Chip stocks fell for two consecutive sessions as AI "horror stories" mount: Meta and Anthropic相继传出新动作,prompting the market to reassess AI trades?

- Core Viewpoint: News of Meta exploring the commercialization of AI computing power and Anthropic developing its own chips has triggered a market repricing of the AI industry, shifting the focus from "competing on capital expenditure" to "competing on capital efficiency." This has led to a significant correction in chip stocks, not because AI demand has peaked, but because the industry is entering a new phase that emphasizes return on investment.

- Key Elements:

- Meta plans to commercialize or lease its surplus AI computing power externally, aiming to improve the return rate on its tens of billions of dollars in AI infrastructure investment.

- Anthropic is in discussions with Samsung to develop its own AI chips, potentially using a 2-nanometer process, aiming to reduce long-term computing costs and lessen dependence on a single supplier.

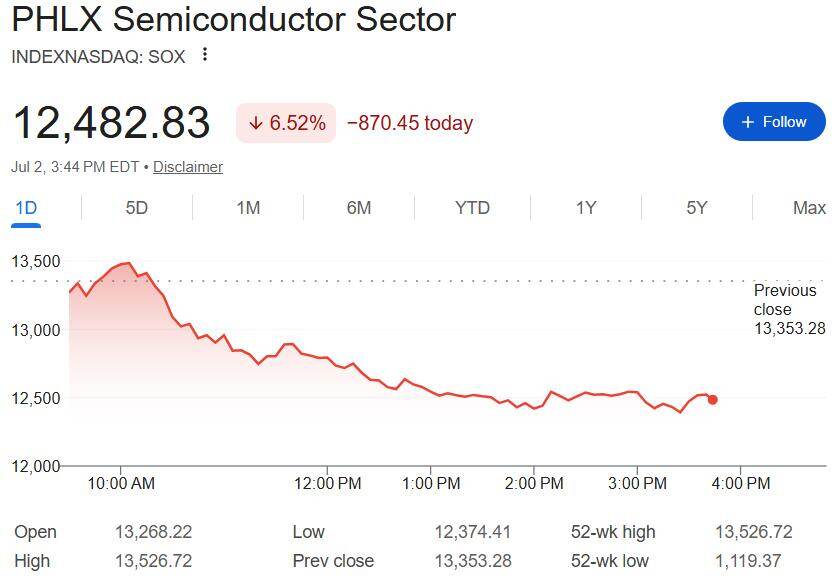

- These two pieces of news have jointly prompted the market to reassess the AI capital expenditure super cycle. The Philadelphia Semiconductor Index has fallen over 10% cumulatively in two days, with semiconductor equipment and memory sectors leading the decline.

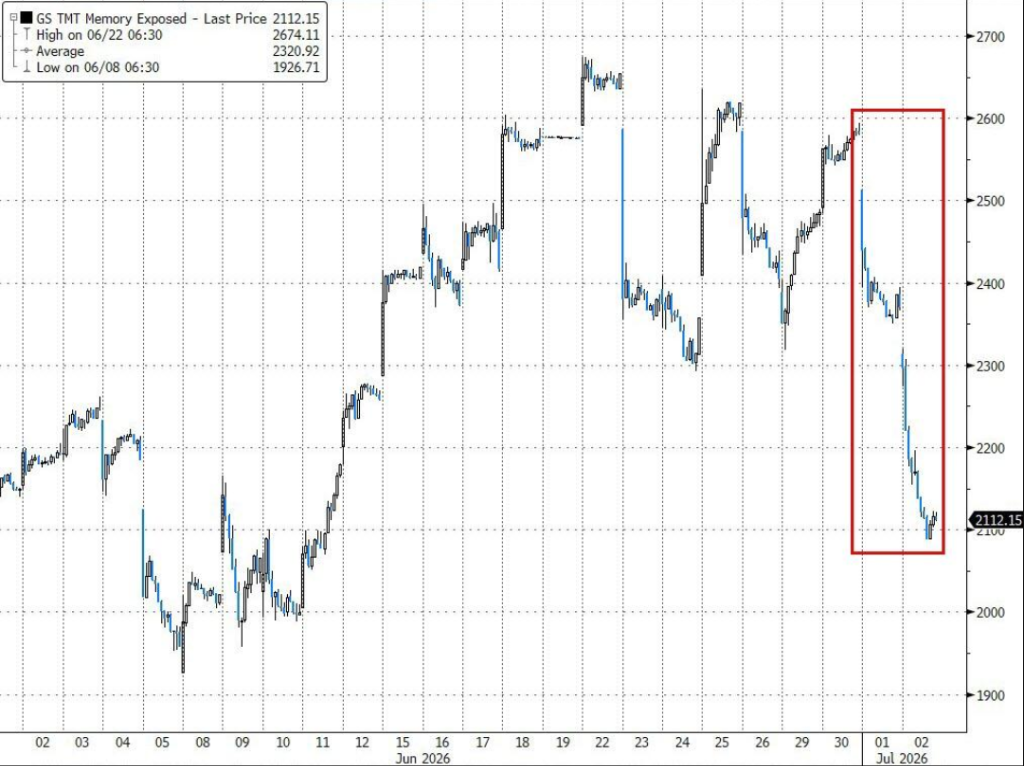

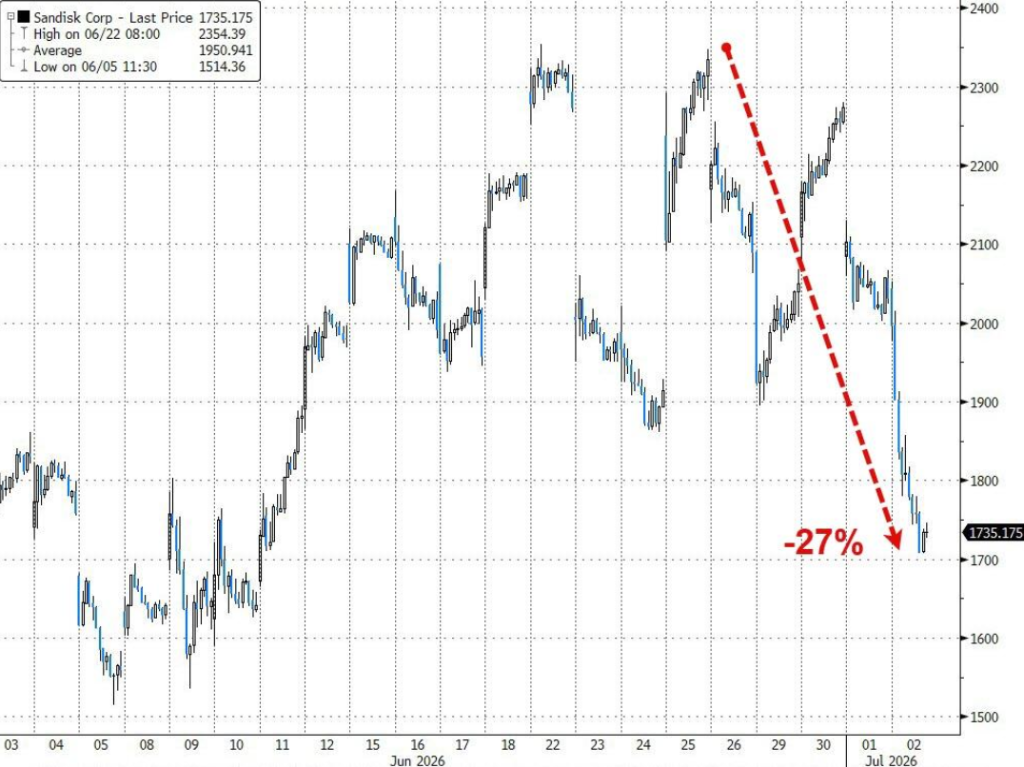

- Goldman Sachs' basket of memory stocks has fallen over 18% in the past two days, marking their most severe two-day drop in 12 years, with SanDisk entering bear market territory.

- Institutions believe the market is not negating AI demand but reassessing the trading logic. AI application penetration remains low, and infrastructure demand exists long-term.

- Competition in the AI industry is shifting from "who invests more" to "who can generate a higher return on every dollar of capital expenditure," with business models placing greater emphasis on creating a closed loop.

Original Authors: Li Dan, Ye Zhen

Original Source: Wall Street News

The AI hardware sector has seen adjustments for two consecutive days, but what truly captured market attention was not the chip companies themselves, but the latest moves from two major AI model companies.

On Wednesday, news emerged that Meta is exploring the commercialization of its surplus AI computing power. The following day, reports indicated that Anthropic is in discussions with Samsung Electronics to collaborate on developing its own AI chips, potentially utilizing Samsung's 2-nanometer process for manufacturing.

Although seemingly unrelated, these two pieces of news collectively touch upon the most sensitive topic in the current AI industry chain – is the AI capital expenditure that has been rapidly expanding for two years entering a new phase?

The market responded by repricing first. U.S. chip stocks have been on a sustained decline over the past two days. The Philadelphia Semiconductor Index (SOX) fell over 10% cumulatively on Wednesday and Thursday, marking its worst two-day drop in nearly a month. The semiconductor equipment sector, most sensitive to the capital expenditure cycle, led the decline. Teradyne (TER), Entegris (ENTG), KLA Corporation (KLAC), Applied Materials (AMAT), and Lam Research (LRCX) all fell over 10% intraday on Thursday. European chip giant ASML's U.S. stock (ASML) once dropped over 5% on Thursday.

Goldman Sachs' basket of AI semiconductor stocks was hit hard, recording its worst two-day performance since tariff day.

Memory stocks suffered severe losses. Goldman Sachs' basket of memory stocks fell over 18% in the past two days, the sharpest two-day decline in 12 years.

SanDisk even entered bear market territory.

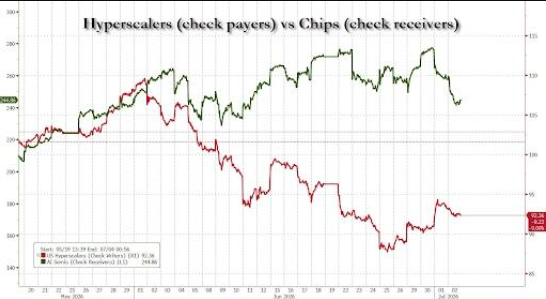

In contrast to the sharp performance of capital recipients like chip companies, the stock prices of hyperscale cloud service providers, who are the capital spenders, have somewhat stabilized.

However, many institutions believe that these two pieces of news are more like catalysts for the market to re-evaluate the AI investment thesis, rather than a fundamental reversal in the health of the AI industry. The market is truly trading not on whether "AI demand has peaked," but on the AI industry transitioning from a "battle of capital expenditure" to a "battle of capital efficiency."

The Market's Real Concern Isn't Anthropic Making Chips, but the Changing Logic of AI CapEx

Over the past two years, the AI hardware sector has been on a tear, driven by a core narrative that has barely changed: rapid iteration of AI models leading to sustained explosive demand for computing power, chronic GPU supply shortages, and tech giants continuously raising capital expenditure. This has triggered an unprecedented "AI capital expenditure super-cycle" driving demand for GPUs, High Bandwidth Memory (HBM), high-speed networking, advanced packaging, and semiconductor equipment.

This logic not only propelled Nvidia to become the world's most valuable company but also made equipment makers like Applied Materials, Lam Research, ASML, and KLA, as well as memory manufacturers like Micron Technology and SanDisk, the biggest winners in the capital market.

However, the two pieces of news appearing on consecutive days this week have led the market to seriously discuss: If the AI industry begins to focus more on capital efficiency rather than merely expanding investment, will this capital expenditure super-cycle enter a new phase?

On Wednesday, reports indicated that Meta is planning to build an AI cloud computing business, potentially opening AI models deployed on its infrastructure to external customers or directly leasing surplus AI computing power to commercialize returns on its tens of billions of dollars in AI infrastructure investment.

Then, on Thursday, news broke that Anthropic is discussing developing its own AI chips.

Viewed in isolation, the two companies are taking different paths. But together, they point to a shift – AI companies are starting to think about how to improve the return on investment of existing infrastructure, not just how to continue expanding capital expenditure.

It is this change in expectations that has triggered a market re-evaluation of the AI trading logic.

Anthropic's Custom Chip Signals the Beginning of a 'Cost Optimization Era' for AI Companies?

More significant than the market's initial concern about "whether custom chips will reduce GPU procurement" is the business logic behind Anthropic's move.

Reports suggest that Anthropic is in discussions with Samsung Electronics to develop custom chips tailored for AI training and inference, though these talks are still in their early stages.

If it proceeds, Anthropic would join Google, Amazon, Microsoft, and Meta as another foundational model company venturing into proprietary AI chip development.

This does not necessarily mean abandoning Nvidia GPUs; rather, it represents a natural evolution of the AI industry.

Over the past two years, the primary competitive focus for major model companies was acquiring more GPUs and building more data centers. However, as model scales continue to grow, training and inference costs are rising rapidly. Reducing the cost per token, improving computing power utilization, and decreasing reliance on a single supplier are becoming new competitive priorities.

ASICs designed for specific models can achieve a better balance between performance, energy consumption, and cost. This is the key reason behind the sustained push for Google's TPUs, Amazon's Trainium, and Meta's MTIA in recent years.

In this sense, Anthropic's exploration of custom chips looks more like a significant marker of the AI industry shifting from "competing on investment" to "competing on efficiency," rather than a cutback in AI investment.

Meta and Anthropic: Two Different Paths, One Shared Goal

Meta and Anthropic are adopting different strategies, but their objectives are highly aligned.

Meta aims to generate revenue from temporarily idle AI computing power, improving the return on its tens of billions in capital expenditure. Anthropic seeks to reduce long-term computing costs through custom chips, enhancing its autonomy over infrastructure.

Whether it's selling surplus computing power or developing ASICs, neither action is essentially about reducing AI investment. Instead, both are seeking more sustainable AI business models.

However, for the capital market, these two news items can easily trigger a different association: if AI companies start paying more attention to capital efficiency, will future GPU procurement, cloud computing leasing, and new data center investments maintain the same high growth rates as the past two years?

Consequently, the market has begun to reassess whether expectations for AI capital expenditure can continue to be virtually "ever-increasing."

This explains why, during the market adjustment over the past two days, the steepest declines were not among model companies, but among semiconductor equipment firms most closely tied to new capital expenditure. Compared to GPU and memory manufacturers, equipment orders are often a more direct reflection of future investment plans for fabs and chip companies, making them the most sensitive to changes in CapEx expectations.

Institutions: Market Seems More Like a Re-Evaluation of AI Trades, Not a Denial of the AI Super-Cycle

Despite the consecutive-day decline in semiconductor stocks, most institutions have not interpreted the two news items as a sign of cooling AI demand.

Regarding Meta, many analysts believe that selling surplus computing power is more akin to finding a commercial outlet for its massive AI CapEx, thereby enhancing the sustainability of future investments in GPUs, networking equipment, data centers, and energy infrastructure, rather than cutting CapEx.

Regarding Anthropic, institutions generally view custom chips as aligning with the long-term development trend of major AI model companies. Even as more companies adopt ASICs, they still rely on advanced manufacturing processes, HBM, high-speed interconnects, advanced packaging, and data center construction. Demand for AI infrastructure will not disappear; instead, it may be redistributed across different segments.

More importantly, the current penetration rate of AI applications remains relatively low. Industry insiders point out that as inference demand continues to grow, token consumption and computing power requirements for large models are still far higher than previously anticipated. The AI infrastructure buildout is still a considerable distance from maturity.

Therefore, this week's market action seems more like a periodic repricing of AI trades following a historic rally.

If the AI competition over the past two years was about "who invests more," the signals from Meta and Anthropic suggest the AI industry is entering a new phase – where the competition shifts to who can generate the highest return for every dollar of capital expenditure.

For the market, this shift in expectations is sufficient to serve as a catalyst for the AI hardware sector correction. But for the industry itself, it may not necessarily mean the end of the super-cycle. Instead, it could signal that AI infrastructure investment is beginning to move towards a more mature stage that emphasizes closed-loop business models.