The History of Crypto Prediction Markets: Elite Fall, Duopoly Rise, and a Hundred Schools of Thought

- Core Thesis: This article systematically reviews the development history of prediction markets, from a 1988 academic experiment at the University of Iowa to a competitive landscape of multiple contenders in 2026. It reveals the evolutionary path from the illusion of idealistic decentralization to the pragmatic, dual-track approach of compliance and wild growth, pointing out that the industry has entered a new phase defined by mechanism design and capital dominance.

- Key Elements:

- The 1988 Iowa Electronic Markets (IEM) experiment proved that the wisdom of crowds, based on real-money incentives, could predict outcomes more accurately than traditional polls, establishing the fundamental logic of prediction markets.

- From 2014 to 2018, decentralized projects like Augur attempted to build an "unshutdownable Intrade" using blockchain. However, due to high Ethereum gas fees, complex dispute mechanisms, and the controversy surrounding "assassination markets," they ultimately became mired in low user adoption and liquidity dry-ups.

- From 2019 to 2020, modular projects like Omen solved the underlying architecture by integrating Gnosis conditional tokens, Reality.eth oracles, and the Kleros on-chain court. Nevertheless, they still failed to achieve mainstream adoption due to high barriers to entry and cumbersome governance.

- After 2020, two giants emerged: Kalshi (the compliant establishment faction) and Polymarket (the wild west faction). The former secured regulatory approval by fighting for a CFTC license, while the latter monopolized global traffic and mainstream awareness through low-cost L2 solutions and stablecoin settlement.

- Polymarket exposed the flaw of capital manipulating outcomes (e.g., UMA whales altering truth), while Kalshi was constrained by the ceiling of compliance. This represents the ultimate trade-off between "speed and risk" versus "compliance and stability."

- The 2024 U.S. presidential election became a turning point for the sector. A single market on Polymarket attracted over $36 billion in liquidity, validating a trillion-dollar level of demand and attracting a wave of capital and major players to enter the market, creating a highly competitive landscape.

- In 2026, the prediction market ecosystem saw comprehensive growth, with multiple development paths emerging: the yield generation faction (Predict.fun), the macro-focused faction (Opinion.trade), and the protocol-layer outlier (42.space). These are also deeply integrated with traditional sports betting and public chain ecosystems.

01 Origin: An Economics Class in Iowa

In the 1990s, U.S. public opinion and financial decisions largely relied on professional polling agencies. The entire industry defaulted to the judgments of authoritative institutions, believing they provided the closest approximation to the truth.

For example, after the first oil crisis erupted in 1973, public opinion in the U.S. business community was thrown into a state of extreme panic.

Image: A 1974 U.S. gas station warning sign. The consumer panic following the oil crisis became the historical backdrop for the inaccuracy of traditional polls. Source: Wikimedia Commons

At the time, the most authoritative Harris Poll continuously released reports on public sentiment, concluding that "American consumers have completely abandoned large cars, and the entire nation will fully shift to compact, fuel-efficient vehicles over the next decade."

Armed with this definitive conclusion, Detroit's auto giants and Wall Street investment banks treated the poll as the "market truth."

In the absence of sufficient sales evidence, Ford and Chrysler, relying solely on polling data, hastily cut multiple profitable large-car production lines and invested hundreds of millions of dollars into forcibly developing small cars, an area where they lacked expertise. Wall Street subsequently readjusted its valuation models for the entire automotive industry stock.

This industry-wide portfolio shift, directly triggered by polling data, led U.S. automakers to suffer prolonged passive losses in the following years when faced with the aggressive攻势 of Japanese fuel-efficient cars.

This demonstrated that while the public opinion polling system of the time played a positive role, its accuracy was not highly reliable.

Then, in 1988, three professors from the University of Iowa—George Neumann, Robert Forsythe, and Forrest Nelson—began to boldly question the traditional polling system: Could the judgment of a few experts truly surpass the collective judgment of millions?

Image: Old Capitol at the University of Iowa, where the IEM academic prediction market experiment began in a classroom. Source: Wikimedia Commons

To test this hypothesis, they abandoned traditional methods like paper surveys and questionnaires. In an economics classroom at the University of Iowa, they conducted a niche experiment that challenged conventional wisdom:

They built a minimalist trading market open to students for trading U.S. presidential election outcomes, setting clear capital thresholds. Participants could deposit a minimum of $5 and a maximum of $500, using real money to price expectations through genuine competition.

The trading price within the market corresponded directly to a candidate's probability of winning. After the election, participants who bet correctly would split the entire prize pool proportionally.

Interestingly, the market price formed by the spontaneous competition of ordinary traders had a prediction error 0.5% lower than all professional national polls.

Without expert endorsement, data models, or media guidance, relying solely on the collective competition of real interests, this model easily outperformed the entire industry's authoritative judgment system, shocking the academic world.

In fact, when everyone bets for their own benefit, a freely flowing trading market becomes the optimal vehicle for uncovering hidden information, predicting the future, and revealing the truth.

This new polling model was later named the Iowa Electronic Markets (IEM).

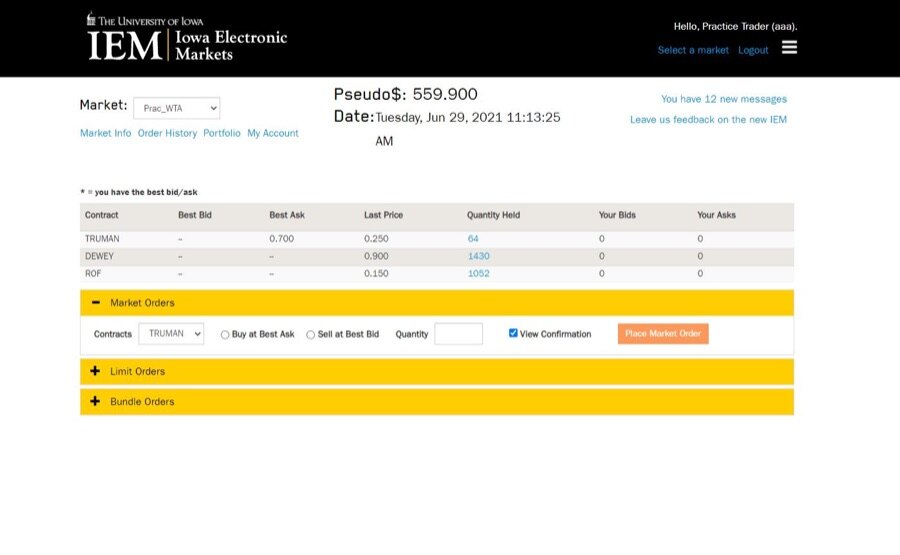

Image: Example of the Iowa Electronic Markets (IEM) trading interface. Source: https://csi.its.uiowa.edu/our-work/iowa-electronic-markets

This experiment can be seen as the first instance where collective intelligence triumphed over elite authority in a quantifiable and practical way, laying the core underlying logic for prediction markets thirty years later.

However, at the time, IEM was considered an "outlier" and struggled for mainstream acceptance.

On one hand, traditional polling systems relied on expensive sample surveys, telephone interviews, or offline questionnaires.

This model supported a vast ecosystem of academic institutions, news media think tanks, and political consulting firms, underpinned by complex interests.

The result of amateur traders outperforming professional analysts directly threatened the authority and commercial value of traditional polling institutions, essentially encroaching on their "turf."

Consequently, the IEM model of predicting election results by buying and selling contracts was defined as illegal gambling at the time.

Although the IEM received an exemption from the U.S. Commodity Futures Trading Commission (CFTC), it was strictly limited to "academic research" and prohibited from commercialization.

Because of this, the platform imposed strict limits on the trading capital of each participant (typically allowing only $5 to $500), preventing the market from achieving the scale and liquidity needed to compete with mainstream financial markets or commercial polling agencies.

On the other hand, as a university-led academic experiment, the interface and participation门槛for this model were relatively complex for the general public, many of whom couldn't even recite multiplication tables.

Therefore, the IEM's primary participant base was limited to scholars, specific students, and a small group of enthusiasts, failing to establish a popular use case.

For nearly two decades afterward, IEM remained trapped within academic circles, unable to reach the masses or grow, ultimately becoming a niche research tool.

02 The Idealist's "Eye of God"

In 1999, Irish entrepreneurs Ron Bernstein and Sean McNamara founded the prediction market internet platform Intrade. Subsequently, in 2003, the platform was acquired by Tradesports. Irish accountant John Delaney served as its CEO, and under his leadership, it became one of the most famous prediction markets.

Image: Intrade co-founder Ron Bernstein (left). Source: https://www.youtube.com/watch?v=2rYpzgeCRlw

Of course, Intrade positioned itself as a commercial prediction market open to the global public, meaning its goal was to make money. Users could trade on real-world outcomes such as U.S. presidential elections, wars, economic data, and corporate events. The market price could be seen as a real-time reflection of the probability of an event occurring.

As a first mover, Intrade quickly grew into one of the most influential prediction market platforms globally. Its trading prices were not only widely cited by the media but also served as an important reference for political analysts, scholars, and some Wall Street institutions observing future trends. Especially for major events like U.S. presidential elections, Intrade's prediction accuracy was often higher than many traditional polling agencies, earning it a reputation as the industry benchmark.

However, as its influence grew, established capital powers became displeased and began to wield regulatory sticks.

Because the platform allowed U.S. users to trade contracts involving political, economic, and financial events, U.S. regulators gradually viewed it as an unlicensed derivatives exchange. In 2012, the CFTC sued Intrade, accusing it of offering unlicensed event contract trading services to U.S. investors.

Image: U.S. Commodity Futures Trading Commission (CFTC). Intrade's commercial expansion ultimately collided with regulatory boundaries. Source: Wikimedia Commons

Facing regulatory pressure, Intrade was forced to block access for U.S. users. However, the U.S. market accounted for the majority of its trading volume. After losing its core user base, the platform's liquidity rapidly shrank. Simultaneously, internal disputes over fund management and financial problems erupted. Finally, in 2013, Intrade announced the cessation of all trading operations and entered liquidation.

This platform, once globally popular and considered the most likely to bring prediction markets into the mainstream financial system, thus exited the historical stage under the dual pressures of regulation and business crisis.

But the story of prediction markets was just beginning.

The Pioneer of Decentralized Prediction Markets: Augur

Intrade's sudden shutdown due to regulatory crackdown deeply affected a young American named Jack Peterson.

At the time, Jack Peterson was a quintessential academic. In his early thirties, he already held a Ph.D. in Biophysics from the University of California, San Francisco, and was a recipient of the U.S. Department of Defense Science Scholarship, deeply involved in research on biophysics and complex system games.

In his view, Intrade's prediction market model brought research closest to the truth, and its collapse made him realize that any trading system built by humans can never escape power intervention and interest manipulation. As a scholar obsessed with the underlying logic of collective intelligence, he felt compelled to act.

In 2014, he abandoned a stable scientific career, dove headfirst into the early blockchain space, and immersed himself in researching on-chain consensus, event adjudication, and game incentive systems. He aimed to let code replace human judgment, making outcomes as fair as possible and free from centralized interference.

Similarly, Joey Krug, a 19-year-old freshman at a California liberal arts college, was a cryptography geek. A prodigy, he had encountered Bitcoin early on and was captivated by the narrative of decentralized, permissionless finance. He frequented Ethereum's earliest core Skype community, discussing the ecosystem's future daily with early cypherpunks like Vitalik Buterin, and keenly sensed that prediction markets would be Ethereum's first killer app.

On another front, a young man named Jeremy Gardner, inspired by Bitcoin's ideals, dropped out of college to found the nation's largest university crypto club, spreading the crypto gospel across campuses, hoping to attract more young people to the cryptographic wave.

Around 2014, they gradually got to know each other within the earliest Ethereum developer community.

At the time, Jack Peterson was researching how to use blockchain to reconstruct prediction markets and was developing an early prototype called Dyffy. Meanwhile, the 19-year-old cryptography prodigy Joey Krug was already active in Bitcoin and Ethereum developer circles, deeply interested in the potential of smart contracts. The two instantly connected over the shared vision of decentralized prediction markets.

For Joey, continuing academic theory was less appealing than personally participating in the experiment about to change internet rules. He subsequently dropped out of Pomona College to dedicate himself full-time to project development.

Soon after, Jeremy Gardner joined them. This young evangelist possessed strong community organization skills and a talent for spreading ideas. He helped the project quickly build its initial base of supporters and spread its vision throughout the Ethereum ecosystem.

As the team took shape, they launched the decentralized prediction market project Augur and later established the non-profit Forecast Foundation to oversee the protocol's long-term development and governance.

In terms of team division of labor, Jack Peterson was responsible for prediction market mechanisms, game theory models, and protocol architecture design; Joey Krug handled smart contract development and technical implementation; Jeremy Gardner focused on community building, advocacy, and ecosystem expansion.

The key difference from Intrade was that Augur aimed to completely eliminate the role of a centralized operator. Anyone could create markets freely without platform approval. Event outcomes would be adjudicated by $REP holders through on-chain consensus, rather than relying on a centralized agency for arbitration. Even if the founding team left, the protocol could continue to operate.

It wasn't the beginning of prediction markets, but it was the first time in history someone attempted to reconstruct them using blockchain. In a sense, Augur aimed to create an Intrade that no one could shut down. This way, even if future regulatory crackdowns occurred, they couldn't eliminate the entire market by merely shutting down a single company.

In 2015, Augur conducted one of the earliest IC0s in the Ethereum ecosystem, successfully raising $5.1 million and issuing the $REP governance token. Vitalik Buterin personally served as a project advisor. The project was at the peak of its glory.

Gnosis: The Hidden Master from Berlin, Building Foundations, Not Seeking the Throne

While Jack Peterson and the Augur team were attempting to rebuild Intrade using blockchain, a team in Berlin, Germany, was also focusing on prediction markets.

Germany's Stefan George and Martin Köppelmann were among the earliest tech geeks to encounter Bitcoin and Ethereum, but their development paths differed.

Stefan George came from a traditional software background, having worked within the SAP system for years on enterprise software development. Compared to American crypto entrepreneurs who reveled in revolutionary narratives, he was more like a typical German engineer, with an almost obsessive interest in system design and underlying architecture. After encountering Bitcoin in 2013, he became deeply fascinated by this peer-to-peer cash system.

Martin Köppelmann entered the crypto world even earlier. He started researching cryptography and distributed systems in university and was already a well-known developer and evangelist in the German Bitcoin community around 2013. Compared to Stefan, Martin had a more idealistic streak. He had long been interested in market mechanisms, collective decision-making, and using open networks to coordinate collaboration among strangers.

The two first met in the German Bitcoin and Ethereum communities. (It's worth noting how much the Bitcoin and Ethereum communities contributed to the industry's early days.)

At the time, Berlin was becoming one of Europe's most important crypto hubs. A large number of developers, cryptography researchers, and free software geeks gathered there, discussing Bitcoin, smart contracts, and the future shape of the internet.

Stefan and Martin were also both focused on prediction markets, frequently engaging in deep discussions about them, hoping to reshape the model in a decentralized way.

However, their perspectives differed. They realized that while prediction markets appear to trade presidential elections, World Cup champions, or interest rate decisions, what they actually trade are future outcomes themselves. If future outcomes cannot be expressed in a standardized way, no matter how ingeniously designed the market mechanism is, it will struggle to scale.

What does that mean?

For instance, the Augur team was constantly thinking about how to rebuild a decentralized version of Intrade. They focused on market governance, event adjudication, dispute resolution, and how to use economic incentives to make the system self-sustaining. Whether it's the U.S. presidential election, the World Cup winner, or the Fed's interest rate decision, these are essentially trades on future outcomes. But future events themselves cannot be traded directly on-chain.

So, to make a market viable, you first need to deconstruct complex real-world events into standardized outcomes. These outcomes must then be mapped into on-chain assets that can be traded, settled, and circulated.

Based on this idea, the duo designed a framework. This framework allows developers to break down a real-world event into multiple possible outcomes and generate corresponding on-chain assets for each.

For example, a presidential election can be broken down into the victory outcomes of different candidates; the World Cup can be broken down into the possibilities of different teams winning; an interest rate decision can be broken down into scenarios like rate hike, rate cut, or hold steady. Ultimately, these are mapped into tokens. Users are no longer just trading a market; they are trading the various possibilities of the future itself.

In 2015, just before the Ethereum mainnet launch, Stefan George and Martin Köppelmann launched the Gnosis project, hoping to make significant strides on Ethereum.

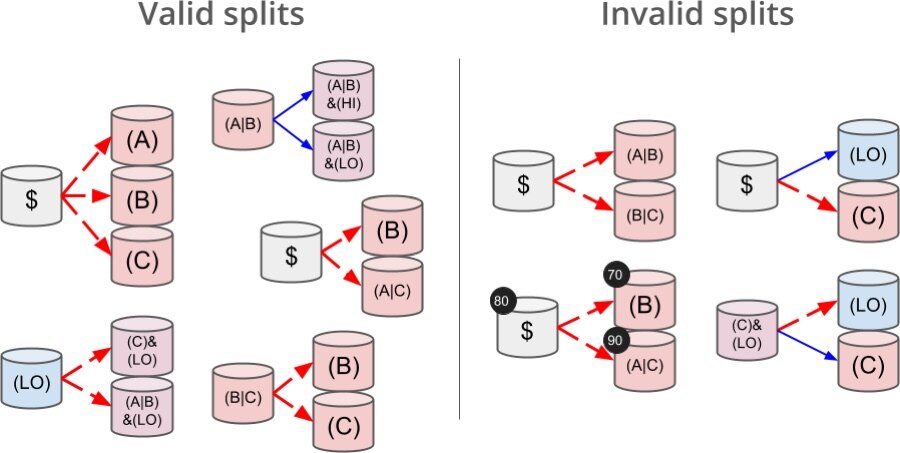

As a side note, many people later came to see Gnosis as an infrastructure project, but in reality, it entered the industry as a prediction market startup. Gnosis poured increasing resources into building the underlying framework. After years of exploration and iteration, the team developed the Conditional Tokens framework, which would later influence the entire industry. But that's a story for later.

Image: Diagram illustrating valid/invalid partitions in Gnosis Conditional Tokens. Source: https://conditional-tokens.readthedocs.io/en/latest/developer-guide.html

Returning to the Conditional Tokens framework we just mentioned: today, this logic of assetizing events seems quite natural, but at the time, it was a significant breakthrough in the development of prediction markets.

It provided the industry with its first unified standard for assetizing events, allowing future events to enter the on-chain trading system in a standardized way. The underlying logic of Gnosis's own Omen and the rapidly rising Polymarket can both trace their roots back to this Conditional Tokens framework.

When the IC0 frenzy arrived in 2017, Gnosis became one of the most attention-grabbing star projects. The project completed a financing round of approximately $12.5 million in a short time and was once considered one of the most promising entrepreneurial projects in the Ethereum ecosystem. However, unlike Augur, as the industry matured, Gnosis did not continue to allocate