One million in a week: The crypto arbitrageur's new hunting ground in US stocks

- Core Thesis: The crypto industry is applying the perpetual contract funding rate arbitrage strategy to US stocks. By executing a "spot long + perpetual short" hedging operation, traders capture high funding rates, generating a stable "rent-collecting" yield. This represents the early-stage dividend of crypto financial innovation permeating traditional assets.

- Key Elements:

- Perpetual contracts use a funding rate mechanism to balance long and short forces. When longs are overcrowded, they must pay fees to shorts, with rates reaching annualized hundreds of percent (e.g., Samsung Electronics on Binance hit 364%).

- Major crypto player Cbb employs a hedging strategy: buying US stocks spot while simultaneously shorting the perpetual contract on Hyperliquid. This approach has yielded $2.4 million in funding fees over recent months, independent of stock price movements.

- Institutions like Ethena plan to apply delta-neutral arbitrage strategies to US stock perpetuals, projecting stable annual revenue of $40 million to $80 million through funding rate capture.

- Binance now supports spot and perpetual contract trading for over 7,000 US stocks, while open interest on decentralized platforms like Hyperliquid continues to grow, expanding the market base.

- The early opportunity window for this arbitrage may narrow as arbitrage capital floods in, similar to the case where Bitcoin's perpetual funding rate was compressed from an annualized 18% to 9%.

Futures, options, contracts for difference — these terms sound highly professional.

In the past, many people assumed derivatives were the most high-barrier aspect of traditional financial markets, but these instruments are becoming increasingly common in the crypto industry.

Recently, beyond the US stock targets themselves, the crypto community has been buzzing with discussions like: "I've been having a blast arbitraging on Hyperliquid, I don't even feel like doing research anymore," and "All I see is funding."

A few years ago, this kind of talk would have been about arbitrage opportunities in Bitcoin and Ethereum. But now, with US stocks coming on-chain as a new trend, their targets have shifted to American equities like Samsung, Nvidia, and GameStop.

Although trading US stocks has almost become mindless now. Just throw money into the hot sectors—chips, energy, optics—and your account will likely go up. Someone around you always doubles their money by betting on one or two stocks. But these savvy crypto professionals make money in a way that has *nothing* to do with whether stocks go up or down.

A group of crypto natives is quietly building a new profitable business around US stocks, using strategies born in the crypto market.

A Contract That Never Expires

This logic starts with something called a perpetual contract. Perpetual contracts are the highest-volume "alternative futures" in the crypto market. They never expire, require no manual rollover, and are specifically for betting on price movements with leverage. You can open a $50 position with just $5, trade 24/7, and no one stops you from placing an order at 3 AM.

But perpetual contracts had a problem from the start: how do you keep the price of a contract that never expires tethered to the actual stock price, without it drifting away?

The crypto industry's solution for perpetual contracts was to introduce a mechanism called the funding rate.

In simple terms, the funding rate is a head tax: whichever side has more people pays.

For example, you're bullish on Nvidia. Instead of waiting for the US stock market to open, you open a 5x long position on a perpetual contract.

The problem is, too many people want to do the same thing. The long side is overcrowded, with few on the short side. To balance the two sides, the system dictates: the side with fewer people gets paid, and the side with more people pays. So, as a long trader, you automatically send a payment to those on the short side every few hours. The more people going long with you, the more you pay. It can get so expensive it feels like paying a fine.

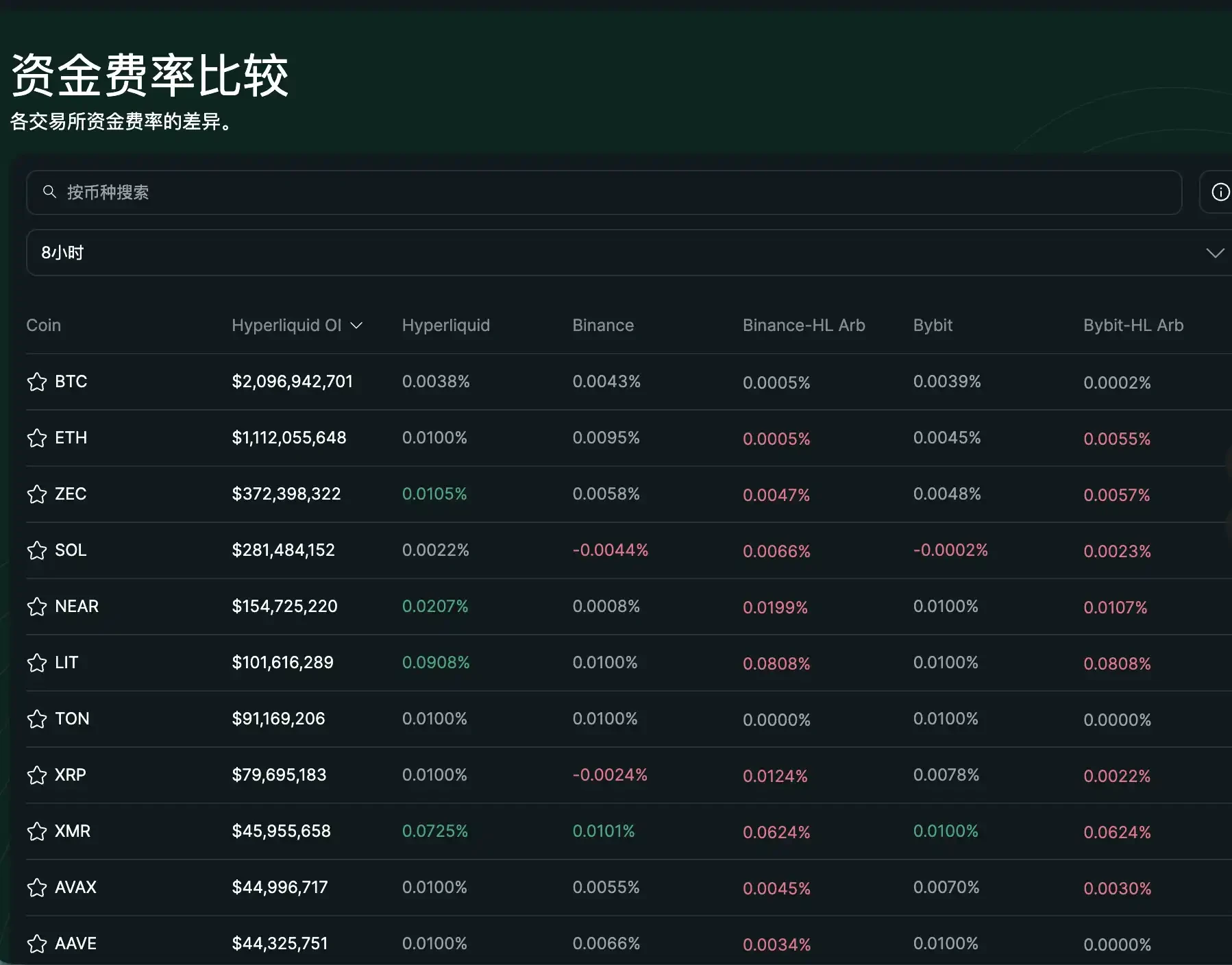

How expensive can this fine get? Let's look at some real numbers.

Binance is the world's largest cryptocurrency exchange by trading volume. The annualized long rate for its Samsung Electronics perpetual contract is 364%. This means if you are fully long on Samsung for an entire year, this head tax alone would eat up more than three times your principal. Nokia's annualized rate is 403%, and BBX is 591%.

Another platform that must be mentioned is Hyperliquid. It is currently the largest decentralized perpetual contract trading platform by on-chain volume. No account registration or KYC is needed; anyone can connect their wallet and start trading. It's a product in the crypto space that brings the perpetual contract experience closest to that of a centralized exchange.

Hyperliquid Trading Interface

On Hyperliquid, Dell's rate is 281%, GameStop (GME) is 227%, and even Zoom has a rate of 287%. A video conferencing company, and still so many are rushing to leverage bets on its rise.

An interesting aspect of this rate is that it serves as a clear signal of market sentiment.

It shows how overheated the market is right now. Which stock is being chased the most, where the long side is most crowded, that's where the rate is highest. The reverse is also true. Eli Lilly, one of the largest pharmaceutical companies in the US, has a negative funding rate on both Binance and Hyperliquid. On Binance, going long on Eli Lilly not only requires no payment but also earns you an annualized 65%. On Hyperliquid, you can earn 103%.

This indicates that there are too many people shorting Eli Lilly. The system must pay people to go long to maintain balance. The funding rate for the same stock can also differ across platforms. For Apple, the rate is 0% on Binance but -14% annualized on Hyperliquid. This difference itself creates an arbitrage opportunity. These numbers don't lie: the more aggressively a side is pushed, the more lucrative it is to be on the opposite side.

These extreme funding rates are visible in real-time on platforms like Hyperliquid, also spawning cross-exchange arbitrage opportunities (e.g., the rate differential between Binance and Hyperliquid).

A New Business After US Stocks Go On-Chain

Cbb (X: @Cbb0fe) is a well-known whale in the crypto space. He made his initial fortune in the crypto market and has been arbitraging token perpetual contracts for years. He once publicly detailed how he earned $5 million running arbitrage bots on the Hyperliquid chain.

He is also one of the first to transplant this strategy to US stocks.

Cbb's operation logic is simple: buy the actual stock in the regulated market while simultaneously opening an equivalent short position in the perpetual contract. If the stock price goes up, the profit from the spot position compensates for the loss on the contract; if the price goes down, the profit from the contract covers the spot loss.

With this hedge, price movements become irrelevant. The only thing he cares about is that intermediate head tax—the funding rate. He recently stated that he has earned $2.4 million just from collecting funding fees. While everyone else is frantically trading US stocks panning for gold, he is selling them shovels. Now that US stock perpetuals have emerged, he has directly applied this well-honed crypto strategy to underlying assets like Apple and Samsung.

You might ask, why is this opportunity unique to the crypto space? Can't it be done in traditional finance? Traditional markets have similar costs, like stock borrowing fees or overnight interest. You pay a cost for margin long positions or borrowing stocks to short. However, that money goes into the broker's pocket. The entire mechanism is opaque; you can't see the overall long/short ratio in the market, and you certainly can't act as a counterparty to receive this fee. Brokers keep this business for themselves; ordinary people can only pay, not earn. Perpetual contracts lay this mechanism bare. Anyone can see the real-time funding rate, and anyone can be the one receiving the payment. This is a creation of the crypto world, now applied to US stocks.

It's not just individuals like Cbb. Institutions are also starting to eye this lucrative opportunity.

Ethena, one of the largest stablecoin projects on the Ethereum ecosystem, is considering allocating a portion of its reserves for this hedging strategy. They estimate this could generate an additional $40 million to $80 million in revenue annually.

Through a delta-neutral hedge (long spot + short perpetual), Ethena captures the funding rate, making it a core mechanism for its USDe yield. This strategy has been embedded in its protocol mechanism, functioning as quantifiable "rent-seeking" income rather than pure speculation.

For institutions, this isn't gambling. It's a stable cash flow that can be incorporated into asset allocation. Its nature is closer to collecting rent, with the tenants being those eager to use leverage to trade US stocks.

So the question is: will astronomical annualized rates like Samsung's 364% and BBX's 591% persist, or will they eventually be arbitraged away?

Let's look at Bitcoin as a benchmark. In the early days, the annualized funding rate for Bitcoin perpetuals was consistently around 18%. After the spot ETF launched, Wall Street arbitrage capital flowed in, compressing the rate to 9% within months—a 50% cut.

US stock perpetuals are likely to follow the same path. The high rates now are because few arbitrageurs have entered the market, and the order books are thin.

But now, Binance has listed over 7,000 stocks for spot trading, the NYSE is promoting 24/7 trading, and the US futures regulator, the CFTC, is signaling a willingness to create a compliant pathway for perpetual contracts. Both sides are moving towards the middle. The CFTC has already opened a compliance path for Bitcoin perpetuals, platforms like Coinbase are launching pilot perpetual products, and Hyperliquid's open interest (OI) for stock perpetuals is growing steadily. As arbitrage capital floods in, the rate compression we saw with Bitcoin—from 18% down to 9%—is likely to be repeated for US stock perpetuals.

Therefore, this current phase is essentially an early-stage window of opportunity. Those who get in first can capture the fattest part of the pie.