「Old Guard Stocks」Turned «New Money»: From Dell to Nokia, How AI Is Revaluing Old Infrastructure?

- 核心观点:AI行情正从聚焦模型与GPU的稀缺性,转向大规模基础设施建设阶段。这导致戴尔、诺基亚等拥有系统集成、网络连接和存储交付能力的老牌科技股,因其能承接AI数据中心从芯片到落地的复杂工程,而开始被市场重新估值为AI基建关键参与者。

- 关键要素:

- 估值逻辑转变:市场关注点从AI的“想象力”转向订单、收入和交付能力,使戴尔(Dell,AI服务器订单244亿美元)、HPE等系统集成商受益。

- 网络连接价值凸显:AI集群扩大后,Corning(光通信收入同比增36%)、Nokia(获英伟达投资)和Cisco(数据中心交换订单增超40%)因提供光纤、无线网络等关键连接基础设施而获重估。

- 存储需求爆发:AI模型训练及数据归档创造大量存储刚需,Western Digital(营收同比增45%)等机械硬盘厂商的高容量产品因成本优势,在冷数据存储场景中价值回升。

- 重估验证标准:真正的重估需满足三个条件:有明确的订单与收入兑现、管理层上修全年业绩指引,以及能持续转化为健康的利润质量,而非仅是短期补库存。

- 双重叙事性质:这次重估并非市场怀旧或简单炒作,而是AI进入部署周期后,基础设施环节的系统性价值重定价,但不会平均分配给所有“老牌科技股”。

If you had said a year ago that Dell, Nokia, Cisco, Corning, and Western Digital would once again become hot targets in AI trades, you would probably have been dismissed as out of touch...

For a long time, when the market talked about AI, the first thoughts were typically Nvidia, memory, optical modules, power, and data centers. These were either close enough to the GPU or directly in the hottest part of computing power expansion. In contrast, legacy tech companies like Dell, HP, Nokia, Cisco, Corning, and Seagate were more often labeled as "slow growth," "old stories," and "inflexible valuations."

But, surprisingly, this group of once less-glamorous legacy tech stocks has recently performed quite impressively, prompting the market to reconsider them.

The market quickly adapted and found a suitable explanation: As AI moves from model parameters to real data centers, the market will naturally seek out companies with delivery capabilities and infrastructure expertise. This is why Dell, HP, Nokia, and others are being re-evaluated.

So, is this a genuine industrial revaluation, or is the market just wrapping a new narrative around these legacy tech stocks temporarily?

1. AI Market Shift: Why Re-evaluate Legacy Tech Stocks?

In the past few years, the core logic of AI trading was very clear: first look at the models, then at computing power.

This is easy to understand. Whoever has the best model and can secure the most GPUs gets the most direct market premium. In this phase, investors were most willing to buy into AI imagination, the computing power supply gap, and core beneficiaries like Nvidia.

But the problem is that AI cannot just remain in press releases and model parameters. Models need data centers for training; large-scale inference deployment requires servers, networks, storage, and power; and for enterprises to truly use AI, they need a complete IT architecture and delivery capability.

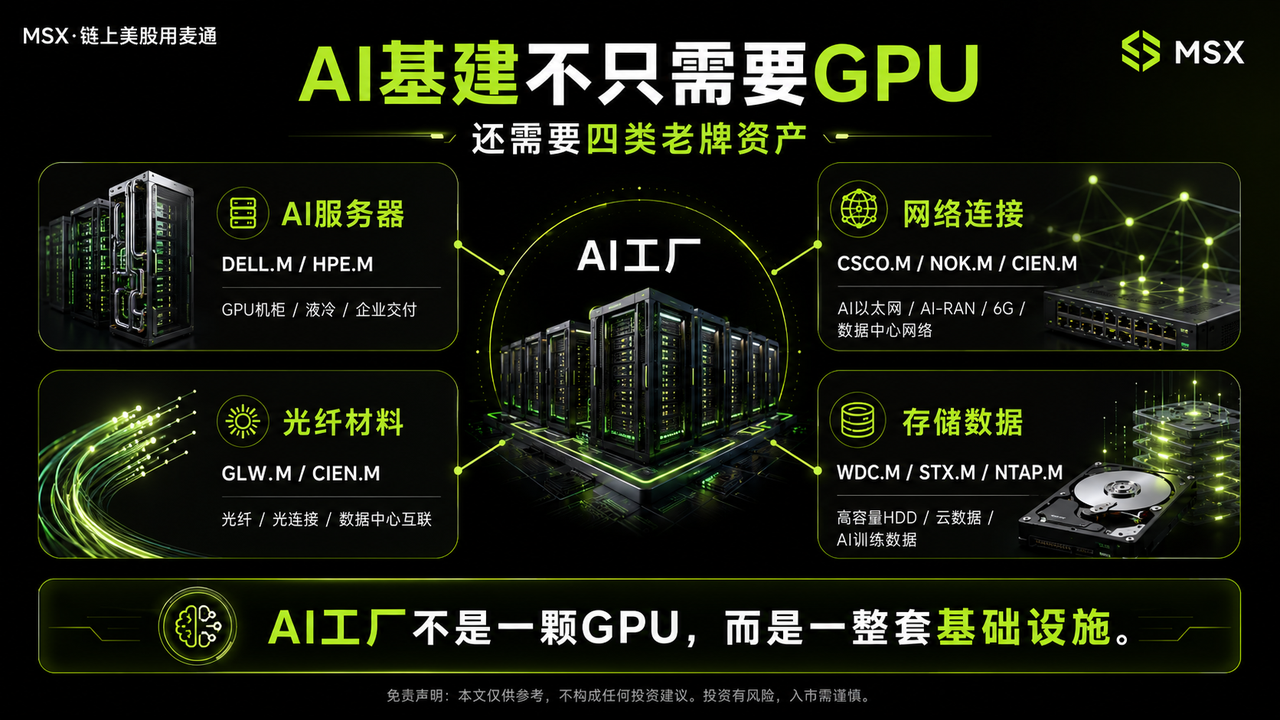

In other words, AI is not a problem solved by a single GPU, but a whole complex system engineering project. This is the starting point for the repricing of legacy tech companies.

Previously, the market saw Dell as PCs and traditional servers, HPE as enterprise hardware, Nokia as the old 5G equipment story, Cisco as traditional network gear, Corning as glass and fiber optic materials, and Western Digital and Seagate as hard disk drive cyclical stocks.

These labels weren't wrong, but within the AI infrastructure cycle, their roles have changed. Building an AI data center requires rack-scale servers, liquid cooling, storage, network switches, fiber optic connections, data management, power support, and enterprise-grade delivery capabilities. The larger the AI cluster, the higher the demands for system integration, network transmission, storage capacity, and operational capabilities.

Therefore, the essence of this revaluation isn't sudden market nostalgia or legacy companies collectively latching onto AI. It's that as AI enters the phase of orders, revenue, and delivery, the market is re-evaluating "who can actually build the AI infrastructure."

These companies may not be the sexiest, but they share a common advantage: the customer base, channels, supply chain, delivery experience, and infrastructure capabilities accumulated over the past decades are becoming valuable again in the large-scale deployment phase of AI.

In other words, AI is repricing a batch of "old assets" based on "new demands."

2. From Servers to Networks to Storage: Legacy Tech Stocks Entering the AI Infrastructure Chain

Overall, the legacy tech stocks being revalued by AI can be broadly divided into three lines: Servers & System Integration, Networks & Connectivity, and Storage & Data Management.

The first line is Servers and System Integration.

Dell is the most typical example. In its latest fiscal quarter, Dell delivered very strong data: Q1 FY27 revenue reached $43.8 billion, with AI orders hitting $24.4 billion and confirmed AI server revenue of $16.1 billion. The company also raised its full-year FY27 AI server revenue forecast to $60 billion and its mid-point full-year revenue guidance to $167 billion.

The importance of this data lies in changing how the market views Dell. Previously, investors focused on PC cycles, traditional servers, and enterprise hardware demand. Now, the market is starting to see if Dell can become a general contractor in building AI factories.

Its advantage isn't making its own GPUs, but its supply chain, delivery capabilities, enterprise customer relationships, server system design, and ability to complement the Nvidia ecosystem. An AI server isn't just selling a GPU; it involves integrating it into a rack, connecting it to the network, power, and liquid cooling system, and then delivering it to cloud providers and enterprise clients.

Dell captures this value-adding step from the chip to the system deployment. HPE's logic is similar.

HPE's stock surged after its latest earnings report, primarily due to strong AI infrastructure demand. The company's Q2 revenue reached $10.68 billion, up 40% year-over-year; Cloud & AI related business revenue was $7.71 billion, and it raised its full-year FY2026 growth forecast. More importantly, HPE's acquisition of Juniper Networks enhances its networking capabilities, transforming it from a traditional server company into more of an "AI network + enterprise infrastructure" platform.

Thus, the revaluation logic for Dell and HPE isn't about "them becoming the next Nvidia." Instead, they are becoming crucial system integrators within the AI factory construction team.

The second line is Networks and Connectivity.

One of the most overlooked aspects of AI infrastructure is connectivity. Computing power doesn't exist in isolation. Data centers need high-speed internal interconnects, data centers need fiber optic connections between them, and as AI applications expand to the edge and terminals, stronger telecom networks and wireless infrastructure are needed. The larger the scale of AI training and inference, the more networks and connectivity transition from supporting roles to critical infrastructure determining computing power efficiency.

This is why Corning, Nokia, and Cisco are being re-evaluated by the market. Corning is a classic example. It's not a traditional AI chip stock, but its fiber optics, optical connectivity, and optical communications materials are precisely the vital supporting components for AI data center expansion.

The company's Q1 2026 core sales reached $4.35 billion, up 18% year-over-year; its optical communications business sales hit $1.846 billion, up 36% year-over-year. The company also noted that Gen AI product demand and new long-term agreements with large hyperscaler customers are significant growth drivers. This shows that AI data centers need not just GPUs but also the foundational materials to truly connect the computing power.

Nokia's story extends from traditional 5G equipment to AI-RAN, 6G, and AI-native wireless networks. Nvidia previously announced a $1 billion investment in Nokia, aiming to collaborate on advancing AI-RAN and the transition from 5G to 6G. This signal is significant because future AI traffic won't remain confined to data centers; it will also flow into terminal devices like phones, cars, robots, and AR/VR headsets. As long as AI applications continue to diffuse to the edge and mobile networks, telecom infrastructure companies will regain narrative space.

Cisco's logic leans more towards data center networking. The company's Q3 FY2026 revenue reached $15.8 billion, up 12% year-over-year; data center switching orders grew over 40% year-over-year. Remember, in AI clusters, the network is not just simple cabling; it's a critical component affecting data transfer efficiency, compute utilization, and cluster stability.

The common logic for these companies is: the more AI moves towards large-scale deployment, the more valuable networks and connectivity become.

The third line is Storage.

This line has become widely known in the market over the past two months. The market realizes AI needs not only computing power but also storage. While the past focus was on HBM, DRAM, and NAND, high-capacity HDDs are now back in the spotlight because AI model training, inference logs, video data, enterprise data, and cold data archiving all generate massive storage capacity demands.

Western Digital is a representative example. The company's latest quarterly revenue increased 45% year-over-year to $3.34 billion and provided next-quarter revenue guidance above market expectations. More importantly, the market noted that its high-capacity hard drive demand is primarily driven by AI and cloud data centers. Seagate is similar, benefiting significantly from high-capacity nearline drives, with data center customers constituting an increasing share of its business.

Of course, in the AI era, not all data needs to reside on the most expensive, high-speed storage. A vast amount of cold data, training data, logs, video data, and archival data still requires cost-effective, high-capacity hard drives. Thus, the revaluation logic for WDC and STX isn't "the sudden rebirth of HDDs," but that the explosion of AI data makes storage a necessity once again.

3. What Constitutes a True Revaluation?

However, the AI-driven revaluation of legacy tech stocks doesn't mean all old companies are blindly worth buying.

A crucial distinction lies in whether a company is genuinely integrated into the AI infrastructure chain. To judge if a company is truly being revalued, one should consider at least three criteria:

- First, evidence of orders and revenue: For example, Dell's AI orders and AI server revenue, HPE's Cloud & AI related business, Corning's optical communications revenue, Cisco's data center switching orders, and WDC's high-capacity hard drive demand – these are more significant than simply telling an AI story.

- Second, upward guidance revisions: If AI remains confined to press releases and product launches, stock prices can easily rally and then fade. But if management is willing to raise full-year revenue expectations, business growth forecasts, or key product shipment estimates, it signals that AI demand is not just short-term sentiment but may be changing the company's growth trajectory. This is why the market is repricing companies like Dell and HPE.

- Third, can profit quality keep pace? The biggest issue for legacy hardware companies has always been gross margins and cyclicality. Rapid AI server revenue growth doesn't guarantee high profit elasticity. Rising storage prices could be a short-term supply-demand mismatch. Increased network equipment orders must translate into sustainable profits.

A truly good revaluation involves simultaneous improvement in revenue growth, order visibility, and profit quality.

If only revenue rises while gross margins are squeezed thin, or if demand is just a short-term restocking cycle, then the valuation revaluation will be limited. Ultimately, the market buys not "old companies telling new stories" but "can old assets combined with new demands generate new profits."

This is the most noteworthy aspect of this "old trees blooming new flowers" phenomenon. AI will not turn all traditional tech companies back into growth stocks. It will only select those that are truly entrenched in critical infrastructure bottlenecks and can convert AI demand into orders, revenue, and profit.

Final Thoughts

Objectively speaking, the AI market momentum has moved beyond just "who has the better model" or "who has more GPUs." The real change is that AI is entering a phase of genuine construction.

As AI data centers multiply, server companies will be repriced. As computing clusters become more complex, network companies will be repriced. As data centers require more fiber optic connections, materials companies will be repriced. As AI data continues to explode, storage companies will be repriced.

This is the reason legacy tech stocks are being seen by the market again. They haven't suddenly become young again; rather, the AI era is re-engaging the infrastructure they already possess.

But this also means this revaluation won't be evenly distributed among all "legacy stocks."

Only those legacy tech companies that can truly enter the capital expenditure cycle of data centers and enterprise deployment have the potential to move from "valuation recovery" to "logical revaluation."