SpaceX races toward the "biggest IPO in history": Commercial aerospace has one foot in the era of public market pricing

- Key Takeaway: The article argues that SpaceX's IPO will shift commercial aerospace from concept speculation to value reassessment. The core lies in identifying companies with truly sustainable business models, rather than chasing short-term sentiment.

- Key Elements:

- SpaceX is expected to go public on June 12 (ticker SPCX) with a target valuation of $1.75 trillion, making it the world's largest IPO. Its public market pricing will provide a valuation anchor for the commercial aerospace sector.

- The long-term value of commercial aerospace stems from technologies like reusable rockets, which have lowered the cost of accessing space, unlocking the potential of new business models such as satellite internet and remote sensing data.

- SpaceX's business structure comprises three layers: Launch & Space Systems (engineering & technology moat), Starlink Satellite Internet (subscription revenue model), and AI & Computing Power Business (long-term imagination coexisting with current losses).

- The commercial aerospace sector should be viewed in layers. Platform companies (like Rocket Lab) are closest to SpaceX's full-stack capability logic, while satellite networks (e.g., AST SpaceMobile) and space data services (e.g., Planet Labs) each have their own focus.

- Represented by Rocket Lab (RKLB), the company is transitioning into a "space infrastructure platform" through the first flight of its medium-lift reusable rocket, Neutron, and defense contracts (e.g., the $816 million SDA project).

- SpaceX's price-to-sales ratio of over 100x means high valuation is a core risk; if growth falls short of expectations, valuation corrections could be severe. Ultimately, its IPO will distinguish between core assets, comparable assets, and sentiment-driven assets.

Original Author: Mike, Frank, MSX Maitong

If everything proceeds according to plan, SpaceX will be listed on Nasdaq on June 12 under the ticker SPCX.

Barring any surprises, this will become the largest IPO in the history of global capital markets——According to the currently disclosed issuance plan, SpaceX plans to raise approximately $75 billion, with a target valuation of around $1.75 trillion, surpassing not only the fundraising scale of Saudi Aramco's IPO but also positioning it among the most valuable publicly listed companies globally from day one.

However, for the market, SpaceX's significance extends far beyond "just another star tech stock listing."

More importantly, the commercial spaceflight sector, a trajectory long caught between immense imagination and high entry barriers, finally has a true public market pricing anchor. In the past few years, investors knew the space economy was attractive and recognized the long-term potential in satellite internet, commercial launches, remote sensing data, and defense aerospace, but they struggled to determine the actual value of these assets.

Once SpaceX trades at a public market price, all publicly listed commercial space companies will be placed on the same valuation table for reassessment. The market will re-differentiate who is closer to SpaceX's capability frontier, who holds real orders and revenue, and who is merely riding the thematic wave.

Therefore, re-understanding the commercial space sector around the time of SpaceX's listing isn't about chasing short-term sentiment; it's about answering three questions: First, why is commercial space worth long-term attention? Second, which companies within the sector truly possess sustainable business models? Third, after SpaceX goes public, will it syphon funds away from the sector or lift the entire segment?

1. Commercial Space: From Government Project to Commercial Asset

To understand why commercial space deserves long-term focus, one must grasp the historic transformation this industry is undergoing.

For decades, accessing space was essentially an extension of national power. The US had NASA, the USSR had its space program, later succeeded by Roscosmos. Rocket development, satellite launches, and space exploration were fundamentally large-scale government-led projects. While commercial capital participated, it could hardly become the dominant force.

The reasons are simple: costs were too high, cycles were too long, and failure rates were too significant. Traditional satellite launches cost hundreds of millions of dollars, project development took years, and commercial return cycles could span decades. For most enterprises, this wasn't a track suited for standard business models but rather a component of national strategic investment.

Because of this, SpaceX's key to changing the industry wasn't just getting a rocket into space; it was reshaping the cost curve of reaching orbit.

Reusable rockets are the core of this change. The first stage of the Falcon 9 can autonomously return and land after launch, undergo refurbishment, and be used again. This technology transforms launches from a disposable consumable into infrastructure whose cost can be amortized repeatedly. Launch costs, once hundreds of millions of dollars per event, have been compressed to tens of millions. With the maturation of next-generation systems like Starship, costs are expected to continue declining.

Once the cost curve breaks downwards, previously unviable business models begin to make sense.

Satellite internet is the most direct example. The economic viability of launching thousands of satellites into low Earth orbit (LEO) was once almost unimaginable. But after reusable rockets lowered costs, Starlink transitioned from a grand vision into a subscription-based network charging global users.

Remote sensing data services follow the same logic. Commercial satellites imaging the Earth, tracking crops, monitoring ports, serving defense and insurance industries were previously limited by high satellite manufacturing and launch costs, hindering large-scale commercialization. However, as deployment costs fall and data processing capabilities improve, space-based data has the potential to evolve from "high-end custom services" into "continuous subscription data products."

Looking further ahead, areas like in-space manufacturing, on-orbit servicing, lunar missions, and space-based AI data centers are still in early exploration. But the underlying logic remains consistent: only as the marginal cost of accessing space continuously declines will new demand be unlocked.

Historical parallels are common. The breakthrough in shale gas technology lowered extraction costs, reshaping the US energy landscape; smartphones lowered the barrier to mobile computing, triggering the mobile internet explosion; cloud computing shifted IT infrastructure from a one-time capital expenditure to pay-as-you-go, enabling SaaS to become a major industry.

Commercial space is traversing a similar path. It's not linear growth in an existing market but the re-opening of new markets following a breakthrough in the cost curve.

This is why the global space economy is transitioning from a niche tech narrative to a long-term industrial narrative. Multiple institutions estimate that the global space economy is expected to grow from approximately $630 billion in 2023 to around $1.8 trillion by 2035, with the real growth driver being the commercialization inflection point spurred by falling launch costs, satellite manufacturing, data processing, and defense demand.

2. Understanding SpaceX Through Its Prospectus: What Is It Doing Now?

The reason SpaceX commands such high market attention is that it is no longer merely a rocket company.

Based on currently disclosed information, SpaceX's business structure can broadly be broken down into three layers: Launch & Space Infrastructure, Starlink Satellite Internet, and the AI & Computing business formed after incorporating xAI.

The first layer is Launch Services and Space Systems.

This is SpaceX's foundational capability and the bedrock of all other businesses. The Falcon 9, Falcon Heavy, Starship, and the launch system built around NASA, the US Department of Defense, and commercial clients form SpaceX's engineering moat. Reusable rockets not only provide lower costs but also enable higher mission frequency.

In the aerospace industry, high frequency itself is a moat. More launches mean more data, faster engineering iteration cycles, and more mature cost control. This virtuous cycle is difficult for traditional aerospace companies to replicate quickly.

The second layer is Starlink.

If the rocket business proves SpaceX's engineering prowess, Starlink demonstrates its commercial capability. A LEO satellite internet constellation is fundamentally a global communications network. The wider its coverage, the more users it has, and the more mature its user terminals, the greater the potential to continuously amortize marginal costs.

This is also the biggest difference between SpaceX and most other commercial space companies: it sells not just one-off projects but also generates recurring subscription revenue. Starlink caters to individuals, enterprises, aviation, maritime, government, and defense sectors, transforming a capital-intensive space project into a revenue model closer to a telecom operator and internet infrastructure provider. For capital markets, this layer is also the most easily understood and modeled part of SpaceX's valuation.

The third layer is the AI & Computing business.

This is the most imaginative, yet also the most controversial, part of SpaceX's current valuation. With the incorporation of xAI, the company's narrative has extended from "rockets + satellite internet" to "space infrastructure + AI infrastructure." Whether through massive ground-based computing clusters or more futuristic orbital AI data centers, SpaceX is positioning itself within the infrastructure competition of the AI era.

However, this layer also introduces new uncertainties. According to disclosed data, Starlink has demonstrated strong profitability, but the overall SpaceX group is still burdened by high capital expenditures and losses from the AI business. In other words, SpaceX isn't a pure "already stably profitable" company, but one that, having proven commercialization in its core business, continues to channel cash flow and market expectations into the next grand narrative.

This is also why its valuation is so complex.

It possesses the certainty of NASA and defense contracts, the growth potential of Starlink's subscription revenue, and the long-term imagination of AI, Starship, Mars missions, and space data centers. It's not a traditional aerospace stock, nor a pure internet stock, but a composite giant built on engineering capability, communications networks, government orders, and AI infrastructure.

This is precisely why the market is willing to give it a trillion-dollar valuation, and also the reason why investors must remain cautious.

3. Within the Sector: Syphoning or Lifting?

Having understood the long-term logic of commercial space, the real questions begin: Which companies within the commercial space sector deserve long-term attention?

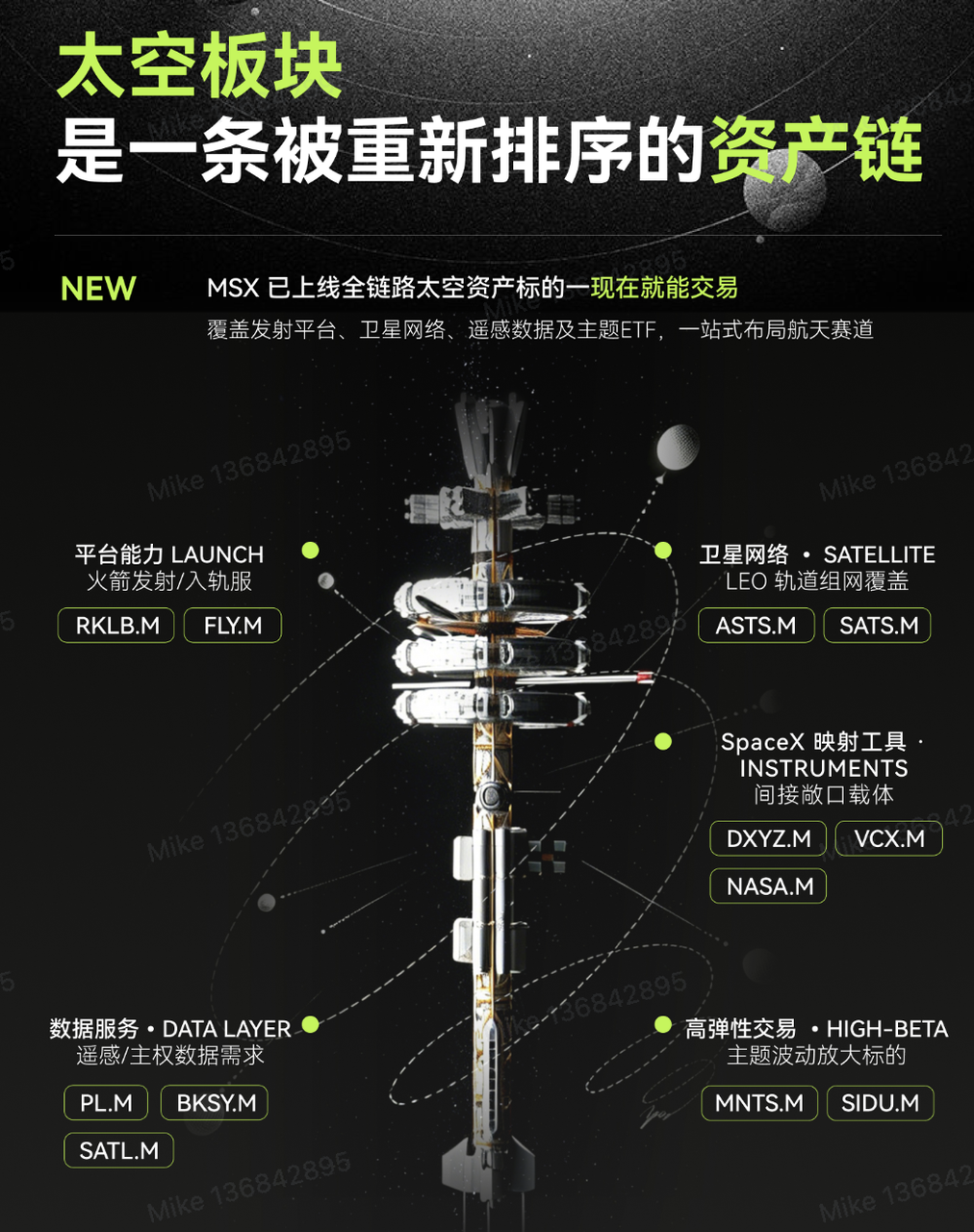

A fundamental judgment needs to be established first: Commercial space is not a homogeneous sector. Internally, it includes platform companies similar to SpaceX's logic, satellite network companies, data service firms, high-beta small-cap companies, and ETFs or closed-end funds offering indirect exposure. Therefore, the valuation logic and risk-reward profiles for different assets are entirely distinct.

Failing to stratify and simply grouping everything under the label "space stocks" makes it easy to buy the weakest comparable assets during peak market sentiment. A more reasonable approach is to break down commercial space into five layers:

Layer 1: Platform Space Infrastructure

This layer most closely mirrors SpaceX's logic in the public market. What makes SpaceX scarce isn't just its rockets, but its full-stack capability spanning launch, satellites, ground stations, communication networks, government contracts, and long-term AI infrastructure. Among publicly listed companies, the closest equivalents are RKLB.M (Rocket Lab) and FLY.M (Firefly Aerospace).

Rocket Lab is the most typical platform candidate among currently listed space companies. It has the Electron small launch vehicle business, a satellite and space systems business, and is extending into medium-lift reusable rockets with Neutron. In 2025, Rocket Lab achieved full-year revenue of $602 million and ended the year with a backlog of $1.85 billion, placing its revenue visibility in a relatively leading position among listed commercial space companies.

On the surface, Rocket Lab's current valuation isn't cheap. However, the market's willingness to pay a premium essentially prices an identity transition: it's no longer just a "small rocket company" but is transforming into a space infrastructure platform driven by the three engines of "launch + satellites + defense orders."

The biggest catalyst for 2026 is the maiden flight of the medium-lift reusable rocket, Neutron. Management's latest guidance points to Q4. If Neutron's first flight is successful, Rocket Lab will, for the first time, possess medium-lift capacity comparable to the Falcon 9 in certain mission scenarios, moving from the small payload market into a larger primary track. Concurrently, Rocket Lab's defense profile is strengthening. The company secured the SDA Tranche 3 project, involving 18 satellites worth approximately $816 million, which is gradually transitioning from orders into revenue.

Combined with M&A integrations in areas like laser communications, space robotics, and satellite components, Rocket Lab's story is no longer just "can they launch?" but "can they become the second space infrastructure platform in the public markets?"

Firefly resembles the second tier in its platform capability ascendancy. The company went public in August 2025 at an IPO price of $45, raising approximately $868 million. Its business covers launch, lunar missions, and defense directions. It already has clients like NASA and Lockheed Martin. However, it is still in a high-growth, unprofitable, high-volatility phase.

The advantage of such companies is high beta. The obvious disadvantage is that mission failures, order delays, or a decline in market risk appetite can lead to more severe valuation compression than for mature platforms.

Therefore, Rocket Lab is better suited as a core sample of the commercial space platform logic, while Firefly is more of a high-growth beta sample.

Layer 2: Satellite Networks & Connectivity Services

The second layer focuses on coverage, access, and long-term service revenue.

The most representative company in this layer is ASTS.M (AST SpaceMobile). Its core is not satellite manufacturing but building a satellite communication network accessible by standard smartphones – often referred to as "direct-to-cell."

If this model succeeds, ASTS's potential is enormous. It targets uses like filling gaps in global mobile coverage, connecting remote areas, disaster communications, and defense communications. Theoretically, it can partner with existing mobile operators rather than fully replacing them. However, ASTS's challenges are clear: commercial validation is still ongoing. Satellite deployment pace, cash burn rate, spectrum coordination, and operator partnership progress will all affect the speed of valuation realization.

SATS.M (EchoStar) is more of a mature satellite operations platform. Its growth prospects are lower than ASTS, but its assets and business are more established, making its volatility relatively more manageable. For investors, this type of asset is better suited as a stable observation sample in the satellite communications infrastructure direction, rather than purely chasing high beta.

Layer 3: Space Data Services

The third layer is where the space economy can most easily transition from "concept stock" to "operating asset."

The representative company is PL.M (Planet Labs). Its logic is straightforward: selling continuously updated Earth observation data. Agriculture, insurance, energy, ports, defense, and government management are all potential use cases for its data.

In fiscal year 2026, Planet Labs reported revenue of approximately $308 million, a year-end backlog of $900 million, and achieved its first positive Adjusted EBITDA. This is significant because it indicates the company is moving from "burning cash on stories" towards "business self-sustenance."

In comparison, BKSY.M (BlackSky) leans more toward spatial intelligence and defense subscriptions. Its key differentiators are high-frequency remote sensing, AI analytics, international clients, and government contracts. Its business model is closer to a "spatial intelligence service provider," with defense and sovereign demand being important pillars.

SATL.M (Satellogic) is smaller, offering higher beta but weaker certainty, making it better suited as a high-beta supplementary sample rather than a core sector asset.

Layer 4: High-Beta Small Caps

Companies like MNTS.M (Momentus) and SIDU.M (Sidus Space) fall into the fourth layer.

Their common characteristics are small market capitalization, early-stage monetization, high volatility, and pricing heavily dependent on events, themes, and technological validation. When a theme heats up, these stocks often move first because only small trading volumes are needed to move the price. However, once the market shifts back from sentiment to comparative valuation, they are also most susceptible to re-evaluation.

Layer 5: SpaceX Proxy Instruments

Before SpaceX officially lists, the market has created another set of choices: gaining indirect exposure to SpaceX via ETFs, closed-end funds, or pre-IPO instruments.

For example, instruments like DXYZ.M, VCX.M, and NASA.M have, to varying degrees, captured the scarcity premium before SpaceX's listing.

DXYZ's core logic is "anticipated SpaceX trading + scarce private tech assets." It provides public market investors a channel to indirectly trade in a private giant.

VCX is more like a basket of unlisted tech assets, containing not only SpaceX but also other AI and pre-IPO tech companies. Therefore, its pricing logic is more closely tied to the overall risk appetite for unlisted tech assets.

NASA.M functions more like a combination of a space-themed ETF and a SpaceX exposure tool. Listed in late March 2026, it quickly attracted capital on the back of the SpaceX IPO anticipation, becoming one of the most closely watched space-themed instruments in the market.

However, these instruments face a very real problem: once SpaceX itself is listed, the scarcity premium for these substitutes diminishes.

When SpaceX couldn't be bought directly, the market was willing to pay a premium for alternative exposure. But when SPCX becomes directly tradable, some capital may flow from these proxy instruments to the original asset. This doesn't mean these instruments will necessarily lose all value, but their pricing logic will change: from being the "only entry point" to being a "portfolio allocation" choice.

This is also a key reason why the space sector may see divergence after the SpaceX IPO.

Finally, it's worth noting that, as the core holdings of MSX Q2 Top Picks, RKLB.M, YSS.M, BKSY.M, and PL.M all recorded positive returns, with an average gain exceeding 100%.

Final Thoughts

Of course, the commercial space sector merits long-term attention, but that doesn't mean any price is worth chasing.

SpaceX's current target valuation is around $1.75 trillion, implying a price-to-sales ratio (based on 2025 revenue) close to 100 times. This valuation suggests the market has already priced in years of future growth, including Starlink's expansion, Starship's maturation, the AI computing business's explosive growth, and the long-term commercialization of space infrastructure.

If post-IPO revenue growth falls short of expectations, Starlink user growth slows, or AI business capital expenditures continue to rise, the valuation correction could be very severe.

High valuation itself is one of SpaceX's biggest risks.

However, the true significance of the SpaceX IPO lies in forcing the market to clearly distinguish between core assets, comparable assets, and mere sentiment-driven assets.

For investors, what is most worth watching in commercial space over the long term is not the word "space" itself, but rather which companies can transform imagination into orders, orders into revenue, and revenue into cash flow once the cost curve declines.

Going forward, the true dividing line in the commercial space sector will no longer be the scale of the story told, but how a company proves its foundation for survival.

The answer will be revealed soon.