Tiger Research: The Rise of Perpetual Contracts in the Tokenized Stock Market of 2026

- Core Thesis: Against the backdrop of a bearish cryptocurrency market diverging from traditional stock market trends, the tokenized stock market—particularly perpetual futures—has grown counter-cyclically. By offering 24/7 trading, leverage, and price discovery functions, it has enabled new strategies such as delta-neutral trading and cross-exchange arbitrage, attracting institutional attention.

- Key Elements:

- Market Divergence: In Q1 2026, the cryptocurrency market cap fell by 20.4%, and spot trading volume dropped by 39.1%. Meanwhile, stock indices like the S&P 500 hit new highs, with capital flowing from cryptocurrencies to the tokenized stock market.

- Advantages of Perpetual Futures: They offer 24/7 trading, leverage of up to 20x, and the ability to trade stocks not available on local exchanges. Their prices serve as a leading indicator for the next day's opening price when the spot market is closed (correlation of 0.85-0.89).

- Delta-Neutral Strategy: When the spot market exhibits a premium (e.g., SK Hynix averaging 0.23% intraday), simultaneously holding a long position in KRX spot and a short position in perpetual contracts allows one to profit from funding rates without directional exposure.

- Cross-Exchange Arbitrage: Different exchanges (e.g., Binance vs. Hyperliquid) may price the same stock perpetual contract differently (e.g., SK Hynix averaging a 1.03% spread). Hedging directional risk by taking opposing positions allows traders to capture the spread.

- Emerging Business Opportunities: Liquidity fragmentation creates opportunities in market making, regional oracles (for Asian timezone asset pricing), tokenized issuance (expanding coverage of large-cap Korean stocks), and basis hedge funds.

This article was written by Tiger Research. Although the cryptocurrency market is in a downturn, the tokenized stock market continues to grow. It is divided into fully collateralized spot futures and perpetual futures, with perpetual futures attracting the most attention and giving rise to a series of new strategies.

Key Takeaways

- While the stock market has repeatedly hit new highs, the market cap and trading volume of cryptocurrencies have both declined. As the two diverge, the tokenized stock market has grown by building up open interest in perpetual futures.

- The market is divided into fully collateralized spot futures and perpetual futures. Perpetual futures are notable because they allow for 24/7 trading of stocks unavailable on domestic exchanges and also enable the use of leverage.

- After regular trading hours end, price movements serve as a leading indicator for the next day's spot opening price, predicting not only the direction but also the magnitude of the price movement.

- Two retail trade strategies exist: a delta-neutral trade that earns a premium from the funding rate via spot trading, and cross-exchange arbitrage exploiting price gaps.

- The same structure also applies to businesses like market making, regional oracles, token issuance, and basis hedge funds. Although the scale is small, opportunities exist in both investment and business as institutional investors join.

1. Stock Markets Are Absorbing Crypto Liquidity

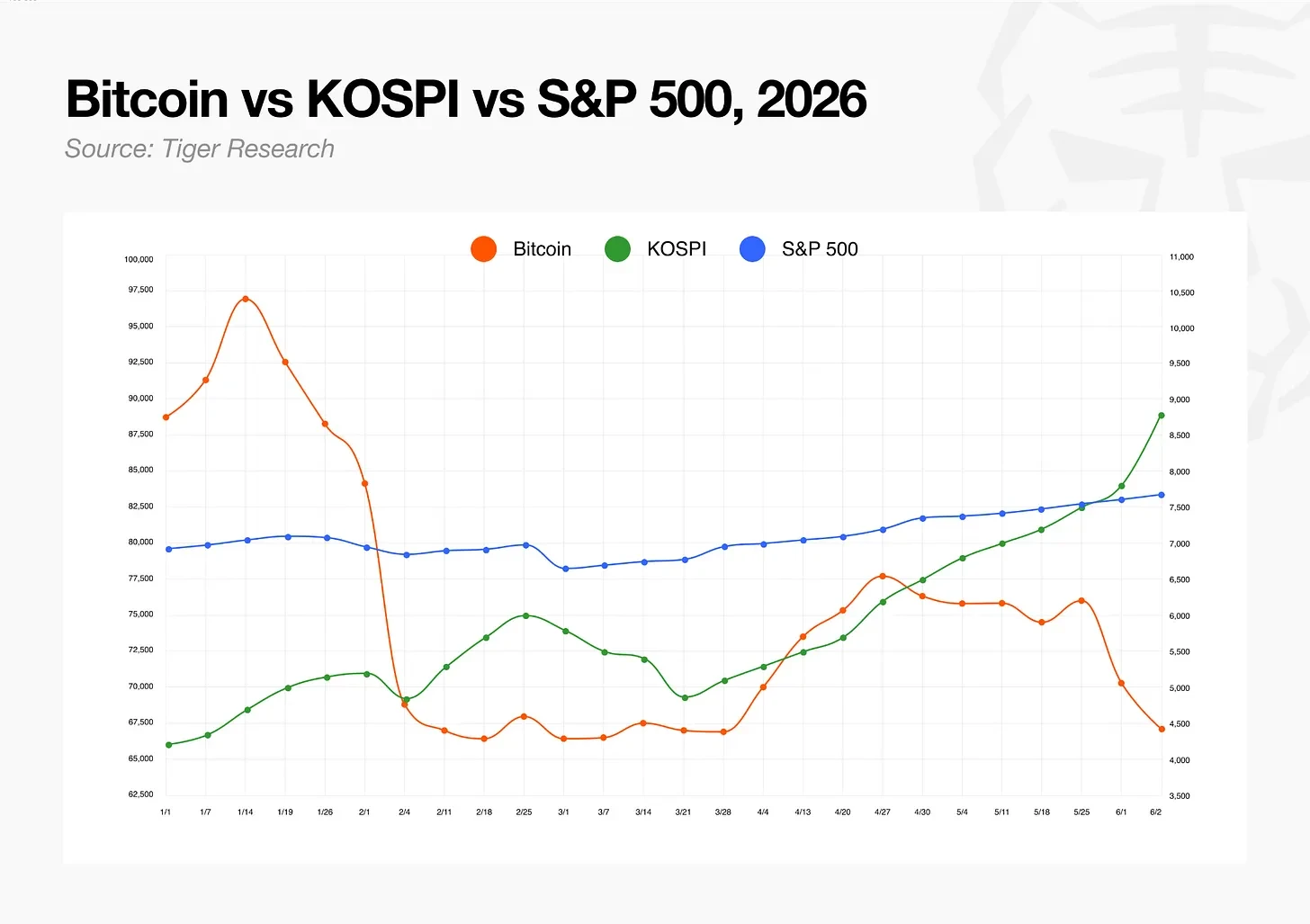

In the first quarter of 2026, the total cryptocurrency market cap fell by 20.4%, and spot trading volume on centralized exchanges dropped by 39.1%. Bitcoin has been declining since hitting its all-time high in October 2025.

The stock market trend was the exact opposite. The S&P 500 easily surpassed its annual target, and the KOSPI (Korea Composite Stock Price Index) doubled this year, benefiting from the semiconductor industry's uptrend. Meanwhile, the total crypto market cap fell sharply, while stock markets in most countries hit record highs. These two paths have never been so clearly divergent.

2. Collateral Divides the Market; Perpetual Futures Flow In

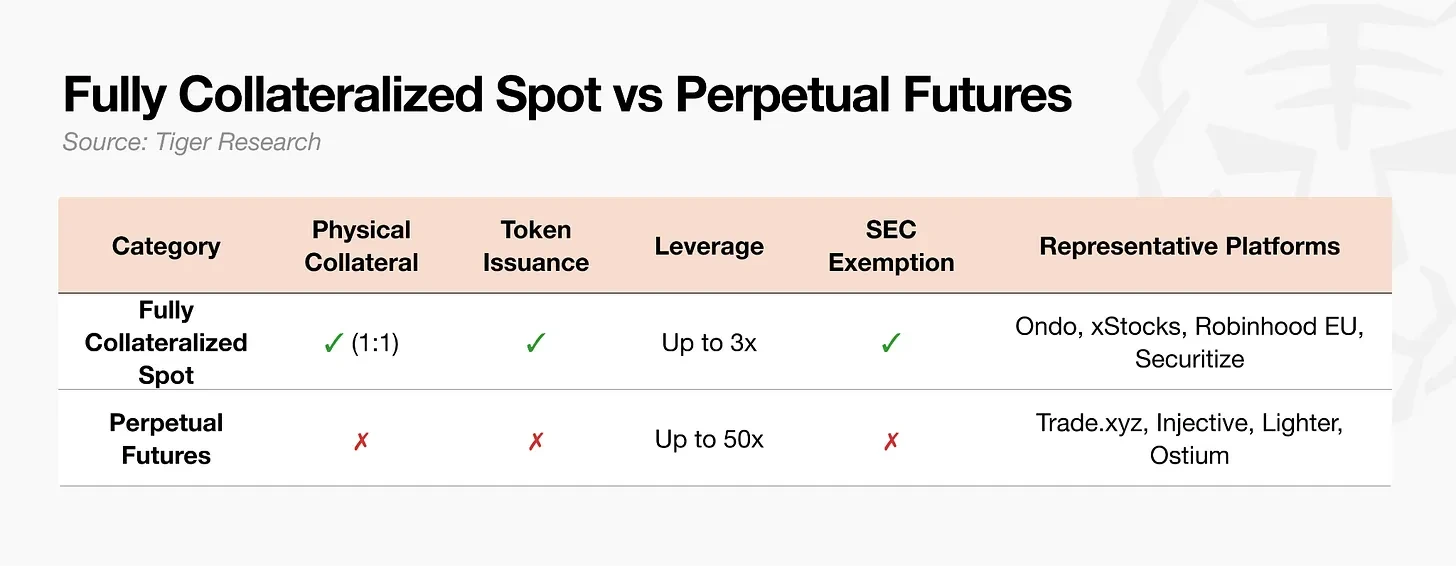

The tokenized stock market is divided into two parts based on collateral structure.

Fully collateralized spot trading deposits real stocks at a 1:1 ratio, then issues tokens. Investors hold the stock itself or a legal claim to it. Issuance details vary by platform, but the underlying asset always exists.

Perpetual futures work differently. They do not hold any actual stock. Traders deposit margin and open a contract that tracks the price, so there are no claimable underlying assets. Margin is typically paid in stablecoins, with an increasing number of platforms now also accepting other assets like Ethereum (ETH).

Perpetual contracts are notable because they retain the advantages of spot trading, offering 24/7 trading of stocks unavailable on local exchanges and providing higher leverage. Some fully collateralized spot products on Kraken xStocks offer up to 3x margin, while perpetual contracts offer leverage up to 20x, depending on the product. Since there is no need to custody the underlying asset and the price is tracked solely through oracle data feeds, listing is fast and a wide range of tickers can be traded.

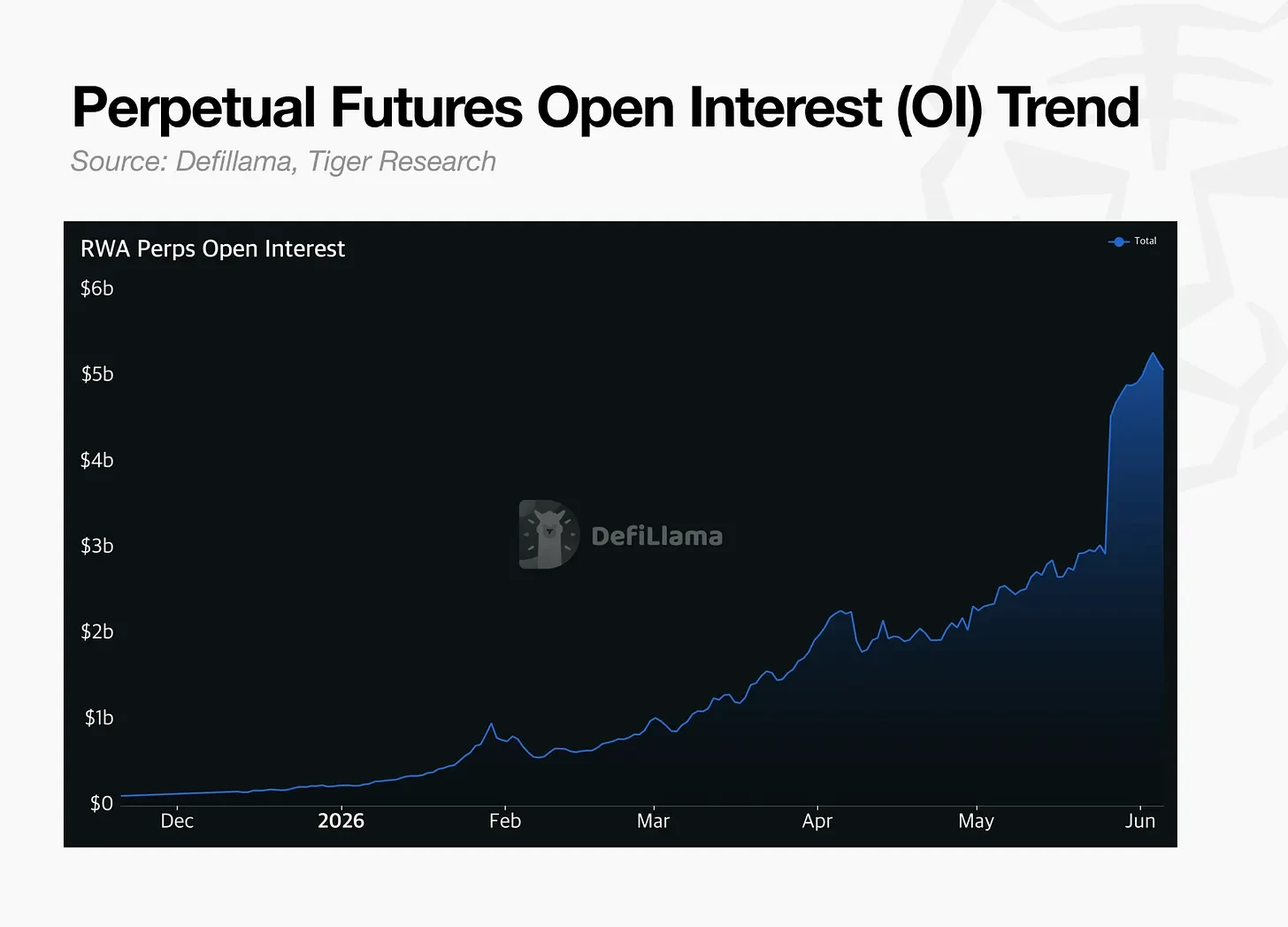

Compared to traditional markets, it is still small. The average daily trading volume in the US stock market is about $1.1 trillion. The open interest for stock options (the total value of currently active contracts) is $2.25 billion. Direct comparison is difficult due to different metrics, but it's clear this market is still in its early stages.

The direction is clear. Open interest (OI) grows every quarter, and regulators are starting to view it as a market. The U.S. Securities and Exchange Commission (SEC) has classified these contracts as an innovative financial product, and the U.S. Commodity Futures Trading Commission (CFTC) is publicly reviewing its institutionalization in the US. Initially operating outside regulatory oversight, it is now rapidly moving into the regulatory framework.

3. A 24-Hour Market vs. Traditional Markets

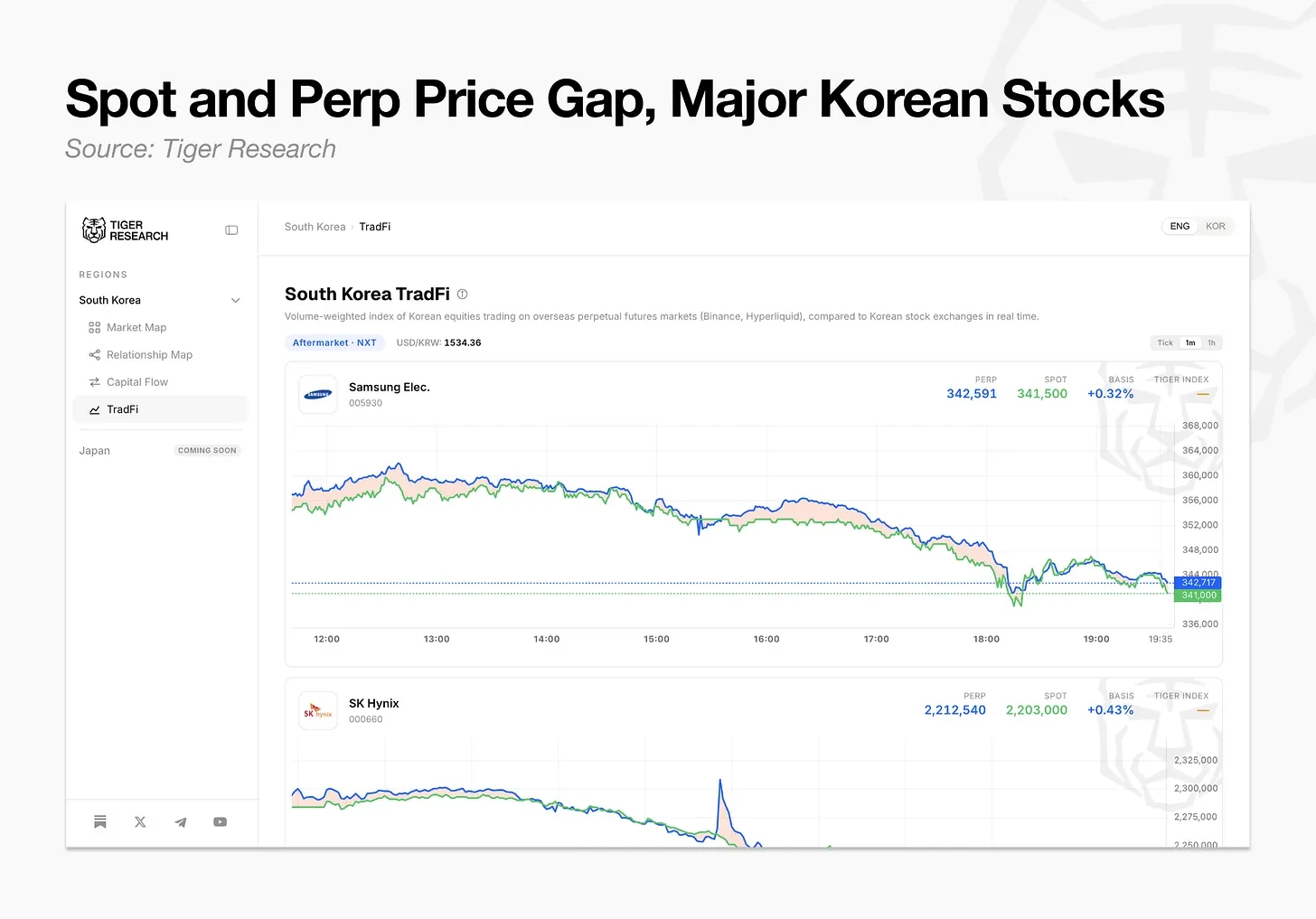

Tiger Research tracked this change and provides a tool that allows real-time comparison of prices for Korean stocks in overseas perpetual contract markets with spot prices on the Korea Exchange (KRX). The tool aggregates prices from perpetual contract exchanges supporting stocks like Samsung Electronics, SK Hynix, and Hyundai Motor, uses a volume-weighted average method, and displays them alongside the domestic spot price for each stock.

Current data reveals three patterns.

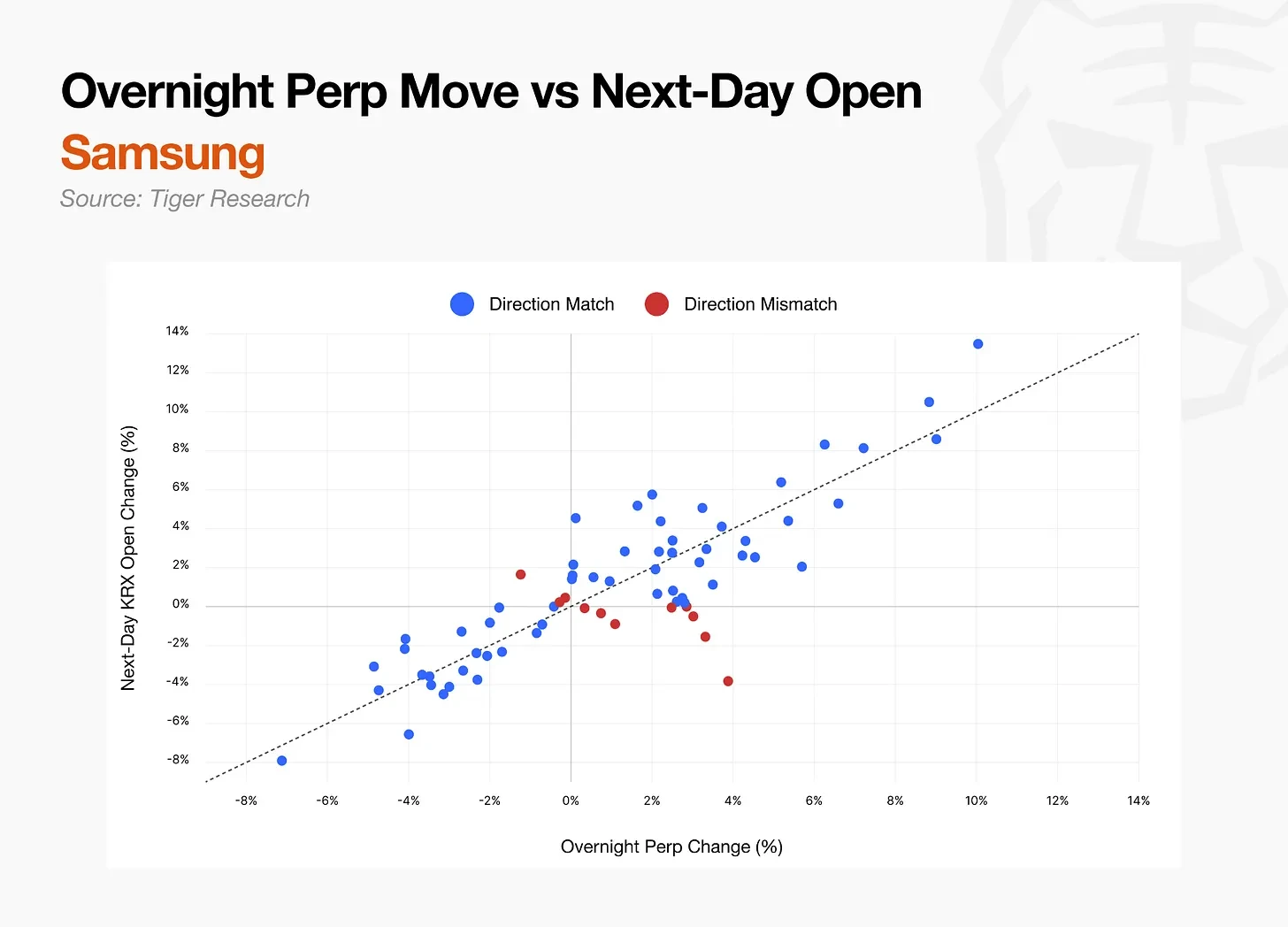

3.1. Overnight Perpetual Futures Movements Predict the Next Opening

The Korean stock market is closed overnight. The US market fluctuates, and reports from Nvidia cause exchange rates to move as well, but the Korean market doesn't resume trading until the next morning. However, perpetual futures trade throughout the night.

This raises a question. What price do perpetual futures reference when spot trading is closed?

The answer is they do not follow a pre-established market price. During trading hours, futures extract the spot price from institutional data. After trading hours, the futures' own trading directly determines the price. They are not replicating the closed spot market price but are discovering new prices based on overnight news and macroeconomic variables.

Data confirms this. On days when the perpetual futures price rose after the stock market close, Samsung Electronics and SK Hynix opened higher in the next trading session 82% and 95% of the time, respectively. When the futures price fell after the close, Samsung Electronics and SK Hynix opened lower 96% and 78% of the time, respectively. The directional alignment is around 85%, with correlation coefficients between 0.85 and 0.89.

The magnitude also aligns. An overnight 3% rise in futures prices leads to an opening rise of about 3%. The regression coefficient between the change in Samsung Electronics futures price and the actual opening gap is 0.93, and for SK Hynix, it is 1.00, almost perfectly predicting the magnitude of the move.

Weekend moves are even sharper. From Friday's close to Monday's open, the predicted futures movement for Samsung Electronics matches the actual Monday opening price 93% of the time, and for SK Hynix, this figure is 87%, as the futures price absorbs two days of global market volatility factors in advance.

By observing overnight futures prices, one can get an advance read on the early morning opening price.

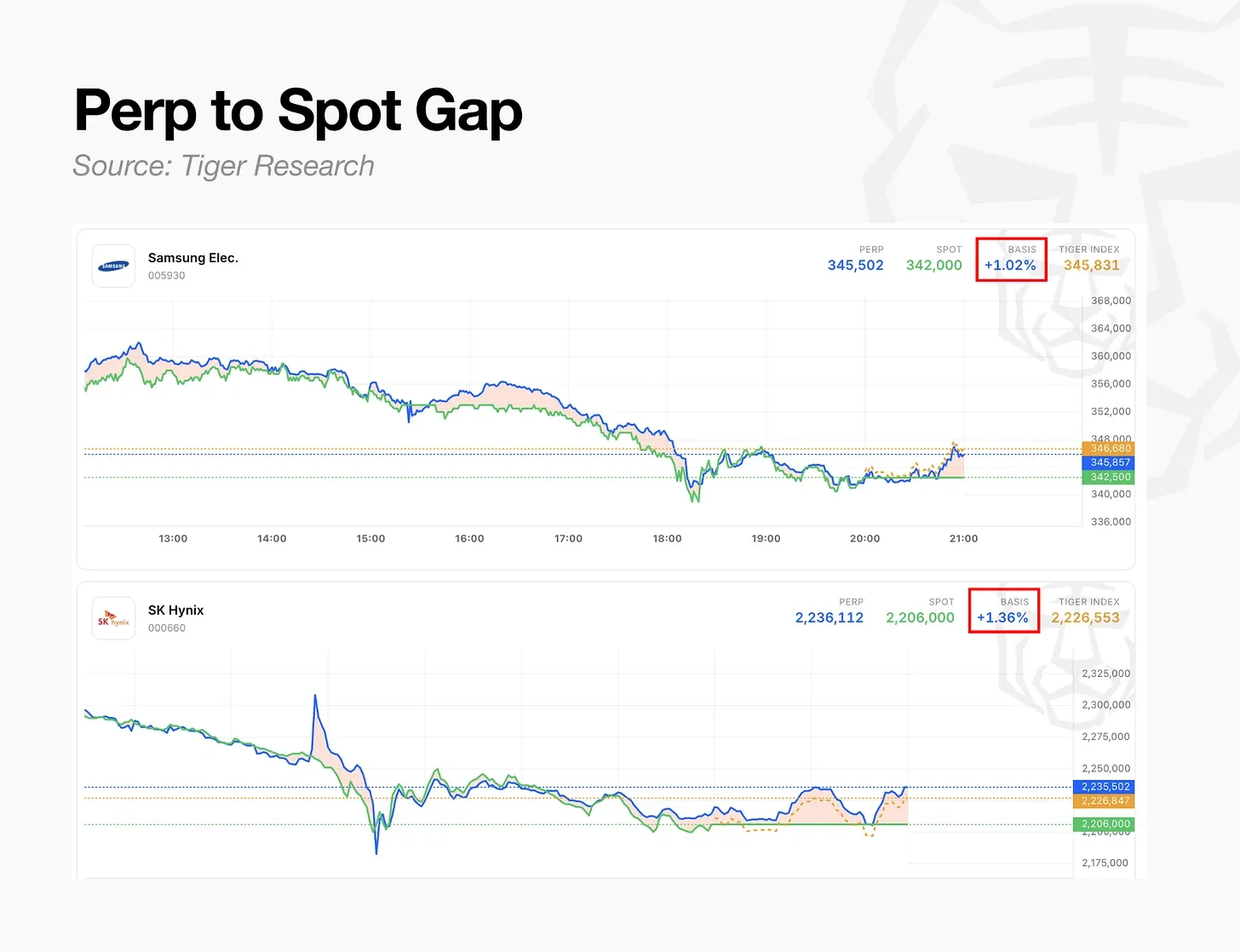

3.2. Delta-Neutral Trade on Spot Premium

Perpetual contracts have no expiration date. To prevent the price from deviating too far from the reference price, long and short positions periodically exchange a fee, known as the funding rate.

For example, when the price is above the reference price, profitable longs pay a premium to losing shorts. The higher the premium, the more they pay. To avoid this fee, traders adjust their strategies, and the price eventually returns near the reference price.

Data shows that Korean stock futures trade at a premium to the spot price, with an intraday average premium of 0.15% for Samsung Electronics and 0.23% for SK Hynix. Selling futures means capturing this premium as funding in each funding cycle.

The strategy is as follows: buy the KRX spot intraday while simultaneously selling an equivalent amount of futures contracts. If the stock rises, the spot position gains, and the futures position loses; if the stock falls, the opposite happens. The two offset each other, so the net result is near zero regardless of the stock's movement. In return, the funding is generated from the sold futures position. The position profits solely from the funding rate without betting on direction. This method of eliminating directional risk is a delta-neutral trade.

The premium doesn't last long. The spot gap typically narrows by half within about 40 minutes. It is suitable for high-volatility periods when the premium expands, but requires continuous monitoring.

3.3. Arbitrage Using Cross-Exchange Price Gaps

At the same time, even for the same stock, perpetual contract prices differ across exchanges. Data from June 2026 shows that Binance's perpetual contract for Samsung Electronics traded at an average premium of 0.93% over Hyperliquid. The SK Hynix contract was 1.03% higher, reaching a maximum of 2.3%.

Positions cannot be transferred between exchanges. Traders need to establish offsetting positions on both exchanges simultaneously. Go short on the exchange with the higher price and long on the one with the lower price, so directional profits and losses cancel out. As the two prices converge, the initial spread turns into profit. On the higher-priced exchange, the short position also earns funding, adding to the return.

Newer exchanges tend to maintain higher prices because less arbitrage capital has flowed in. With more exchanges launching, this price gap recurs in the early stages. At night and on weekends, when spot trading is closed and exchanges set prices independently, the price gap widens further.

4. Market Dynamics and Emerging Opportunities

A major challenge of this market is its fragmentation, which is both a risk and an opportunity. Liquidity is split because the same stock tokens are scattered across existing Korean exchanges as well as platforms like Hyperliquid, Binance, and Lighter. Prices differ between trading venues, making it difficult to identify the "true" price, and price discrepancies create room for confusion and manipulation. Leveraging up in illiquid conditions can trigger cascading liquidations. This presents both opportunities and risks.

The strategies outlined above are for retail use. The same structure provides opportunities for other commercial uses.

- Market Makers: The spread for the same stock traded on different exchanges ranges from 0.15% to 0.75%, widening further at night. Spreads remain persistently wide in the early morning market when arbitrage capital is scarce. Due to illiquidity and fragmented liquidity across multiple exchanges, market making demand is expected to grow.

- Regional Oracles: Perpetual futures discover prices during spot market closures, and their accuracy depends on oracles. Currently, oracles specialized in providing accurate prices for Asian time zone assets like Korea, Japan, and Taiwan are still under development.

- Tokenized Issuance: Currently, listed Korean companies are limited to Samsung Electronics, SK Hynix, and Hyundai Motor. The market needs an intermediary to list and manage KOSPI 200 constituents and major Asian companies.

- Basis Hedge Funds: Investors convert the premium of futures over spot into funding on an hourly basis. Funds dedicated to collecting basis and funding gaps across exchanges turnover capital faster than traditional basis trades, although the market is still too small to absorb fully.

Compared to traditional markets, the perpetual futures market is small, but its significance cannot be ignored. It discovers prices first, trades 24/7, and is rapidly moving towards institutionalization. It presents significant opportunities, both for investment and business.