Why does NVIDIA’s debt issuance go smoothly while SpaceX’s debt issuance triggers a sharp drop?

- Core Thesis: SpaceX is pursuing at least $20 billion in bond financing after its IPO, prompting the market to draw a comparison with NVIDIA. This highlights the fundamental divergence between the space narrative and the AI narrative in their respective cash flow verification stages, as the market reassesses the pressure from SpaceX's massive capital expenditures.

- Key Elements:

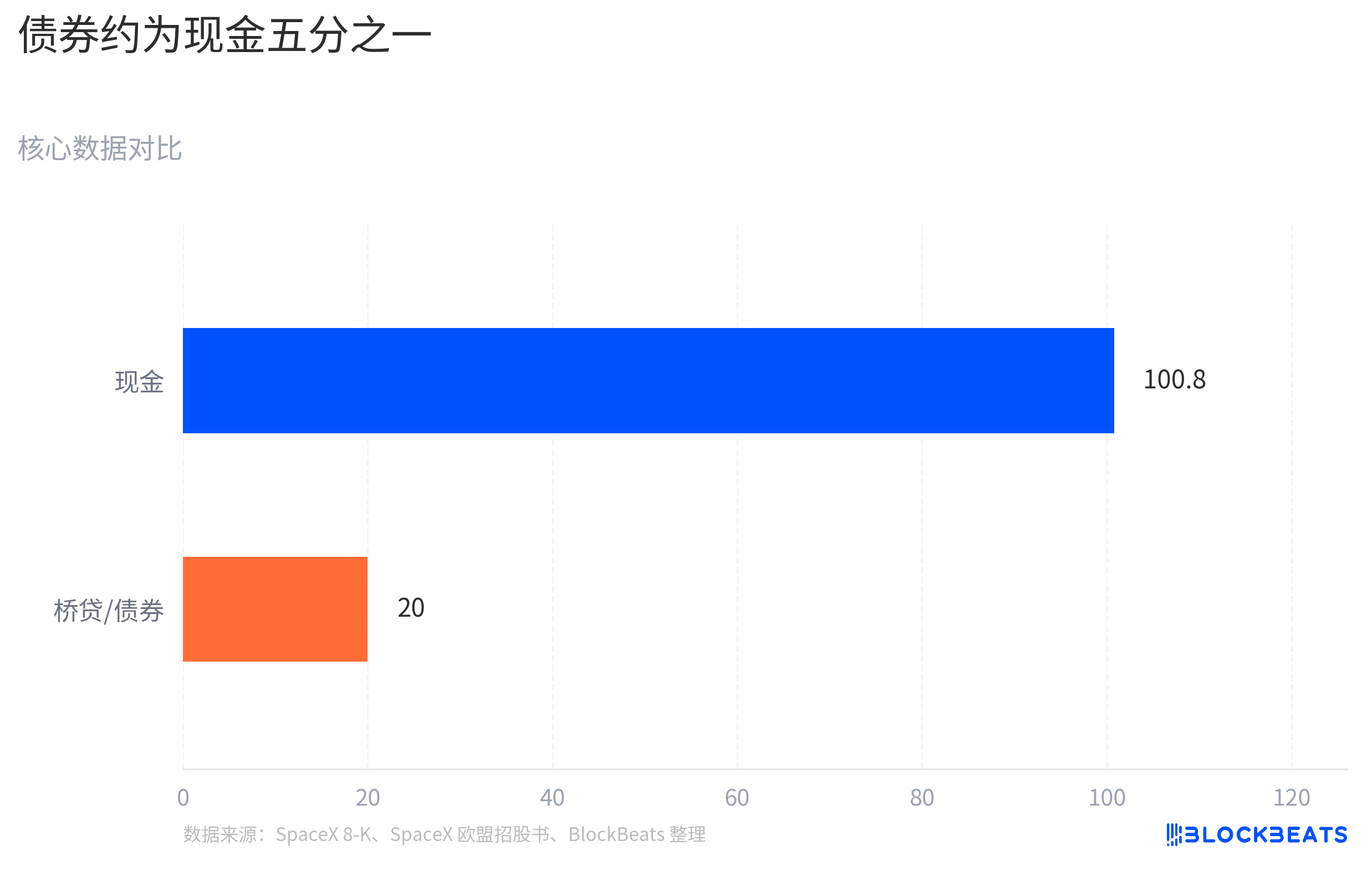

- Following its IPO, SpaceX plans to issue at least $20 billion in bonds to repay the $20 billion unsecured bridge loan maturing in March, with approximately $100.8 billion in cash on its books.

- SPCX shares came under pressure on June 23, falling to around $154.6, below their first-day closing price, as the bond news served as a trigger for the market to reassess its cash flow pressures.

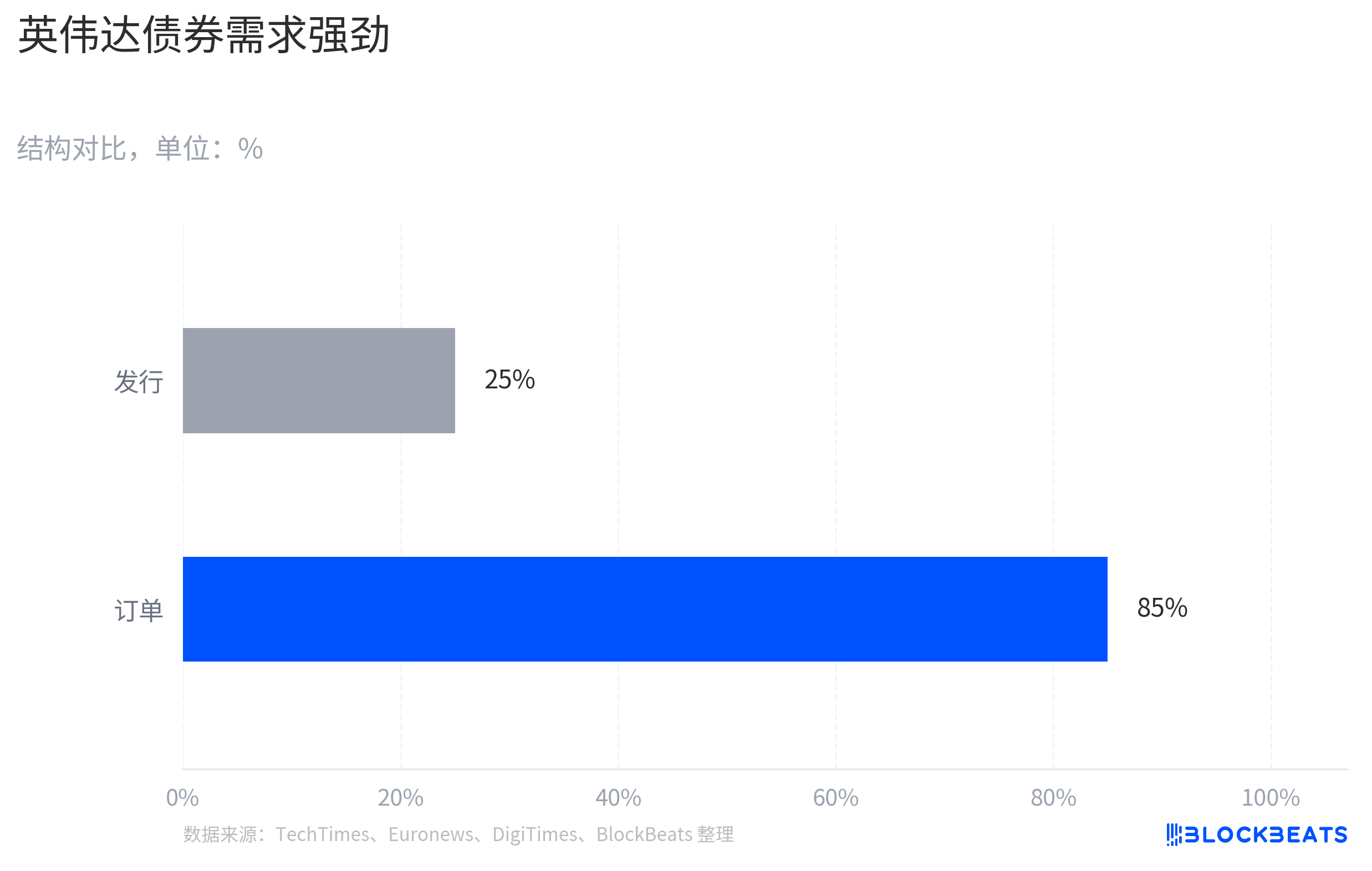

- NVIDIA's concurrent $25 billion bond issuance drew $85 billion in orders, with the market viewing it as locking in long-term capital rather than a sign of stress, reflecting that its AI narrative has entered a phase of revenue and profit validation.

- While Starlink serves as a cash flow engine for SpaceX, its long-range visions—such as Starship, satellite networks, and AI infrastructure—remain in high-investment, not yet fully commercialized stages.

- Debt investors focus more on cash flow, capital expenditures, and debt repayment schedules compared to equity investors. A large-scale bond issuance forces the market to shift its analysis from "narrative potential" to "cash burn rate."

- SpaceX's potential for market recovery depends on whether Starlink's profit expansion can cover the heavier capital expenditures and the speed at which projects like Starship achieve commercial realization.

TL;DR

- SpaceX is advancing at least $20 billion in bond financing post-IPO to repay previous bridge loans; the company has ample cash on hand, but the market is beginning to reassess future capital expenditure pressures.

- Nvidia’s concurrent bond issuance received strong demand, providing a contrasting reference: the AI narrative has entered the phase of revenue and profit verification, while SpaceX’s space narrative still requires more incremental proof.

- Related targets: SPCX, Nvidia, AMD, TSMC, AI data centers, satellite and space commercialization plays.

Around June 22, SpaceX advanced at least $20 billion in bond financing post-IPO to repay its prior bridge loans. Subsequently, the SpaceX-related SPCX faced pressure in the secondary market, trading at approximately $154.60 during intraday trading on June 23, below its first-day closing price but still above the $135 IPO price.

This price movement shouldn't be simplistically attributed to a single bond event, but the financing news did act as a trigger. It quickly brought the space narrative, newly introduced to the public market, back to the question of cash flow: the market began recalculating how much capital SpaceX's long-term projects require and which business segment will cover it.

Nvidia is the most important reference point. On June 15, Nvidia issued $25 billion in high-grade bonds, with order demand reaching approximately $85 billion at one point, leading to an increase from the originally planned ~$20 billion issuance. Both companies raised funds within their mega-narratives, but the market reactions were completely different: Nvidia's bond issuance was more readily seen as locking in long-term capital, whereas SpaceX's was immediately placed under a capital expenditure stress test.

The difference lies not in the bond issuance itself, but in the market's level of trust in their cash flows. Nvidia's AI demand has already entered the stage of revenue and profit verification, making the debt more like an amplifier for an already realized growth curve. SpaceX, however, needs to answer a different question: can the money earned from Starlink support Starship, the satellite network, AI infrastructure, and more distant space visions?

SpaceX's Financing Triggers Market Reassessment of Capex

Issuing bonds itself is not a problem. For high-credit companies, replacing short-term bridge loans with long-term debt is often just capital structure management. SpaceX's at least $20 billion bond financing is also primarily reported as a means to repay the prior bridge loan, and shouldn't be simply interpreted as negative news.

SpaceX is not relying on the bond market to survive. According to filings, as of June 19, the company held approximately $100.8 billion in cash and cash equivalents. Having nearly $100 billion in cash post-IPO at least indicates the company's financial structure is not poor.

However, having ample cash doesn't mean the market won't reassess the future pace of spending. More crucial is the bridge loan structure: SpaceX already had a $20 billion unsecured bridge loan in March, maturing on September 2, 2027, with an extension option. The subsequent at least $20 billion bond financing is primarily described as refinancing or repaying this bridge loan.

Bonds change how the market views SpaceX. Equity investors can pre-pay for Starship, Mars transport, and space infrastructure because they are buying future upside potential. Debt investors, conversely, are more concerned with cash flow, capital expenditure, and the pace of debt servicing. When SpaceX pursues significant bond financing right after its IPO, the market naturally shifts the question from "How big a space story can Musk tell?" to "How much more money will be needed before these engineering feats are realized?"

SpaceX already has a profitable business, but the market is asking whether this business can cover the simultaneous pursuit of long-term projects across the entire company. Starlink is the clearest current cash flow engine, with its satellite internet user and revenue growth distinguishing it from many pure-concept space companies.

But SpaceX's valuation is not built solely on Starlink; it also rests on Starship's high-frequency reusability, global satellite network expansion, Mars transport, and potentially new narratives related to AI infrastructure. These narratives are all grand, and all very expensive. Starship requires continuous testing, iteration, and launch capability development. The satellite network needs replenishment and upgrades. If AI infrastructure becomes further tied into SpaceX's capital story, investors will need to assess when this investment will generate returns.

So, the bond issue is not the sole reason for SpaceX's dip, but it is a clear trigger. It reminds the market that when a space narrative enters the public market, it must not only prove its vision is big enough but also demonstrate sufficient self-sustaining cash generation capabilities.

AI Narrative and Space Narrative Are at Different Stages of Realization

Nvidia's concurrent bond issuance provides a clear reference point for the market. On June 15, Nvidia issued $25 billion in high-grade bonds, with order demand reaching approximately $85 billion at one point. The market didn't primarily interpret this debt as pressure, but rather as a strong company locking in long-term capital.

The difference stems from the cash flow stage behind the bonds. Nvidia's AI demand has already manifested in financial reports through data center revenue, customer orders, and profit margins. Investors are now discussing how long this growth curve can last. For Nvidia, issuing debt is akin to adding financial flexibility to an already proven growth curve.

SpaceX's situation differs. It also has a cash flow engine in Starlink and ample cash post-IPO. However, its valuation incorporates more heavy-capital projects that are not yet fully commercialized. When the market sees SpaceX issuing bonds, the question isn't "Can it borrow money?" but "Will the capital consumption of future projects outpace the realization of cash flow?"

This doesn't mean space commercialization has lost value, nor that the market has dismissed SpaceX. More accurately, the AI narrative for Nvidia represents visible revenue, while the space narrative for SpaceX still requires more incremental proof. Starship's value will only be proven through higher frequency, lower cost, and more stable reusability. Mars transport and space infrastructure are even further off. If AI infrastructure becomes a new growth driver, it too needs real customers, real revenue, and explainable returns on capital.

This is precisely the most overlooked difference in deep tech investing. A company can possess strong technology, a strong brand, and a strong founder simultaneously, but if the validation of its cash flow is slower than its capital investment, the debt will be perceived by the market as a source of pressure.

The phrase "Mars burns cash" is catchy but incomplete. SpaceX has a path to commercialization; however, multiple future projects require continued capital. Nvidia's contrasting reaction highlights this more clearly: the market rewards not a vision label, but the speed at which a story translates into revenue, profit, and free cash flow.

Speed of Cash Flow Coverage Determines Recovery Potential

SpaceX's recovery potential depends on whether the market can see Starlink's profit expansion covering the heavier capital expenditure curve. As long as Starship remains in a high-investment phase, the satellite network needs continuous upgrades, and AI infrastructure lacks a clear path to payment, investors will repeatedly calculate the capital burn rate.

Bond pricing will provide an initial signal. If the final issuance spread, coupon, and order demand show that the credit market is willing to provide long-term capital at relatively low cost, it indicates investors still accept SpaceX's longer timeline for realizing the space infrastructure story. Conversely, if financing costs are high or the market demands a thicker risk premium, equity valuations will continue to face pressure.

More important is the business side. If Starship demonstrates stronger validation in high-frequency reusability and launch costs, the business models for Starlink, deep space transport, and even space infrastructure could all be revalued. Conversely, if subsequent disclosures show Starlink's growth cannot cover the expansion of other projects, the debt will continue to remind the market: SpaceX is still in its heavy-capital vision stage.

This is also the core contradiction in SpaceX's current pricing. It has approximately $100 billion in cash on its books and a cash flow engine like Starlink, but the public market doesn't price solely based on cash balances. Only when Starlink's profits, Starship's reusability progress, and the boundaries of capital expenditure all become clearer can debt transition from a source of pressure back into a tool for growth.