SemiAnalysis vs. the "White-Hair Stock God": What Real Insights Lie Beneath the CPO Report Sell-Off?

- Core Thesis: The market has diverged on the timeline for CPO (Co-Packaged Optics) volume production, leading to a pullback in optical stocks. SemiAnalysis suggests that mass production scale-up could be delayed to 2028-2029, while analyst Serenity counters that Nvidia's supply chain execution could accelerate this process. The core of the debate lies in the *slope* of CPO commercialization, not the *direction*.

- Key Elements:

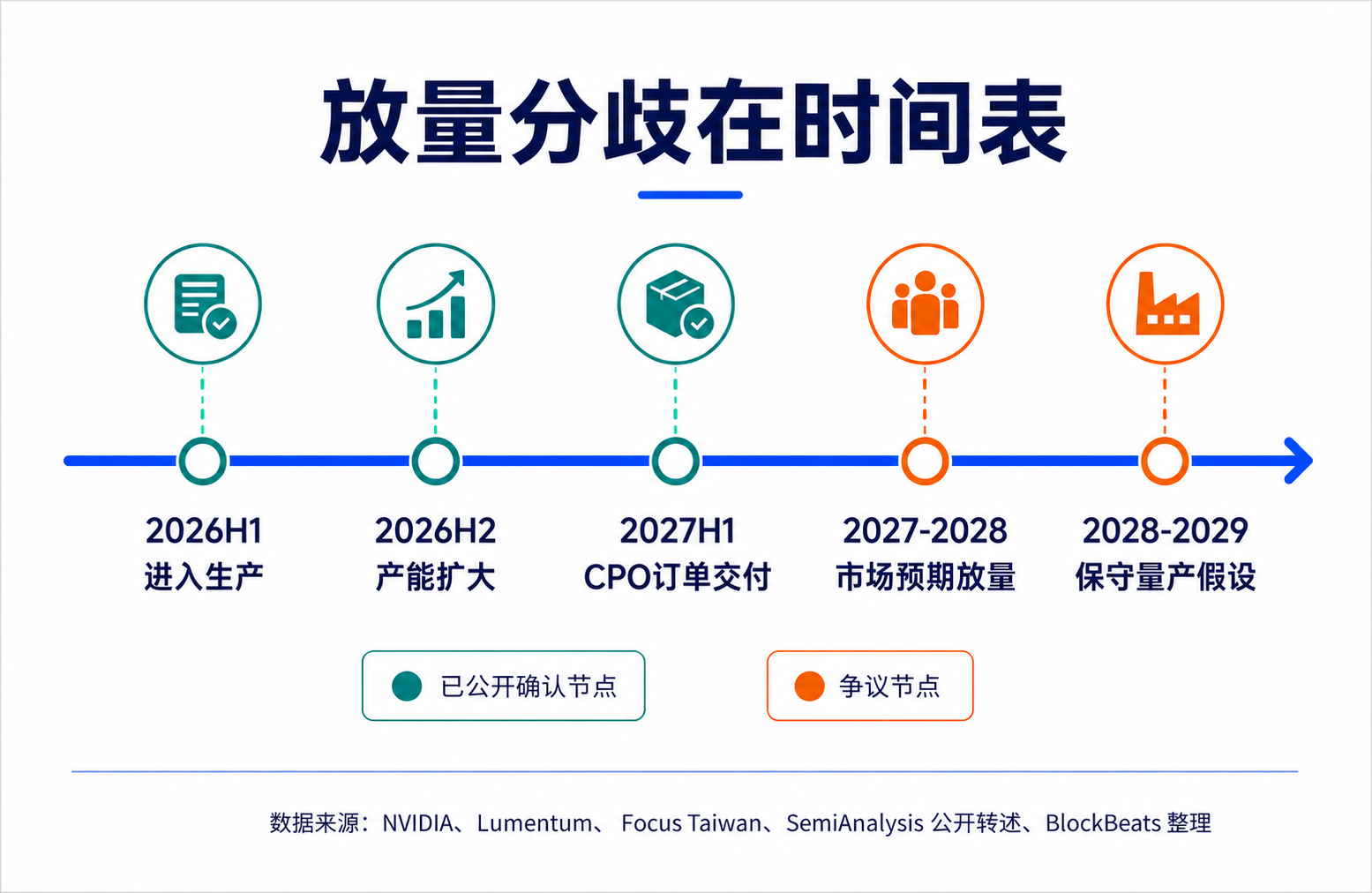

- A June report from SemiAnalysis triggered market volatility. Its core judgment is that mass production of CPO may be delayed to 2028-2029, while NPO (Near-Packaged Optics) projects could accelerate. This led to high-single-digit to double-digit corrections in optical stocks like AAOI and LITE.

- Serenity refutes SemiAnalysis's conservative model, arguing it underestimates Nvidia's ability to compress hardware cycles. Citing signals such as Lumentum's hundreds of millions of dollars in incremental CPO orders and Spectrum-X entering production, Serenity maintains that CPO is still on its ramp-up trajectory from the second half of 2026 to 2028.

- CPO's theoretical advantage lies in solving the bandwidth, power consumption, and signal integrity bottlenecks by placing the optical engine closer to the ASIC. However, its system engineering challenges (e.g., repairability, yield, reliability) may cause its large-scale deployment to lag behind market expectations.

- NPO, positioned between CPO and traditional pluggable modules, becomes a key point of contention: If CPO is delayed, NPO will enjoy a longer market window; if CPO accelerates, NPO could also coexist with CPO at different network layers, reshaping the value distribution between technology routes.

- The market had previously been overly trading on the "CPO endgame" narrative. The disagreement between SemiAnalysis and Serenity essentially shifts the valuation anchor from *direction* to *timeline verification*. The key going forward will be production-level data from the second half of 2026 to 2028, particularly shipment metrics (small-batch vs. large-scale) and field reliability data.

TL;DR

- SemiAnalysis believes that the volume ramp for CPO will be slower than the market expects, and the transition window for NPO may be extended.

- The "White-Haired Stock God" (a well-known analyst) disagrees with this assessment, arguing that NVIDIA and the supply chain are pushing CPO forward faster.

- Related tickers: AAOI, LITE, COHR, GLW, MRVL, SIVE, AVGO, NVDA

The recent downturn in optical stocks, on the surface fueled by a cold shower on the CPO narrative, is fundamentally about the market repricing a more sensitive issue: will the volume ramp in 2027-2028 be a period of earnings realization, or just another phase of introduction and validation?

CPO (Co-Packaged Optics) itself hasn't been negated. The pressure on bandwidth, power consumption, and switching density in AI data centers is still increasing, and the physical limits of copper cables and traditional pluggable optical modules haven't disappeared. The problem is that the previous rally in related stocks already implied an aggressive timeline: after NVIDIA pushed CPO into the commercialization window, components like optical engines, lasers, silicon photonics, and switch chips would quickly enter volume shipment in 2027-2028.

SemiAnalysis's June 9 report precisely targeted this pricing assumption. According to public summaries, the report suggests that the mass production of NVIDIA's 800V DC and CPO might be delayed to around 2028-2029, while 400V DC is still on track for a 2026 ramp-up, with some NPO (Near-Package Optics) projects potentially accelerating. Market volatility ensued, with tickers like AAOI, LITE, COHR, GLW, and MRVL experiencing high single-digit to double-digit pullbacks. The market is trading not on "whether the CPO direction is valid," but on "how quickly CPO can turn into orders."

However, this isn't a one-sided bearish view. "White-Haired Stock God" and AI supply chain analyst Serenity (@aleabitoreddit) subsequently pushed back against SemiAnalysis, arguing that they rely too heavily on conservative engineering models and underestimate NVIDIA's ability to compress hardware cycles. Based on their interpretation of signals from NVIDIA, Lumentum, Foxconn, etc., they emphasize that CPO remains on track for ramps in the second half of 2026, second half of 2027, and 2028.

The value of this debate isn't about declaring a "winner," but about shifting the valuation anchor for the optical supply chain from an end-state narrative to timeline validation: CPO will arrive, but the slope of its ramp determines the value distribution among NPO, pluggable modules, light sources, and switch chips.

Timeline Repricing Behind the Optical Stock Decline

Over the past few months, when the market bought into the optical supply chain, it wasn't buying current revenue; it was buying into the capital expenditure migration towards next-generation network architectures for AI data centers.

As model training and inference clusters scale up, communication pressure between GPUs, racks, and within data centers continues to rise. The network is no longer just a supporting system outside the server; it increasingly becomes the efficiency bottleneck of the AI factory. Higher bandwidth density and lower power consumption raise the ceiling for scaling individual compute clusters, which is why CPO has taken the spotlight.

The theoretical appeal of CPO is straightforward: bring the optical engine as close as possible to the ASIC (dedicated switch chip) to shorten the high-speed electrical signal path, reducing power consumption, loss, and signal integrity issues caused by serial-deserializer circuits and copper traces. Compared to traditional pluggable modules, CPO offers better power efficiency and density potential in the high-bandwidth era.

The market's problem is that it can easily pre-trade "correct direction" as "confirmed volume ramp." NVIDIA's official press release stated that the Vera Rubin platform will introduce Spectrum-X Ethernet Photonics, with CPO switches entering production for scaling AI factories across clusters. A June 3 report noted that an NVIDIA networking executive indicated Spectrum-X CPO switches have begun shipping to select partners, with production capacity expected to expand in the second half of 2026.

These signals prove CPO is advancing, but they don't directly equate to risk-free mass production orders. For capital markets, there's a huge valuation difference between "entering production," "shipping to select partners," "customer evaluation," and "mass production." The pullback triggered by the SemiAnalysis report is essentially the market starting to differentiate between these terms.

SemiAnalysis's Conservative Model: CPO's Challenge is System Engineering

SemiAnalysis isn't saying CPO has no future. Its core judgment is more like: CPO's theoretical advantages are clear, but scaled deployment will be slower than the market imagines.

The reason isn't just that one or two components aren't ready; it's that CPO centralizes the complexity previously distributed across modules, boards, and whole systems into a more deeply coupled system. Higher integration yields better point performance, but it also increases pressure on manufacturing, testing, repair, and supply chain flexibility.

Traditional pluggable modules benefit from modularity. If an optical module fails, you replace the module; switching suppliers is relatively easy. CPO is different. The optical engine is much closer to the ASIC, even within the same package. The power and density benefits come from this close coupling, but the scope of repair also expands. If an optical component fails, it doesn't just affect an easily swappable module; it can involve the higher-value switch chip and the entire system.

SemiAnalysis's previous "CPO Book" repeatedly emphasized serviceability, reliability, yield, and supply chain maturity, especially in hyperscaler cloud scenarios where performance isn't the only metric. Large customers demand high reliability and maintainability. If failure rates, repair processes, and replacement costs in a production environment are uncontrollable, even the best power model might face deployment delays.

InP lasers are also a point of contention. Laboratory-level port operating life data can prove technical feasibility, but it doesn't necessarily cover long-term operation, mass manufacturing, field maintenance, and supply chain redundancy in large-scale data centers. For investors, this distinction is critical: lab validation proves the direction; field reliability determines the volume ramp.

In SemiAnalysis's framework, NPO and pluggable modules aren't backward paths; they are more realistic intermediary layers before engineering risks are fully resolved. CPO is theoretically superior, but if full deployment takes longer, the market must reprice these "less end-state, but easier to mass-produce and maintain" solutions.

Serenity's Rebuttal: NVIDIA Could Compress Hardware Cycles

Serenity's rebuttal doesn't deny CPO's engineering difficulties. It argues that SemiAnalysis underestimates NVIDIA's organizational capabilities within the AI hardware cycle.

The logic is clear: typical hardware adoption is indeed hampered by yield, reliability, and customer validation, but NVIDIA is not a typical customer. It is the definer of GPU cluster architecture and the core driver of networking, switches, system integration, and supply chain rhythm. When AI factory expansion is bottlenecked by network power and bandwidth, NVIDIA has strong economic incentives and industry leverage to compress traditional adoption cycles.

Serenity's evidence is two-fold. First, publicly verifiable company statements, including NVIDIA's official information on Spectrum-X Photonics entering production, and Lumentum's Q2 FY26 remarks regarding CPO orders and delivery cadence. Lumentum mentioned receiving incremental CPO orders on the order of hundreds of millions of dollars, with delivery in the first half of 2027. Company materials also indicated CPO-related business is expected to ramp more broadly in the second half of 2026.

Second, interpretation of supply chain signals, such as Foxconn's early delivery of optical switches to NVIDIA. However, the specific scale of these signals and whether they are for test prototypes or production orders require more public information for confirmation.

This is the crux of the disagreement between Serenity and SemiAnalysis: SemiAnalysis believes system engineering variables will naturally lengthen the cycle; Serenity believes NVIDIA's supply chain execution will steepen the curve.

These two views aren't entirely conflicting. NVIDIA can push CPO into production and customer validation sooner and might drive adoption in certain scale-out scenarios first. But this doesn't automatically mean all AI data center networks will switch to CPO by 2027. Scale-out, single-rack expansion, intra-rack, inter-rack scenarios, and different customers' tolerance for risk and cost models differ, leading to a potentially layered adoption pace.

Serenity is refuting the overly conservative conclusion that "CPO will be significantly delayed," not proving that "CPO is completely risk-free." For the market, this is enough to support a rebound narrative but doesn't rewrite the aggressive 2027-2028 revenue curve back into certainty.

Why NPO Suddenly Became Important

NPO suddenly became important in this debate because it sits neatly between the logic of SemiAnalysis and Serenity.

It is neither the antithesis of CPO nor a simple continuation of traditional pluggable modules. NPO's basic idea is to place the optical engine on a pluggable base substrate near the ASIC, shortening the electrical signal path for some power and density benefits while retaining better testability, replaceability, and supply chain flexibility.

If SemiAnalysis's conservative model is closer to reality, the deep packaging of CPO will slow down due to yield, repair, and reliability issues, making NPO a more viable choice for a longer period. It allows hyperscalers to gradually gain operational experience with optical interconnects without fully assuming CPO risk, giving existing optical module and engine suppliers a longer window.

If Serenity's assessment of NVIDIA's execution is more accurate, NPO might not disappear. It's more likely that NPO, CPO, pluggable modules, and copper interconnects will coexist at different network hierarchy levels. NVIDIA's own roadmap suggests that CPO can lead in scale-out, while some single-rack expansion scenarios might still rely on copper or hybrid architectures in 2027-2028.

For investors, this means the optical supply chain cannot be priced solely on a "CPO wins, everything else loses" basis. Different technical routes benefit different segments: CPO favors highly integrated optical engines, laser sources, silicon photonics, and the switch chip ecosystem. An extended window for NPO and pluggable modules means existing optical module makers, connector, material, and some light source suppliers can continue to enjoy orders and margin support.

The market's previous problem was translating the technological end-state too early into a revenue ramp for a single route. What is now being reopened is the valuation space for intermediate routes.

Production-Grade Data is the Next Validation Point

This debate won't be settled by one report or a series of posts in the short term. SemiAnalysis reminds the market that CPO's difficulty lies in system engineering. Serenity reminds the market that NVIDIA's supply chain orchestration capabilities could change traditional hardware adoption timelines. The real difference between them requires production-grade data from the second half of 2026 through 2028 to validate.

Moving forward, the most critical thing isn't "whether shipments occur," but the nature of those shipments. Shipping to select partners, customer evaluation, initial production, volume ramp, and large-scale deployment are all distinct stages. NVIDIA's subsequent descriptions of Spectrum-X / Quantum-X Photonics production scaling, and optics suppliers like Lumentum and Coherent's descriptions of orders, capacity, and gross margins in their earnings, will carry more weight than the wording of a single event.

Equally important to watch is field reliability and repair data. If CPO proves sufficiently stable in production environments regarding failure rates, replacement processes, yield curves, and total cost of ownership, SemiAnalysis's conservative model will be adjusted. If this data remains stuck at the lab or small-volume validation stage, the window for NPO and pluggable modules will continue to be upgraded by the market.

The optical supply chain is currently trading not on CPO's life or death, but on the slope of its timeline. The next validation point will fall on whether "entering production" can translate into sustainable volume, and the speed at which this volume is ultimately reflected in orders, gross margins, and customer deployment schedules.

While SemiAnalysis raised concerns about CPO technology over the next two years, they still identified five semiconductor sub-sectors they are bullish on:

Copper / AEC / ACC;

Pluggable Optics / DSP;

CPO Test Equipment;

Power Gray Space / UPS Continuity;

Board-level VRM / Silicon-based Power / Passives.

Specific tickers for these are included in the image below for readers' reference.