Hyperliquid盤前契約論争:「約束のSpaceX株式資本、なぜ無効になったのか?」

- コア見解: Hyperliquidエコシステム内の市場TradeXYZは、自社のSpaceX盤前契約SPCXに関して株式資本のリベース(Rebase)を実施しないことを正式に確認した。その価格設定は、市場によるA類普通株1株当たりの想定価格にのみ基づいており、会社の総株式資本や時価総額とは無関係である。以前の文書に記載されていた「118.7億株」は、あくまで教育目的の例示であった。

- 重要な要素:

- TradeXYZは、自社の盤前契約が想定株価を追跡する永久契約であり、総株式資本や時価総額は入力パラメータではないと説明した。

- 以前の文書に登場した「118.7億株」という数字は、公式には教育目的の例示と説明され、誤解を招くとして削除された。

- TradeXYZは、今後SPCXおよび全市場において、総株式資本や時価総額に基づく計算基準を一切使用、公表、依存しないことを確認した。

- SPCXは、SpaceXのIPO後に標準的な外部オラクルによる価格設定に移行することが見込まれ、価格は公開市場の取引価格に徐々に収束する。

- コミュニティの論争の核心は、ユーザーが「118.7億株」を商品ルールとして受け入れていた中で、公式の説明が変更されたことによる透明性と期待管理への疑問である。

- バイナンスなどの競合プラットフォームは、類似の契約に対して株式資本を130.8億株に調整するリベースを実施しており、プラットフォーム間の商品ロジックの違いが浮き彫りになっている。

Original: Odaily Planet Daily (@OdailyChina)

Author: Azuma (@Azuma_eth)

Yesterday, Odaily Planet Daily published an article analyzing the reasons behind the huge price differences in SpaceX pre-listing contracts on platforms such as Binance, OKX, and Hyperliquid. It is recommended to first read "Why are the price differences so large for SpaceX pre-listing contracts across exchanges?".

The article mentioned that when Hyperliquid launched the SpaceX pre-listing contract SPCX via its in-house HIP-3 marketplace TradeXYZ, it previously disclosed a share count of approximately 11.87 billion shares in its documentation. However, that statement was later removed, sparking community speculation about whether the market would subsequently undergo a Rebase.

- Odaily Note: A so-called Rebase refers to adjusting the share data and corresponding position status based on real-world conditions. For example, on the evening of June 8, Binance announced that it would perform a Rebase on its pre-listing contract SPCX, adjusting the share count from the estimated 11.87 billion shares to 13.08 billion shares as disclosed in the latest IPO plan.

TradeXYZ Confirms: No Rebase!

Today, TradeXYZ officially responded to this matter.

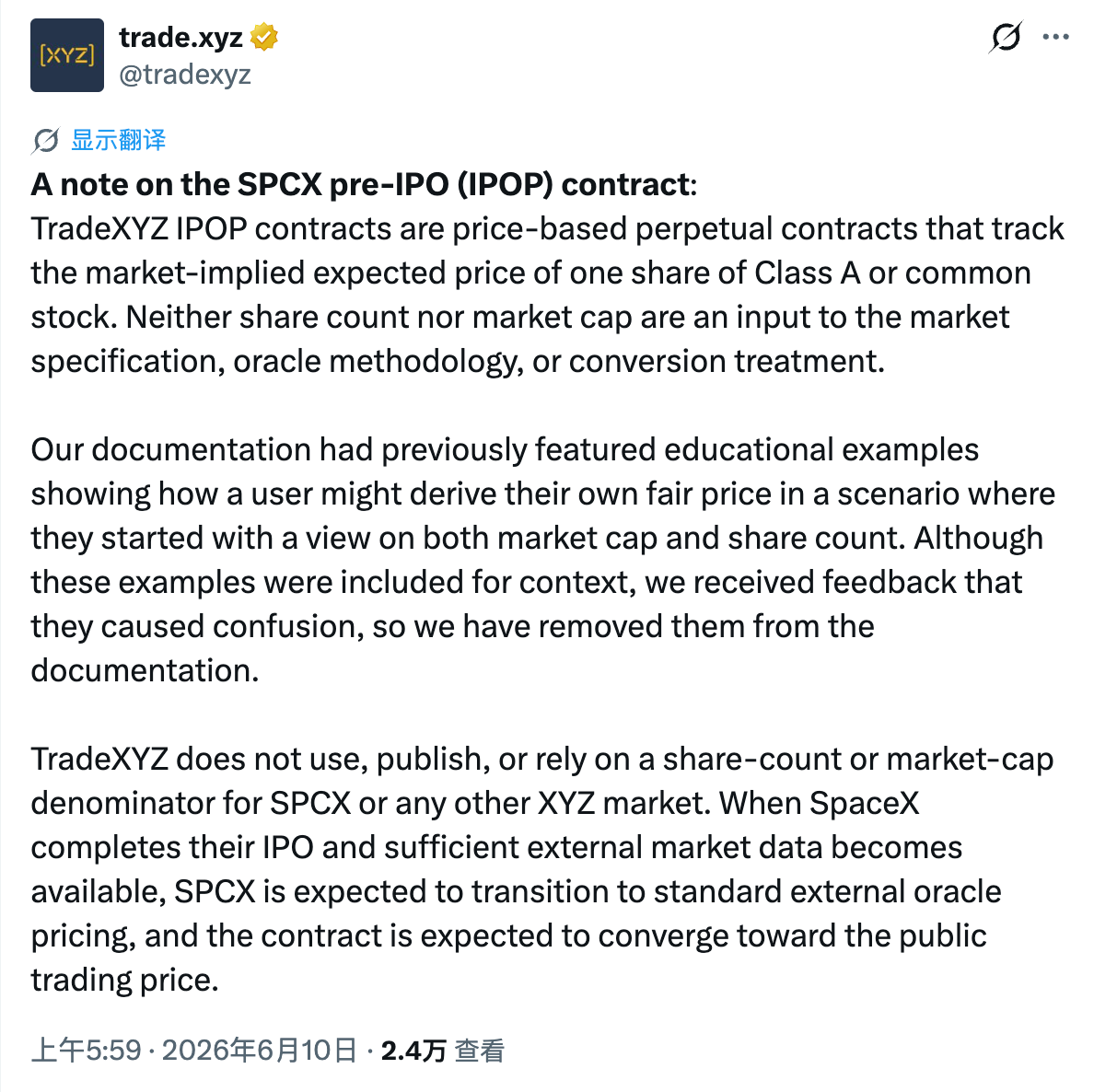

TradeXYZ stated that its pre-listing contracts, including SPCX, are price-based perpetual contracts that track the market's implied expected price per share of Class A common stock (or common stock). The total share count and the company's market capitalization are not input parameters in the market's rules, the oracle pricing methodology, or the final conversion mechanism.

As for the "11.87 billion shares" figure that previously appeared in the documentation, TradeXYZ explained that the official documents previously contained some educational examples illustrating how users, with their own expectations for the company's market cap and total shares, could derive a "reasonable stock price." These examples were only intended to help contextualize the background. However, the team received feedback that this content could easily cause misunderstanding, and therefore it has been removed from the documents.

To clarify, TradeXYZ confirms that it will not use, publish, or rely on any calculation benchmarks based on total shares or market capitalization for SPCX or any other XYZ markets in the future. Once SpaceX completes its IPO and sufficient external price data becomes available in the market, SPCX is expected to transition to the standard external oracle pricing mechanism. At that point, the contract price is expected to gradually converge towards SpaceX's public market trading price post-listing.

In simple terms, TradeXYZ has confirmed it will not conduct a Rebase to correct the share data. As for the previously mentioned "11.87 billion shares," it was just an example – don't take it seriously... Going forward, TradeXYZ's pre-listing contracts will no longer mention share data; they will simply track whatever the actual share count of the real-world company happens to be.

Community Controversy: Why Ignore the Stated Number?

Unsurprisingly, TradeXYZ's statement has sparked significant controversy within the community. The core reason is that for participants in SPCX (especially those who only opened positions on Hyperliquid), the general expectation was that SPCX's pricing logic was directly linked to SpaceX's share count.

The "11.87 billion shares" figure was explicitly written in the official documentation. TradeXYZ had also previously explained that if an investor expected SpaceX's valuation to be at a certain level and assumed a total share count of approximately 11.87 billion, they could derive a corresponding reasonable price range. Therefore, many users had already considered this as part of the product's rules.

Now, however, the official party has deleted the data and backtracked, stating that this content was merely "educational examples." This has naturally left some users feeling betrayed.

Although TradeXYZ's statement today attempts to emphasize a different product logic – unlike platforms such as Binance and OKX which map the stock price via market cap and share count, TradeXYZ tends to view SPCX as an independent trading market where the price directly reflects market participants' expectations for SpaceX's future stock price, rather than a theoretical result calculated through share data – the reality is complex.

For the vast majority of users, understanding the nuances of product rules and design differences across different markets is not easy. In the same timeframe, platforms like Binance and OKX were openly discussing share counts, valuation mapping, and Rebase mechanisms, so the market naturally applied the same logic to evaluate TradeXYZ and Hyperliquid.

This gap between user perception and product design ultimately evolved into a debate about product transparency and expectation management.

Will the Pre-Listing Contract Landscape Change?

Regardless of how this controversy ultimately resolves, the SpaceX pre-listing contract has already become the largest and most closely watched "IPO rehearsal" in the history of the crypto market.

More notably, as more and more unlisted star companies like Anthropic and OpenAI are brought onto on-chain trading markets, the pre-listing contract track itself is entering a new phase of competition.

In the past, the competition between exchanges focused more on who could list a hot target first. However, following the SPCX incident, the market may start paying more attention to another aspect: whose rules are clearer, whose pricing logic is more transparent, and who can provide users with a more stable and predictable product framework.