半年狂揽5GW:SemiAnalysis拆解Meta算力棋局,市场抛售系误读

- 核心观点:SemiAnalysis报告反驳市场担忧,认为Meta在2026年上半年签下超5GW云和托管容量(不含自建),新增算力并非仅用于低价转售,而是作为“可选算力池”,可在前沿模型训练、广告推荐、高溢价外部交易等多场景调配,对CoreWeave等Neocloud供应商的RPO可能构成利好而非威胁。

- 关键要素:

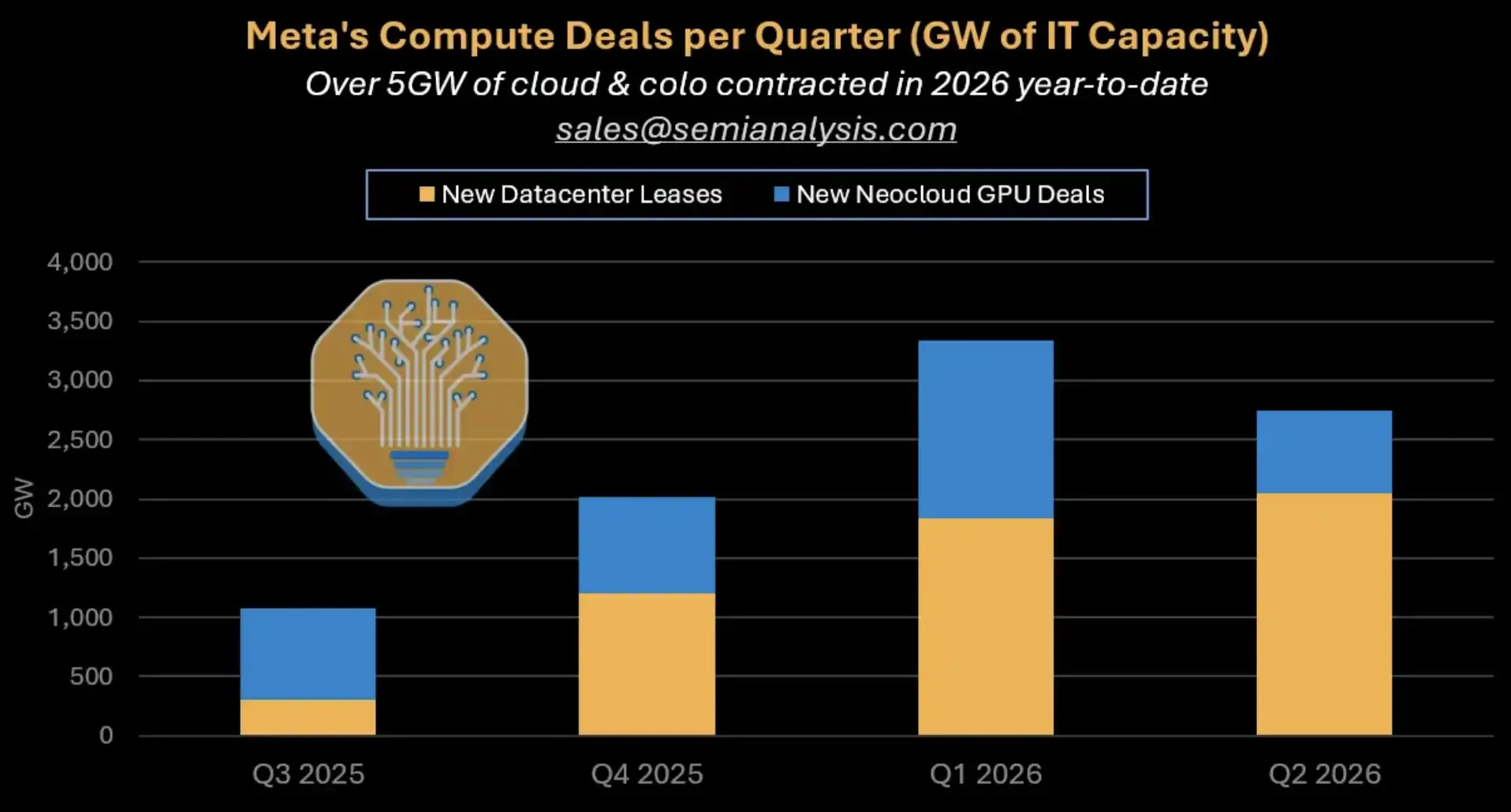

- Meta自2024年初累计签署近10GW合同,其中2026年上半年云和托管签约超5GW,大部分新增容量通过第三方Neocloud实现,而非自建。

- 市场因担心Meta从买方变卖方导致CoreWeave、Nebius股价抛售,但报告认为新增算力有四条高价值消化路径:MSL训练、广告推荐、Claude私有实例、高价短期交易。

- 广告推荐系统是稳定消化途径,Meta称GEM训练GPU翻倍后,Instagram和Facebook Feed广告转化率分别提升5%和3%,提升广告定价能力。

- 类似SpaceX的高价短单年化每GW收入高达31-48亿美元,是典型Neocloud五年IaaS均价的2.6-4倍;若Meta仅拿出200MW,年化收入可能超100亿美元。

- CoreWeave、Nebius等供应商风险并非来自需求消失,其与Meta分别有210亿和最高270亿美元合同;Meta仍愿为速度支付溢价,但大客户集中度和合约灵活性是估值风险。

- 关键风险是MSL前沿模型追赶OpenAI和Anthropic的不确定性;若多条路径无法消化,超5GW外采算力将直接变成资本开支压力。

TL;DR

- Meta has signed over 5GW of cloud and colocation capacity in the first half of 2026, excluding its simultaneously accelerated self-built data centers.

- The new computing power could be directed to MSL training, ad recommendation systems, private instances of Claude, and short-term, high-premium external deals.

- CoreWeave and Nebius' RPO may benefit, but risks remain from MSL's progress catch-up and contract flexibility.

The recent sell-off in Neocloud stocks triggered by Meta may be misplaced. SemiAnalysis released a report on July 2nd stating that Meta has already signed over 5GW of IT capacity in cloud services and colocation for the first half of 2026, and this figure does not include its concurrently accelerated self-built data centers.

This contradicts market concerns over the past few days. According to Bloomberg on July 1st, Meta is developing a cloud business to sell its excess AI computing power. The plan is still in development and the strategy could change. Following the news, shares of Neocloud companies like CoreWeave and Nebius were sold off, as investors feared Meta would transform from a major customer into a potential competitor, leading to a rapid oversupply of AI data centers.

The main narrative from SemiAnalysis offers an alternative interpretation: Meta is not reducing external procurement but is instead using third-party Neocloud providers to secure capacity faster. Since the beginning of 2024, Meta has signed contracts totaling nearly 10GW, and most of the new capacity is still sourced through third parties. For suppliers like CoreWeave and Nebius, Meta's orders could actually continue to boost their Remaining Performance Obligations (RPO).

Meta's quarterly compute capacity transactions breakdown: Cloud and colocation contracts signed in H1 2026 exceed 5GW, distinguishing between new data center leases and Neocloud GPU deals.

Market Fears Meta Becoming a Seller, Report Sees a Larger Buyer

The crux of this debate is not whether Meta might dabble in cloud computing power resale, but rather who will build, absorb, and bear the revenue risk for the massive new capacity.

If Meta were merely to sublease its GPUs, becoming a bare-metal IaaS provider with a ~30% gross margin, then the market's concern over Neocloud valuations would be justified. A major customer turning into a supplier weakens the bargaining power of existing providers and could lead to price competition.

However, within SemiAnalysis's framework, Meta's new capacity functions more like a "flexible compute pool." It can be allocated among internal frontier model training, ad recommendation, enterprise-level model services, and short-term, high-premium external deals, rather than simply being subleased at low prices.

This is also crucial to countering the claim that "only 5GW of data centers are under construction in the US." Just Meta's two largest campus projects under construction account for approximately 2.5GW of capacity. Adding third-party cloud and colocation contracts, the actual construction intensity is higher than some pessimistic estimates.

In simpler terms, the market's question is not whether Meta is buying computing power, but whether all this capacity can be absorbed by high-value scenarios.

Four Pathways to Absorb New Compute Power, MSL is Not the Only Outlet

The top priority for Meta's new compute power remains Meta Superintelligence Labs (MSL) for frontier model training. This is the most direct narrative for capital expenditure: Meta needs large enough training clusters, talent, and room for trial and error to catch up with OpenAI and Anthropic.

But even if MSL progress falls short of expectations, Meta isn't forced to lease out its GPUs cheaply.

The second path is its advertisement recommendation system. Meta's official financial reports show that in Q1 2026, ad impressions grew 19% YoY, and average price per ad grew 12% YoY. Meta Engineering previously noted that the GEM training stack achieved a 23x increase in effective training FLOPs, ~1.43x improvement in MFU, and a 16x increase in GPU scale. After doubling the training GPUs, conversion rates for Instagram and Facebook Feed ads increased by 5% and 3%, respectively.

This path is easier for investors to understand: if more computing power can improve ad conversion rates, it's not just "burning money on GPUs" but part of ad revenue and pricing power. Regarding the specific ranking metric improvements mentioned in the report, limited independent public verification exists, making them more suitable as assumptions in SemiAnalysis's model rather than fully confirmed facts from Meta.

The third path is a model service platform, akin to AWS Bedrock or Google Vertex. SemiAnalysis states that Meta is negotiating with Anthropic regarding private instances of Claude and is attempting to build a "tokens-as-a-service" platform. This capacity can be used internally or sold to SaaS providers and externally distributed, but related deals should be viewed as "potential" rather than realized revenue.

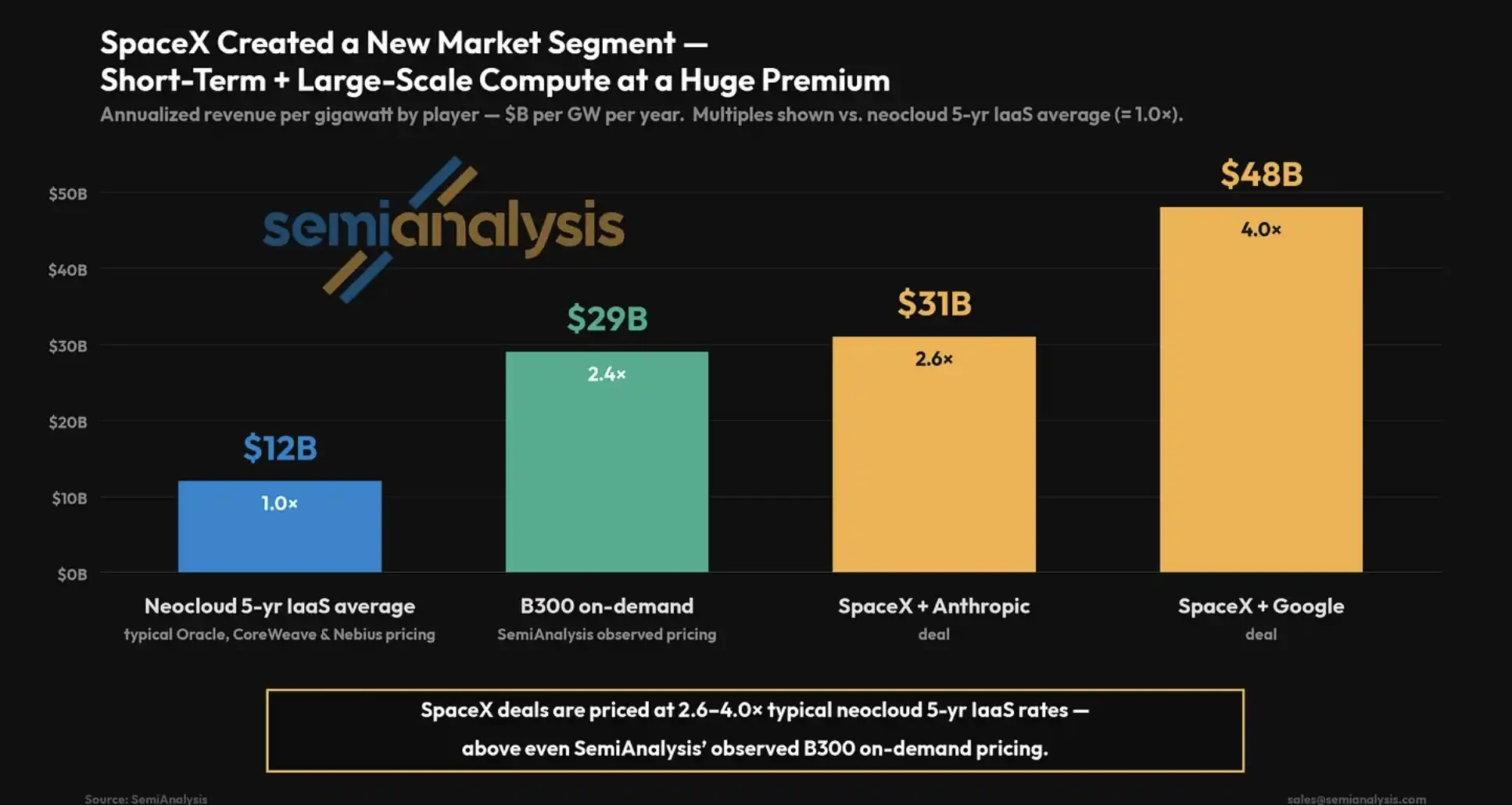

The fourth path is large-scale, short-term, high-premium on-demand compute deals, similar to SpaceX's approach. This is arguably the most striking set of figures in the report.

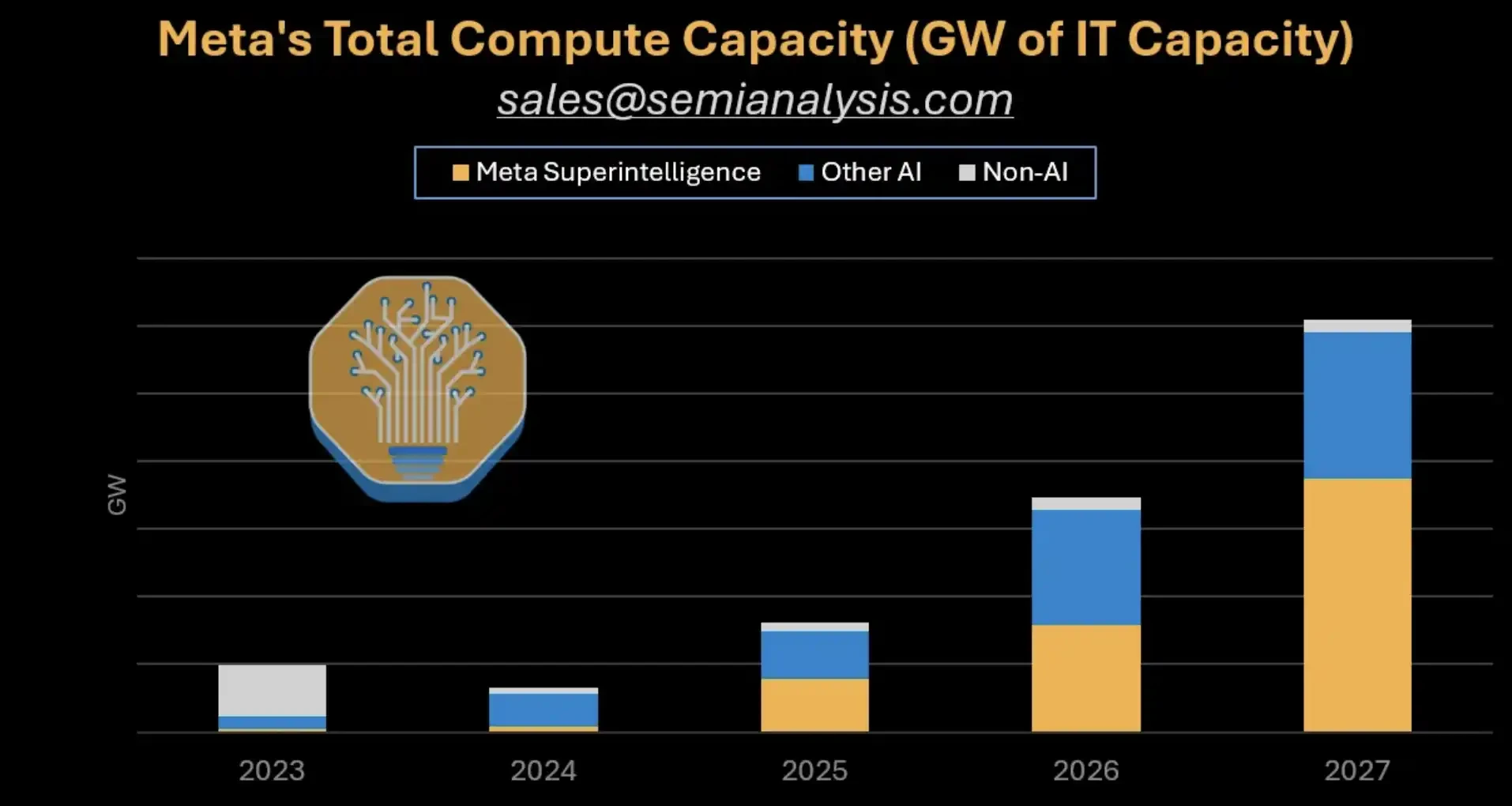

Meta's total compute capacity forecast: Stacked bar chart from 2023 to 2027, distinguishing between MSL, Other AI, and Non-AI, showing significant expansion in 2026-2027.

High-Premium Short-Term Deals Reshape the Revenue Potential of "Selling Compute"

The key to the SpaceX-style deal isn't just "renting GPUs," but the different pricing and contract structure.

SemiAnalysis estimates that the annualized revenue per GW for SpaceX's deals with Anthropic is approximately $3.1 billion, which is 2.6 times the typical Neocloud 5-year IaaS average price. The deal with Google was even higher, at roughly $4.8 billion/GW/year, or 4 times the average. Independent public sources confirming these contract details are limited, so these figures are best understood as scenarios within the report, illustrating the potential for high premiums on scarce short-term compute capacity.

If Meta allocates just 200MW for similar external transactions, the annualized revenue could exceed $10 billion, based on calculations in the report's public slides. This scale could change the market's intuition about "Meta selling compute externally": it doesn't have to be a low-margin sublease but could involve selling time windows to compute-starved top-tier clients using its rapidly deployable data center capacity.

The report also notes that Meta's rapidly deployable data center design is suited for these types of deals. Its value lies not in the lowest cost for long-term leases, but in faster delivery when model companies, AI applications, or large clients urgently need contiguous blocks of compute power.

However, this remains an optional path, not a stable, realized revenue stream. Conditions allowing Meta to replicate a portion of this high-premium contract structure do not equate to it having already become a SpaceX-style compute seller.

SpaceX pricing premium comparison: Typical Neocloud 5-year IaaS costs ~$1.2B/GW/year, SpaceX & Anthropic ~$3.1B, SpaceX & Google ~$4.8B.

Pressure on CoreWeave, Nebius May Not Stem from Vanishing Demand

For Neocloud firms like CoreWeave and Nebius, the previous market concern was this: If Meta builds its own capacity or resells compute, its external procurement would decrease, potentially draining industry orders.

However, based on existing contracts, Meta is still accelerating its use of third-party Neocloud providers. Public data shows CoreWeave has a $21 billion contract with Meta, and Nebius' contract with Meta could reach up to $27 billion. In its Q1 2026 shareholder letter, Nebius stated it secured a second major deal with Meta, with a contract capacity exceeding 3.5GW, and mentioned commitments from Microsoft and Meta.

Meta's willingness to pay a premium for speed is why third-party suppliers still hold value. As long as Meta believes the compute can be absorbed by MSL, its ad system, model services, or short-term high-premium deals, it has reason to let Neocloud providers build clusters first, rather than waiting for its own projects to slowly come online.

"Capacity oversupply" can't be judged by total gigawatts alone. What's truly scarce in AI data centers often isn't paper power, but available GPUs, networking, data center delivery speed, customer migration costs, and contract flexibility. If Meta needs large amounts of contiguous capacity quickly, third-party Neocloud providers remain useful.

This isn't to say Neocloud companies are risk-free. Their valuations still depend on large customer concentration, financing costs, GPU depreciation, long-term contract quality, and whether customers will actually consume the future capacity. If the RPO growth driven by Meta corresponds to high capital expenditure and high customer concentration, the market will still apply a discount.

If MSL Lags, 5GW Becomes a Capital Expenditure Burden

The most cautious part of this report is recognizing that not every optional path for Meta is a guaranteed success.

Whether MSL can catch up to OpenAI and Anthropic remains highly uncertain. Frontier model competition isn't solved by GPU count alone. Data strategy, research team quality, training stability, product distribution, and inference costs all affect outcomes.

Contract terms also influence risk. SemiAnalysis suggests that SpaceX-style deals often include a 90-day mutual cancellation clause. This arrangement provides flexibility for both sides: if a team's progress stalls, compute can be quickly reclaimed; if demand changes, neither party is locked in long-term. Details of these clauses lack independent public confirmation and are best treated as report assumptions.

For Meta, flexibility itself holds value. It can allocate sufficient power and GPUs to MSL for frontier attempts while diverting some capacity to ad recommendations, private Claude instances, or high-premium short-term deals.

Conversely, if Meta ends up signing a large volume of long-term compute deals lacking flexible exit options, the risk increases. If frontier model progress falters and the ad system or model services cannot absorb the new capacity, the over 5GW of newly procured external compute power could become a significant capital expenditure pressure more directly.