八年間の業界振り返り:暗号資産は最終的に別のより価値のある道を歩んだ

- 核心的見解:暗号資産業界は8年の発展を経て、分散型で伝統的な金融を覆すという当初のビジョンを実現できなかったものの、ステーブルコインとトークン化の波を通じて徐々に主流金融と融合し、新たなインターネット金融インフラを構築しつつある。その実際の価値は予想をはるかに上回っている。

- 重要な要素:

- ICOバブル、DeFiサマー、NFTブーム、そして2022年のシステム的な暴落(Terra、FTXの破綻など)を経験し、業界は投機サイクルの中で再構築を繰り返し、焦点は金融インフラへと移行した。

- ステーブルコイン(USDC、USDTなど)が中核的なユースケースとなり、現在の供給量は3000億ドルを超え、2025年の決済規模は100兆ドルに達すると見込まれている。米国債に連動することで、米国の国家戦略的利益に合致している。

- ミームコインの無秩序な繁栄の後、トランプ大統領の当選が規制に友好的な環境を促進し、『GENIUS法案』の可決によりステーブルコインのルールが明確化され、ウォール街は資産のトークン化の展開を開始している(例えばブラックロックCEOが支持を表明)。

- 人工知能と暗号技術の融合が進み、AIエージェントがステーブルコインとウォレットを利用して自律的な取引を行うようになり、無人商業主体の誕生を促し、業界の主流化とバックエンドインフラの置き換えを加速させる。

Original Author: Connor Dempsey

Original Translation: Chopper, Foresight News

I will start a new job on Monday. Before embarking on my fifth career chapter, I want to write this article to reflect on my eight-year journey in the crypto industry.

When I entered the crypto space in 2017, I believed this technology would change everything.

Government-issued fiat currency would be replaced by decentralized tokens; blockchains would eliminate all rent-seeking intermediaries in the transaction chain; power would shift back from large corporations to ordinary users.

Looking back now, almost none of those initial visions have materialized, but the industry has carved out a completely different path.

I have worked for four crypto companies over eight years, witnessing the industry's growth from less than $1 billion to over $4 trillion, surviving multiple speculative bubbles and one systemic collapse. Gradually, I've realized that what the industry is actually building is far more valuable than I initially imagined.

Before starting my next job, I want to document what I've seen and heard, and my predictions for the industry's future direction.

The Illusory Wealth Frenzy: The ICO Mania of 2017-2018

In early 2017, I stumbled upon Bitcoin in a book and was completely hooked. Soon after, I read every Bitcoin book I could find and had the idea of moving to Singapore to write a blog and delve deeper into this new technology.

At the time, I didn't realize I was at the tail end of the ICO (Initial Coin Offering) super-speculative bubble. ICOs allowed anyone to raise funds globally by selling cryptocurrencies to investors, crowdfunding creative projects.

Ethereum was the star of this frenzy.

In November 2017, I published a beginner-friendly guide to Ethereum that went viral on Reddit. That coincided with the peak of the bubble, which burst just a month later.

Reading that article now feels like a time capsule: it captured the era's euphoric optimism and predicted a future that ultimately didn't come true.

My main point was that blockchain networks like Ethereum could be used to build a new generation of consumer applications.

Traditional internet platforms (Facebook, Uber, etc.) generate value mostly for the corporations and a few investors; value created by blockchain applications would be shared between early participants and ICO investors.

The article also envisioned building a decentralized Uber. In this system, early users and drivers would receive tokens for each completed trip, giving them ownership of the network and providing fairer value distribution to early contributors.

It looked good on paper, but this decentralized revolution ultimately failed completely.

It was a crypto speculative feast replicating the 2001 internet bubble.

Ethereum became the most powerful fundraising platform ever, with over 3,000 ICO projects raising a total of $22 billion globally.

But, just like the internet bubble, the underlying technology wasn't mature enough to support the sky-high valuations the market gave it.

More critically, ICOs completely distorted the incentive structure between entrepreneurs and investors. Project teams could raise tens of millions overnight with just an idea; investors only held tokens, hoping the project would materialize and appreciate in value. Founders, holding large amounts of native tokens, could become instantly wealthy upon listing, losing all motivation to build a solid product.

During the bull market, founders and early investors made a fortune; during the bear market, ordinary retail investors were left holding the bag. Despite some well-intentioned builders, ICOs ultimately became a breeding ground for greed, hype, and fraud.

Throughout centuries of financial history, every speculative bubble has been the same.

Building on the Ruins: The Circle Quiet Period 2018-2019

As the market declined, leveraging the little fame I gained on Reddit, I joined Circle in early 2018 as an entry-level marketing employee.

Circle had been around for four years by then, with several consumer products (investing, payments, exchange) not yet profitable. However, its over-the-counter (OTC) trading desk was quietly generating consistent revenue, supporting the entire company's operations.

For the next two years, the industry languished in the post-ICO bubble depression. Most ICO projects were abandoned and defunct, countless tokens went to zero, and industry sentiment hit rock bottom.

But it was precisely this darkest hour that sowed the seeds for the industry's next renaissance.

The industry's focus shifted away from consumer applications and concentrated on rebuilding the traditional financial system on the internet.

Stablecoins pegged to the US dollar were initially created to allow traders to easily move in and out of crypto positions. By holding a 1:1 reserve of dollars and Treasuries, the token price is always anchored at $1.

Tether's USDT rose rapidly during the ICO boom, with its dollar reserves mostly held in offshore bank accounts. Stablecoins were initially used for trading but soon found another use case: for people without access to the traditional banking system who wanted to hold dollar-denominated assets.

Examples include people trying to bypass capital controls, wealthy Chinese diversifying assets abroad, and citizens of Argentina and Turkey suffering from inflation.

In 2018, Circle partnered with Coinbase to launch the compliant dollar stablecoin USDC. Early uses were still primarily for trading, but people began to envision this "internet money" providing anyone with an internet connection 24/7 access to US dollar assets.

Simultaneously, the quality projects that survived the ICO era were mostly focused on finance. Ethereum was not just for fundraising; it could rebuild the underlying infrastructure of financial markets: Uniswap for trading, Aave and Compound for lending, together forming the DeFi ecosystem.

Stablecoins and DeFi became deeply intertwined, and a once-in-a-century global pandemic propelled them to their peak.

Back to the Wild West of the Internet: The Messari Era 2019-2021

At the end of 2019, I joined Messari, a 13-person data research startup, as its first full-time marketing hire.

The company had only 4 analysts focusing on cutting-edge DeFi research; DeFi's total market cap at the time was just $665 million.

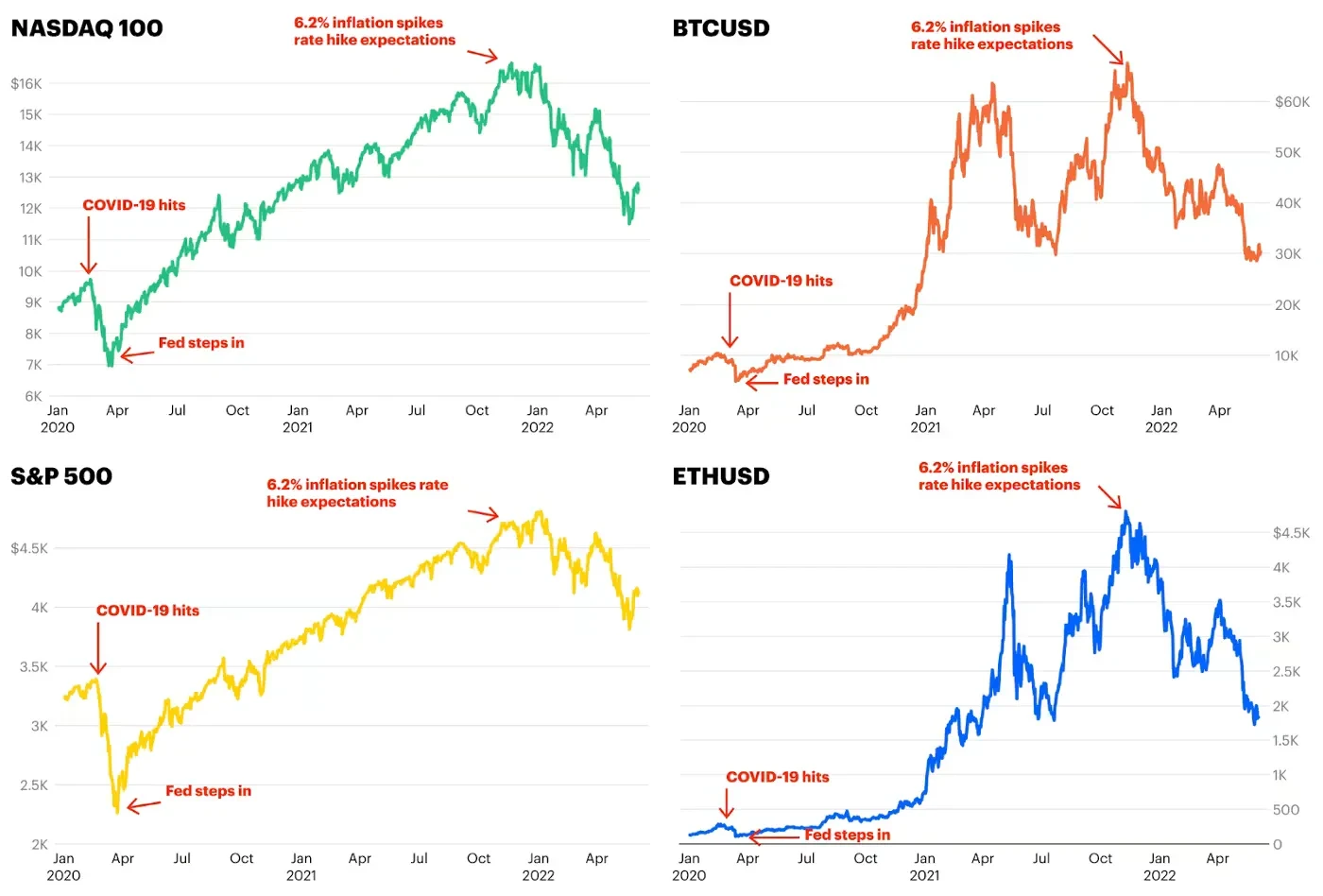

In early 2020, the COVID-19 pandemic hit, bringing the global economy to a near standstill and causing all asset classes to crash.

To prevent an economic collapse, central banks worldwide began massive money printing, with total global stimulus reaching $9 trillion in 2020 alone.

With massive liquidity seeking a home and everyone confined at home, huge amounts of hot money flowed into Bitcoin, Ethereum, DeFi, and various speculative assets.

Bitcoin soared from under $4,000 to nearly $70,000, reaching a trillion-dollar market cap with institutional backing, outperforming macro assets like gold.

The loose monetary environment also spawned the famous "DeFi Summer," where the market cap of DeFi protocols exploded 250 times to $180 billion.

While DeFi was intended to rebuild traditional finance, DeFi Summer felt more like a massive online game driven by profit-seeking traders, with tens of billions of real dollars at play.

The core gameplay was yield farming. Anonymous developers launched new protocols, often with food-themed names like YAM Finance, Spaghetti Money, and SushiSwap. Traders could deposit mainstream tokens like ETH, USDC, or USDT and claim the newly issued tokens (YAM, SPAGHETTI, SUSHI).

It was absurd and crazy: newly launched projects with food-themed tokens could reach a $1 billion market cap within days. Early players would cash out at the top, causing token prices to crash.

This was truly the Wild West of the internet.

Like the ICO mania before it, DeFi Summer created a new wave of crypto millionaires but ultimately succumbed to a bubble burst. This wave also gave us Sam Bankman-Fried, a new crypto billionaire who would later become the central figure in the industry's next disaster.

At the Peak of the Bubble: The Coinbase Era 2021

Shortly after Coinbase's $100 billion market cap IPO in April 2021, I was invited to join the company's Corporate Development and Venture Capital team.

My work involved M&A, early-stage crypto venture investments, writing industry trend analyses, and helping produce Coinbase's short-lived podcast. It remains one of the best teams I've ever worked with.

It was during this period that another speculative bubble quietly formed: the NFT craze, centered around digital artworks.

If DeFi was the arena for professional traders, NFTs broke into the mainstream public consciousness. They offered artists a new way to monetize online and laid the foundation for asserting ownership of digital assets on the internet.

But, just like ICOs and DeFi Summer, NFT speculation quickly spiraled out of control. Cartoon apes, punks, and penguins sold for millions of dollars each; a collage by the artist Beeple fetched an absurd $69 million at Christie's.

Cryptocurrency entered the mainstream completely: Larry David mocked crypto skeptics in a Super Bowl ad; Sam Bankman-Fried's exchange FTX spent $135 million on the naming rights for the Miami Heat's arena. Everyone seemed to be getting rich from tokens, NFTs, and crypto stocks.

The madness of 2017 returned, amplified by unprecedented monetary stimulus, making this bubble four times larger.

The Reckoning: The Great Industry Crash of 2022

But soon, the party ended, and the industry collapsed.

The stimulus that had inflated all asset prices through rate cuts, money printing, and fiscal aid eventually translated into consumer inflation. Bitcoin, Ethereum, the Nasdaq, and the S&P 500 all peaked simultaneously in late 2021; inflation was out of control, forcing central banks to tighten the very policies that had pushed stocks and crypto to all-time highs.

As interest rates rose and fiscal stimulus ended, investors began re-evaluating their high-flying assets: Is that cartoon ape really worth $1 million? Why is a sushi-themed token worth $3 billion? How is Dogecoin supporting a $90 billion valuation?

Pessimism spread, triggering a chain of collapses across the industry.

If the ICO crash was like the 2001 dot-com bubble burst, 2022 was more akin to the 2008 global financial crisis: a small number of toxic assets combined with high leverage nearly brought down the entire industry.

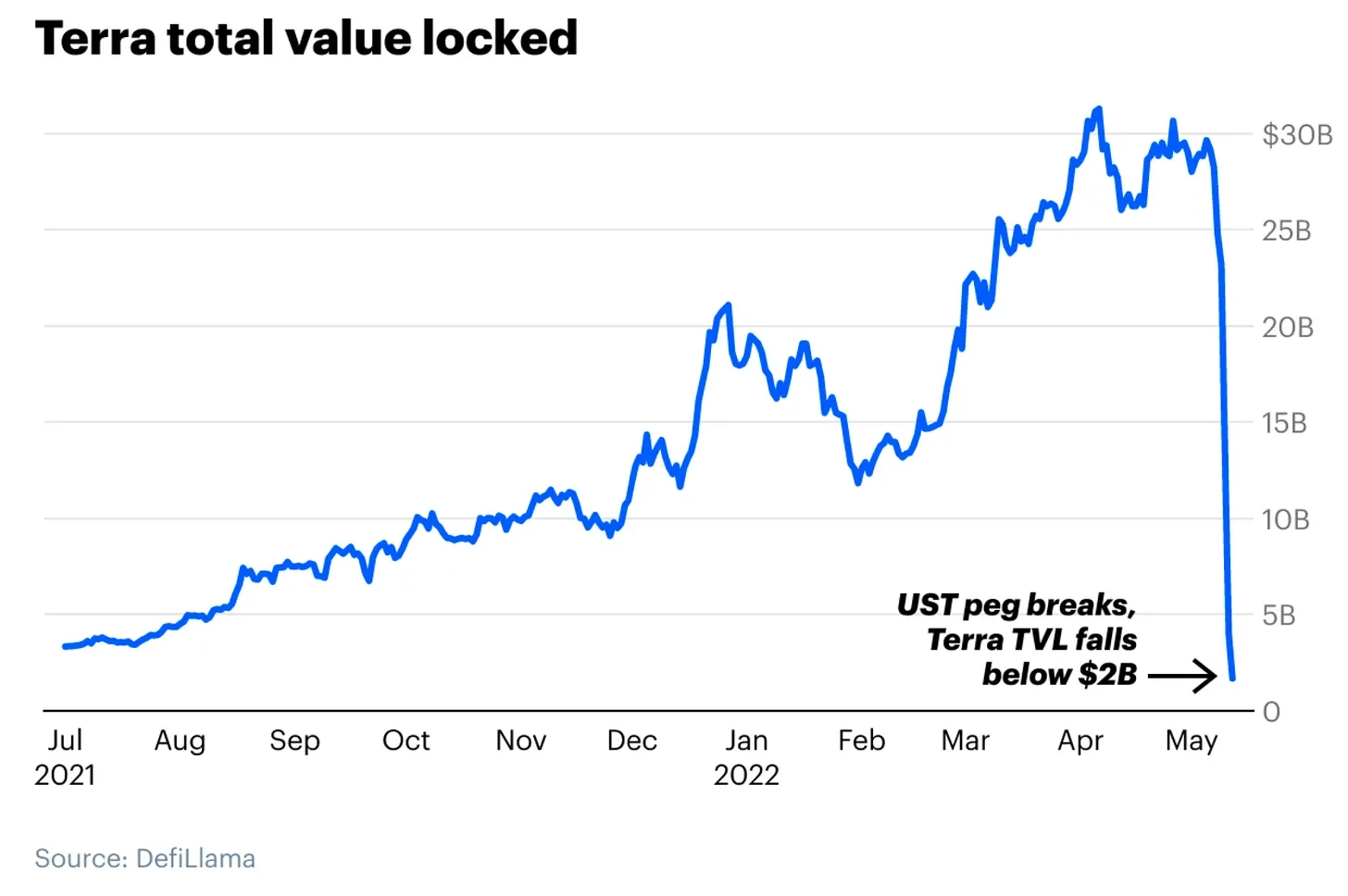

The first domino to fall was the Terra algorithmic stablecoin UST.

Stablecoins like USDC and USDT are backed 1:1 by cash and Treasuries, while UST used a complex algorithmic mechanism to maintain its $1 peg. The mechanism worked when markets were calm but failed completely during a sell-off.

In a matter of days, $32 billion in market cap vanished, and countless holders saw their assets go to zero.

Next came the multi-billion dollar hedge fund Three Arrows Capital, which was heavily exposed to Terra and leveraged, leading to its bankruptcy. 3AC had borrowed heavily from crypto lending platforms like Celsius and Voyager, which in turn had misappropriated user deposits to chase seemingly safe 8% yields. When 3AC collapsed, these platforms froze withdrawals and filed for bankruptcy, wiping out ordinary user funds.

During my time at Coinbase, we watched FTX and Sam Bankman-Fried step in to rescue several failing crypto lenders like BlockFi. He was hailed as the "JP Morgan of crypto," the industry's white knight.

But the truth eventually emerged: SBF and FTX were the biggest risks of all.

Remember the expensive arena naming rights deal? That spending, and indeed SBF's entire business empire, was propped up by FTX's native token, FTT. SBF used FTT as collateral for massive loans. When FTT's price crashed, the loans were liquidated, and FTX went bankrupt.

Worse, FTX secretly used customer funds for investments and to plug holes in its balance sheet. This $32 billion giant collapsed within a week, with $8 billion in customer deposits missing.

SBF violated the cardinal rule of exchanges: never touch user assets.

This was the "Lehman Moment" for the crypto industry.

Gambling and Casinos: The Memecoin Mania 2023-2025

After the FTX collapse, SBF was sent to prison. In just 12 months, the crypto industry's market cap shrank from $3 trillion to less than $1 trillion.

Then, the Biden administration began a comprehensive crackdown on the US crypto industry.

SEC Chair Gary Gensler sued most compliant US crypto companies for securities violations, including Coinbase, Kraken, Uniswap, and Robinhood. The companies that had operated within the rules for years became the SEC's primary targets.

At the same time, Senator Elizabeth Warren worked behind the scenes to pressure traditional banks to cut ties with crypto clients, effectively isolating the industry from the banking system and forcing many teams to move overseas.

This regulatory approach had several unintended consequences.

Firstly, any crypto project with a business model (like DeFi protocols) was deemed a potential securities violation, facing the risk of a lawsuit. The safest legal option became the Memecoin – a token with no utility, no clear vision, pure narrative.

Platforms like Pump.fun launched millions of memecoins. Celebrities like Iggy Azalea, Caitlyn Jenner, and the Hawk Tuah girl launched their own, all ending in farce.

The crypto industry became a giant casino once again, on a scale larger than ever before. Over 6 million memecoins were launched, with the sector's market cap peaking at $150 billion in late 2024, an even bigger bubble than the NFT craze.

Institutionalization: The Crossmint Era 2025-2026

Setting aside this industry sideshow, the crypto bet on Trump's election ultimately paid off.

As the prospect of a Trump victory became clear, Bitcoin hit new all-time highs. Market pricing was logical: the world's largest economy was shifting from hostile regulation to friendly support. Gary Gensler resigned. The new SEC dropped lawsuits against US crypto companies. Traditional banks reopened their doors to crypto clients.

Most importantly, the GENIUS Act was passed in July 2025, the first federal crypto-specific legislation in the US, establishing a clear regulatory framework for stablecoins.

Washington sent a clear signal to Wall Street: the crypto industry, especially stablecoins, was about to become a major commercial sector. Stablecoin companies like Bridge and BVNK were acquired by Stripe and Mastercard for over $1 billion valuations; Rain completed a nearly $2 billion Series C round; my former employer, Circle, the issuer of USDC, went public, reaching a peak valuation of $60 billion in June 2025.

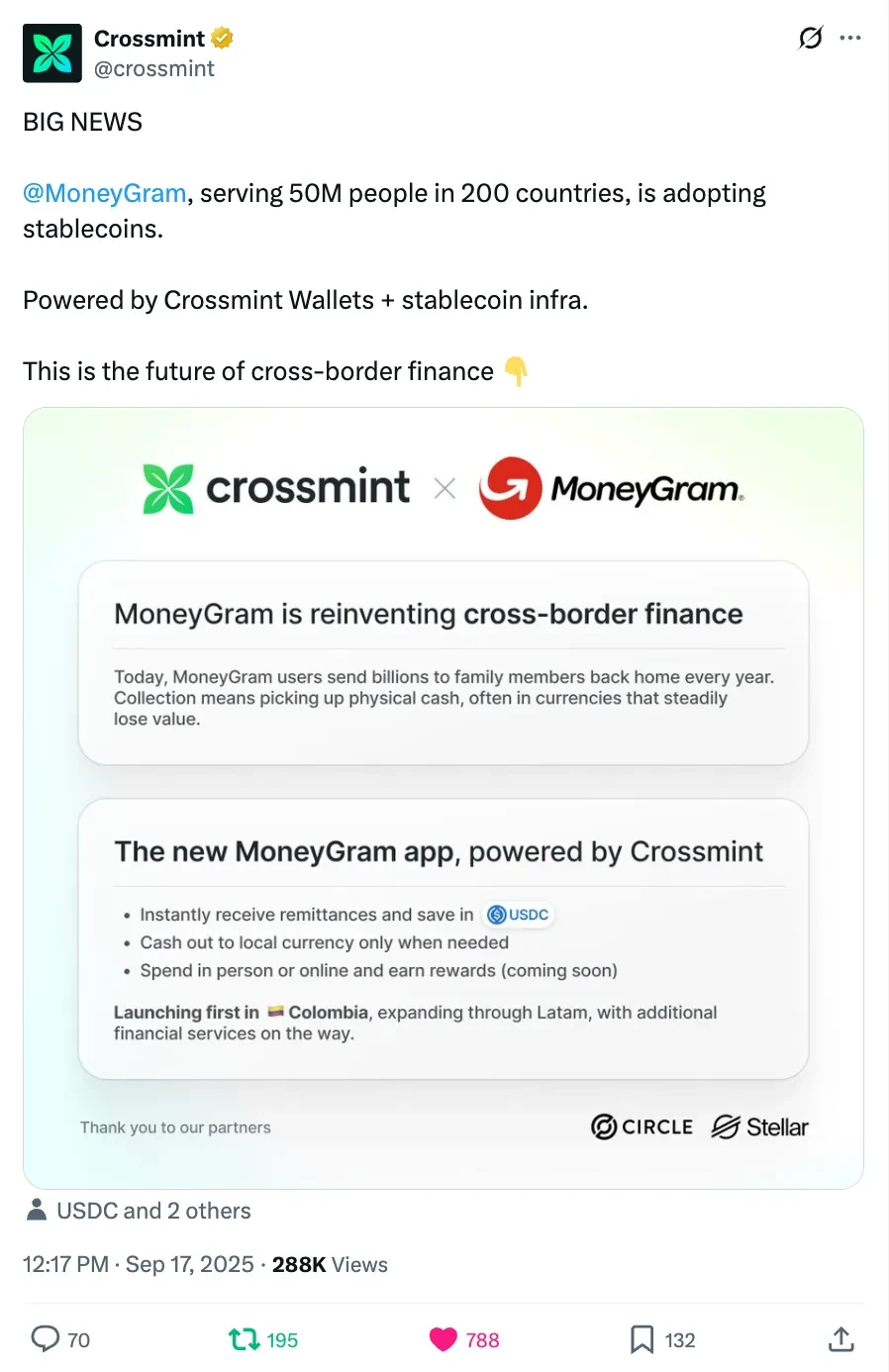

By then, I was Head of Marketing at Crossmint, where we partnered with MoneyGram to help the century-old remittance giant use stablecoins for global cross-border transfers.

As the value of dollar tokenization became clear, Wall Street began seriously considering tokenizing other assets on-chain. Even Larry Fink, CEO of BlackRock, who once called Bitcoin an "index of money laundering," changed his tune, stating that tokenization is the next generation of financial markets, and all asset classes like stocks and bonds will eventually move onto blockchains.

An Unforeseen Revolution: The State of the Industry Today

Eight years after that Reddit post, we still don't have a decentralized Uber.

Blockchains haven't eliminated all intermediaries, and decentralized tokens haven't replaced national fiat currencies.

But I believe, looking back, this turbulent period will be defined as the chaotic embryonic stage of a new internet-native financial system. Each boom and bust has strengthened the underlying infrastructure, reshaped global finance