NVIDIA Roadshow Preview: Nearly $100 Billion in Quarterly Revenue, Yet Still Confident in 'Growth Acceleration'?

- Core Thesis: NVIDIA's growth is still accelerating, but the driving force is shifting from a few top AI labs and hyperscale cloud providers towards diversified new sources such as networking, CPU, Sovereign AI, and industrial/enterprise clients. Its competitive moat has widened from GPU performance to its full-stack AI platform capabilities. By increasing shareholder cash returns, it is poised to exhibit both high-growth and value stock attributes.

- Key Elements:

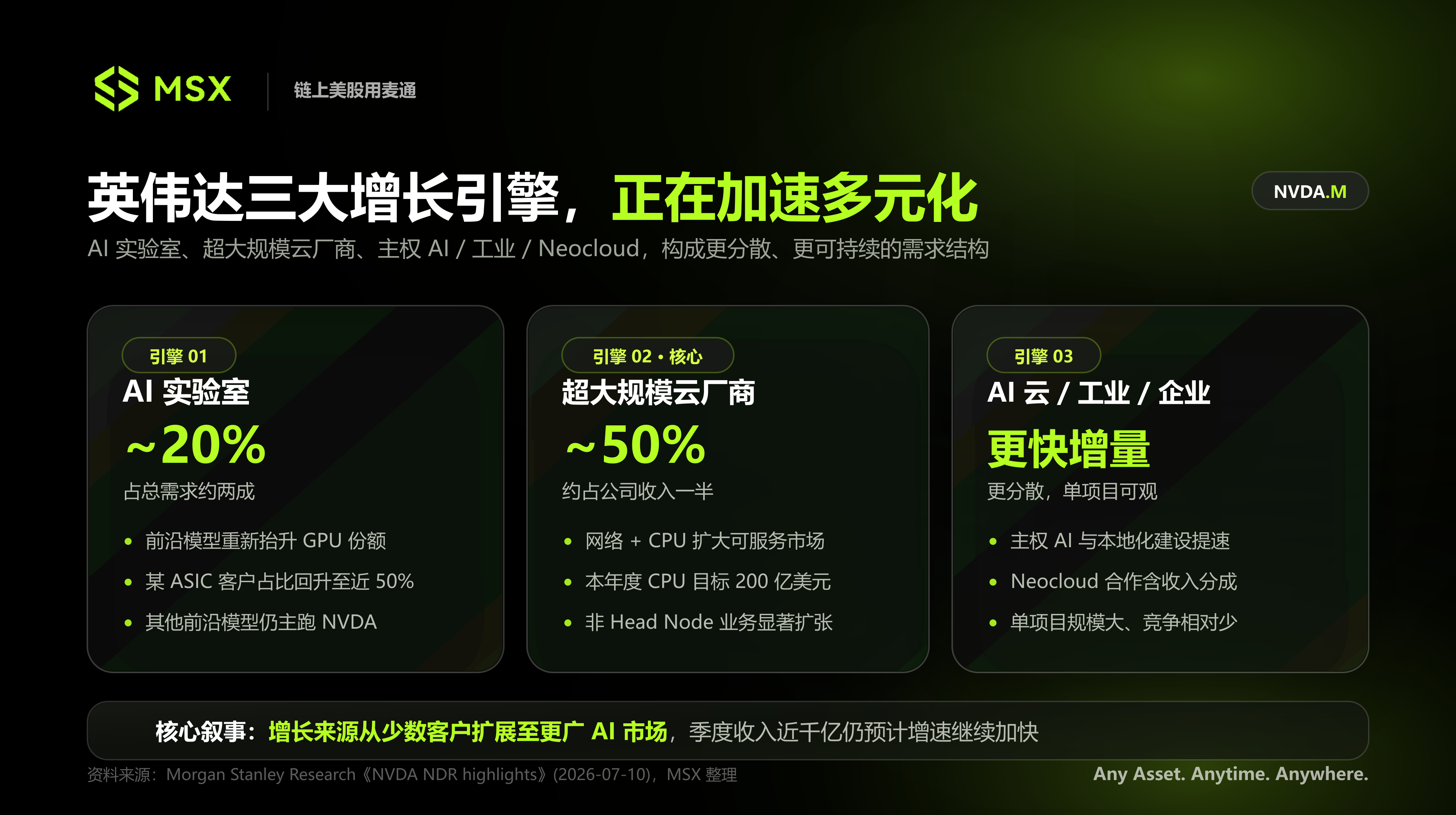

- Diversification of Growth Sources: NVIDIA's demand can be segmented into AI labs (~20%), traditional cloud providers (~50%), and emerging customers (AI cloud, industry, Sovereign AI). For one major customer primarily using ASICs, its share of NVIDIA computing power has risen to nearly 50%, demonstrating the platform's comprehensive cost advantage.

- ASICs Are Not a Zero-Sum Game: Customer choice depends on the total computing cost per token and deployment efficiency, not the single chip price. NVIDIA builds its moat through a platform consisting of CUDA, networking, CPU, and interconnects.

- Stable Product Roadmap: NVIDIA denies that Rubin Ultra has been delayed to 2028, confirming it is still on track for shipment in 2027. Only certain rack-scale solutions will be adjusted, while core technology directions (800V power, optical interconnects) remain unchanged.

- Memory and Power as Supply-Side Constraints: Memory shortages are expected to persist for several years. NVIDIA is adjusting memory configurations and system architecture to improve system delivery efficiency under limited supply – this is not a sign of weakening demand.

- Transition to a Value Asset: Management expects to allocate 50% or more of free cash flow to shareholder returns (stock buybacks and cash dividends), aiming to attract value-oriented investors alongside growth-focused capital.

- Morgan Stanley Rating: Maintains an "Overweight" rating and a $288 price target. It projects revenue of $215.9 billion to $783.9 billion between 2026 and 2029, believing the risk/reward profile is attractive within the semiconductor sector.

Original Report: Morgan Stanley Research "NVDA NDR Highlights Diversified Growth Opportunities," July 10, 2026

Compiled & Organized by: DaiDai

Editor: Frank

Key Takeaways:

- NVIDIA sees accelerating growth, but the drivers are shifting: Demand is no longer solely reliant on top-tier AI labs and hyperscale cloud providers. Networking, CPUs, Neoclouds, Sovereign AI, and industrial/enterprise clients are emerging as new sources of growth.

- ASICs and GPUs are not a zero-sum game: At one major frontier model customer previously relying heavily on ASICs, NVIDIA's computing share has risen to nearly 50%. In numerous real-world workloads, the ultimate comparison isn't just chip price, but the total computing cost per token and deployment efficiency.

- Vera Rubin roadmap remains on track for now: NVIDIA denied rumors that Rubin Ultra has been delayed to 2028, confirming it is still planned for shipment in 2027. While some rack-level solutions will be adjusted, key directions like the 800V power architecture and optical interconnects across racks remain unchanged.

- Memory and power are supply-side constraints, not signals of weakening demand: NVIDIA expects memory shortages to potentially last for several years and will improve system delivery efficiency under constrained supply by adjusting memory configurations, networking, and system architecture.

- Morgan Stanley continues to rank NVIDIA as its top semiconductor pick: The report maintains an "Overweight" rating and a $288 price target. It believes that as the company increases its cash return ratio, NVIDIA is transitioning from a pure high-growth asset to increasingly possessing the value characteristics of a large-cap tech stock.

When a company's single-quarter revenue approaches $100 billion, the market's focus often shifts from how much more it can grow to how long this growth can be sustained.

This is precisely the scrutiny NVIDIA currently faces.

Recently, debates surrounding NVIDIA have centered on three main issues: whether global AI infrastructure investment is approaching its peak; whether the push for in-house ASICs by cloud giants like Google, Amazon, and Meta will gradually erode GPU market share; and whether the next-generation Vera Rubin product roadmap has faced delays or adjustments.

In early July, Morgan Stanley organized several Non-Deal Roadshows (NDRs) for NVIDIA in California. NVIDIA's CEO Jensen Huang, CFO Colette Kress, along with management and the investor relations team, directly engaged with institutional investors to address the market's most pressing concerns regarding growth, competition, and products, aiming to explain the changing sources of its next phase of growth.

Morgan Stanley summarized the meeting's tone as "positive" in its post-meeting report, and NVIDIA's management offered an even more assertive assessment: Even with quarterly revenue approaching $100 billion, the company's current growth rate is expected to continue accelerating.

The core support for this judgment doesn't hinge on a single customer suddenly increasing purchases; rather, it stems from NVIDIA's transition from a company primarily dependent on GPU cycles and a few key customers towards a full-stack AI platform encompassing computing, networking, CPUs, models, and cloud infrastructure.

I. NVIDIA is Redefining Its Sources of Growth

According to NVIDIA's management during the meetings, the company's future demand primarily comes from three market categories: AI labs, traditional hyperscale cloud providers, and emerging customers including AI clouds, industrial enterprises, businesses, and sovereign AI.

This means the market's familiar narrative of "AI labs training large models, cloud providers buying GPUs" can no longer fully explain NVIDIA's next phase of growth.

1. AI Labs: ASIC Customers Are Also Increasing GPU Usage

Currently, AI labs account for approximately 20% of NVIDIA's total demand.

A noteworthy detail from the roadshow was that a leading frontier model customer, previously heavily reliant on ASIC development, initially had a low usage rate of NVIDIA's platform. However, NVIDIA's share of its related computing power has now increased to nearly 50%.

This at least indicates that the substitution of GPUs by ASICs is not a one-way path.

As model scale, inference load, and system complexity continue to rise, customers need to compare not just the price of a single chip, but the total cost at which the entire system can generate Tokens. For numerous real-world workloads, NVIDIA believes the lowest unit token cost still comes from its complete platform.

Other leading frontier models also primarily run on NVIDIA's platform. For NVIDIA, the opportunity with AI labs extends beyond just following the scaling of model training; it also includes regaining market share from customers who were previously more inclined towards their own chips.

2. Hyperscale Cloud Providers: Expanding from GPUs to Networking and CPUs

Under the new business scope, traditional hyperscale cloud providers remain one of NVIDIA's most important sources of demand, accounting for roughly half of the company's revenue.

However, the current constraints facing the cloud provider market are gradually shifting from chip supply to land, power, and physical space. Simply put, customers are not unwilling to continue investing, but are finding it increasingly difficult to rapidly expand data centers in the old ways.

In this context, NVIDIA is increasing its value capture within each data center – beyond GPUs, the company is expanding its addressable market through networking equipment, CPUs, interconnects, and rack-level system solutions.

Management reiterated the $20 billion CPU-related revenue target for this year during the meetings, hinting that a significant portion of this demand comes not from Head Nodes responsible for cluster control and scheduling, but from independent compute racks equipped with Vera CPUs.

Vera is not a general-purpose CPU merely designed to maximize core count; it is optimized for single-threaded workloads and memory access typical in AI data centers. The direction it represents is that NVIDIA is no longer just selling accelerator cards, but is further entering the realms of CPUs, networking, interconnects, and complete system solutions.

This also explains why Morgan Stanley believes that cloud providers' in-house ASIC development and NVIDIA's continued growth can coexist. After all, large cloud providers will continue developing and deploying custom chips, and ASIC suppliers like Broadcom may also maintain high growth. However, as long as the overall AI computing market expands rapidly enough, GPUs and ASICs do not have to engage in a zero-sum competition.

Morgan Stanley expects both NVIDIA's and Broadcom's AI-related businesses to maintain very high growth rates over the next year, suggesting the market may not see drastic share shifts in the short term.

3. Sovereign AI, Industrial & Neocloud: More Fragmented, Potentially Larger

Compared to AI labs and hyperscale cloud providers, demand from Sovereign AI, industrial enterprises, and Neoclouds is more fragmented and projects often take longer to start, but this may be the most noteworthy incremental market for NVIDIA in its next phase.

Geopolitics, data sovereignty, and supply chain localization are driving more countries and regions to build independent AI infrastructure. Concurrently, enterprises in finance, retail, biotech, manufacturing, etc., are starting to transform AI from a general-purpose tool into an integral part of their internal production systems.

Such projects typically require longer initiation, approval, and deployment cycles, but once they enter the implementation phase, the scale of individual projects can be substantial, and they often face less direct chip competition compared to the top-tier cloud market.

Neoclouds offer another growth model.

These new types of cloud providers, centered around GPU computing power, are absorbing demand that traditional cloud providers cannot meet in time. NVIDIA's partnerships with some Neoclouds may involve not only co-investment and credit support but also potential revenue-sharing mechanisms.

While the market currently focuses more on whether NVIDIA is assuming credit risk for its customers, on the flip side, revenue sharing implies NVIDIA could share in the long-term returns from downstream GPU cloud services. Based on this, Morgan Stanley believes that in the future, NVIDIA may not just sell hardware to Neoclouds but could gradually become a stakeholder in a vast GPU cloud network.

II. ASICs, Rubin, and Memory Constraints – What Truly Affects Growth?

Realistically, the biggest debates surrounding NVIDIA today are not about whether AI will still grow, but whether chip competition, product roadmap issues, and supply constraints will diminish the company's share in this growth cycle.

Based on information from these roadshows, NVIDIA's response is that these problems are real, but they have not yet changed the company's core growth trajectory.

1. ASICs Will Grow, But Doesn't Necessarily Mean GPUs Will Lose Share

For stable, mature, and sufficiently large workloads, ASICs can indeed offer lower chip costs and better customization efficiency. However, model architectures, inference methods, and development tools are still evolving rapidly. Customers need flexibility, a software ecosystem, and system delivery capability simultaneously.

Therefore, what truly determines customer choice is not the selling price of a single chip, but the total cost of model training, inference, networking, memory, and software working in concert.

NVIDIA's moat is no longer just GPU performance, but the platform capability built from CUDA, networking, CPUs, interconnects, complete system solutions, and model tools.

2. Rubin Roadmap Shows No Material Delay Yet

The roadshow also addressed recent controversies surrounding the Vera Rubin product roadmap.

NVIDIA denied market rumors that Rubin Ultra has been delayed to 2028, confirming the product is still planned for shipment in 2027. However, it also acknowledged that some rack configurations will be adjusted. The original Kyber rack solution will be replaced by a design management describes as "superior."

This change likely supports a larger scale-up domain within a single rack, but it does not signify a change in the core technical direction. Key technologies like the 800V power architecture and optical interconnects across racks are proceeding as originally planned.

For NVIDIA, attempting more aggressive system designs with each product generation is part of maintaining its leadership. What truly needs watching is not whether the roadmap has undergone adjustments, but whether the company can correct course promptly before mass production and manage large-scale delivery risks.

Morgan Stanley believes Vera Rubin will still be a significant product cycle driving NVIDIA's growth over the next 12 months.

3. Memory Shortages: Another Issue Easily Misread by the Market

Management expects memory supply constraints could persist for several years.

If the AI industry aims for order-of-magnitude token growth annually, while memory supply cannot expand synchronously, merely increasing the number of GPUs is insufficient to solve the problem. The configuration relationships between compute, networking, and memory must be redesigned accordingly.

One potential adjustment is reducing the amount of LPDDR5 configured per rack, allowing the limited memory supply to support more rack deliveries. Another direction involves relying more on networking, caches, and faster on-chip memory to reduce dependence on traditional DRAM in certain scenarios.

Management also mentioned related technologies using SRAM as a primary memory architecture. SRAM is typically more expensive than DRAM, but for specific inference workloads, its low latency and high bandwidth could offer system-level value.

In the short term, these statements may impact market sentiment towards some memory companies, but the logical starting point is not weakening memory demand. Quite the opposite, NVIDIA needs to continuously adjust its architecture because the company predicts that memory supply will struggle to fully meet the demands of AI computing growth in the long run.

Therefore, for the memory industry, what truly matters is not whether NVIDIA reduces the per-system configuration of a certain memory type, but how the value of memory within AI systems will be redistributed among HBM, LPDDR, SRAM, caches, and networking.

4. The Importance of Nemotron and Open Models

Beyond hardware, NVIDIA is also strengthening the role of open models and enterprise AI software.

Using examples like circuit design, management pointed out that general-purpose closed-source models may not meet enterprise requirements for specialized knowledge, data security, and workflow control. What enterprises truly need is often not directly calling an external model, but building a controllable, customizable AI system around their own data and expertise.

This is the significance of open models like Nemotron.

They allow enterprises to train, fine-tune, and deploy models based on their own business needs while retaining control over the model, data, and infrastructure. For NVIDIA, open models are more than just a software product; they are a crucial entry point connecting GPUs, networking, inference frameworks, models, and enterprise applications.

What NVIDIA aims to build is no longer just a set of high-performance computing hardware, but a complete AI technology stack that enterprises can fully control and deploy.

III. How Does Morgan Stanley Value NVIDIA?

Another important goal of this roadshow was to expand NVIDIA's coverage among value-oriented investors.

As is well known, over the past few years, NVIDIA has been primarily viewed as a classic high-growth asset. However, as the company's market cap and institutional holdings have expanded significantly, many growth-oriented funds are already heavily invested in NVIDIA. Some institutions are even nearing their internal single-name position limits. Therefore, for NVIDIA, the potential for continued allocation increases solely from growth capital is becoming limited.

Consequently, NVIDIA needs to provide the market with another valuation framework.

Management stated that from this point forward, the company will allocate 50% or more of its cash flow to shareholder returns. In this context, increasing share buybacks and cash returns allow NVIDIA to maintain its high-growth attributes while gradually acquiring the value characteristics of a large, mature technology company.

In other words, NVIDIA wants the market to value it using two frameworks simultaneously: On one hand, it remains an AI infrastructure company capable of high-speed growth; on the other hand, it is becoming a mega-cap tech platform capable of generating and returning massive amounts of cash.

Based on this assessment, Morgan Stanley continues to rank NVIDIA as its top pick in the semiconductor sector, maintaining an "Overweight" rating and a $288 price target, outlining three risk-reward scenarios:

- Base Case: Price target of $288, based on approximately 22x calendar year 2027 EPS of $13.08. The report expects NVIDIA's revenue to grow 82.0% in 2026 and 52.4% in 2027.

- Bull Case: Price target of $330, based on approximately 23x calendar year 2027 EPS of $14. Core assumptions include sustained high growth in the data center business, with networking, Vera Rubin systems, and software revenue driving a higher premium for NVIDIA's full-stack AI computing platform. Further upside could come from the scaling of AI PC, autonomous driving, and robotics businesses, as well as a higher revenue mix from high-margin software and AI services.

- Bear Case: Price target of $160, based on approximately 16x calendar year 2027 EPS of $10. Key risks include data center supply catching up to demand faster, leading to a significant slowdown in AI infrastructure growth; customers reducing dependence on NVIDIA through in-house ASICs; competitors like AMD regaining market share; and negative impacts from tariffs and export restrictions exceeding expectations.

Regarding earnings projections, Morgan Stanley forecasts NVIDIA's GAAP revenue for 2026-2029 to reach $215.938 billion, $393.005 billion, $598.809 billion, and $783.877 billion, respectively; gross margins of 71.3%, 74.4%, 72.5%, and 72.0%; and EPS of $4.61, $8.96, $13.08, and $17.63.

The core judgment behind these forecasts is that even with NVIDIA's already massive revenue base, the expansion of AI infrastructure is still expected to drive relatively high revenue and profit growth for several years. Networking, CPUs, software, and system-level solutions will contribute more incremental value beyond GPUs.

Of course, Morgan Stanley acknowledges that memory, networking, and other supply chain segments might have higher earnings elasticity in certain phases. In fact, during past semiconductor cycles, Morgan Stanley has rotated its top sector pick from NVIDIA to companies like SanDisk and Micron.

However, from a risk-reward perspective, Morgan Stanley still considers NVIDIA one of the most attractive core assets in the semiconductor sector.

On one hand, the company's current valuation multiple might be constrained by its mega-cap size and index weighting. On the other hand, compared to other computing semiconductor companies like AMD and Broadcom, NVIDIA does not command a particularly significant valuation premium. Morgan Stanley believes that as growth sources further diversify and cash returns increase, the valuation gap between NVIDIA and some of its peers may eventually converge.

However, market positioning does not reflect uniform optimism. The report indicates that active institutional ownership has reached 50.9%, suggesting a high position basis among growth investors. Meanwhile, Morgan Stanley's quantitative model places NVIDIA's assessment for the next 3 and 24 months in the 4th quintile, not yet entering the range most favored by quantitative capital (1st quintile being most favored, 5th quintile least favored).

This creates a subtle aspect in NVIDIA's current valuation: fundamental expectations remain strong,