1.6 Billion Market Cap Is Just the Beginning: The Real Value of Tokenized Stocks Lies in On-Chain Infrastructure

- Core Thesis: The tokenized stock sector has growth potential, but current issuance is primarily through custodial wrapper models, making early investment opportunities scarce for retail investors. The true value lies in betting on the proliferation of native on-chain asset tokenization, rather than directly trading tokenized stocks.

- Key Points:

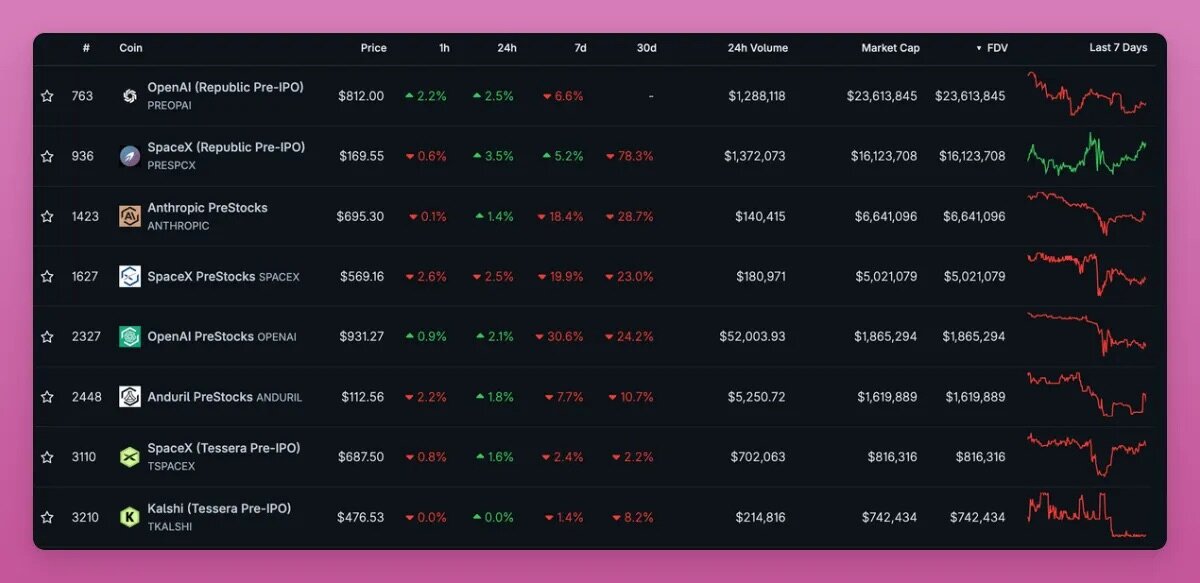

- Tokenized stocks carry multiple risks, including issuer custodial risk, insufficient liquidity, and smart contract risk—for example, the SPCX token on the xStocks platform dropped 40% due to a lock-up issue.

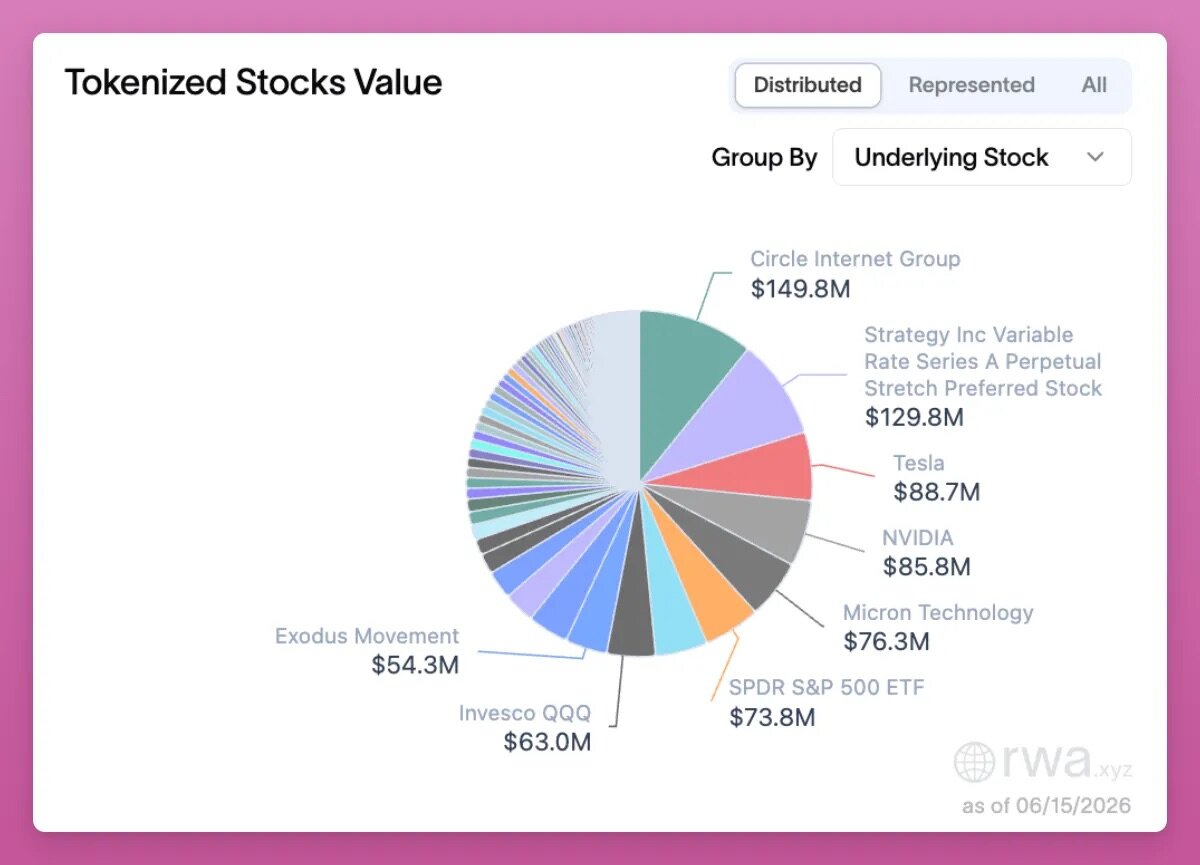

- The sector remains tiny, with a total circulating value of only $1.5 billion (lower than Uniswap's $1.9 billion). Most underlying assets are stocks of mature companies (e.g., Strategy's position valued at $129 million), not early-stage investment opportunities.

- Standard Chartered predicts that the total value of on-chain tokenized assets will exceed $4 trillion by 2028, with the growth of tokenized equity boosting revenue for platforms like Uniswap and providing the crypto industry with counter-cyclical characteristics.

- Backpack achieved native on-chain equity issuance via Superstate's Opening Bell, granting holders dividend and voting rights. Its token, BP, can be exchanged for actual equity, with a recent price surge of 200%.

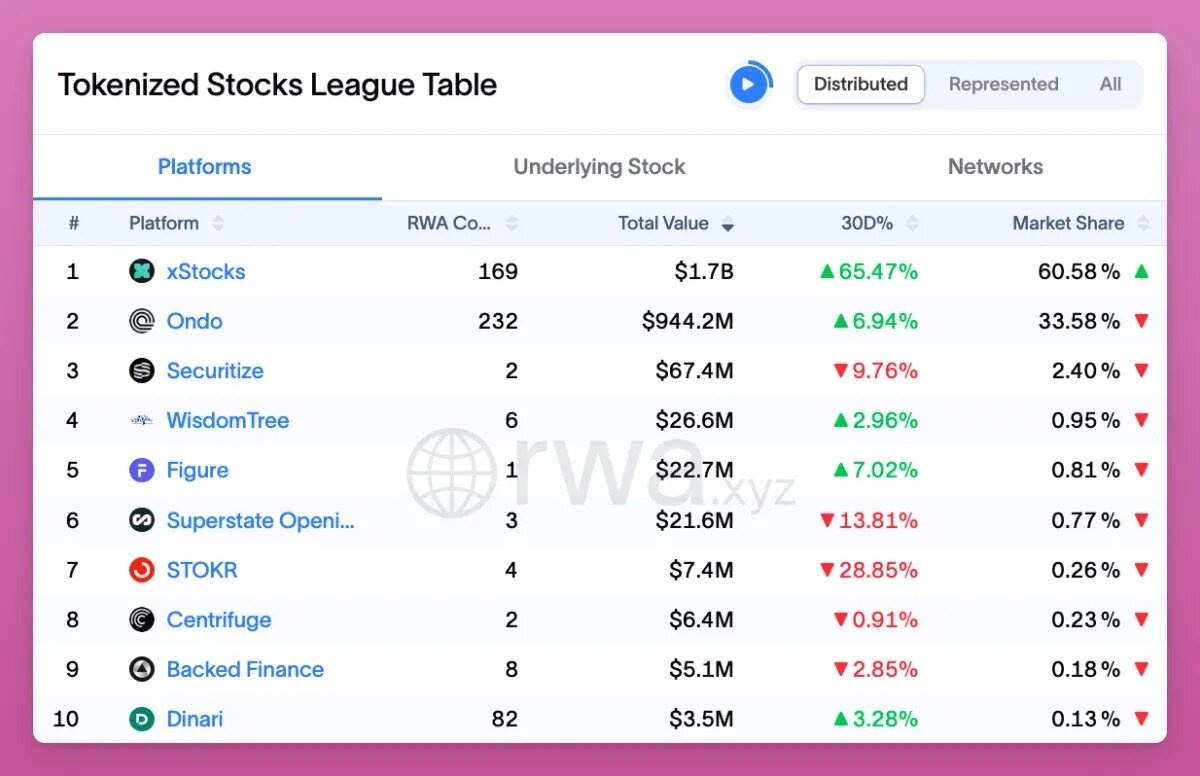

- Market leader xStocks holds a 60% share but launched a points program (xPoints) following its acquisition by Kraken; the prospects for a token generation event remain uncertain. Ondo's ONDO token offers only governance functions and faces nearly 50% token dilution.

- Trading opportunities include engaging in delta-neutral hedging or point farming on platforms like Backpack and Variational, but one must be wary of platform shutdown risks, such as those seen with Ventuals.

Original Author: Ignas | DeFi Research

Original Translation: Saoirse, Foresight News

In my opinion, there’s only one way to make big money from tokenized stocks.

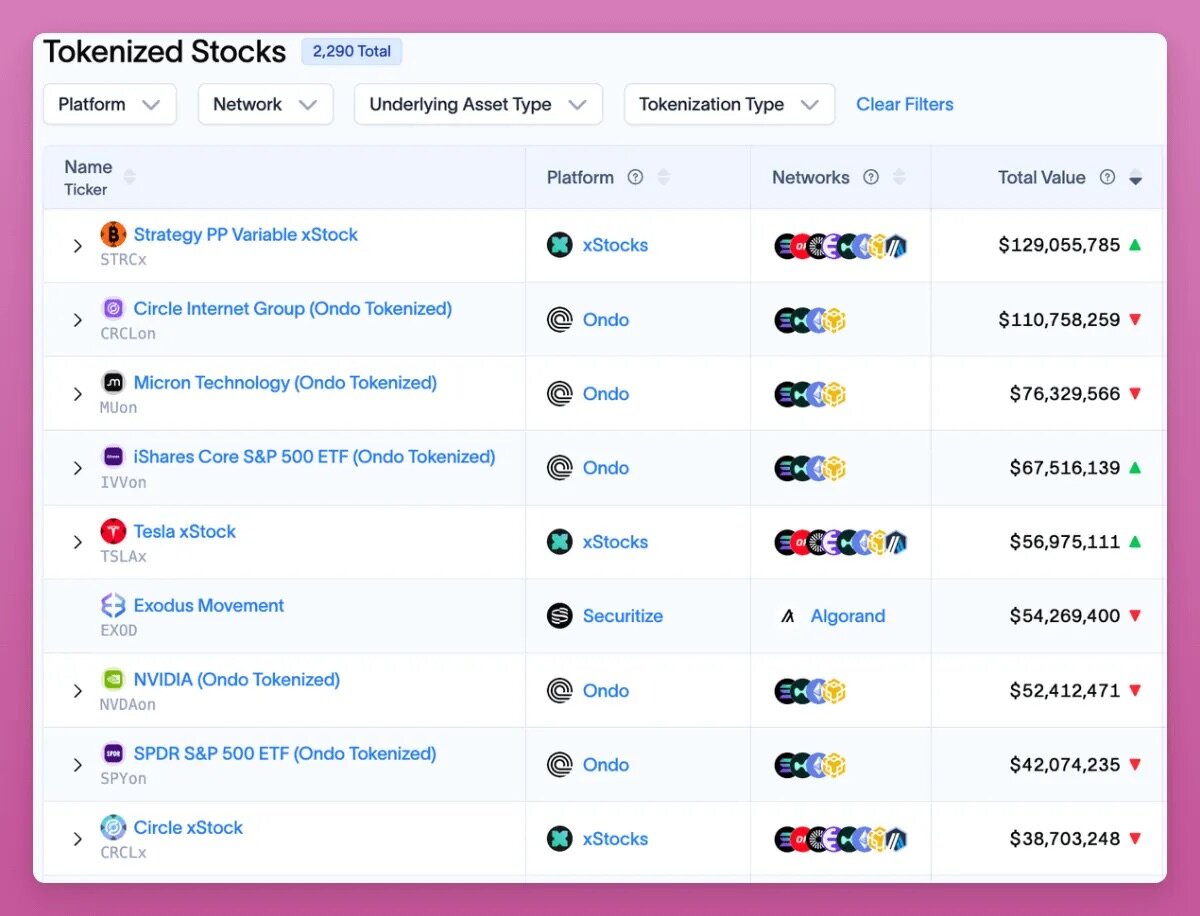

Of course, you could buy these tokens hoping for a 10x spike, but aside from rare exceptions like Micron Technology (MU), the odds of such a windfall are minuscule. For starters, only 2,290 stocks have been tokenized, and only about 130 have a market cap exceeding $1 million. The vast majority of tokenized stocks have virtually no liquidity on-chain.

According to RWA data site rwa.xyz, Strategy is among the largest of these assets, with a total value of $129 million.

Currently, most tokenized stocks are established publicly traded companies. If you're looking to uncover undervalued, overlooked stocks, traditional brokers like Interactive Brokers offer more opportunities.

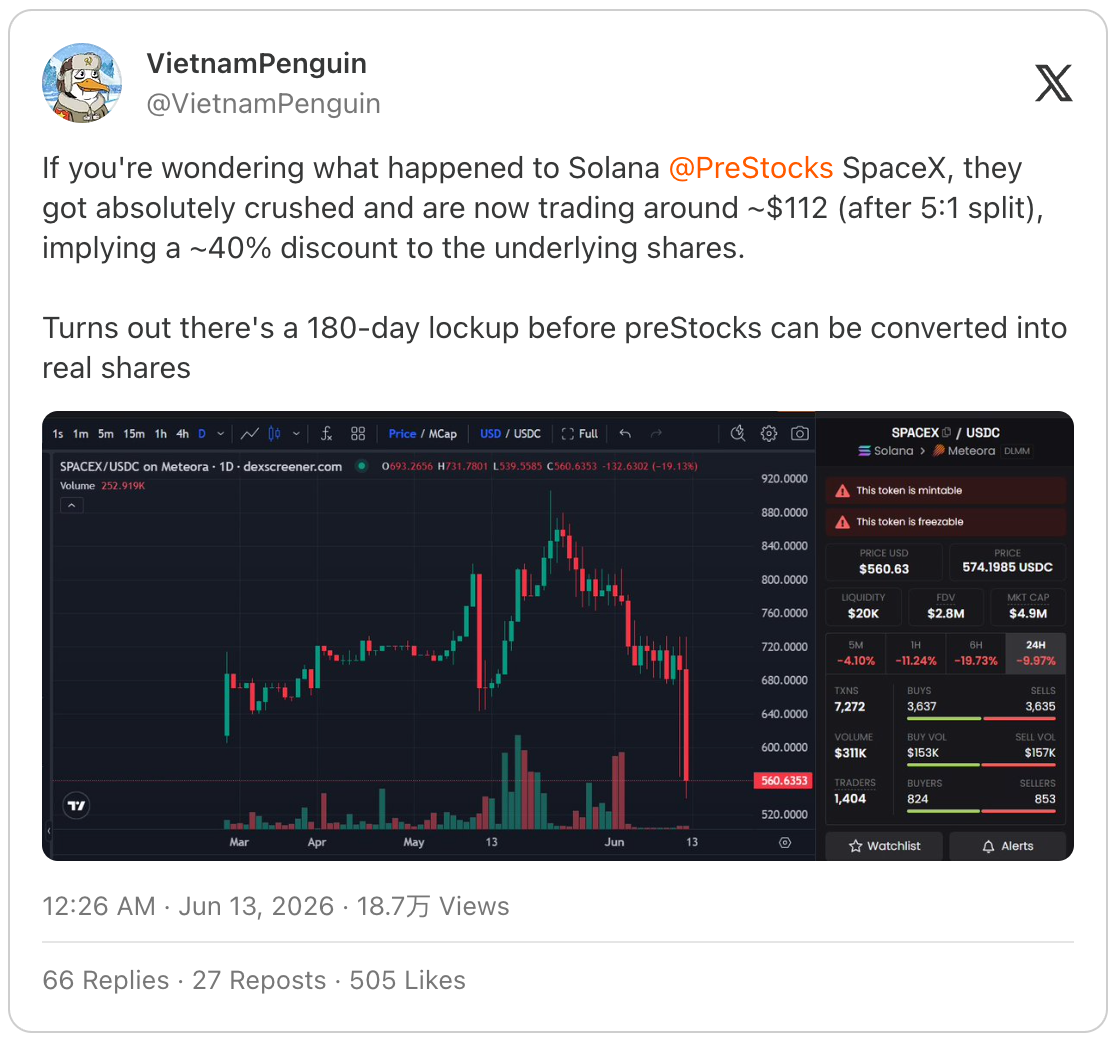

Secondly, holding tokenized stocks introduces risks that don't exist with traditional brokerage positions. For example, investors who bought SpaceX tokenized stocks (SPCX) on the PreStocks platform discovered these tokens require a 180-day lock-up before they can be exchanged for actual shares. This news caused the token's price to plummet by 40%.

Source: https://x.com/VietnamPenguin/status/2065470925252759680

Thus, investors must bear the native crypto risks of smart contract vulnerabilities and self-custody asset risks (without enjoying the benefits of self-custody), along with liquidity risks, in addition to the risks introduced by the issuer and the asset custodian.

However, I'm not entirely dismissing the tokenized stock sector. It's one of the most promising segments in crypto: it can attract new users and retain existing ones who might otherwise cash out their crypto assets to invest in traditional financial markets. Tokenized stocks bring on-chain trading and fee revenue to blockchains, and can draw venture capital, developers, and market attention to the industry.

Tokenized stocks themselves offer several opportunities: you can deposit them into decentralized exchange (DEX) liquidity pools to earn yields, use them as collateral for loans, or hold SPCX spot on-chain while shorting the corresponding perpetual contracts to earn delta-neutral yields, along with DEX platform points.

Speaking of hedging strategies, you can buy tokenized stock spot and short them on the Variational platform. The platform's native token, VAR, is arguably the best airdrop opportunity right now:

- 50% of the total token supply will be allocated to the community;

- Points campaign ends on September 30, leaving only about a 3.5-month window for mining;

- After the token launch, the team plans to use 30% of platform revenue for buybacks and burns;

- The platform is still in a closed beta.

Tokenized Stocks Are Not an Early-Stage Investment

But my biggest concern with tokenized stocks is this: the sector essentially makes crypto investors the exit liquidity for traditional financial assets.

The crypto industry has created many millionaires in the past because we got in early on new frontiers: Bitcoin, smart contract L1s, project airdrops, NFTs, the Hyperliquid airdrop, and many more. The tokenized listing process of SpaceX highlighted this issue for me.

Its offering model and hype cycle mirror that of a high-profile crypto L2 token launch: a small circulating supply, an extremely high fully diluted valuation, and price movements completely disconnected from the company’s fundamentals. In the short term, traditional financial markets are currently in a phase where "high FDV is just a gimmick," identical to the crypto industry two years ago.

There’s no denying that rockets, AI, and Starlink sound promising, but the company's valuation, equity unlock schedule, revenue data, and governance mechanisms are hardly encouraging.

The core value of tokenization lies in broadening asset distribution channels: any user with a Phantom, MetaMask, or Rabby wallet can hold these tokens. Their volatility is lower than Bitcoin or altcoins, but they aren't pegged to the dollar like stablecoins, placing their risk-return profile in between. For investors outside developed markets, or those who don’t want to or can’t cash out their crypto assets into traditional finance, tokenized stocks offer an attractive solution.

But this doesn't mean we’ve captured an early investment opportunity. The former allure of crypto was allowing ordinary retail investors to back revolutionary startups. An IPO valued at a $2 trillion scale is far from an early-stage bet.

The true long-term upside for crypto lies in companies issuing equity on-chain from their inception. ICOs and fair launches were good attempts, but the last bull market saw the industry become increasingly extractive: projects had inflated early-stage private valuations, further inflated at TGE, and offered mere scraps to the general public. Cobie articulated this brilliantly in his blog post.

I’m still investing via Cobie's Echo platform because it genuinely offers early-stage project access: my investment in the MegaETH round has already returned 3.85x, even though the market for tokens has been lackluster post-launch.

Apptronic, a humanoid robot company, is an example where I participated in its Series B strategic funding round, despite a high valuation. Such investment opportunities are typically closed to ordinary retail investors on traditional financial platforms.

By the way, besides Echo, I'm also bullish on the Legion platform, but it still needs to find quality, fairly valued projects to invest in – and that’s not easy.

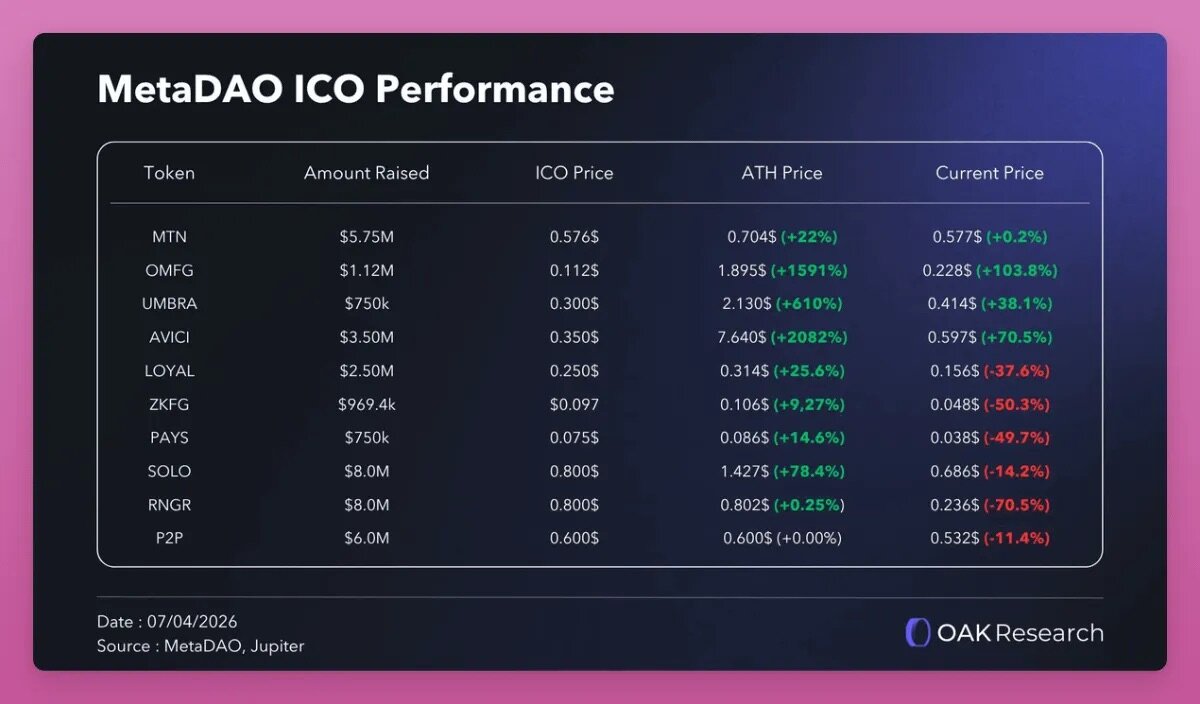

MetaDAO’s model is excellent: the ownership tokens issued by the platform grant holders legal equity, use vesting schedules to oversee treasury spending, and unlock tokens based on company performance. This perfectly addresses the core flaws exposed by the ICO craze. Consequently, given the current market environment, the various ICO projects launched by MetaDAO have performed relatively better overall.

Source: X Platform OAK Research

Beyond this, there’s the native on-chain issuance model, like Superstate’s Opening Bell product line. Its first asset is Galaxy stock, where corporate equity is issued compliantly directly on-chain.

Imagine if large companies bypassed the traditional IPO process and instead issued equity directly on Ethereum or Solana, rather than just wrapping off-chain legal share certificates on a blockchain. Then, blockchain’s immutability and security would become the industry's core competitive advantage, and the value of the tokens we hold would correspondingly increase.

MetaLeX is adopting this approach: creating fully programmable on-chain companies, where corporate capital, equity, and vesting schedules are all managed on-chain.

Back to the present, major centralized exchanges like Binance, Coinbase, and Kraken are heavily expanding into traditional finance, listing tokenized stocks, bonds, and ETFs. However, the xStocks platform failed to deliver the underlying physical shares, leading Binance, Bybit, and Bitget to delist SpaceX tokenized stocks, leaving over $1 billion in user orders unfulfilled. In contrast, trading orders through traditional brokers are more reliable.

Stablecoins were originally used for short-term asset parking while waiting to enter native crypto assets; now, they serve as a liquidity outlet to absorb capital from older, traditional finance investors.

Some might argue that pre-IPO tokenized stocks allow ordinary people to get early exposure to top-tier companies like OpenAI and Anthropic. Indeed, by market cap, these two are the hottest primary market tokenized assets, but both companies are valued close to a trillion dollars.

This is far from early-stage investing: Anthropic’s latest Series H strategic round valued the company at $965 billion. Funding rounds: Series A, B, C, D, E, F, G, H (latest)

The Tokenized Equity Sector Is Still in Its Infancy

Standard Chartered Bank set a price target of $100 for the Uniswap token UNI, implying a potential 40x increase! The logic follows: the bank predicts that the total value of tokenized assets circulating within decentralized finance will grow 37x by 2030 (from 3.5% of total assets currently to 30%); the total on-chain tokenized asset market could exceed $4 trillion by 2028.

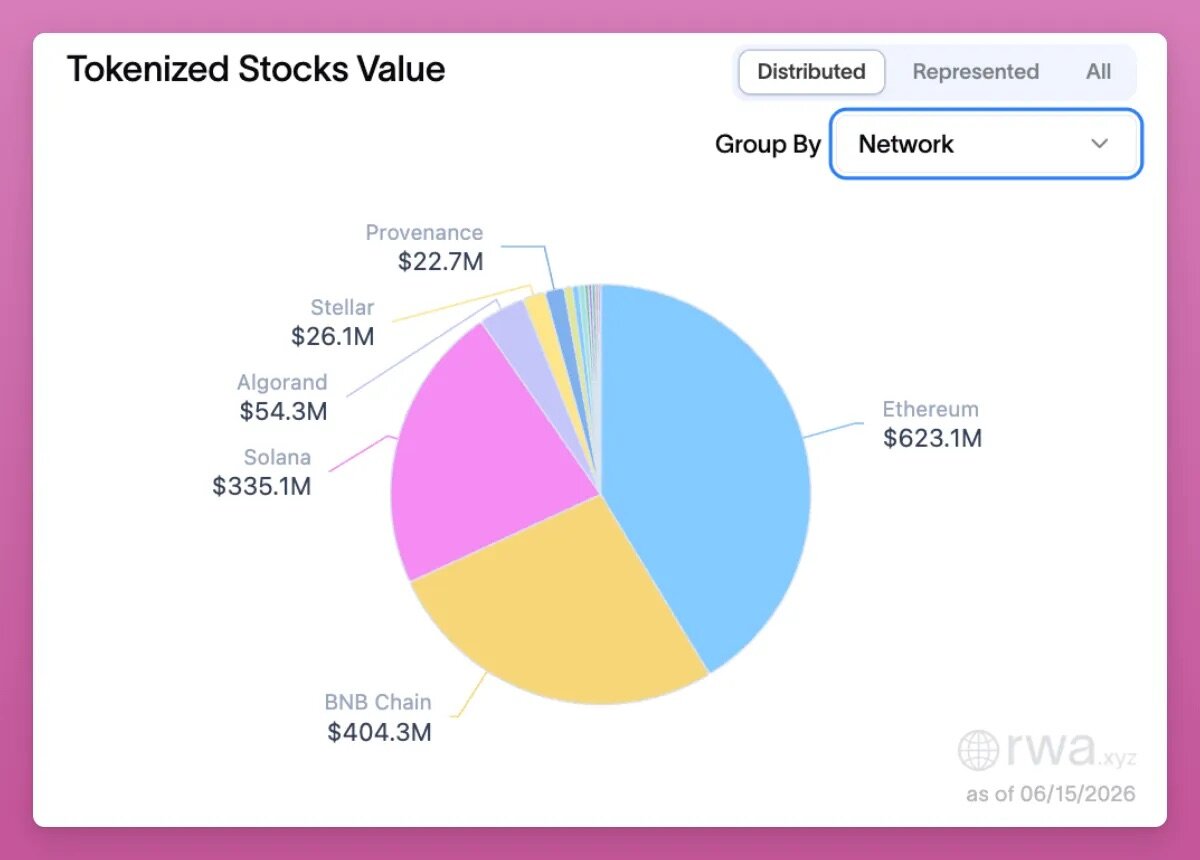

As of now, the freely transferable value of tokenized equities across platforms is $1.5 billion (these assets can be transferred peer-to-peer between wallets off the issuing platform), primarily deployed on Ethereum, BNB Smart Chain, and Solana. But the sector remains tiny: $1.5 billion is even less than Uniswap’s UNI token market cap of $1.9 billion.

Standard Chartered has a history of highly optimistic price predictions (previously forecasting Ethereum at $40,000 and Bitcoin at $500,000 by 2030), but the underlying logic for being bullish on UNI is sound: as the total value locked in tokenized equities rises, it drives on-chain trading volume higher and increases platform fees. These fees are now used to buy back and burn UNI tokens.

Uniswap won't be the only beneficiary. If the tokenized equity sector takes off, the entire crypto ecosystem will profit: lending protocols like Aave, Fluid, and Kamino, as well as DEXs on various chains like Pancakeswap and Jupiter, will all get a piece of the pie.

The development of tokenized equities could give crypto a counter-cyclical characteristic: currently, when Bitcoin and Ethereum prices fall, decentralized lending experiences significant deleveraging, protocol revenues shrink, and platform tokens come under pressure. Perpetual DEXs are the first to profit from tokenized stocks, with spot exchanges set to be the next wave of beneficiaries.

Following the Standard Chartered report, the UNI token rose 13% in a single day, but there are more investment opportunities within the sector. Over the past two weeks, Backpack’s platform token BP surged by 200%.

Backpack, as a centralized exchange, had previously struggled to find a core business that truly met market demand, competing against established giants like Binance while vying for users against Hyperliquid’s decentralized perpetual platform. Tokenized assets seem to have finally provided it with a core growth trajectory.

The vast majority of tokenized stocks on the market (xStocks, Ondo) use a custodial wrapping model: the issuer holds the physical stock, mints a token tracking its price, and users only gain price exposure without owning the actual equity. Backpack, via Superstate’s Opening Bell product line, achieves native on-chain issuance: these tokens are SEC-registered equities with the same rights as stocks listed on Nasdaq – holders are entitled to dividends and voting rights – and the platform holds all necessary compliance licenses (Backpack’s founding team is from the former FTX Europe division).

This logic extends to the platform's native token, BP: staking BP for one year allows holders to convert BP into actual corporate equity upon the company’s IPO or acquisition (with a 7-day redemption window each year).

There are also direct trading opportunities within the tokenized equity sector. By total freely transferable value, Ondo ranks second in the industry, and the platform has issued a native token, ONDO.

However, ONDO only serves governance functions and has almost no value capture mechanism otherwise; all platform revenue goes to the company, not to token holders. While the market is discussing activating fee-sharing mechanisms, their implementation remains uncertain. Moreover, the token faces immense dilution pressure, with nearly 50% of the supply still to be unlocked by 2029.

If market sentiment for tokenized equities heats up, there might be an opportunity for short-term speculation on ONDO, but I wouldn't hold it long-term.

The industry leader, xStocks, commands a 60% market share, with a total scale of about $1.7 billion. Backed Finance purchases real stocks and ETFs, places them with a custodian in a 1:1 reserve, and then mints tokens tracking the asset prices. Products are deployed on Solana and Ethereum (with a small portion on Arbitrum L2). Users can trade on the Kraken exchange five days a week, or trade 24/7 on-chain, covering approximately 60 assets. While the number of assets is fewer than Ondo, liquidity is better.

Holding an xStock token does not mean holding the underlying physical stock; it is merely a claim against the issuer. If the platform fails, investors are just unsecured creditors of a cross-jurisdictional wrapping service provider, a model completely different from Backpack's, where holders have real equity.

More ironically, Kraken filed its own IPO application just weeks before acquiring Backed Finance last year, at a valuation of $20 billion. This raises significant questions about whether the platform will issue an independent token.

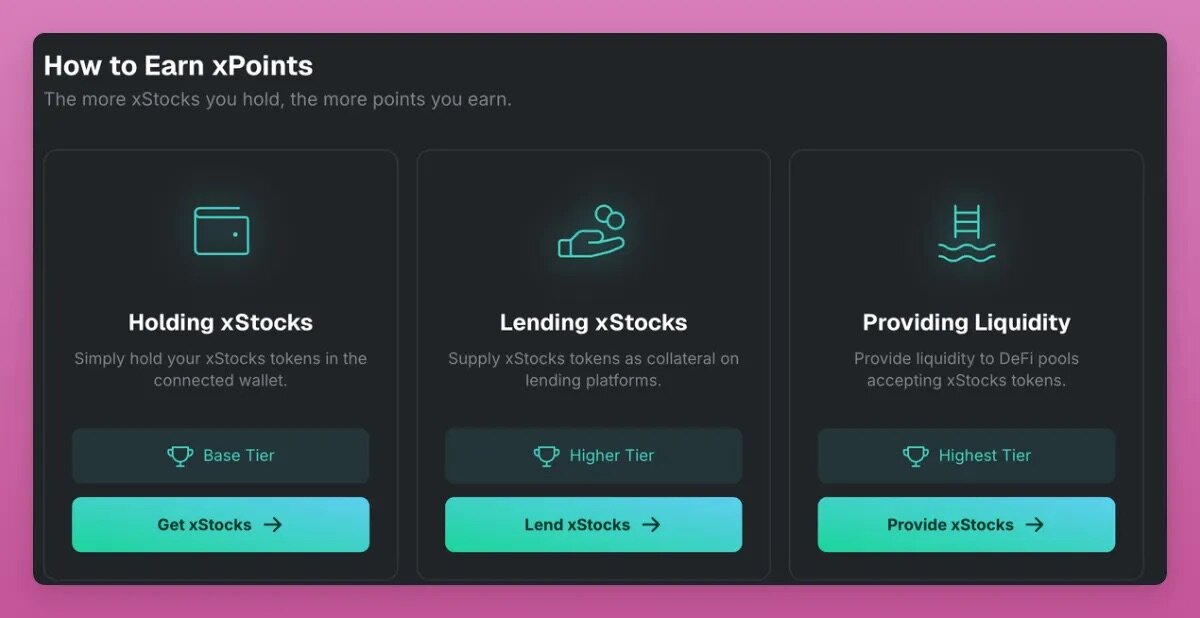

Following the acquisition, xStocks launched the xPoints campaign in March. Points programs usually precede a token launch, but the platform has yet to confirm if a token will be introduced.

xPoints Campaign Website

This is quite puzzling: since Kraken can already sell its own equity through traditional channels, why launch a separate xStocks platform token?

A more plausible explanation for the points program is that Kraken has partnered with Nasdaq for tokenized stocks, and the platform needs trading volume and liquidity to scale its business, thereby boosting Kraken’s overall performance metrics.

I don’t want to be the exit liquidity for this sector again. But if you are willing to participate in points mining, here are the rules for earning points:

- Providing liquidity: 7x points (highest tier, supporting Raydium, Orca, Byreal)

- Asset lending: 5x points (on Kamino)

- Simply holding the token: 1x base points

- Trading on the Kraken CEX does not earn points; only on-chain operations qualify.

The third largest player in the industry is Securitize, and I don't plan to participate in its points mining. The company will go public via a SPAC merger with Cantor Equity Partners, with an estimated valuation of $1.25 billion, led by a $47 million investment from BlackRock. The platform has no native token, so there’s no yield from mining.

As mentioned, there are several arbitrage strategies within the sector: for example, when perpetual funding rates are negative, you can short on Hyperliquid (also mining trade.xyz points) or Variational, while simultaneously buying spot tokens. You can also compare funding rates across exchanges on the Ostium platform (which currently has no token).

If managing positions manually is too cumbersome, you can look into the Nado platform. It is an order book DEX supporting spot, margin, and perpetual futures within a unified margin account. The development team previously built Kraken and launched the INK product. The platform will support tokenized stock spots and perpetuals, enabling delta-neutral strategies. It’s a low-profile opportunity worth considering for points farming.

But be cautious: the primary market token platform Ventuals just announced its shutdown, telling users that all platform points are now worthless. Participating in token airdrop mining now requires more effort, and the certainty of returns has significantly decreased.

The Story is Far from Over

The term "crypto" now encompasses a vast range of sectors, including perpetuals, NFTs, prediction markets, and meme coins. The RWA sector is also expanding rapidly, with sub-sectors deserving deep, individual analysis.

Stablecoins, money market funds, credit, private equity, and tokenized stocks are distinct subcategories, each with vastly different risk and return profiles.

The unique advantage of tokenized stocks lies in asset turnover efficiency: stocks have inherent price volatility, creating arbitrage and trading opportunities that don’t exist with passive real-world assets.

I believe this will lead to a resurgence for blockchains focused on trading, with Solana being a particularly strong beneficiary (I view Ethereum as a storage chain for high-value assets, better suited for passive investment).

Previously, the Solana ecosystem was heavily reliant on meme coins. The new narrative of "everything tradable