When the market has "priced in perfection" in advance, even Samsung Electronics' strong earnings are not enough.

- Core Thesis: Although Samsung Electronics' Q2 operating profit surged 19 times year-over-year to a record high, even surpassing Nvidia, because the market had already priced in "perfect" expectations, the earnings release triggered profit-taking, leading to a sharp single-day stock decline. This highlights the "buy the rumor, sell the news" trading logic.

- Key Factors:

- "Seemingly perfect" earnings: Q2 operating profit of 89.4 trillion KRW (approx. $58.4 billion) beat expectations, and revenue doubled to 171 trillion KRW. However, the stock price once fell 8%, and other chip stocks like SK Hynix also came under pressure.

- Market focus shift: Investors are no longer solely focused on profit growth but are turning their attention to the sustainability of free cash flow improvement and shareholder return policies. Pessimistic views suggest that valuations are no longer safe.

- Macro backdrop warning: Meta's hint at curbing AI capital expenditure triggered the largest two-day sell-off in high-beta momentum stocks since the pandemic, and the high-valuation logic of the memory chip sector faces a systemic revaluation.

- Emerging structural issues: Losses in the foundry and logic chip business may widen. Additionally, special bonus provisions related to compensation agreements were booked; excluding this cost, operating profit would have been even more above expectations.

- AI demand supports industry activity but marginal trends are weakening: Memory supply shortages are expected to last at least until 2027, but Counterpoint warns that high profit margins of 75-80% could attract regulatory pressure.

Original Author: Dong Jing

Original Source: Wall Street CN

Samsung Electronics delivered a historic quarterly report with a 19-fold surge in profit, only to see its stock price plunge sharply on the day of the announcement. It's not that the performance was insufficient; rather, the market had already priced in "perfection" – the earnings release merely served as a signal for capital to exit.

On July 7, a Wall Street CN article reported that Samsung Electronics' second-quarter operating profit soared approximately 19 times year-over-year to 89.4 trillion won (about $58.4 billion). This not only set a new quarterly record but also surpassed Nvidia's operating profit of $53.536 billion in the previous quarter, making Samsung the world's most profitable company on a quarterly operating profit basis. Revenue doubled to 171 trillion won, both figures exceeding analysts' average expectations. However, after the earnings release, Samsung's stock price plunged up to 8% in a single day, dragging South Korea's KOSPI index down 6%, while SK Hynix fell over 7%.

Another Wall Street CN article highlighted that the "buy the rumor, sell the news" logic played out once again. On the eve of the earnings release, the Philadelphia Semiconductor Index in the US rose 2.2% in a single day, the S&P 500 gained 0.7%, and the Nasdaq 100 climbed 1.3%. As the positive news materialized, capital quickly rotated out.

Brian Cho, portfolio manager at Causeway Capital Management, stated bluntly that what the market really wants to see is whether improvements in free cash flow can translate into sustainable, step-change growth, and how management will treat shareholder returns – the pricing logic has shifted from "how fast are profits growing" to "can these profits be converted into real cash distributed to shareholders."

Furthermore, the sharp reversal in market sentiment has a macroeconomic backdrop. Last week, Meta signaled it would rein in capital expenditure, triggering the largest two-day sell-off in high-beta momentum stocks since the COVID-19 pandemic. Samsung's decline also pressured peer chip stocks SK Hynix and Micron, and the high-valuation logic for the entire memory chip sector is facing a systemic reassessment.

Brilliant Performance, But Not Good Enough

A Wall Street CN article noted that Samsung's second-quarter operating profit is estimated at 89.4 trillion won, up 56% quarter-over-quarter, beating the average analyst forecast of 84.2 trillion won. Revenue for the period was 171 trillion won, exceeding the market estimate of 169.2 trillion won and representing a year-over-year increase of approximately 129%. The company plans to release its complete financial report on July 30, which will disclose net profit and segment data for each business unit.

The core driver of this growth is the continued tight supply of memory chips. Robust demand from AI data centers for High Bandwidth Memory (HBM) has led manufacturers to prioritize capacity for high-end products, causing a shortage of traditional DRAM and NAND memory chips and driving prices higher across the board.

According to HSBC data, average selling prices (ASPs) for DRAM rose over 40% quarter-over-quarter in Q2, while NAND prices increased over 50%. Citigroup Research data is similar, showing Q2 DRAM and NAND ASPs up 44% and 53% quarter-over-quarter, respectively.

However, while the 171 trillion won revenue exceeded the average analyst estimate, it fell short of some institutions' optimistic forecast of 173.9 trillion won. Against a backdrop of already elevated valuations, even this slight shortfall was enough to trigger profit-taking.

The brilliance of the memory business masks several cracks in the company's overall structure. Analysts expect losses in Samsung's foundry and logic chip (LSI) business to have widened further in the quarter, partly due to bonus expenses being proportionally allocated to the overall cost of the semiconductor division.

In May, Samsung reached a compensation agreement with its chip division employees, linking performance bonuses to operating profit. It stipulated that, provided specific profitability targets are met, 10.5% of the semiconductor division's annual operating profit would be set aside for special bonuses. Some analysts point out that without this provision, Samsung's operating profit would have exceeded market expectations even further.

AI Demand Supports Memory Boom, But Marginal Signals Weaken

The core logic driving this memory chip super-cycle remains intact: the massive global expansion of AI data centers is fueling strong demand for high-end memory chips, and memory shortages have become a key bottleneck for AI development.

Multiple industry executives, including Nvidia CEO Jensen Huang and OpenAI COO Brad Lightcap, have issued warnings on this issue. Major manufacturers are prioritizing supply for high-end memory products, leading to simultaneous shortages in traditional memory. Analysts expect the supply shortage to persist at least until 2027.

Market research firm Counterpoint estimates that the average operating profit margin for the three major memory manufacturers – Samsung, SK Hynix, and Micron – will remain in the 75% to 80% range in the second quarter. In its report, the firm noted that some views consider such high profit margins as "excessive profiteering" and warned that "if this situation persists, memory manufacturers could face regulatory pressure."

Furthermore, a Wall Street CN article mentioned that more noteworthy than the earnings themselves are signals emanating from the upstream supply chain. Meta recently hinted at capping its AI capital expenditure, which the market interpreted as an early warning that tech giants' AI infrastructure investment might be peaking. This directly triggered one of the most severe two-day sell-offs in high-beta momentum stocks since the start of the COVID-19 pandemic.

The team at BlackRock Investment Institute, led by Jean Boivin, put the issue more directly: The core of the AI bubble debate is not current valuations, but whether future profits can be sustained at extraordinary levels. If AI fails to translate its current scarcity into genuine productivity improvements, the currently sky-high profit expectations will face a correction.

Samsung Lags Behind SK Hynix, Korea Bets on AI Chip Dominance

From a national strategic perspective, the South Korean government views Samsung and SK Hynix as core pillars in its quest for global AI leadership. Samsung Group and SK Group each plan to build two chip factories in southwestern South Korea, with a combined investment of 800 trillion won to rapidly expand capacity. South Korea aims to double its memory chip production capacity within five years, and Samsung has announced it will invest over $70 billion in capacity expansion and R&D by 2026.

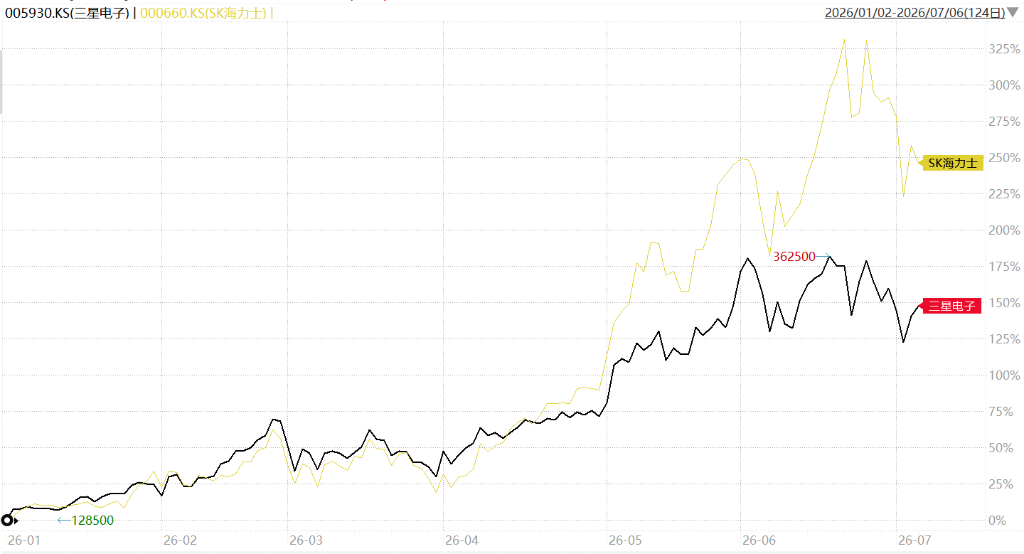

In terms of stock performance, Samsung has rallied approximately 165% year-to-date, but this significantly underperforms competitor SK Hynix's gain of about 260%. The gap is primarily due to differences in product mix. SK Hynix's business is highly concentrated on high-end memory chips catering to AI computing demands, whereas Samsung's product portfolio is more diversified, spanning both chips and consumer electronics. This divergence sends a clear signal: in the current race, focus, rather than scale, is favored by capital.

Samsung's complete financial report will be released at the end of this month. The breakdown data for each business segment will then tell the market how much real value has been generated from this wave of AI capital expenditure. That number will serve as a key reference coordinate for the next phase of the AI hardware investment thesis.