Reviewing the History of China's Crypto Exchanges: Wild West Rise, Offshore Exodus, and Compliance Rebuilding

- Core Thesis: This article systematically outlines the development journey of Chinese cryptocurrency exchanges from their inception in 2011 to 2026. The central narrative traces: from the dominance of the domestic market by the Big Three—BTCC, Huobi, and OKCoin; through the forced closures following the "September 4" regulation in 2017; to the offshore rise of platforms like Binance; and finally, to an industry entering a new phase of global compliance and professionalization amid comprehensive crackdowns in 2021 and large-scale regulatory settlements after 2022.

- Key Elements:

- Three Major Eras: 2011-2017, the domestic wild west and the era of the Big Three; 2017-2021, the offshore migration and secondary boom; Post-2021, global compliance restructuring and the complete clearance of the mainland market.

- Key Regulatory Milestones: The "September 4" announcement in 2017 terminated domestic fiat currency trading; The "September 24" notice in 2021 classified all cryptocurrency-related businesses as illegal financial activities, with overseas platforms serving Chinese clients also deemed non-compliant.

- Fate of Major Players: Li Lin (Huobi) cashed out and exited; Justin Sun took over and renamed it HTX. Xu Mingxing (OKX) stepped back from the spotlight as OKX achieved a $25 billion valuation after an investment from the Intercontinental Exchange (ICE). Changpeng Zhao (Binance) paid a $4.3 billion fine, served a brief prison term, and subsequently received an investment from Abu Dhabi's MGX.

- Evolution of Industry Structure: From the HBO (Huobi, Binance, OKEx) triad rivalry to a stable state by 2026, dominated by OKX (globally compliant), Binance (under regulatory pressure), and differentiated service providers like HTX, KuCoin, and Gate.io.

- Core Supporting Data: From 2014 to 2016, China's three largest exchanges accounted for over 80% of global Bitcoin trading volume. By 2021, mainland China's market trading volume had dropped to zero. OKX's valuation reached $25 billion.

This article took me five days of extensive research to compile the history of Chinese crypto exchanges, aiming to review the transformation of China's cryptocurrency exchanges from their rugged beginnings to global reshaping. I believe this is also an industry saga interwoven with technological idealism, wealth mania, regulatory shifts, and global migration.

From the birth of BTC China in a Shanghai apartment in 2011, to the tripartite struggle sparked by Huobi and OKCoin in 2013; from the era when the Chinese yuan once dominated the global Bitcoin market, to the abrupt end of the golden age for domestic exchanges with the "9.4" regulation in 2017; from Binance, HTX, OKX and other platforms shifting to offshore markets, to the compliance restructuring in an era of strict regulation, the story of Chinese exchanges encapsulates almost the entire journey of the crypto industry from chaos to order.

Over this decade-long path, some rose from internet cafes and residential apartments to the world stage, some topped the global rankings amidst bull and bear cycles, some sold their stakes and exited, some retreated behind the scenes, and others sought a ticket back into the mainstream financial system under the heavy pressure of regulation.

Are you ready? Let's start from that unmarked Shanghai apartment and retrace this path of Chinese exchanges—through primitiveness, frenzy, overseas expansion, and compliance.

01 The Primitive Dawn

During the rainy season of 2011 in Shanghai, the humidity and heat were suffocating. In a less than 20-square-meter apartment in Jing'an District, there wasn't even a proper signboard. Two worn-out computer desks and a jam-prone second-hand printer constituted all the assets of China's earliest cryptocurrency exchange.

Yang Linke, cigarette dangling, stared at the flickering characters on the screen. Huang Xiaoyu typed out the last line of matching engine code. These two young men, scraping by on the fringes of the internet, never expected they were pushing open a primitive door that would eventually sweep the globe.

Back then in China, no one considered Bitcoin a legitimate business. This string of virtual code from overseas was hidden only in the corners of geek forums. And the story of China's cryptocurrency exchanges quietly began with these two young men of vastly different backgrounds and personalities.

Yang Linke was a native of Wenzhou, Zhejiang. Born in 1985, he never took the conventional path of schooling. Dropping out in his early teens, he worked as a network administrator in internet cafes in Wenzhou and Shanghai, spending his youth fixing machines, troubleshooting errors, and watching gamers play amidst the smoky air. Later, he dabbled in virtual items and built small websites, never making big money but sharpening an eye for niche demands.

He didn't understand cryptography, nor had he ever been in touch with overseas geek circles. When he first saw "Bitcoin" on a tech forum in 2010, his sharp instincts told him this was a virtual token that could be transferred online without any control. A simple thought popped into his head: if people are playing with it, some will want to trade it; if there's trading, there needs to be a place to match buyers and sellers.

At that time, even over-the-counter trading of Bitcoin in China was scarce. Buyers and sellers posted on forums, transferred money privately, and manually moved coins—it was cumbersome and dangerous, like roadside bartering before organized markets existed. Yang Linke saw this unclaimed territory, but he had no technology, no team. All he could do was find someone who could code to partner with.

The person he found was Huang Xiaoyu.

Unlike grassroots-born Yang Linke, Huang Xiaoyu was a well-known tech geek in the small circle. Deeply immersed in programming for years, he specialized in website development and backend architecture. He was also among the earliest in China to understand Bitcoin's underlying logic. Introverted and not one for the spotlight, he was obsessed only with code and decentralized technology. When Yang Linke found him on a forum and bluntly said, "I'll handle operations, you write the code, let's build a Bitcoin trading website together," Huang Xiaoyu agreed almost without hesitation.

Perhaps it wasn't for the money, but for a geek's stubborn conviction—something so pioneering deserved a Chinese trading platform of its own.

The two pooled together tens of thousands of yuan as startup capital, rented this residential apartment office, with no investors, no formal employees, and no compliance procedures. They wrote code and adjusted pages during the day, promoted on forums at night. When hungry, they ate instant noodles; when tired, they slept on the desk.In June 2011, BTC China (BTCC) officially launched, becoming China's first cryptocurrency exchange and one of the earliest trading platforms globally.

The early BTCC website was extremely rudimentary, featuring only the simplest order book and price chart. There wasn't even a candlestick chart, and the only tradable asset was Bitcoin. Deposits and withdrawals were entirely manual: users transferred money to Yang Linke's personal bank account, and he manually checked and credited their crypto balance. For withdrawals, users submitted requests, and Huang Xiaoyu manually sent the coins one by one.

The first batch of users numbered only a few hundred—all programmers, geeks, and overseas students—with daily trading volume of just tens of thousands of yuan. Yang Linke later recalled that at that time, they never thought about making money; they just felt they were doing something very cool, like building the first road through uncharted territory.

Two ordinary people—one daring to dream, one daring to act—set up the first tent of Chinese exchanges in the wilderness.

But this grassroots geek site remained tepid for a full two years after its launch, never breaking out of its small circle. It wasn't until 2013 that an elite from overseas stepped in, completely rewriting BTCC's fate. His name was Bobby Lee.

Bobby Lee's life was worlds apart from Yang Linke's and Huang Xiaoyu's.

He went to the US for study early on, graduated from Stanford University, and worked at Silicon Valley tech companies and Wall Street institutions. He was familiar with overseas financial markets, media operations, and business strategies. A steadfast believer in Bitcoin, he was also among the first to introduce Bitcoin to the Chinese business community.

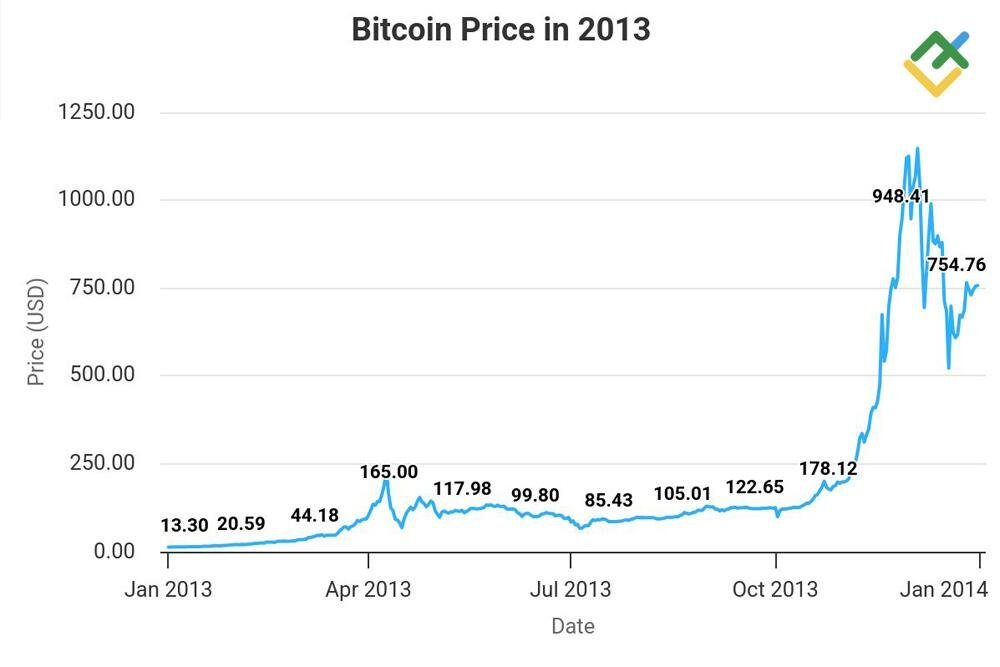

In 2013, Bitcoin's price skyrocketed from $13 at the start of the year to $1,100 by year-end. The first global bull run swept in, and Chinese market demand exploded. BTCC's grassroots model could no longer handle the influx of users. Bobby Lee immediately saw BTCC's first-mover advantage, decisively joined to lead operations, and with three bold moves, turned this small geek site into an industry benchmark.

He first ended the residential workshop model, registered a proper company, and built a complete team for technology, operations, and customer service. He also connected with domestic and international financial media, pushing Bitcoin and BTCC into the public eye, striving to make ordinary people aware of Bitcoin and Bitcoin trading. Simultaneously, he optimized the deposit and withdrawal processes, improved system stability, and initially established security mechanisms to handle this explosive user growth.

In 2013, BTCC reached its peak. Daily trading volume broke through billions of yuan, and user numbers surged, making it the most influential exchange in China and globally. The first-generation iron triangle of Yang Linke, Huang Xiaoyu, and Bobby Lee firmly held their position as China's exchange pioneers.

That period was the absolute primitive era for Chinese crypto exchanges. No regulatory policies, no industry standards, no risk control requirements. There were no formal payment channels, no custodian services for funds—user assets were all held in the founders' personal accounts.

This primitive era accomplished the industry's most crucial initial accumulation:

BTCC proved that the early business model of matching yuan and Bitcoin was viable. It spread users from the geek circle to ordinary investors, providing the most tangible entrepreneurial blueprint for those who followed.

Of course, the primitive revelry eventually heard its first warning bell.

In December 2013, the People's Bank of China and four other ministries jointly issued the "Notice on Preventing Bitcoin Risks." For the first time, it clearly defined that Bitcoin was not a currency but a virtual commodity. It drew a red line, prohibiting financial institutions and payment entities from participating in related businesses, and directly pointed out the fatal risks of exchanges: unregistered, insecure, prone to attacks, and the possibility of operators absconding with funds.

Although this notice did not shut down exchanges, it placed the first restraint on the wildly growing industry.

Yang Linke knew clearly after reading the notice that the days of grassroots workshops and gray areas were numbered. Little did he know that a battle among giants that would upend the industry was already on the horizon.

In the winter of 2013, BTCC moved out of the apartment into a proper office building. As the logo lit up, the three pioneers stood by the window, their eyes full of hope.

They had transformed from an internet cafe manager, a tech geek, and an overseas elite into the first generation of founders of Chinese exchanges, completing the journey from 0 to 1 in the most straightforward way. But they hadn't anticipated that two more aggressive entrepreneurs would soon break their established mold and propel Chinese exchanges to the pinnacle of the world.

Li Lin and Xu Xingming were already sharpening their skills nearby.

02 The Rise of the Three Giants and Chinese Power Dominating the World

Also in 2013, deep into the night at a startup café in Beijing's Zhongguancun, the lights were still blazing.

Li Lin stared intently at the Bitcoin candlestick chart on his computer. Just emerging from the failure of a group-buying venture, he sensed an unprecedented opportunity.

Meanwhile, a few streets away, Xu Xingming's fingers were flying across the keyboard. This tech geek, proficient in high-concurrency trading systems, was building his own trading engine.

Two young men with completely different backgrounds, mindsets, and strategies targeted the Bitcoin trading track in the same year. Instead of copying BTCC's grassroots pioneering path, they used mature internet industry playbooks to forcibly break the first-generation pattern established by Yang Linke and Bobby Lee, pushing Chinese crypto exchanges from a niche geek circle to the throne of global dominance.

Li Lin was from Shaoyang, Hunan. Born in 1986, he was a seasoned internet product veteran. A computer prodigy during his school years, he joined major companies like Renren and Oracle after graduation, mastering product design and user operations. In 2010, he seized the group-buying trend, founding a platform that briefly ranked among China's top ten, but ultimately fell in the fierce "thousand-group-buying wars."

This failure gave him a crucial insight: small entrepreneurs could only break through by focusing on vertical tracks, addressing pain points, and adopting asset-light operations.

In 2013, as Bitcoin surged from $13 to $1,000, domestic trading demand exploded. Li Lin immediately tried BTCC and was frustrated by its poor experience: page stuttering, complicated deposits, and unreachable customer service. User needs were severely neglected. He instantly grasped the industry's key vulnerability: China doesn't lack people wanting to trade crypto; it lacks a good, fast, and reliable trading platform.

At that time, BTCC relied on its first-mover advantage but still retained the rough edges of a geek site. In September 2013, Li Lin announced the launch of Huobi Exchange. Leveraging the motto "Easy to Use, Free, Fast," it reached a trading volume of hundreds of millions within three months, challenging BTC China's first-mover advantage.

Li Lin's strategy for breaking through was user experience: instant deposits and withdrawals, 24/7 customer service, and a smooth interface. He then played the trump card of permanent free trading, directly undercutting the fee-based model of the first-generation platforms.

Just as Li Lin was aggressively capturing the market with superior user experience, Xu Xingming, who also wanted to profit in this track, took a completely opposite path.

Born in 1985 in Suzhou, Jiangsu, Xu Xingming was a tech geek. A graduate of Beijing University of Posts and Telecommunications, he mastered distributed systems and high-concurrency architectures during college. After graduation, he worked at Yahoo China, participating in the development of world-class trading systems, and later became the Technical Director at Docin.com, gaining deep understanding of platform stability for millions of users.

When he encountered Bitcoin, he didn't focus on retail user experience at all. His eyes were set on the core barrier of the trading system. At that time, the matching engines of all domestic platforms couldn't handle massive trading and high-frequency quant trading. Institutional users had no place to land. Xu Xingming's goal was to build China's most stable, fastest exchange tailored for institutions.

In October 2013, OKCoin officially launched, positioning itself with the labels "Top-Tier Technology, Professional Trading," creating a rivalry with Huobi.

He personally led the team in writing the matching code, creating a system capable of millisecond transactions and tens of thousands of concurrent orders, directly crushing BTCC's outdated architecture. He focused on quant and high-frequency trading, firmly attracting professional investors and institutional teams, forming a stark contrast with Li Lin's retail-focused approach.

One understood users and targeted retail; the other understood technology and served institutions.

Li Lin and Xu Xingming, in the same year on the same track, forged complementary yet competing paths to the top.

By the end of 2013, both Huobi and OKCoin had risen, completely shattering BTCC's sole dominance. The tripartite structure of the Chinese exchange industry was formally established.

At that time, BTCC held onto its status as the first mover, leveraging overseas resources and its long-standing reputation to retain loyal users. Huobi became the platform with the largest user base due to its excellent user experience and aggressive operations. OKCoin, with its top-tier technology, monopolized the institutional and quant markets.

Instead of maliciously fighting, the three giants grew the overall market together. With the opening of yuan on-ramps and the standardization of trading processes, it became easier for more people to enter the crypto space. Exchanges transformed from a niche business into one of the most profitable entrepreneurial tracks of the time.

The global influence of Chinese exchanges was just emerging. Then, a sudden global black swan event allowed them to take over the world.

In February 2014, a thunderbolt struck the global crypto industry. Mt. Gox, the Japanese exchange that once handled over 70% of global Bitcoin trading volume, was hacked due to an attack and internal mismanagement, losing 850,000 Bitcoins and filing for bankruptcy.

The global cryptocurrency trading system collapsed instantly. Users panicked and fled, liquidity dried up, prices plummeted, and exchanges in Europe and the US suffered total defeat, creating a massive vacuum in the market.

China's three major platforms seized this historic opportunity: their yuan trading system was mature, their user base was large, and liquidity was abundant. Huobi and OKCoin's systems were capable of handling the overflow of global traffic, while BTCC used its overseas resources to connect with international users.

Within just three months, the center of global Bitcoin trading shifted from Tokyo to Beijing and Shanghai.

From 2014 to 2016, the three platforms—BTCC, Huobi, and OKCoin—consistently held over 80% of global Bitcoin trading volume, at their peak exceeding 90%. The yuan became the primary pricing currency for Bitcoin. China's trading times, policy directions, and user sentiment directly influenced the global Bitcoin price.

Huobi's customer service in Beijing was still processing orders in the early hours, BTCC's matching engine was running at high speed late at night in Shanghai, quant teams in Shenzhen were executing high-frequency trades on OKCoin's order book. China had become the absolute center of the global cryptocurrency world.

These were the three most glorious years for Chinese exchanges. No heavy regulation, no vicious internal competition, no catastrophic defaults. The three giants jointly ruled the world, profiting enormously. Li Lin, Xu Xingming, and Bobby Lee stood at the pinnacle of the industry, becoming globally recognized Chinese faces in the crypto community.

While the giants reigned, smaller platforms also sprang up like mushrooms, entering a period of prosperous competition. BTC China captured the lower market with low fees, Bitcoin Trading Net focused on spot trading, and BitCNY pioneered the listing of niche altcoins. By 2016, the number of formal domestic exchanges exceeded 30, spreading from first-tier cities to small towns, and the Bitcoin trading community was taking shape.

This phase involved only pure spot trading. Everyone believed the golden age would last forever.

But beneath the surface of prosperity, undercurrents were already stirring.

Competition among the three giants for users was intensifying, and simple spot trading could no longer satisfy their expansion ambitions. Smaller platforms were eyeing futures, leverage, and altcoins to find new profit points. Regulatory attention was also shifting from "defining virtual commodities" to the rapidly expanding financial risks.

In 2016, the price of