President Q1 Holdings Disclosure: Is Trump's Money Accelerating Toward AI Infrastructure?

- Core Viewpoint: Trump-affiliated accounts underwent a massive portfolio restructuring in Q1 2025 (over 3,700 transactions exceeding $220 million in total value). The core direction shifted from established platform tech giants like Microsoft, Amazon, and Meta, as well as defensive assets, towards a systematic increase in exposure to AI infrastructure supply-side sectors, including semiconductors, AI hardware, and enterprise software. This reflects a judgment on future industry directions and policy priorities.

- Key Elements:

- Massive Reduction in Old Economy Tech Giants: The largest Q1 sell-offs in the stock account were concentrated in Microsoft, Amazon, and Meta, all reaching the highest disclosure bracket of $5 million to $25 million. Simultaneously, it reduced holdings in defensive assets like dividend-style ETFs, indicating an elevated risk appetite.

- Systematic Buying Across the AI Value Chain: Purchases covered the entire AI infrastructure chain, encompassing semiconductors (Nvidia, Broadcom, AMD, Intel), AI hardware (Dell, Intel), enterprise software (Oracle, ServiceNow), and EDA tools (Synopsys), reflecting a comprehensive bet on AI infrastructure.

- Policy Sensitivity and Timeline Controversy: In the case of Dell, the related account first established a position (February 10), followed by Trump's public endorsement, after which Dell secured a government contract. This timeline has drawn significant market attention to the potential link between trading and public policy.

- Coexistence of Core Holdings and Offensive Positions: While increasing exposure to AI infrastructure, the account also purchased S&P 500 ETFs, Russell 1000 ETFs, and bonds, maintaining overall market exposure and liquidity. The strategy involved actively making thematic bets on top of a broad-based asset foundation.

- Structural Trend Signal: This portfolio shift highlights three structural clues: the AI trade moving from models to infrastructure supply; diversification of semiconductor investment targets (beyond just Nvidia); and the AI transformation of enterprise software becoming a potential undervalued segment.

Original Author: Mike, Frank, MSX Maitong

Since 2025, two men have been most effective at "moving the market" with their public remarks.

One is Jensen Huang. Whenever he takes the stage at a keynote to talk about GPUs, Blackwell, or data centers, the market immediately reimagines the ceiling of AI. The other is Donald Trump. Beyond directly endorsing specific stocks, his public statements and policy implementations influence the expectations of entire industrial chains.

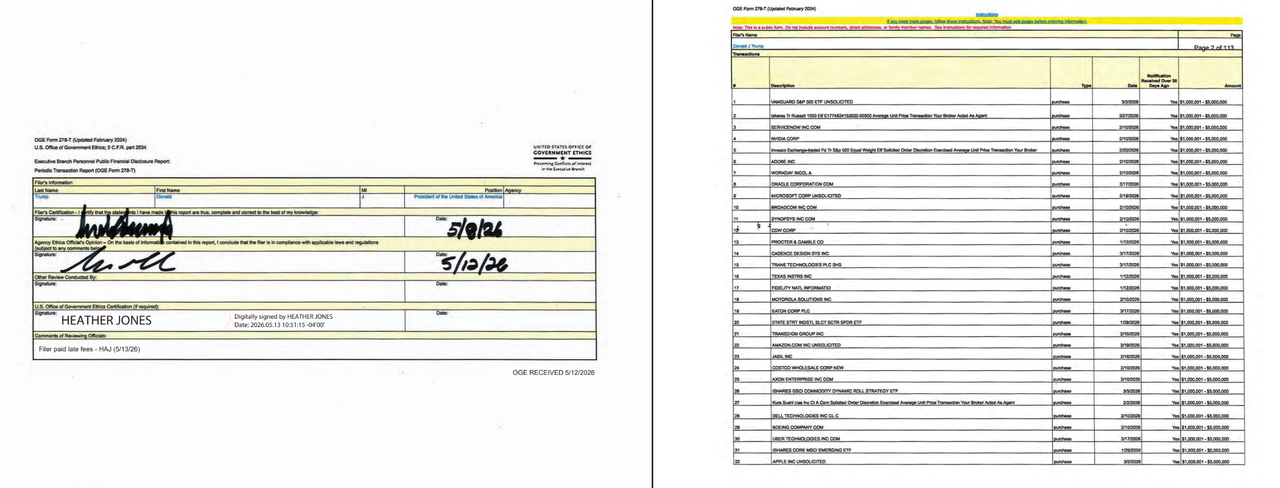

Interestingly, Trump recently filed his personal financial disclosure with the Office of Government Ethics (OGE), as required by law, detailing his stock holdings, funds, transaction records, and value ranges. While the disclosure document doesn't prove every trade was personally directed by Trump, nor should it be simply interpreted as explicit buy or sell recommendations, it at least offers a window for observation:

When the accounts of the most policy-influential individual begin to show clear directional adjustments, the market naturally becomes curious about the underlying industrial judgments.

After a thorough analysis, MSX found that the most noteworthy aspect of this Q1 disclosure is precisely that Trump's related accounts have begun trading intensively, with a clear direction shifting towards AI infrastructure, particularly by significantly reducing positions in some legacy platform technology and defensive assets to increase allocation to the AI infrastructure supply side.

Undoubtedly, as the ultimate decision-maker of U.S. policy, his portfolio structure, to some extent, reflects his judgment on future industrial directions. It also provides ordinary investors a window into what the world's most powerful "smart money" is thinking.

1. $220 Million in Trading Volume, Over 3,700 Trades

Looking at the most straightforward data first, it's a textbook example of "diligent trading."

According to the disclosure filing, Trump-related accounts completed 3,711 securities transactions in Q1. Roughly calculated based on actual trading days, this equates to dozens of operations daily. Aggregated by the lower end of the reported ranges, the transaction volume exceeded $220 million. This is clearly not a passive, static account; it's approaching the quarterly trading volume of a small to mid-sized hedge fund.

More interestingly, this differs greatly from his investment style during his first term (2017-2021). Back then, disclosures showed he held approximately 100 individual stocks across finance, healthcare, industrials, and other sectors, resembling a diversified blue-chip portfolio. After entering the White House, he entrusted his assets to family and related institutions, significantly reducing individual stock holdings, with less active trading than now.

It's worth noting that President Obama invested in Treasury bonds and diversified mutual funds, while Biden entirely refrained from stock trading during his term. Previous presidents generally chose to divest assets or establish blind trusts to avoid conflicts of interest. Trump's approach in his second term has completely broken this convention.

Delving deeper, a very thematic portfolio adjustment emerges.

Let's first see where the money exited.

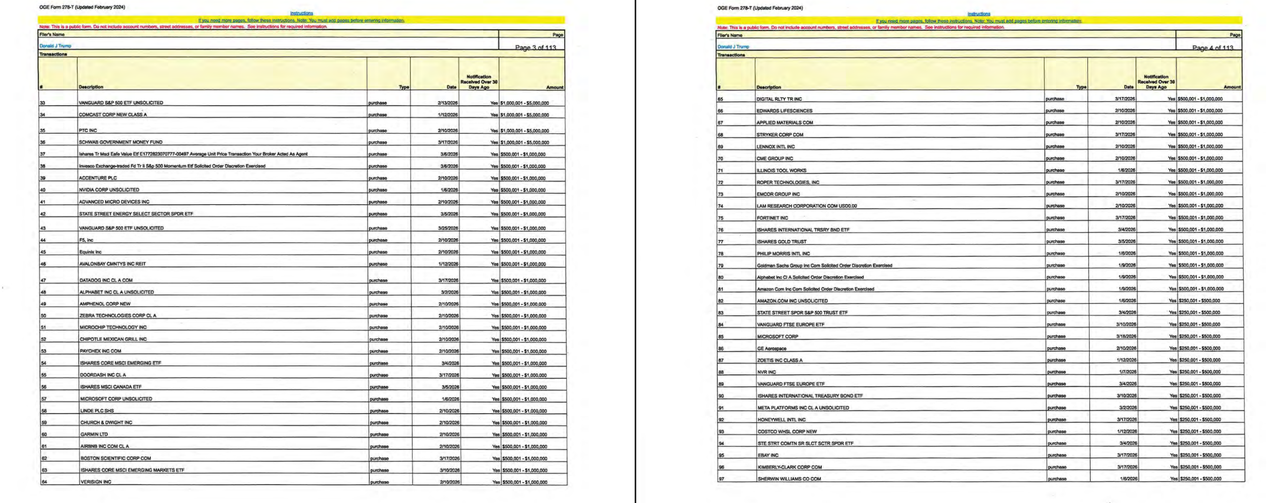

In Q1, the largest sell-offs in Trump-related accounts were concentrated in Microsoft, Amazon, and Meta. Based on the disclosed ranges, these trades all hit the highest bracket of $5 million to $25 million. These three companies are undoubtedly core assets among U.S. tech stocks, but they share a common trait: they represent the super winners of the previous era of consumer internet, advertising platforms, e-commerce, and cloud services.

Microsoft has software and cloud, Amazon has e-commerce and AWS, and Meta has social networks and ad systems. They are not without an AI story; indeed, they are major AI spenders. However, from a portfolio perspective, these companies have already fully realized significant valuation gains in recent years. Therefore, large-scale selling doesn't necessarily equate to a bearish view; more accurately, it indicates reducing the weight of legacy platform tech holdings.

Specifically, the filing doesn't show a complete liquidation of these positions. Some stocks still have small buy records. This "big sell, small buy" structure suggests active shrinking of exposure rather than a complete exit.

Also appearing on the large sell-off list is the Vanguard Dividend Appreciation ETF, a dividend-style ETF. This suggests the capital rotation isn't just flowing out of old tech giants but also includes some defensive, stable assets.

This is crucial. If it were just selling Microsoft, Amazon, and Meta to buy another batch of tech stocks, it would merely be sector rotation within tech. However, if even defensive ETFs are being reduced, it indicates the portfolio's overall risk appetite may be increasing, with capital shifting from stable, legacy platform assets towards more offensive industrial directions.

So, where did the money go?

The answer is clear: semiconductors, AI hardware, enterprise software, consumer electronics, broad-market indices, and some bonds and preferred stocks.

2. From Chips to Servers to Enterprise Software: Systematic Coverage of the AI Infrastructure Chain

Buying only Nvidia would be simply betting on the AI computing leader. However, what's more notable in this disclosure is that Trump-related accounts didn't buy a single name; they bought the entire AI infrastructure chain.

Layer one is semiconductors. Nvidia, Broadcom, Texas Instruments, Intel, AMD, Micron, and Marvell all appear on the buy or increase list. This includes GPUs and CPUs, analog chips, storage, and interconnects. It covers the strongest commercial AI computing leader and the most policy-sensitive representative of U.S. domestic manufacturing. It's a full-chain coverage.

Nvidia and Broadcom need little explanation. The former is the core AI computing play. The latter benefits from trends in custom chips, networking chips, and the hyperscalers' in-house chip development. AMD represents the alternative narrative for GPU and data center computing. Micron corresponds to storage demand, and Marvell to interconnects, custom chips, and high-speed data transmission.

More interestingly, Synopsys and Cadence are also on the buy list. These companies provide EDA tools, i.e., chip design software. Ordinary investors might not think of them first, but in the semiconductor value chain, they are the critical "picks and shovels" at the very upstream. Almost every complex chip, from design to tape-out, depends on these tools. This further confirms the rotation isn't just chasing the hottest AI leaders but extends upstream to the foundational tools of the semiconductor chain.

Layer two is AI hardware and servers, with Dell being the most sensitive and discussed name. The filing shows Trump-related accounts opened a $1 million to $5 million position in DELL on February 10th. Months later, Trump publicly endorsed Dell's hardware products. Subsequently, Dell secured large government-related contracts, and its stock price strengthened significantly.

This timeline is sensitive precisely because it shows: account purchase, followed by public backing, followed by government procurement and stock price appreciation. Strictly speaking, the disclosure alone doesn't prove a causal link between the trade, public statements, and subsequent contracts. However, from a market observation perspective, such trades naturally attract attention as they hit highly sensitive nodes: AI hardware, government procurement, and presidential public statements.

Intel presents another type of sensitivity. Unlike Dell, Intel's core logic is not just commercial but also political. The U.S. government had already decided on a major equity investment in Intel, and Intel has been a core asset in the narrative of U.S. semiconductor domestic manufacturing, supply chain security, and industrial policy (see related article: "Intel at the 'Lifeline' Moment: Can Lip-Bu Tan Liquidate the Legacy and Save It?"). Against this backdrop, Trump-related accounts buying INTC multiple times in Q1 naturally attracts amplified market interpretation.

Nvidia represents the commercial winner in AI computing, while Intel represents the domestic manufacturing base the U.S. government wants to support. Their logics differ but point in the same direction: AI infrastructure is no longer just a market theme; it's becoming a direction propelled by both industrial policy and fiscal resources.

Layer three is enterprise software. Oracle, ServiceNow, Adobe, and Workday all appear on the buy list. Unlike Nvidia, Dell, or Intel, these companies don't provide computing power or hardware. Instead, they embed AI directly into enterprise workflows. Oracle corresponds to databases and cloud infrastructure, ServiceNow to enterprise process automation, Adobe to creative and marketing productivity, and Workday to HR and financial management systems.

The logic here is clear: AI can't ultimately remain only in models and chatbots. It needs to enter real enterprise budgets, daily operations like office work, customer service, marketing, finance, HR, development, and data analysis. Ultimately, the biggest advantage of enterprise software companies is that they are already embedded in customer workflows. Once AI features become a default capability of these software suites, the impact isn't just a new story; it could change renewal rates, pricing power, module upgrades, and customer stickiness (see related article: "The 'Repair' Myth of Software Stocks: After the Rebound, Is AI Agent a Killer or a Savior?").

Therefore, what's truly noteworthy in this disclosure isn't just which AI hardware companies were bought, but also that the AI transformation of enterprise software is becoming another important clue.

Layer four is consumer electronics. Apple received a significant increase in holdings, with multiple additional purchases. Compared to pure AI chips or enterprise software, Apple represents the AI end-device gateway. Whether it can successfully realize an AI device cycle is still debated in the market. However, within a portfolio covering AI infrastructure and applications, Apple is an unavoidable super gateway.

Layer five includes broad-market indices like S&P 500 ETFs, Russell 1000 ETFs, and QQQ, which also appear on the large buy list. This suggests the accounts aren't completely detached from the broader market, making a unilateral bet on one theme. Instead, they are maintaining overall exposure to U.S. equities while actively increasing allocation to AI infrastructure and key industrial chains.

The filing also includes numerous bond trades, including municipal bonds, corporate bonds, high-yield bond ETFs, and bank preferred stocks. The municipal bonds cover multiple states, while the corporate bonds include issuers like Netflix, Occidental, and CoreWeave.

Thus, from a portfolio perspective, we can derive a clear investment self-portrait: on one hand, using broad-market indices, bonds, and preferred stocks to maintain a base and liquidity; on the other hand, using semiconductors, servers, enterprise software, and AI infrastructure names to enhance offensive characteristics.

3. Can You Copy This Playbook?

Seeing such disclosures, many people's first reaction is whether they can follow the trades.

However, directly copying the trades offers little practical value for several simple reasons:

- First, OGE disclosures have a time lag. By the time ordinary investors see the filing, the trades have already occurred.

- Second, the disclosed amounts are ranges, not precise figures. For example, $1 million to $5 million, or $5 million to $25 million, leaves a huge gap, making it difficult to gauge the true position weight.

- Third, the related accounts might be independently managed by third-party institutions. Outsiders don't know if each trade results from active judgment, portfolio rebalancing, or a model-driven allocation.

Therefore, this disclosure is not suitable as a short-term trading signal.

Its real value lies in showing a broader directional change. That is, the most astute "smart money" is moving from legacy platform tech and some defensive assets towards the AI infrastructure supply side. Specifically, from the core assets of the previous internet cycle—advertising, e-commerce, traditional cloud services—towards chips, servers, storage, interconnects, domestic manufacturing, and the AI transformation of enterprise software.

This direction also overlaps with current U.S. policy priorities.

After all, domestic semiconductor manufacturing, supply chain security, AI infrastructure, government procurement, and enterprise digitalization are not just market stories. They are directions propelled by policy, fiscal resources, industry, and capital collectively. Especially for names like Intel, its significance extends beyond earnings elasticity; it represents America's desire to regain initiative in advanced manufacturing and chip supply chains.

This is the most compelling aspect of Trump-related accounts increasing their Intel holdings. It doesn't necessarily mean Intel is the best chip stock, but it indicates that within the AI infrastructure narrative, the market is currently favoring those positioned at the epicenter of policy resources. Similarly, the Dell case illustrates that AI infrastructure isn't just about GPUs. Servers, hardware, government procurement, and enterprise deployment all become part of translating AI capital expenditure into real-world outcomes.

So, for ordinary investors, the real takeaway from this disclosure isn't a specific stock, but three structural clues.

- AI trading is moving from models and applications to infrastructure: Previously, buying AI was more about betting on large model potential and computing power expectations. Now, capital is increasingly focusing on who provides the chips, servers, storage, networking, packaging, design tools, and enterprise software.

- Semiconductors are no longer just about Nvidia: Nvidia remains the core name, but this disclosure shows capital also covering chain nodes like Broadcom, AMD, Micron, Marvell, Intel, Synopsys, and Cadence. As AI infrastructure deepens, it becomes less about a single leader and more about the repricing of the entire supply chain.

- The AI transformation of enterprise software might be the most easily underestimated piece: Hardware builds the computing power; enterprise software puts AI to use. The value of companies like Oracle, ServiceNow, Adobe, and Workday isn't about telling a brand-new AI story, but their ability to embed AI into existing workflows and convert it into revenue through customer stickiness and product upgrades.

As for the large sell-offs in Microsoft, Amazon, and Meta, it's also too simplistic to interpret this as "these stocks are set to fall." More accurately, it's a signal of capital reallocation. When legacy platform giants have already appreciated significantly, capital naturally begins seeking assets closer to the next wave of capital expenditure, closer to policy support, and closer to infrastructure buildout.

Regardless, the era dividend of the consumer internet hasn't disappeared. However, AI infrastructure, semiconductor localization, and enterprise software AI transformation are indeed accelerating as the main themes capital prefers to chase in the next phase.

This is precisely what makes the Q1 portfolio disclosure of the world's most powerful individual most worthy of attention.