Citi Bullish on AI Optical Interconnect: Market Targeting $92 Billion by 2028, New Yisheng Target Price Doubled

- Core View: Citi Research predicts that driven by demand for high-speed interconnect in AI data centers, the global optical interconnect market will reach $92 billion by 2028. This growth is primarily fueled by the technology migration from 800G to 1.6T, 3.2T, and CPO/NPO solutions, increasing demand for high-speed optical modules, silicon photonics, and laser chips. The Chinese supply chain is the most direct beneficiary, but supply bottlenecks and high valuations pose constraints.

- Key Elements:

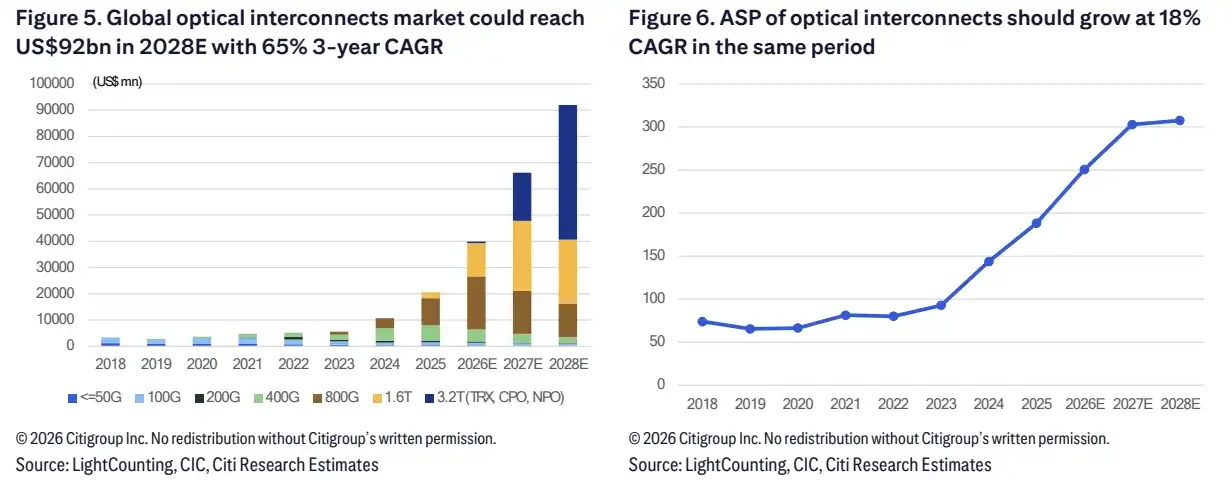

- Citi predicts the global optical interconnect market will reach $92 billion by 2028, with a compound annual growth rate of approximately 65% from 2025 to 2028, mainly driven by data center interconnect demand.

- Technology iteration is accelerating; the proportion of high-speed products above 800G in data centers is expected to rise from 37% in 2025 to 89% in 2028, with 1.6T transceiver shipments growing at a CAGR of 215%.

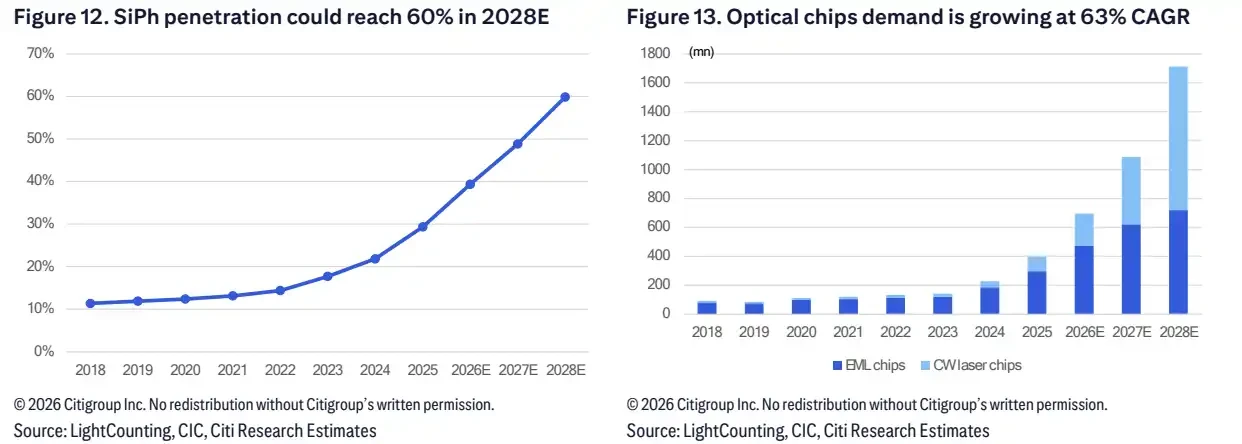

- The penetration rate of silicon photonics solutions in high-speed optical modules will increase from 29% in 2025 to 60% in 2028, driving the CAGR of CW laser chip demand to 114%.

- Citi has significantly raised the target prices for New Yisheng, Dongshan Precision, and Tianfu Communication, believing that AI optical business is the primary source of growth.

- Taichenguang's rating has been downgraded to Sell, with main risks stemming from decoupling from core customers, intensified competition, and a high valuation of 59 times.

- Growth faces three constraints: tight supply of EML/CW laser chips, uncertain deployment timeline for CPO/NPO technology, and optimistic expectations already priced into the valuations of some companies.

TL;DR

- Citi forecasts the global optical interconnect market will reach $92 billion by 2028 and has raised price targets for Eoptolink, DSBJ, and TFC.

- The migration from 800G to 1.6T, 3.2T, and CPO/NPO is driving up demand for high-speed optical modules, silicon photonics, and laser chips.

- China's optical communication supply chain is the most direct beneficiary, but laser chip supply, yield rates, and high valuations could still constrain the pace of realization.

Behind the $92 Billion: Data Centers Take Over Optical Interconnect Demand

In a research report on June 24, Citi raised its forecast for the AI optical interconnect market, estimating that the global market size will reach $92 billion by 2028, with a compound annual growth rate of approximately 65% from 2025 to 2028. In the same adjustment, price targets for Chinese optical communication companies such as Eoptolink, DSBJ, and TFC were significantly raised.

The basis for this judgment is not complex. As AI data centers continue to expand, the amount of data that needs to be transferred between GPUs and ASICs increases, and the connection requirements between cabinets, switches, and servers will also rise accordingly. High-speed optical modules, silicon photonics, and laser chips are no longer just supporting equipment for data center expansion; they are crucial links determining whether computing power can be efficiently connected.

Citi's model shows that the average selling price for optical interconnects is expected to maintain a compound annual growth rate of about 18% from 2025 to 2028, primarily driven by the increasing share of high-speed products like 800G, 1.6T, and 3.2T.

Global optical interconnect market size is projected to rise to $92 billion by 2028E, with ASP stabilizing after maintaining an 18% CAGR from 2025-2028.

After 800G: 1.6T, 3.2T, and CPO/NPO Take the Baton

General investors first need to understand a key change: this round of upgrades is primarily driven by data center interconnects, not traditional telecom or enterprise networks.

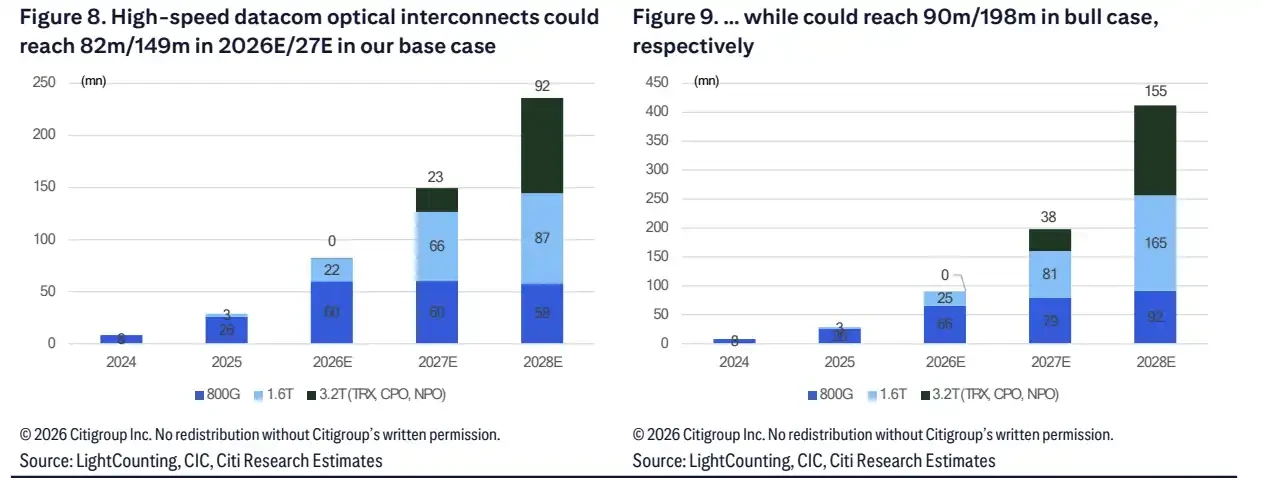

In Citi's model, global optical interconnect shipments are expected to increase from 110 million units in 2025 to 300 million units in 2028, a three-year compound annual growth rate of approximately 40%. The share of data center business in total shipments is projected to rise from 71% in 2025 to 89% in 2028.

Product specifications are also moving up. The share of high-speed products above 800G in data center optical interconnects is expected to increase from 37% in 2025 to 89% in 2028. This implies that growth is not just about "buying more optical modules," but a faster substitution of lower-speed products with higher-spec ones.

800G remains one of the mainstays in recent years, but 1.6T, 3.2T, and newer packaging solutions have higher growth rates. In the base case scenario, shipments of 1.6T transceivers are expected to achieve a CAGR of 215% from 2025 to 2028. 3.2T will start to ramp up from 2027, with shipments of 4 million units in 2027, rising to 35 million units in 2028.

CPO and NPO represent later technology migrations. In the base case scenario, CPO/NPO shipments are expected to reach 18 million and 56 million units respectively by 2028. In the bullish scenario, they could rise to 33 million and 116 million units in 2028. The significant difference between the two scenarios mainly depends on cloud provider demand, yield improvements, and the deployment pace of platform architectures from companies like Nvidia and Google.

Demand for high-speed optical interconnects diverges significantly after 2027, with 1.6T and 3.2T/CPO/NPO being the main source of elasticity between the base and bullish scenarios.

Silicon Photonics Rises to 60%: Value Shifts to Laser Chips and Optical Engines

If the $92 billion represents the market opportunity, then "silicon photonics" and "laser chips" determine how this growth is distributed within the supply chain.

Citi expects the penetration rate of silicon photonics in high-speed optical modules to rise from 29% in 2025 to 60% in 2028. Under this assumption, the total demand for optical chips in 2028 is estimated at approximately 1.714 billion units, with a CAGR of about 62% from 2025 to 2028.

Among these, demand for EML chips is expected to reach 718 million units, a three-year CAGR of approximately 34%. CW laser chips will see faster growth, with demand projected to reach 987 million units by 2028, a three-year CAGR of approximately 114%.

This is also why supply constraints are repeatedly mentioned. As high-speed optical modules ramp up, the bottleneck may not necessarily occur in the module assembly stage, but could appear in laser chip supply, packaging yields, and upstream capacity lock-in. By locking in upstream supply through long-term agreements and strategic investments, pure module manufacturers are essentially securing their position for the subsequent ramp-up of 1.6T, 3.2T, and CPO/NPO.

Silicon photonics penetration rate is expected to reach 60% by 2028E, optical chip demand is approximately 1.714 billion units by 2028E, with CW laser chip CAGR reaching 114%.

DSBJ, Eoptolink, TFC Get Upgrades; T&S Communications Downgraded

At the individual stock level, the most direct changes involve Eoptolink, DSBJ, and TFC.

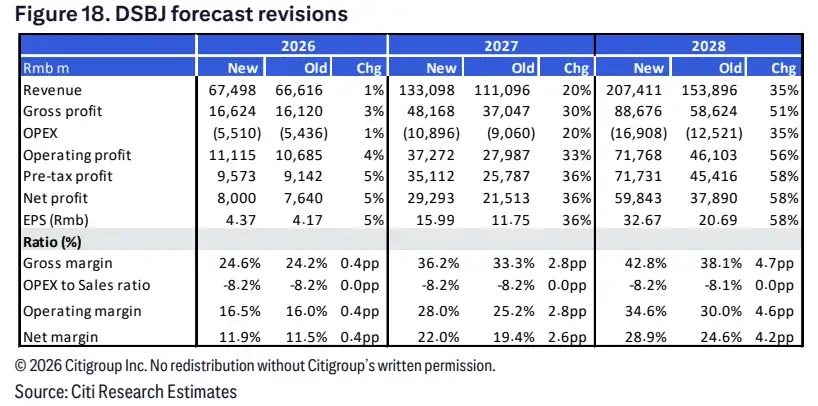

DSBJ is one of the most notable companies in this round of upgrades. Citi raised its price target from RMB 225 to RMB 350 and increased net profit forecasts for 2026 to 2028. Research reports indicate that the AI optics business is seen as the main incremental driver, expected to contribute significantly higher profits in the coming years.

In terms of valuation, DSBJ is now broken down into segments like traditional business, optical modules, optical chips, and AI PCB. This breakdown suggests that when the market looks at DSBJ, it is no longer just considering its traditional PCB or electronics manufacturing business, but evaluating whether it can translate its AI optics business into realized profits.

Eoptolink's price target was raised from RMB 353.57 to RMB 701, primarily driven by 3.2T transceivers and NPO. TFC's price target was raised from RMB 318.57 to RMB 419, with benefits concentrated on CPO ramp-up and 3.2T optical engines.

DSBJ earnings forecast upgraded.

Divergence is also emerging. T&S Communications (300570.SZ) was downgraded from Buy to Sell, with a price target lowered from RMB 156 to RMB 152. Citi cut its EPS forecasts for 2026 and 2027 for T&S Communications, mainly considering risks associated with decoupling from Corning, increased competition in the Asian supply chain, and high valuation. According to the report, T&S Communications' current valuation is approximately 59 times 2027 P/E, while the target price corresponds to 31.8 times 2027 P/E.

This set of rating changes indicates that upward revisions in AI optical interconnect demand do not mean all companies in the supply chain will benefit equally. The market values high-speed product capabilities, silicon photonics and laser chip deployment, customer structure, supply chain stability, and whether the current stock price has already priced in growth.

It is worth noting that these price targets are still assumptions within brokerage models, not company commitments. For investors, the upward target price revisions reflect institutions factoring in AI optical interconnect demand, product upgrades, and China's supply chain share simultaneously. However, subsequent execution concerning orders, delivery, and profit margins needs to be monitored.

Growth Story Hinges on Laser Chip Supply, Yields, and Valuations

This round of upgrades does not mean AI optical interconnects have entered a risk-free growth phase.

The first constraint is supply. Both EML and CW laser chips could become tight, especially under scenarios of rapidly increasing silicon photonics penetration and accelerating deployment of 1.6T and 3.2T. Upstream capacity and yields will directly impact final shipments. If key chip supply cannot keep pace, orders and expectations may rise first, but revenue recognition will depend on delivery timelines.

The second constraint is technology implementation. CPO/NPO are seen as significant drivers of growth after 2027, but whether the new architectures can ramp up as per the bullish scenario depends on cloud provider capital expenditure, network architecture choices, equipment yields, and the progress of platform solutions from companies like Nvidia and Google. The large gap between the base and bullish scenarios suggests that shipments over the next two years are not yet locked in.

The third constraint is valuation. T&S Communications was downgraded from Buy to Sell by Citi, citing risks like decoupling from Corning and high valuation. Accelink Technologies also maintained a Sell rating, with the main pressure also coming from valuation.

The $92 billion market forecast has pushed AI optical interconnects into the spotlight, but stock prices have already priced in a significant amount of optimistic expectations. The real differentiator will be not just how many AI orders a company secures, but who can penetrate into higher-end product generations, lock in upstream laser chip supply, and translate the ramp-up of 1.6T, 3.2T, and CPO/NPO into sustainable profits.