AI PC Battle: Don't bet on the camp, bet on the tollbooth

- Core Thesis: The essence of the AI PC competition is not the architecture war between x86 and Arm, but the identification of a 'tollbooth' logic within the industry chain; prioritize investing in segments that can generate sustained cash flow, such as advanced manufacturing processes and computing platforms, rather than betting on a specific camp.

- Key Elements:

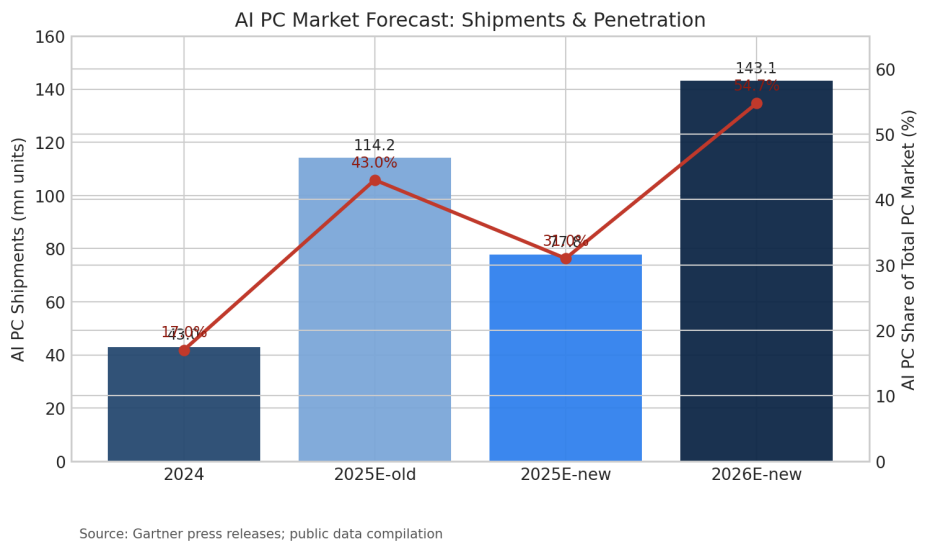

- Gartner predicts AI PC penetration will reach 54.7% by 2026; short-term disruptions from tariffs are possible, but the long-term trend of AI PCs becoming standard remains unchanged.

- User upgrade motivation depends on whether local AI applications (e.g., enterprise-level private computing) can surpass basic experiences like 'meeting minutes'.

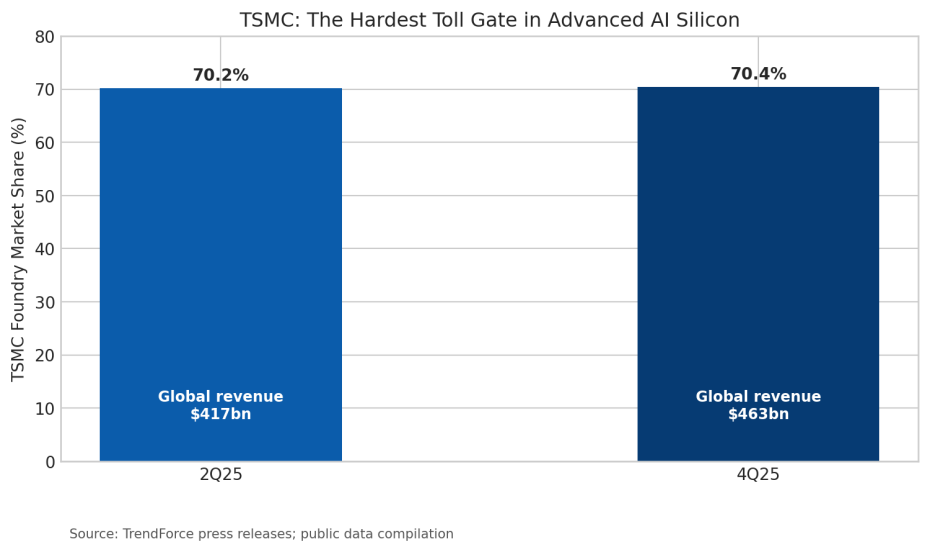

- TSMC, as the 'tollbooth' for advanced manufacturing, held approximately 70.4% of the global wafer foundry market share in Q4 2025, benefiting from competition among all players.

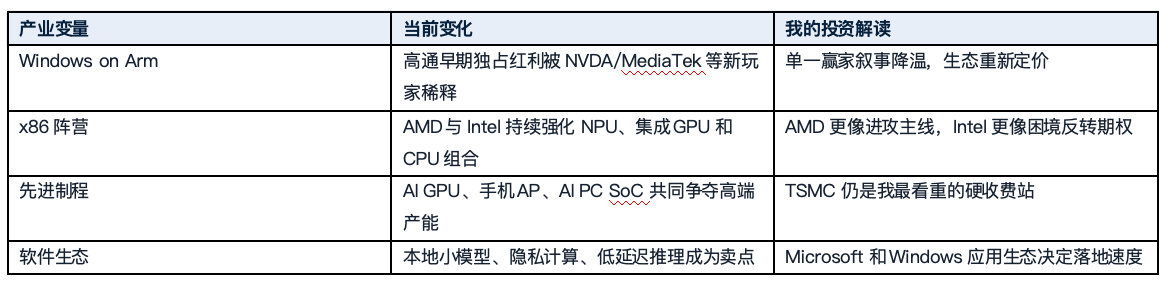

- The entry of Nvidia and MediaTek has shifted the Windows on-device AI ecosystem from single-player trials to a multi-player landscape, intensifying competition.

- Investment targets are tiered: TSMC as a core holding, AMD and Nvidia for offensive flexibility, while ARM and Intel represent high-risk turnaround opportunities.

Original Author: Roger Lee, BIT Stocks Special Analyst

With 21 years of experience in investment banking, asset management, and financial institutions, specializing in long-term research on the AI industry chain, U.S. stock macro liquidity, and options strategies.

Report Date: June 4, 2026

Investment Summary

My core conclusion is simple: Don't bet on factions in the AI PC battle; bet on the toll collectors. TSMC as the foundation, AMD for offense, ARM as a small speculative position for the long haul, Intel only as a lottery ticket, Qualcomm awaits repricing, and NVIDIA, don't chase FOMO after news surges.

NVIDIA and MediaTek entering the AI PC space, on the surface, adds a new chip combination to consumer PCs, but the essence is the Windows on-device AI ecosystem moving from single-point trials to multi-player competition. My assessment is that this war shouldn't be simplified into a "x86 vs. Arm" religious alignment. What's truly worth studying is who can navigate upgrade cycles, sustain gross margins, cash flow, and pricing power within the industry chain.

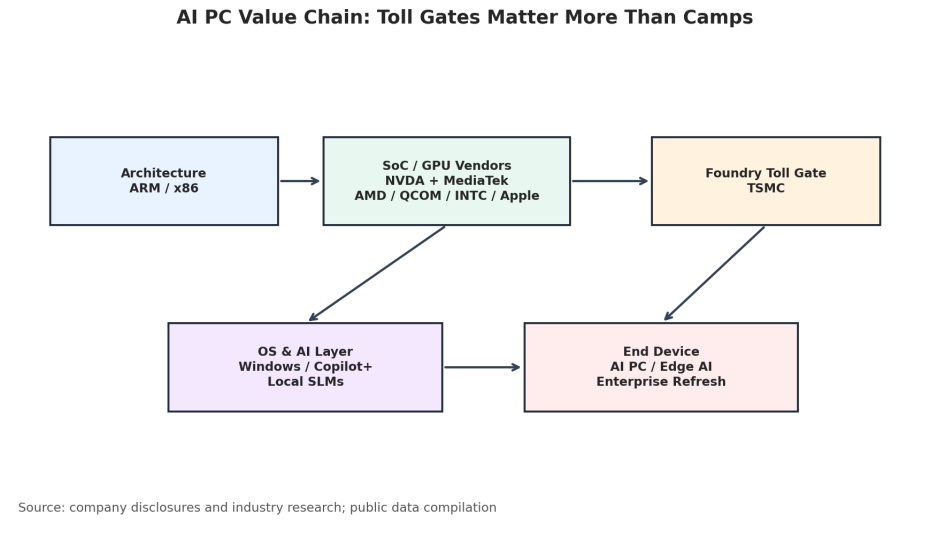

I view AI PC as a three-tiered opportunity: The first tier is the advanced process tollbooth. Regardless of who wins, TSMC collects the tolls. The second tier is computing power and platform spillover. AMD and NVIDIA represent x86 offense and GPU software stack extension, respectively. The third tier is architecture diffusion and turnaround plays. ARM and INTC both have upside potential, but position sizing discipline must be stricter.

1. Industry Outlook: AI PC Moving from Concept to Shipment Validation

Gartner in 2024 initially projected 2025 AI PC shipments at 114.225 million units, a 43% market share. After revisions in 2025, impacted by tariffs and procurement pace fluctuations, the forecast was cut to 77.792 million units, a 31% share. However, 2026 is still expected to reach 143.113 million units, a penetration rate of 54.7%. My takeaway from this data isn't that "AI PC demand is disproven," but rather that short-term rhythm may fluctuate, but the long-term direction towards standardization remains unchanged.

From an investment perspective, the real challenge for AI PC isn't "whether it has an NPU," but whether users are willing to upgrade their devices for a locally-based AI experience. If application layers remain limited to meeting notes, image generation, and simple assistants, upgrade elasticity will be lower than the market's most optimistic expectations. However, if enterprise users start adopting privacy computing, low-latency inference, and local knowledge base deployment as standard configurations, AI PC will evolve from a consumer electronics narrative to an enterprise IT upgrade story.

From an investment perspective, the real challenge for AI PC isn't "whether it has an NPU," but whether users are willing to upgrade their devices for a locally-based AI experience. If application layers remain limited to meeting notes, image generation, and simple assistants, upgrade elasticity will be lower than the market's most optimistic expectations. However, if enterprise users start adopting privacy computing, low-latency inference, and local knowledge base deployment as standard configurations, AI PC will evolve from a consumer electronics narrative to an enterprise IT upgrade story.

2. Competitive Landscape: Chipmakers Battle, TSMC Collects Toll Fees

The surface-level narrative of AI PC is Arm challenging x86, but I'm more focused on where the profit pool migrates. NVIDIA's strength lies in GPUs and AI software stack, AMD's in x86 CPU and GPU combinations, Qualcomm's in low power and connectivity, and Intel's in the existing ecosystem and enterprise channels. Each has its advantages, but a key commonality is evident: High-end chips are inseparable from advanced processes.

TrendForce data reveals Q2 2025 global wafer foundry revenue was approximately $41.7 billion, with TSMC holding a 70.2% share. In Q4 2025, global wafer foundry revenue reached about $46.3 billion, with TSMC's share around 70.4%. This indicates that as long as AI PCs, AI servers, mobile APs, and edge AI chips continue to compete for advanced processes, TSMC isn't just a simple cyclical stock but more akin to a toll gate entrance for the entire AI hardware era.

I don't believe every new product launch is worth chasing, but I do believe that with every instance of intensified industrial competition, one should ask the reverse question: If the winner is uncertain, who can charge all winners? Within the AI PC domain, my answer remains advanced processes, packaging, key IP, and platform software, rather than simply betting on any single architecture slogan.

3. Ticker Ranking: TSM for Core Holdings, AMD for Offense, Intel/ARM for Upside Potential

Over the past year, semiconductor tickers have already priced in expectations for AI PC, on-device AI, and computing power spillover. Yahoo Finance daily prices show that AMD, Intel, ARM, and TSM all exhibited strong elasticity within the sample period, but they represent different risk-reward profiles. My approach isn't to buy all AI PC-related tickers together, but to layer them based on certainty, valuation discipline, and position within the industry chain.

My core conclusion is straightforward: This isn't a war to buy only the winner; it's a war to buy the tollbooths, the platforms, and the companies with certain cash flows. If the market prices in full sentiment on the day of a news announcement, I'd rather wait. If a correction brings the risk-reward of good companies back into a reasonable range, I'll prioritize TSM and AMD, followed by the opportunistic plays of ARM and Intel.

4. Risk Warning

The risks along this theme cannot be ignored. First, AI PC applications may underperform expectations, leading to weaker-than-anticipated upgrade cycles. Second, if Windows on Arm compatibility improvements are too slow, the narratives for Qualcomm and new entrants will be suppressed. Third, tariffs, paused corporate procurement, and macroeconomic uncertainties can impact PC demand. Fourth, if advanced process supply and demand face periodic mismatches, TSMC could also see valuation pullbacks. Fifth, valuations across the entire AI chain are elevated, and once U.S. stock risk appetite declines, the tickers with the highest elasticity often experience the fastest drawdowns.

Therefore, I prefer to treat AI PC as a long-term industry migration, not short-term news trading. The truly professional approach isn't buying slogans on launch day, but waiting for the emotional tide to recede and then buying ecosystems, tollbooths, and companies capable of consistently delivering cash flow.

5. Data Source Explanation

Data References

This report was prepared by a special analyst. The views expressed in this report represent only the personal stance of the author and do not represent the views of the BIT platform. This material is for reference only and does not constitute investment advice.