two-thirds of this oracle is Ventuals' own market, making this design far more self-referential than its marketing suggests.

Its manipulation resistance is built on the price path, not stair-stepped collars. Orders cannot deviate more than 20% from the oracle, enforced by the matching engine. The mark price updates every three seconds, with a maximum change of 1% per update. Once the short-term shock price deviates more than 2% from its one-minute average, the mark price's update coefficient immediately drops to zero, so sudden volatility must persist for the mark price to follow. Funding rates are dynamic: ~15% annualized when the market is close to the oracle, rising exponentially with divergence, approaching ~1% per hour near the collar's edge.

The endgame design is also completely different. When a company lists, the Ventuals market settles and stops: funding goes to zero, the mark price is forcibly rewritten to the valuation implied by the first-day closing price, and all positions are force-closed. It's more like a prediction market betting on the first-day close than a perpetual. Trade.xyz's IPOP directly converts to a regular stock perpetual and continues trading