MSTR STRC深層分析:11.5%利回りの背景にあるBTC資金調達のフライホイール

- 核心見解:STRCは、固定収益需要をビットコインの買い圧力に巧みに変換する資金調達手段であり、強気相場では11.5%の変動利回りを提供する。しかし、そのリスクの本質はビットコイン資産カバレッジにおける「プットオプションの売り」であり、脆弱点はmNAVが1.0倍を下回り、下方スパイラルを引き起こす可能性がある点にある。特に2026年下半期にその確率は約70%と見込まれる。

- 主要要素:

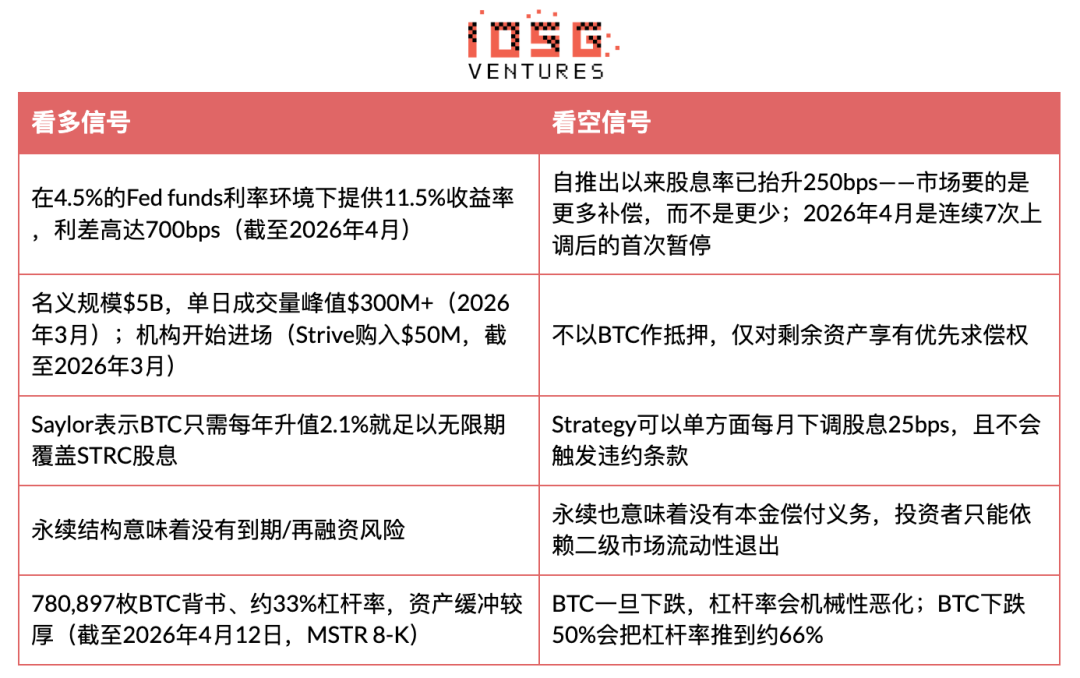

- STRCの名目規模は50億ドルで、開始以来Strategyに35億ドル以上のBTC購入資金を提供してきた。その安定性は担保サポートではなく、投資家の信頼と継続的な配当オークションに依存している。

- リスク発動経路は3段階:BTC下落による100ドルアンカーの崩壊、配当引き上げの罠(現在は9%から11.5%に引き上げ済み)、mNAVが1倍を下回った後のフライホイール断裂。これによりStrategyは、買い増しと安定したナラティブ放棄の間で選択を迫られる。

- 2026年4月の配当初回引き上げ停止(強気シグナル)とMSTR ATM増発の停止が同時に発生したことは、mNAVが1.0倍近くまで圧縮され、フライホイールが部分的に機能不全に陥っていることを示している。

- 清算時におけるSTRCの優先順位は、82億ドルの転換社債およびSTR F優先株よりも低い。BTCが50%以上下落した場合、その資産バッファーは著しく薄くなる。

- NYDIGはそのリスクを「ビットコイン資産カバレッジにおけるプットオプションの売建て」と表現する。アナリストの見解は強気派が安全な利回り商品と見做す一方、弱気派は価格設定を誤った信用リスクと見做す点で分かれている。

Original Author: Benji

Original Source: IOSG Ventures

Core Thesis: STRC is an ingeniously designed financing tool that converts fixed-income demand into buying pressure for Bitcoin. In a bull market, it offers 11.5% floating yield with relatively low price volatility. However, its risk structure is fundamentally equivalent to "selling a put option" on Bitcoin's asset coverage ratio. Therefore, when BTC declines, it cannot substitute for genuine fixed-income products.

STRC's true vulnerability isn't the BTC price, but mNAV. Once MSTR's mNAV falls below 1.0x for over 4 consecutive weeks, the flywheel enters a downward spiral in passive mode within 3 months. We estimate a ~70% probability of this trigger occurring in the second half of 2026, presenting a potential buy-in entry point for STRC around $85–$90. If the trigger isn't met, it means Saylor has successfully created an entirely new category of BTC-native credit instruments.

Background

Strategy (formerly MicroStrategy) launched STRC ("Stretch"), a perpetual preferred stock with a target par value of $100, maintained by monthly floating dividends. As of March 31, 2026, STRC had a notional size of $5B, with peak daily trading volume exceeding $300M (as of March 2026 data). It has provided over $3.5B in BTC purchasing funds for Strategy since its launch, making it its most important current financing vehicle. As of April 12, 2026, Strategy's balance sheet held 780,897 BTC with a leverage ratio of 33%, and had approximately $21.6B remaining issuable under the STRC ATM.

This instrument occupies a novel category: it looks like a money market fund (stable price, high yield), but the credit risk it carries derives entirely from a single company's BTC holdings.

Before elaborating our argument, let's clarify "where we could be wrong."

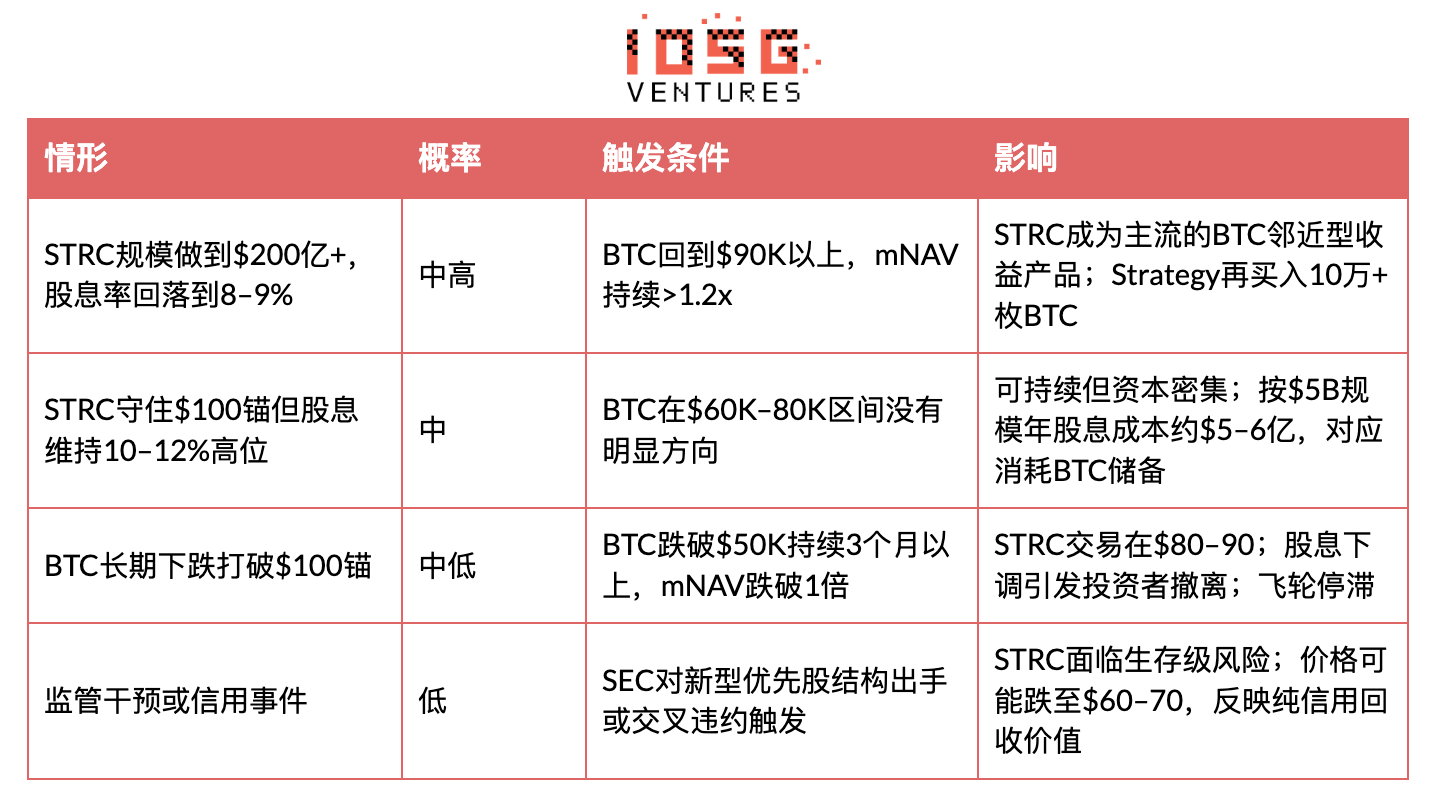

If our analysis is wrong, it will be because: traditional fixed-income allocators are truly willing to accept reflexive risk for a 700bps spread; STRC grows to $50B in size within 3 years, becoming the de facto BTC yield curve; and Saylor successfully securitizes BTC into an interest-bearing collateral asset acceptable within institutional portfolios. This outcome would represent the largest integration of crypto into traditional finance to date—a $50B+ asset class that simply didn't exist before 2025.

In this optimistic scenario, the April 2026 dividend suspension isn't a warning signal, but a feature: a maturing instrument begins stabilizing its yield after early price discovery, similar to the gradual repricing of high-yield bond ETFs as institutional adoption increases.

Thesis Breakdown

STRC's core innovation: it converts yield-seeking capital into buying pressure for BTC. When STRC trades near $100, Saylor issues new shares via ATM (approx. 40% of daily volume), uses the proceeds to buy BTC, and then issues MSTR common stock at a premium to NAV (mNAV>1x) to deleverage. The net result: $100M of STRC daily volume can leverage approximately $120M in BTC purchases.

But this mechanism's vulnerability lies in its underlying circularity: STRC stays stable at $100 because investors believe it will; and Saylor maintains this belief through continuous dividend increases. This anchor isn't collateral-backed but confidence-backed, sustained by a continuous dividend auction without a formal ceiling. Once this confidence breaks, the auction becomes increasingly expensive.

Evidence & Comparison: STRC vs. Other BTC Exposure Instruments

Key Insight: For Strategy, STRC converts fixed-income demand into fuel for BTC accumulation. For investors, it offers Sharpe-optimized returns in a benign environment, but with an embedded BTC "sold put." NYDIG's description is precise: "It is akin to shorting a put option on Bitcoin's asset coverage ratio—earning yield in exchange for assuming the downside risk that BTC declines could erode the asset buffer."

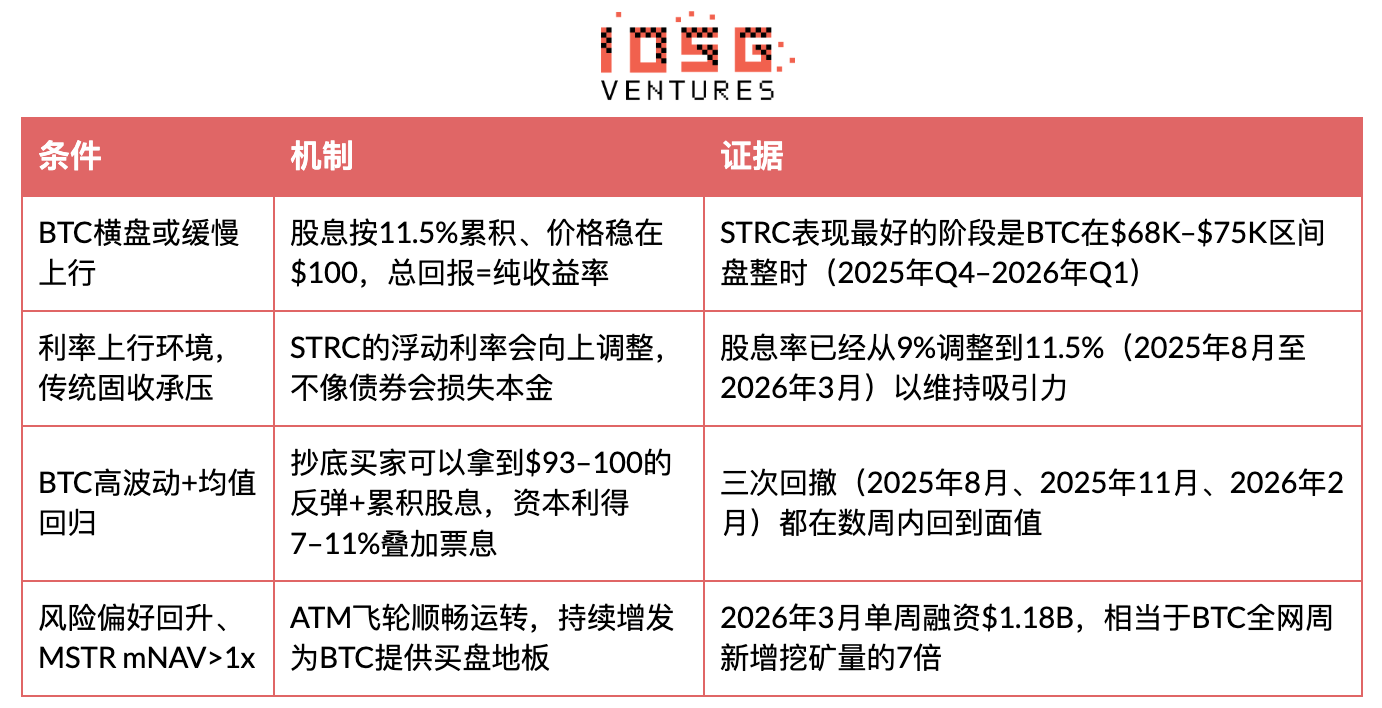

When STRC Performs Well

When STRC Performs Poorly

When STRC Crashes: The Death Spiral Scenario

The key question is: can STRC enter a self-reinforcing downward cycle? The answer is yes, but under specific conditions. This mechanism has three interconnected failure paths.

Phase 1: BTC decline breaks the $100 anchor

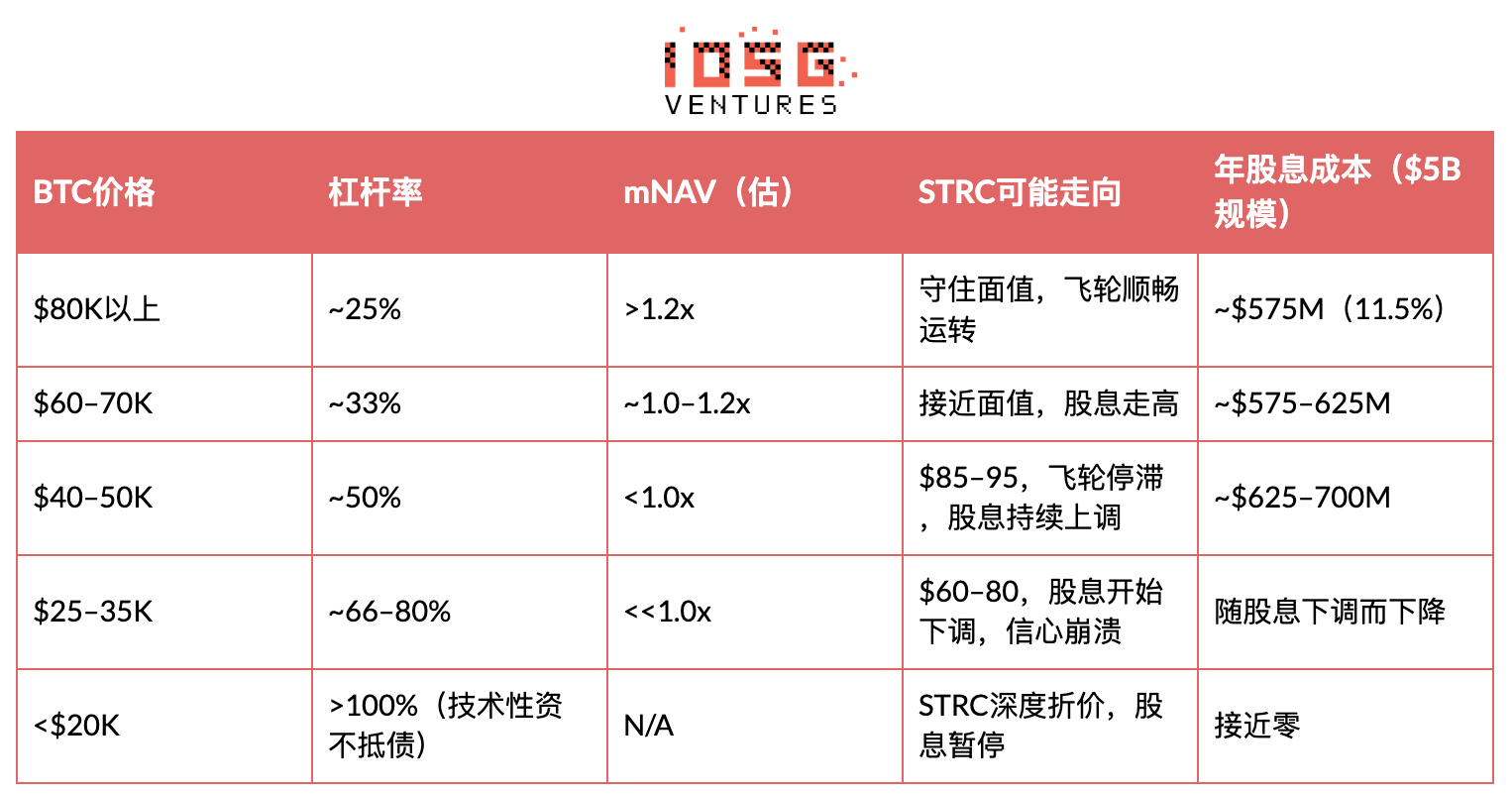

During a sharp BTC decline (e.g., ~45% retracement from all-time highs in late 2025), Strategy's leverage ratio mechanically increases. Based on 780,897 BTC and a 33% leverage ratio (as of April 12, 2026, per MSTR 8-K), a further 50% decline in BTC would push the leverage ratio to ~66%. STRC's credit quality deteriorates as its priority claim on remaining assets thins. The price breaks below $100. This scenario has occurred three times (Aug 2025: ~$92, Nov 2025: intraday low, Feb 2026: ~$93), but each time BTC rebounded quickly, pulling the anchor back.

Phase 2: The Dividend Hike Trap

Per Strategy's guidance to the SEC: if the monthly VWAP is between $95–$99, the dividend rate increases by 25bps monthly; if it falls below $95, the rate increases by 50bps monthly. From 9% to 11.5%, the dividend rate has accumulated a 250bps increase over roughly 8 months (Aug 2025 to Apr 2026), averaging ~31bps per month—a pace faster than any comparable company's preferred stock repricing under stable market conditions. April 2026 marks the first pause after 7 consecutive increases. Two interpretations: (a) demand stabilizing—bullish; (b) Strategy hitting the yield sensitivity ceiling of traditional fixed-income buyers—bearish. This is the single most important signal to track over the next 1–2 months.

If BTC remains depressed, dividends must continue to rise to attract buyers back near par value. At a $5B size, each 100bps increase means approximately $50M in additional annual cash costs; if STRC expands to $20B (authorized ATM capacity), the cost of each 100bps becomes $200M annually. A bear market lasting over 6 months at the current pace of increases would push STRC's yield to 13–15%; at this level, annual dividend payments on a $20B size would exceed $2.6–3.0 billion, consuming a significant portion of Strategy's potential BTC reserve earnings and forcing a choice between "continuing to raise" and "abandoning the stable narrative."

The lack of a formal upper limit on dividend increases—this "no cap" dynamic—is precisely what bears focus on.

Phase 3: Flywheel Breaks When mNAV Falls Below 1x

This is the true breaking point. Strategy relies on issuing MSTR common stock at a premium to NAV (mNAV>1x) to buy BTC and deleverage. If BTC falls deeply enough and mNAV drops below 1x, issuing common stock would dilute existing shareholder value, and Saylor cannot deleverage through issuance. Strategy then faces a trilemma: (a) continue issuing STRC at higher dividend rates and accept higher leverage; (b) unilaterally cut dividends (up to 25bps/month) per the SEC filing terms, allowing the STRC price to fall; or (c) sell BTC into a falling market.

Saylor has repeatedly stated he will never sell BTC. BitMEX Research concludes that (b) is most likely: "Strategy won't sell bitcoin; it will simply abandon STRC's stable narrative." All pressure will transfer to STRC holders.

An early warning sign has already flashed: during the week of April 6–12, 2026, MSTR's ATM issuance was $0—all financing came via STRC ($1.00B, 10.028 million shares; MSTR 8-K). mNAV is already too tight for Saylor to risk diluting common stock. The precondition for Phase 3 is partially triggered—the flywheel is running on one leg.

Quantifying the Crash Scenario

Why this differs from UST/Terra: UST relied on an algorithmic mint-and-burn mechanism, with only an endogenous token (LUNA) for support. STRC is backed by real BTC, and Strategy has the discretion to choose to cut dividends rather than face forced liquidation. STRC's floor is not zero—it's the priority claim on remaining assets in bankruptcy liquidation. However, if BTC declines by over 60% and remains low, this floor could be significantly below $100.

The key variable is time. Each previous STRC drawdown was repaired within weeks because BTC rebounded. A true crash requires a sustained bear market (above 3 months below $50K), allowing the dividend increase mechanism to run long enough to erode confidence. The longer STRC stays below par with continuously rising dividends, the more it resembles a company rolling over increasingly fragile debt at increasingly high interest rates—a pattern with a very clear ending in credit markets.

Capital Structure Priority: Liquidation order is: Convertible Bonds (~$8.2B) → STRF → STRC → STRK → STRD → MSTR Common Stock. STRC sits behind $8.2B in unsecured debt and STR F preferred stock.

Industry Perspectives

"STRC's risk is significantly higher than short-duration US Treasuries... When the music stops, investors might feel somewhat aggrieved." — BitMEX Research, A Bit of a Stretch (Nov 2025)

"The appropriate way to assess STRC's risk is from the perspective of governance and subordination, not just payment risk." — Greg Cipolaro, Global Head of Research, NYDIG (March 2026)

"It is akin to shorting a put option on Bitcoin's asset coverage ratio—earning yield in exchange for assuming the downside risk that BTC declines could erode the asset buffer." — NYDIG Research Report (March 2026)

The core divergence among analysts is here: bulls see STRC as the safest way to earn 11.5% yield currently available; bears see it as mispriced credit risk packaged as a money market product. The bears' core concern directly corresponds to the dividend increase mechanism described above: STRC won't suddenly default, but will slowly reprice—the longer and deeper BTC stays depressed, the more it slides from a quasi-monetary instrument into a distressed yield product. This gradual erosion is the real risk, not an overnight crash.

Implications & Predictions

Bottom Line: STRC is a genuinely novel financial instrument that works beautifully in the environment it was designed for—BTC rising steadily, open capital markets, mNAV>1x. In this state, offering 11.5% yield with manageable volatility is indeed attractive. But its downside structure is asymmetric: collect coupons in good times, bear concentrated, single-name BTC credit risk in bad times. It is not a substitute for Treasuries or diversified high-yield bonds, but a leveraged bet on the continued operation of Strategy's BTC accumulation flywheel, packaged as fixed-income.

Three New Signals (as of April 2026)

Signal 1: First Pause in Dividend Increases in April (as of April 1, 2026, CoinDesk).

After seven consecutive increases from August 2025 to March 2026 (9% to 11.5%), Saylor kept the dividend rate unchanged in April. Two interpretations: (a) demand stabilizing at this yield level, bullish; (b) Strategy hitting the yield sensitivity ceiling of traditional fixed-income buyers, bearish. This is the single most important signal to track in May-June, and the inflection point around which our mNAV trigger framework is centered.

Signal 2: MSTR ATM Issuance at $0 for Week of Apr 6-12, All Financing via STRC ($1.00B; MSTR 8-K, Apr 2026).

At the current BTC price level, mNAV is already too tight for Saylor to risk diluting common stock by issuing MSTR. The precondition for Phase 3 of the death spiral is partially triggered—the flywheel is running on one leg.

Signal 3: Average BTC Purchase Price Last Week was $71,902/coin, Below Strategy's Historical Cost of $75,577/coin (as of Apr 12, 2026, MSTR 8-K)

Strategy is DCA buying into a weakening market. The flywheel is still turning, but each marginal purchase is thinning the asset buffer, not thickening it—the opposite dynamic of the 2024-2025 accumulation cycle.

Investment Recommendation

HOLD, awaiting better entry points and BTC upside.

Current Status: HOLD existing positions. Do not add new positions without better signals. MSTR's mNAV has compressed to near 1.0x. STRC remains around the $100 par value paying an 11.5% dividend, indicating the dividend mechanism is functioning as designed. However, the margin of safety is very thin.

Condition for Re-entry: BTC reclaims $70-75K, and MSTR mNAV has confirmed above 1.1x for two consecutive weeks. At that point, STRC returning near the $100 par value enters a conditional buy zone. Historically, buying at dips below $95 followed by a BTC rebound has yielded 7-11% capital gains plus accumulated coupons—but this has only occurred in environments where BTC rebounds within weeks (Aug 2025, Nov 2025, Feb 2026). Whether the current drawdown continues this pattern or signals a more sustained bear market is the true unknown.

Exit Signal: Initiate sell evaluation upon any of the following: (a) MSTR mNAV falls below 1.0x and persists for over two weeks; (b) STRC VWAP remains below $95 for 4 consecutive weeks; (c) BTC breaks below $55K on significant volume.

Appendix

Timeline

Position Concentration—Who Could Force a Break in Price?

Strive's $50M purchase was mentioned, but there was no discussion on whether STRC has a few large institutional holders—and if they were to rotate out simultaneously, whether it could overwhelm the average daily volume of $258M and self-fulfillingly push STRC below par value. This is the "run" risk.