The Sword of Damocles Over the AI Bull Market: Not Just Korea, US Margin Debt Equally Alarming

- Core Thesis: The current global stock market rally is heavily dependent on leveraged capital, with both margin debt and leveraged ETF scale hitting all-time highs. This pro-cyclical structure, once deleveraging is triggered, will exponentially amplify downside risks. The violent turmoil in the Korean market has already issued a warning.

- Key Elements:

- US margin debt in May soared 54% year-over-year to a record $1.4 trillion. The total assets of leveraged ETFs surged from $115 billion to $220 billion in just 70 days, with capital heavily concentrated in the technology and semiconductor sectors.

- Barclays estimates that leveraged funds have accumulated approximately $300 billion in derivatives since the end of March. The hedging behavior of market makers creates a pro-cyclical effect, triggering a negative spiral of "reduction-selling pressure-further reduction" when markets decline.

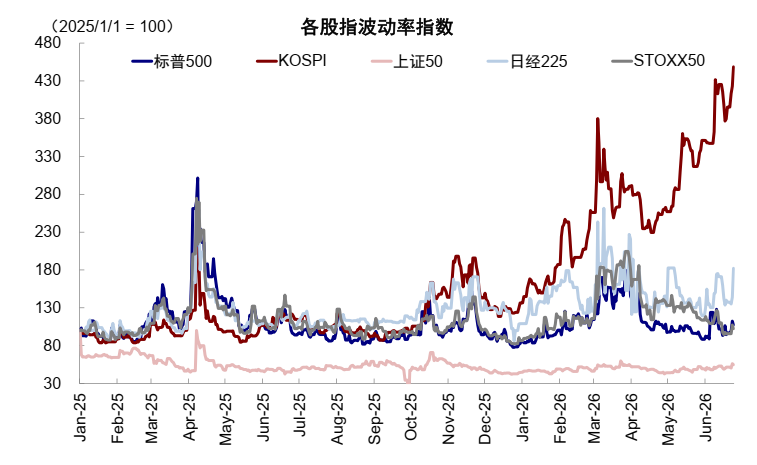

- Due to concentrated positions and high leverage, the KOSPI index triggered circuit breakers twice in a single week. Its broad leverage scale reached 271 trillion Korean Won, and margin calls can be triggered by a 16%-36% decline in underlying assets. Leveraged fund trading once accounted for 50% of the average daily trading volume of Samsung and SK Hynix.

- Morgan Stanley points out that the marginal buyers of US stocks have an unprecedented reliance on leveraged financing. The AXW futures spread, a measure of financing costs, has surged to its highest level since December 2020. Financing is becoming more expensive and scarcer.

- Financial conditions have already tightened by an equivalent of 31 basis points in rate hikes, but the stock market rally has masked this pressure. Once deleveraging begins, investors will reassess the Fed's policy path, leading to a concentrated release of tail risks.

Original Author: Zhang Yaqi

Original Source: Wall Street CN

Global stock markets have repeatedly hit new highs driven by the AI wave, but the fuel supporting this rally is becoming increasingly dangerous. From the United States to South Korea, both margin debt and leveraged ETF assets have surged to historical extremes. The inherent pro-cyclical nature of leverage is multiplying the tail risks of market volatility.

US margin debt surged 54% year-over-year in May, reaching an all-time high of $1.4 trillion. Concurrently, total assets under management in leveraged ETFs nearly doubled in under 70 days, surpassing $220 billion around June 3 (FactSet data). The risks of this leveraging frenzy have already manifested first in the South Korean market: the KOSPI index plunged 10% last week, triggering a circuit breaker, then rebounded sharply only to hit another circuit breaker. This violent volatility dragged down AI-related stocks in the US.

Alarms are now sounding on Wall Street. Barclays analyst Alexander Altmann warned clients this week that leveraged funds have bought approximately $300 billion in derivatives linked to individual stocks and indices since late March. If this scale of positions needs to be liquidated in a short period, "the impact would be chilling," and he characterized it as "unquestionably the largest source of non-discretionary risk in the market today." Morgan Stanley also warned on June 15, noting that the marginal buyer in US stocks is more dependent on leverage financing than ever before, and this financing is becoming both more expensive and scarcer. Charles Schwab, one of the largest US brokerages, has tightened margin requirements this month and issued margin calls to clients exceeding the new thresholds.

All this points to the same logic: when a leverage-driven rally reaches its limit, the deleveraging backlash will amplify the decline by a similar multiple.

US Stock Leverage: Unprecedented Scale and Intensity

The enthusiasm of US investors for buying stocks with borrowed money has reached an all-time high.

Data from the Financial Industry Regulatory Authority (FINRA) shows that US margin debt in May surged 54% year-over-year to a record $1.4 trillion. Running parallel to this is the explosive growth of the leveraged ETF market. These products typically track two or three times the daily return of an underlying asset. According to FactSet data, between March 30 and June 3, total assets under management in leveraged ETFs surged from approximately $115 billion to $220 billion.

The most sought-after products are concentrated in technology and semiconductor stock indices, as well as single-stock leveraged funds for companies like Tesla, Nvidia, and more recently, SpaceX. Direxion’s 3x Bull ETF tracking the semiconductor index gained roughly 700% between late March and late June. However, it plummeted 31% in a single day on June 5, amplifying the benchmark index's decline by three times.

From hedge funds to retail investors opening accounts on Robinhood, a diverse range of participants are piling in. Mark Hackett, Chief Market Strategist at Nationwide Investment Management Group, expressed concern:

"I worry we are accumulating a hidden layer of leverage that isn't fully understood. People are taking a lottery-ticket mentality, buying options on leveraged ETFs with borrowed money – that's three to four layers of stacking."

Derivatives Mechanism: A Pro-Cyclical Amplifier

The danger of leveraged ETFs lies not only in their own amplified profit/loss mechanism but also in their potential to distort the price movements of the underlying assets they track – an effect market participants call "the tail wagging the dog."

Barclays estimates that to absorb the continuous influx of new capital, leveraged funds have purchased approximately $300 billion in derivative contracts linked to individual stocks and indices since late March. After market makers take on these contracts, to hedge their own exposure, they need to buy the corresponding spot stocks, further fueling the rally in technology and semiconductor stocks this year.

The problem is that this mechanism works just as powerfully in reverse and is self-reinforcing. Once the underlying stock falls, leveraged fund assets shrink, forcing position reductions, which in turn pushes stock prices down, triggering more redemptions and selling, creating a negative spiral.

Dave Nadig, Research Director at ETF.com, issued a warning:

"Any market with identifiable, price-insensitive buyers or sellers creates problems. I'm genuinely concerned about the increasing amounts of money flowing into this leveraged single-stock product system, because the more money goes in, the stronger this pro-cyclical trading effect becomes."

South Korea's Warning: Extreme Concentration Meets High Leverage

Market participants view the events in the South Korean market this week as a stress test scenario worth referencing.

According to a CICC research report, the KOSPI index has surged 87% year-to-date, leading global markets, driven primarily by memory chip leaders like Samsung Electronics and SK Hynix. However, the highly concentrated holdings combined with extreme leverage have sharply increased market fragility. On Tuesday, concerns over memory chip expansion plans and news of a domestic discussion on taxing unrealized gains triggered a 10% single-day crash in the KOSPI, activating a circuit breaker. It then staged a strong rebound over the next two days, returning to the 9000-point level, only to hit another circuit breaker on Friday.

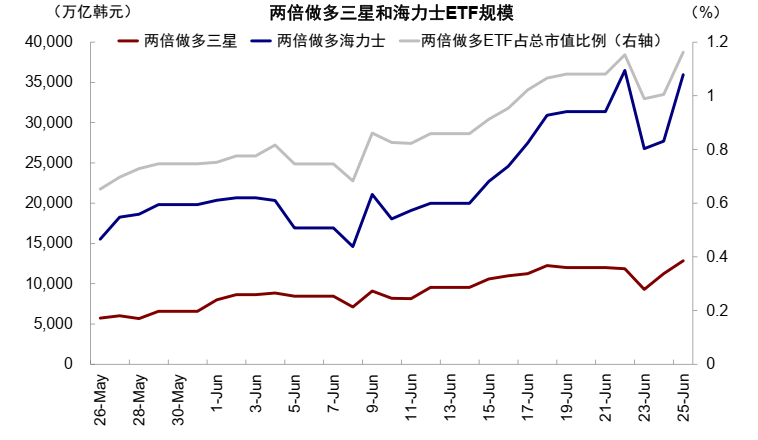

CICC estimates that the current on-exchange leverage multiple in the South Korean market is between 2x and 5x, with total broad leverage reaching 271 trillion Korean Won, an absolute level at historical highs. Theoretically, a 16% to 36% decline in the underlying assets could trigger margin calls. According to a Wall Street Journal report, trading related to leveraged funds tracking Samsung and SK Hynix recently accounted for up to 50% of the average daily trading volume of these two stocks, significantly disrupting stock prices in both up and down directions.

Lee Chan-jin, Governor of South Korea's Financial Supervisory Service, expressed regret at a press conference last week for failing to block the issuance of these leveraged single-stock funds, stating: "These are high-risk products, and about 92% of holders are retail investors. Despite consumer warnings, the trading fever shows no signs of cooling."

Soaring Financing Costs: Borrowing to Buy Stocks Gets More Expensive

According to a previous Wall Street CN article, Morgan Stanley's analysis reveals the pressure buildup from another dimension.

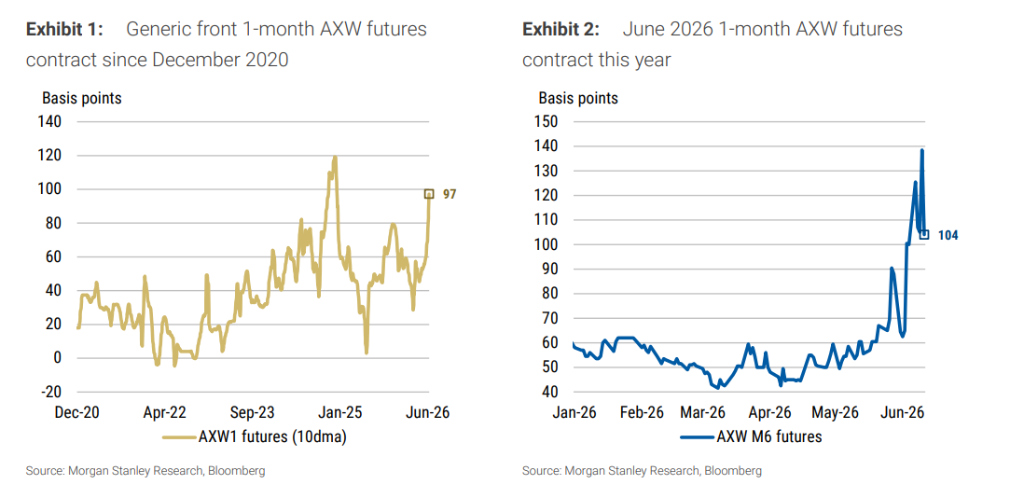

The key metric measuring stock financing costs – AXW futures (tracking the spread between the implied financing rate of S&P 500 total return futures and the benchmark SOFR rate) – for the June-expiring one-month contract surged to +140 basis points last week. Even after the S&P 500 subsequently pulled back from its all-time high, this indicator remained at extremely elevated levels, hitting its highest point since December 2020, excluding year-end special periods.

Meanwhile, New York Fed data shows that as of the week ending June 3, 2026, US primary dealers held $223 billion in equity exposure through securities financing methods like repurchase agreements, an all-time high. Morgan Stanley's "equity financing dependency" indicator – calculated by dividing primary dealer stock repo volume by the S&P 500's free-float market capitalization – has surged nearly 50% over the past year, approaching the historical peak seen in mid-March. This means the accumulated borrowed capital behind every dollar of market value is becoming increasingly dense.

This financing demand is highly concentrated in a few sectors. Morgan Stanley's industry breadth data shows that over the past three months, only the Information Technology sector among the 11 GICS sectors outperformed the S&P 500, gaining 24.2% with an excess return of 13.3%. In about 70% of trading days over the past year, fewer than 5 sectors outperformed the broader market. This implies that the overall market rally is actually supported by leveraged capital concentrated in a very few sectors. Once this capital begins to retreat, the impact on the entire market will be amplified.

Once Deleveraging Begins, the Impact Will Be Multiplied

Morgan Stanley warns that the current situation constitutes a potential non-linear risk: High financing costs prevent leveraged buyers from adding positions; the disappearance of the marginal buyer removes the market's upward momentum; subsequent price corrections trigger deleveraging; selling pressure is then amplified by leverage, ultimately causing declines to exceed expectations. Historical data shows that peaks in AXW futures often closely coincide with tops in the S&P 500.

More alarmingly, Morgan Stanley's Financial Conditions Index (FCI) shows that from the onset of the Iran conflict to June 11, financial conditions tightened by the equivalent of a 31 basis point rate hike, driven mainly by rising 10-year Treasury yields and a stronger US dollar. However, because stock indices are still rising, most investors are unaware of this tightening. The stock market rally itself contributed approximately -21 basis points of easing to financial conditions, somewhat masking the pressure from other factors.

Morgan Stanley's baseline forecast is for the Fed to cut rates by 25 basis points each in March and June 2027, bringing the terminal federal funds rate target range to 3.00%-3.25%. However, the bank warns that if deleveraging triggers a stock market decline, investors will be forced to reassess financial conditions, and in turn, reprice the Fed's policy path. The previously priced-in weight for tail risks of rate hikes would be the first to unravel.

Alexander Altmann wrote in a note to clients: "The technical forces that previously amplified upward momentum through leverage expansion may now start cutting in the opposite direction."