Oracle's Earnings Report Revealed: With AI Cloud Orders Exploding, Where Will the Money Come From?

- Core Thesis: Oracle's central contradiction has shifted from "whether it has an AI story" to "the cost and return of the AI story." While its $553 billion RPO (Remaining Performance Obligations) signals strong demand, the market is closely watching whether massive capital expenditure (CapEx) can be translated into high-quality profits and free cash flow.

- Key Elements:

- Q4 Earnings Market Expectations: Revenue of approximately $19.1 billion, adjusted EPS of roughly $1.96; total cloud revenue guidance of 46%–50% year-over-year growth. This serves as the baseline for assessing performance.

- RPO reached $553 billion, up 325% year-over-year: Represents the scale of contracts signed but not yet recognized as revenue, acting as a "visibility" indicator for future income. However, a high RPO also implies immense delivery pressure and significant upfront capital requirements.

- Core Contradiction: AI cloud infrastructure is an asset-heavy model requiring significant upfront investment in data centers, GPUs, and power. High CapEx is reshaping the company's financial structure, with market concerns that Oracle may transition from a high-cash-flow software company to a capital-intensive entity.

- Key Earnings Watchpoints: Whether cloud revenue approaches the upper end of guidance, RPO continues to expand, the strength of FY2027 revenue guidance, and management's clear articulation of CapEx pacing and cash flow improvement strategies.

Oracle's problem isn't that it lacks an AI story. It's that the story has become expensive enough to warrant serious scrutiny.

After the US stock market closes on June 10, Oracle will report its FY2026 Q4 earnings. The market currently expects Q4 revenue of approximately $19.1 billion and adjusted EPS of around $1.96. Last quarter, Oracle provided Q4 guidance for total revenue growth of 19%–21% year-over-year, total cloud revenue growth of 46%–50%, and non-GAAP EPS of $1.96–$2.00.

Looking at these numbers alone, Oracle remains firmly in the AI cloud narrative.

Meanwhile, over the past year, OCI, AI cloud orders, large customer contracts, data center expansion, and market imagination surrounding clients like OpenAI, Meta, and NVIDIA have repositioned Oracle from a traditional database and enterprise software company into the investment framework of AI infrastructure.

But for this earnings report, the market's real focus is no longer whether Oracle has an AI story, but rather: AI cloud orders are massive, but are these orders worth the high capital expenditure Oracle is committing to them?

1. By the Numbers, Oracle is Already at the AI Cloud Table

Oracle's most staggering data point last quarter was undoubtedly its RPO reaching $553 billion, a 325% year-over-year increase.

RPO can be simply understood as the scale of contracts the company has already signed but has not yet recognized as future revenue. For cloud computing companies, a larger RPO typically implies higher future revenue visibility, broadly reflecting demand sentiment and reserved computing capacity.

This is why, after Oracle disclosed its RPO last quarter, the market quickly included it as one of the core targets within AI cloud infrastructure.

However, it's crucial to note: RPO is not profit, nor is it cash flow arriving immediately. Instead, it's more like a massive order book – a thicker book certainly indicates stronger demand, but it leads investors to ask three more practical questions: When will these orders be delivered? How much capital needs to be deployed upfront before delivery? And after delivery, will the gross margin and cash recovery speed be satisfactory?

This is the core divergence surrounding Oracle now.

- Bulls argue that the $553 billion RPO proves AI cloud demand is real, long-term, and already locked in by large customers, positioning Oracle as a key capacity provider during a period of tight AI compute supply;

- Bears, however, worry that if fulfilling these orders requires massive data center investments, GPU procurement, power resources, and long-term financing, then the higher the RPO, the greater the potential pressure on short-term free cash flow and the balance sheet.

So, Oracle's RPO itself isn't the issue.

The real question is how quickly RPO can be converted into revenue, and at what level of profitability and cash flow quality it translates into shareholder value.

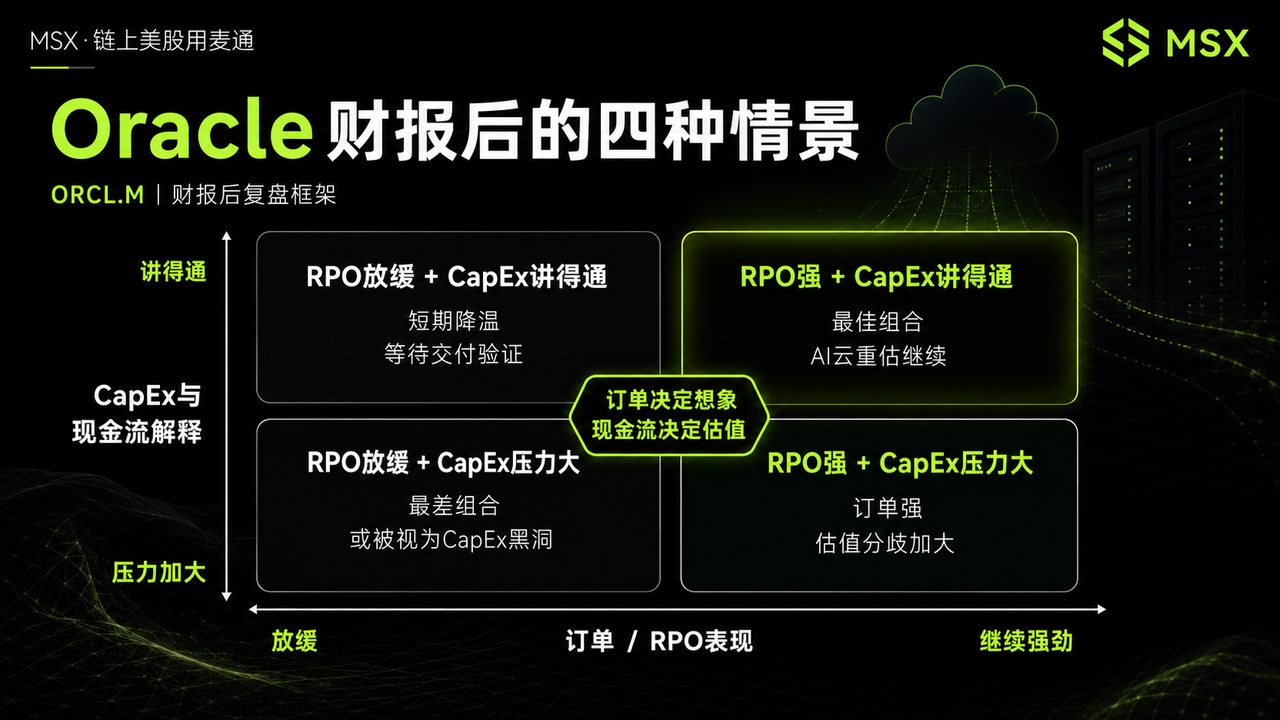

This brings us to the first key focus of this earnings report: whether RPO continues to expand and whether management can provide a clearer timeline for order fulfillment. If RPO hits new highs, it signals that large AI cloud contracts are still flowing in, enhancing Oracle's future revenue visibility. However, if RPO growth decelerates significantly, the market may worry that the peak of AI cloud orders is passing.

Orders are the starting point of the story, not the endpoint.

For Oracle now, the market has acknowledged it has secured its ticket to the AI cloud game. The next step is to see if it can turn that ticket into real revenue, profit, and cash flow.

2. The Story is Expensive: CapEx Pressure Behind OCI Growth

Oracle's most core label has historically been databases and enterprise software.

But now, the market is far more focused on OCI, or Oracle Cloud Infrastructure.

Last quarter, Oracle guided for Q4 total cloud revenue growth of 46%–50% year-over-year. If actual cloud revenue approaches or exceeds the high end of this guidance, it indicates that AI cloud demand remains robust and OCI's growth trajectory hasn't materially slowed. Conversely, if cloud revenue falls short of expectations, the market will worry that, despite the large RPO, the conversion and delivery pace of orders may not be as fast as imagined.

This highlights the major difference between AI cloud and traditional software.

Traditional software companies have low marginal costs, making revenue growth easier to convert into profit. But AI cloud infrastructure is not an asset-light business; it requires building data centers in advance, procuring GPUs, and securing capabilities for power, land, cooling, networking, and operations.

Orders can be signed quickly, but data centers cannot be built overnight, GPUs don't arrive automatically, and power capacity isn't always readily available.

Therefore, Oracle's biggest bottleneck now may not be a lack of demand, but a lack of capacity to meet that demand.

This is also why the market has become more critical of Oracle.

If it were a pure software company, incremental revenue would typically bring high incremental profit margins. But as Oracle is increasingly priced by the market as an AI cloud infrastructure company, it must submit to a different set of scrutiny standards: capital expenditure intensity, asset turnover efficiency, depreciation pressure, financing costs, free cash flow, and long-term return on invested capital.

In other words, Oracle hasn't simply upgraded from a "software company" to an "AI company." It's more like a high-cash-flow enterprise software company transforming into one that simultaneously operates a software business and a heavy-asset AI cloud business. The valuation logic has changed, and the market will naturally re-price it.

This is a key reason why Oracle's stock price has faced pressure recently. The market isn't rejecting AI cloud demand; it's worried that Oracle might take on excessive capital expenditure pressure to chase orders.

Therefore, in this earnings report, management must address several questions:

- How much higher will future CapEx go?

- Can data center construction keep pace with orders?

- Are the gross margins on AI cloud contracts good enough?

- When will free cash flow improve?

- Are financing costs and balance sheet pressures manageable?

These questions are more important than simple revenue and EPS figures. Oracle's trading focus has shifted from "does it have AI orders?" to "can these AI orders generate adequate returns on capital?"

If management merely continues to emphasize strong orders, it may no longer suffice. What the market truly wants to hear is how fast Oracle can convert these orders into revenue-generating cloud capacity, and whether that capacity will ultimately yield high-quality cash flow.

3. AI Cloud Dark Horse, or CapEx Black Hole?

This Oracle earnings report is, in essence, an examination of AI cloud capital returns.

From a data perspective, the market will first focus on whether Q4 revenue and EPS meet expectations. The market anticipates revenue of ~$19.1 billion and EPS of ~$1.96. Merely meeting expectations may not be enough to alleviate CapEx concerns. A clear beat, especially with both cloud revenue and earnings quality performing well, would provide stronger support for the stock price.

Second, the focus will be on whether cloud revenue approaches or exceeds the high end of guidance. Last quarter, Oracle guided for 46%–50% year-over-year growth in total cloud revenue for Q4. This is a key indicator of whether OCI is accelerating. If cloud revenue is near or above the high end, it confirms AI cloud demand is materializing. If it falls short, the market will re-evaluate the pace of RPO conversion.

Third, the market will watch for RPO expansion. If RPO continues to hit new highs, it suggests large AI cloud contracts are still incoming, increasing Oracle's future revenue visibility. But if RPO growth slows markedly, the market may fear the peak of AI cloud orders is passing.

Fourth, the focus will be on whether FY2027 revenue guidance is strengthened. The market is now highly focused on Oracle's revenue visibility over the next year. If management can further reinforce the AI cloud growth trajectory and order conversion pace, Oracle's AI cloud narrative will be on firmer ground. Conversely, weak future guidance could lead the market to believe current valuations have already priced in too much optimism.

Finally, and most importantly, is the CapEx and cash flow narrative. Oracle must prove that its current high spending isn't just chasing the AI trend, but will translate into higher future revenue, better margins, and more stable cash flow.

If management can clearly articulate the CapEx cadence, data center delivery timelines, customer demand, financing arrangements, and the path to free cash flow improvement, market concerns about Oracle will ease. However, if these issues remain vague, the stock price may continue to oscillate around the tension between "growth" and "cash burn."

This is the core of the current divergence on Oracle.

Bulls believe Oracle is becoming a capacity provider in the AI cloud era. In a context of tight AI compute supply, whoever can offer stable, scalable cloud capacity will secure large customer orders and long-term revenue visibility. Oracle's advantages lie in its existing enterprise customer base, its portfolio of database and cloud services, and the massive order book it secured during the AI cloud demand explosion.

From this perspective, Oracle is no longer just a traditional software company but a crucial link in the AI infrastructure chain.

But bears worry Oracle is buying growth with increasingly high capital expenditures. AI cloud is not an asset-light business. Data centers can face delays, power and GPU supply can be constrained, depreciation and financing costs can rise, and free cash flow can remain under pressure. If order fulfillment disappoints or gross margins are lower than expected, Oracle's AI cloud story could shift from "high growth" to "high spending, low returns."

Neither argument is entirely without merit.

The bull case for Oracle rests on real AI cloud demand, extremely strong RPO, fast OCI growth, and long-term revenue visibility from large customer contracts. The bear case centers on the heavy-asset nature of AI cloud changing the company's financial structure, requiring the market to reassess its cash flow quality and capital return capability.

This Oracle earnings report isn't a proof problem for the AI story; it's a proof problem for capital expenditure returns.

If RPO continues to expand, cloud revenue maintains high growth, management strengthens future revenue visibility, and CapEx, cash flow, and financing arrangements are explained clearly enough, then Oracle's AI cloud story can continue to be told.

But if growth remains primarily at the order-book level without alleviation of delivery, cash flow, and CapEx pressures, the market will rightly ask: is this an AI cloud dark horse, or a CapEx black hole?

In a nutshell, Oracle just needs to prove that these orders are worth burning that much cash.