Precious metals follow the decline; what signal is gold sending to the market?

- Core View: The Federal Reserve, under Warsh's leadership, kept interest rates unchanged, but the more hawkish tone on inflation pushed real interest rates and the US dollar higher, leading to a synchronized decline in gold, silver, and South Korean AI semiconductor stocks. This indicates market pricing power has shifted from safe-haven narratives back to the cost of capital.

- Key Factors:

- The Fed's June FOMC meeting kept rates unchanged but emphasized that inflation remains above 2% and mentioned energy supply shocks, reinforcing expectations that high rates will persist for longer.

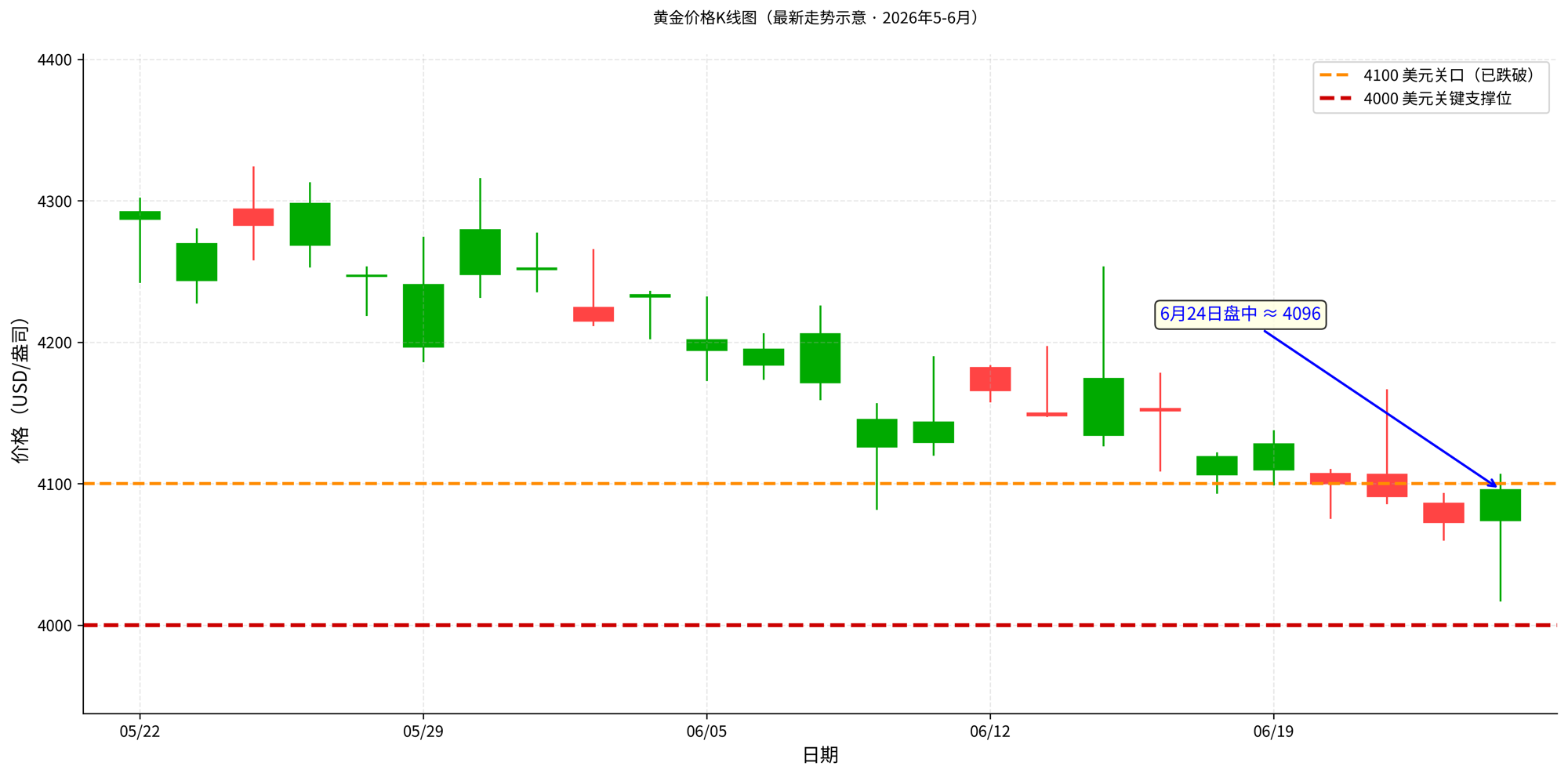

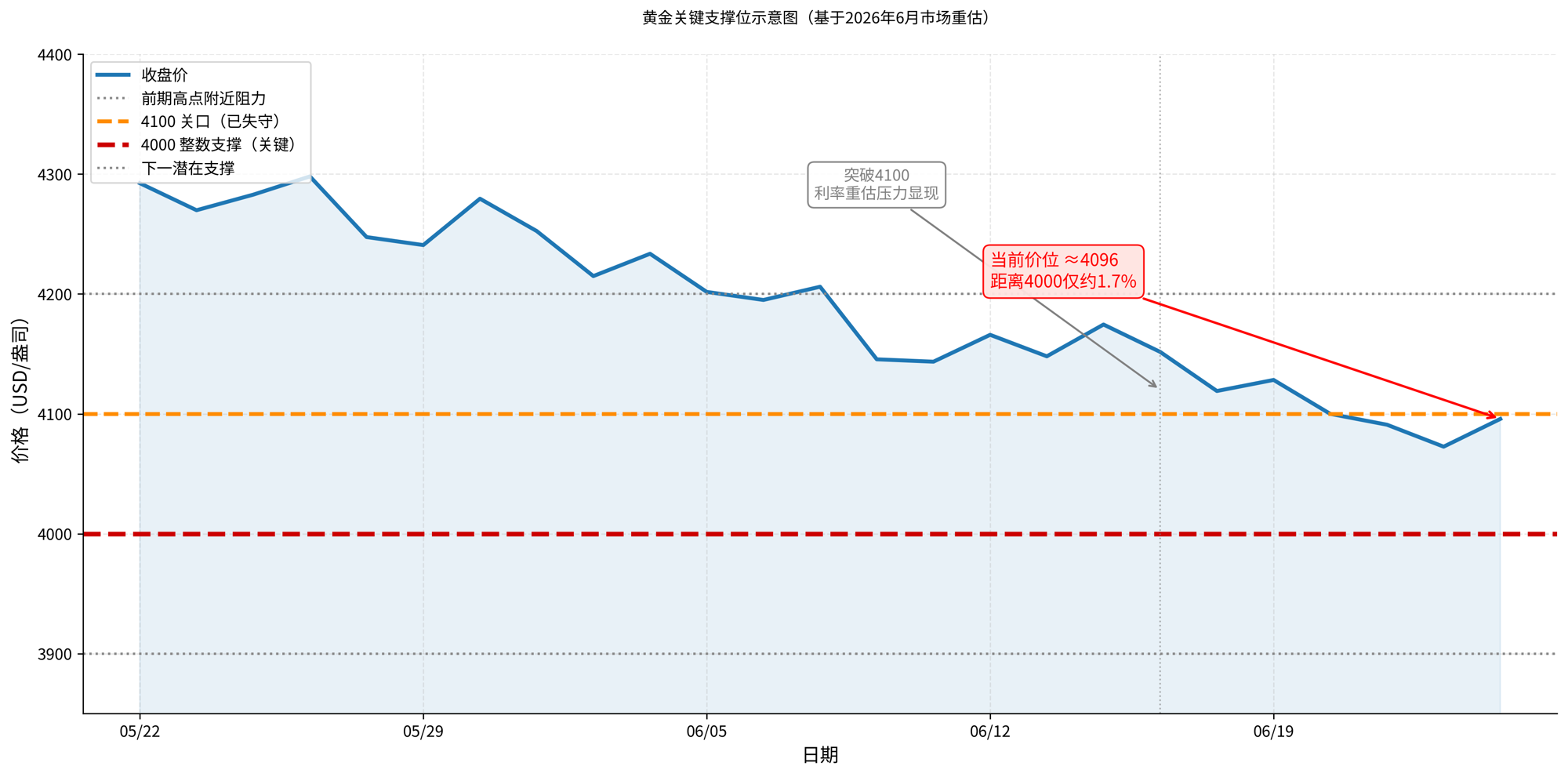

- Gold fell below $4,100 per ounce, approaching the psychological $4,000 mark. The decline is not due to a failure of safe-haven demand, but rather a rise in real interest rates increasing the opportunity cost of holding gold.

- South Korea's KOSPI fell over 8% at one point, triggered by a circuit breaker, dragged down by AI semiconductor heavyweights (Samsung, SK Hynix), suffering alongside gold and silver.

- The core reason for the simultaneous decline in precious metals and stocks is the market repricing liquidity, with capital flowing from crowded positions (precious metals, tech stocks) into the US dollar, cash, and short-term bonds.

- The crash in the Korean market acts as a magnifying glass, reflecting interest rate and dollar pressures, but is not the direct cause of gold's decline. AI earnings reports (e.g., Micron) can influence risk sentiment, but gold pricing remains dependent on the Fed and interest rates.

- Gold's long-term supports (central bank buying, safe-haven demand) have not disappeared, but are being suppressed by the cost of capital in the short term. If the $4,000 level is lost, it could trigger stop-losses and a liquidity-driven sharp sell-off.

- Future confirmation hinges on two lines: the implementation of hawkish Fed policies under Warsh's leadership and the direction of the US dollar. For silver, additional focus is needed on industrial demand expectations.

TL;DR

- After Warsh's first FOMC meeting, the Fed held rates steady, but the heightened language around inflation and energy shocks reinforced expectations of higher rates.

- Gold, silver, and South Korean AI semiconductor stocks fell together. The core reason isn't that safe-haven assets failed, but that real interest rates and the US dollar are reasserting their dominance in asset pricing.

- Related assets: Gold, Silver, US Dollar Index, 10-Year US Treasury, KOSPI, Samsung Electronics, SK Hynix, Micron, Nvidia.

Since June, South Korea's KOSPI index has fallen over 8% at one point, triggering a circuit breaker, dragged down by heavyweight semiconductor stocks. Gold and silver also declined during the same period.

The anomaly lies in the fact that if this were merely a traditional decline in risk appetite, investors would typically sell stocks and buy gold. But this time, risk assets and precious metals were sold off together. The Korean market provides an extreme example: core AI supply chain stocks like Samsung Electronics and SK Hynix fell, while gold and silver also faced pressure. The market is not currently trading "where is the safest place," but rather "the cost of holding uncertain assets has become higher."

This cost is the real interest rate. Simply put, the real interest rate is the true price of money after adjusting for inflation expectations. When it rises, bonds and cash become more attractive, making non-yielding assets like gold and silver less appealing. High-valuation tech stocks also get compressed as higher discount rates make future profits less valuable today.

Therefore, the Korean circuit breaker was the surface shock, but gold's concurrent decline is the more critical signal. The narrative that supported both AI semiconductors and precious metals in 2025 is now being tested by the same macro variable. This doesn't necessarily mean the AI bull run is over, nor does it invalidate gold's safe-haven status. But it does indicate that with the Fed under Kevin Warsh adopting a firmer tone, interest rates and the US dollar have temporarily reclaimed short-term pricing power.

Gold Under Pressure: Opportunity Cost Trumps Safe-Haven Demand

Gold does not always rally during periods of panic. Its biggest fear isn't just a stock market decline, but a strengthening US dollar and rising real interest rates.

After Kevin Warsh was sworn in as Fed Chair on May 22, the FOMC held the federal funds rate target range at 3.50%-3.75% on June 17. On the surface, this was a pause; however, the statement continued to emphasize that inflation remains above the 2% target and mentioned that supply shocks, including energy, are pushing up some prices.

For the market, this was more significant than whether an immediate rate hike occurred. Previously, investors were betting on a pivot to easing. Now, they are facing the prospect of higher rates for longer, with rate hike risks potentially being re-priced in.

The decline in gold and silver occurred after this shift in the macro anchor. On June 24, major market data sources showed gold had fallen below $4100 per ounce, with Trading Economics spot quotes briefly around $4069, leaving only about a 2% gap to the critical $4000 level. This level is important not just as a psychological barrier, but also because many technical analyses identify $4000 as a key support zone for this correction. With $4100 breached, the market is no longer trading a simple pullback, but questioning whether gold will meaningfully test the $4000 support.

If $4000 is convincingly broken, the issue isn't simply looking at how much further it could fall, but assessing whether the correction could amplify into a sharper sell-off. Given gold's significant prior gains and the accumulated profit in holdings, a breach of this key level could trigger simultaneous short-term stop-losses, trend-following fund reductions, ETF outflows, and margin pressures. At that point, while long-term supports like central bank buying and safe-haven demand remain, short-term prices will first obey liquidity and risk control. Market confidence in 'gold as a defensive asset' could face a new test.

This is not to say that geopolitical risks, central bank purchases, and industrial demand are unimportant. Gold's strong rally in 2025 was indeed backed by multiple supports: central bank buying, a weaker dollar, and safe-haven demand. Silver's even larger gains were related to its industrial properties and supply-demand dynamics. However, when interest rate expectations suddenly revise upwards, precious metals are first revalued as non-yielding assets.

The reasons for holding gold haven't disappeared; they are just temporarily overshadowed by a higher opportunity cost of capital. While risk events can stimulate safe-haven buying, high interest rates increase the cost of holding gold. When the latter dominates, gold can fall alongside stocks.

Gold and Silver Falling Together: The Market is Pricing Liquidity

The simultaneous decline of gold and silver cannot be simply interpreted as "safe-haven assets failing." More accurately, the market is repricing liquidity.

When easing expectations were strong, gold benefited from a weaker dollar, falling real interest rates, and safe-haven demand. Silver additionally leveraged its industrial properties and supply-demand expectations, offering greater elasticity. However, when the Fed re-signals a hawkish stance, the pricing logic reverses: a stronger dollar pressures dollar-denominated gold and silver; rising real interest rates increase the opportunity cost of holding non-yielding assets; and the market proactively reduces exposure to volatile positions.

This is why gold and silver can decline together with stocks. On the surface, they belong to different asset classes, but in short-term trading, they both depend on the same variable: the price of capital. If capital becomes more expensive, the market will first sell the most crowded, most profitable, and most easily liquidated positions, rather than first distinguishing whether their long-term narratives remain intact. Silver is more sensitive due to its industrial component; once risk assets pull back simultaneously, industrial demand expectations also get discounted.

Therefore, the core of this decline is not "why didn't gold act as a safe haven," but rather that the market's direction for seeking safety has changed. Amid expectations of higher rates, the short-term safe-haven choices for capital might be the US dollar, cash, and short-term bonds. Gold remains a long-term safe haven, but during a phase of rapid interest rate repricing, it will first suffer from the opportunity cost shock.

South Korea is a Magnifying Glass, Not the Cause of the Precious Metals Decline

The reason South Korea's market crash is observed within the same context is not that Korean semiconductors directly determine gold prices, but because it amplifies the pressure from the same macro trade.

South Korea's stock market benefited from AI memory demand in 2025, with heavyweight semiconductor stocks like Samsung Electronics and SK Hynix driving significant index gains. By 2026, the problem became: if too much capital was crowded into one direction, a rise in macro interest rates could trigger selling. Who sells first, and how much, can impact prices more than short-term changes in company fundamentals. The KOSPI's over 8% drop triggering a circuit breaker in June was the result of this crowded trade being re-examined.

However, causality needs to be clarified. Current public evidence does not suggest that "deleveraging in South Korea directly infected global precious metal positions." A more prudent assessment is that Korean semiconductors and precious metals are simultaneously bearing the same macro pressure: rising interest rates, a strengthening dollar, and increasingly expensive liquidity. The Korean market reacted more violently due to its index concentration and crowded AI positions. Gold and silver, due to their non-yielding nature and dollar denomination, are directly exposed to interest rate repricing.

In other words, South Korea is not the cause of gold's decline, but a display screen reflecting the market's risk appetite and leverage levels. It tells investors that when expectations of high interest rates resurface, assets that have experienced significant gains and accumulated heavy positions over the past year will be scrutinized first. While precious metals aren't tech stocks, they too must undergo repricing when the cost of capital rises.

AI Volatility Affects Sentiment, but Precious Metals Still Follow Rates

Fluctuations in AI semiconductors can impact market sentiment and also affect assets like silver that possess industrial attributes. However, this is not the primary narrative explaining the trajectory of gold and silver.

If the key variable for gold and silver is the real interest rate, then the key variable for AI semiconductors is order fulfillment. Micron's earnings report can serve as a window into risk appetite, as it influences the market's assessment of "whether high-valuation assets can still withstand high interest rates." If the AI supply chain continues to report strong earnings, risk appetite might find support, and silver's industrial component could be more easily revalued. If guidance disappoints, the market might further reduce growth asset positions, and contracting risk appetite would continue to pressure high-beta assets.

But the core pricing for gold still needs to revert to the Fed, the US dollar, and real interest rates. No matter how good AI earnings reports are, it's difficult to directly offset the pressure rising real rates place on gold. Conversely, weaker AI earnings do not necessarily drive gold higher, unless they simultaneously trigger easing expectations, a weaker dollar, or stronger safe-haven demand.

This is the difference between a market repricing and a fundamental falsification. A repricing means the discount rate has changed, causing investors to assign lower valuations to the same profits. Falsification means demand itself has faltered, necessitating downward revisions to future profits. For precious metals, the more important factor currently is the former: the market is first re-evaluating gold and silver based on a higher cost of capital, rather than altering long-term safe-haven logic due to changes in a specific industry chain.

Interest Rates and the Dollar are Testing This Decline

The easiest conclusion to overstate now is to equate synchronized declines directly with the end of a trend. Gold declining doesn't mean its bull market is over. The Korean circuit breaker doesn't mean AI demand has collapsed. A more reasonable perspective is that the market has entered a verification window: interest rate pressure is first compressing valuations and non-yielding asset prices, and then awaits data to confirm whether this is a correction or a reversal.

The Fed under Warsh is the first line of verification. If subsequent inflation and employment data remain strong, and energy prices stay elevated, the FOMC's hawkish tone could potentially translate into more concrete expectations of rate hikes. In that case, gold and silver would face not just short-term technical corrections, but more sustained suppression from real interest rates.

The US dollar is the second line of verification. Since gold and silver are priced in dollars, a stronger dollar directly increases the holding cost for non-US investors and dampens short-term demand for precious metals. If dollar strength combines with rising real interest rates, precious metals usually find it difficult to reverse the pressure relying solely on a safe-haven narrative.

Silver has an additional line of verification: industrial demand expectations. It is more susceptible to the sentiment surrounding risk assets than gold and tends to amplify fluctuations when growth expectations change. If AI, semiconductors, and other high-beta assets continue to face pressure, silver may face a dual repricing of both its precious metal and its industrial metal attributes.

The simultaneous decline of gold, silver, and AI stocks offers a straightforward reminder to investors: seemingly different assets in a portfolio can expose the same risk under a single macro variable. The winning trades of 2025 may not simultaneously lose their fundamental backing in 2026, but they will simultaneously face a more expensive cost of capital. The variables that will truly determine precious metal prices next are how long the pressure from interest rates and the US dollar lasts, and whether safe-haven demand, central bank purchases, and industrial demand can arrive quickly enough to offset this pressure.